Key Insights

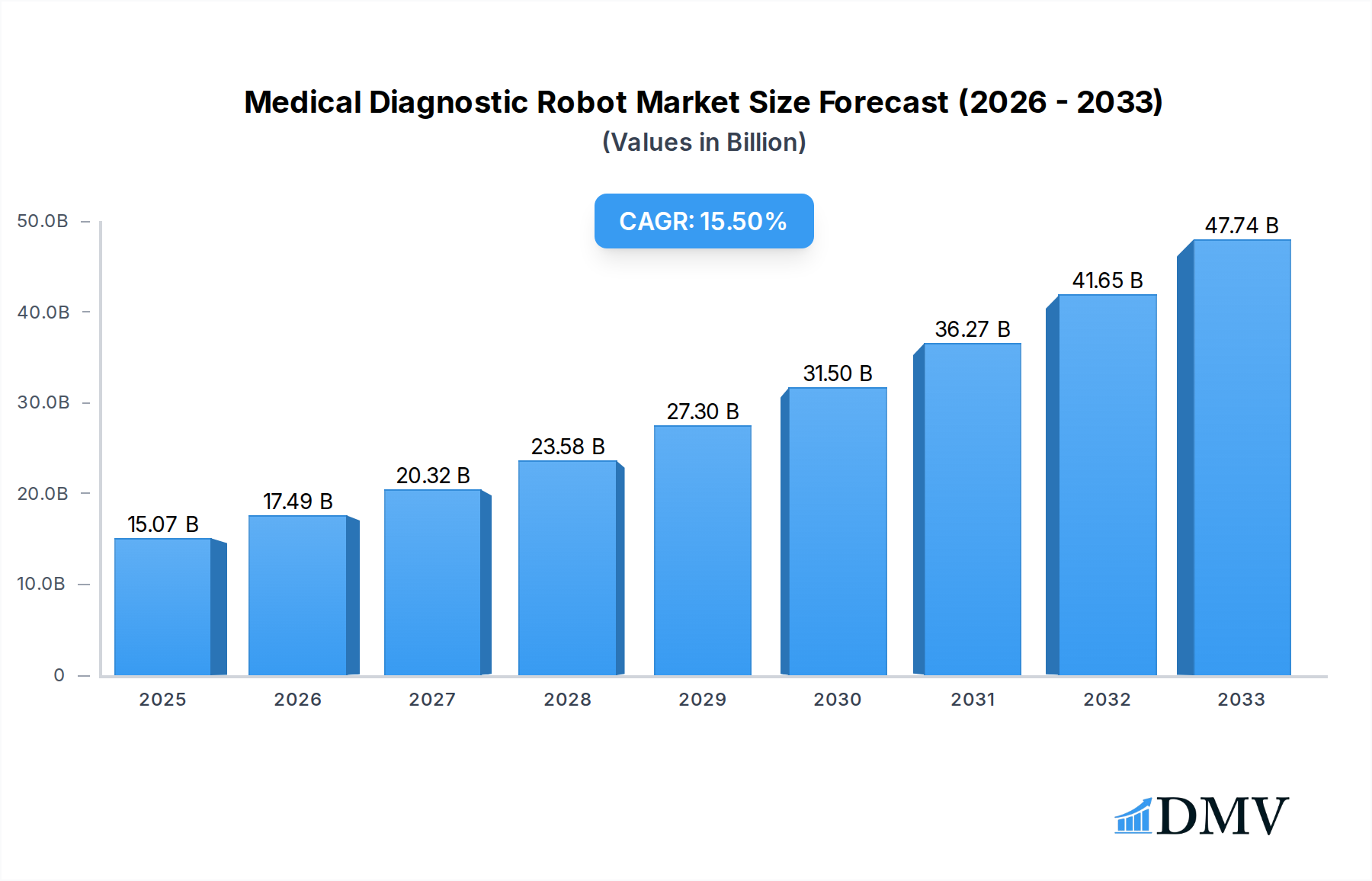

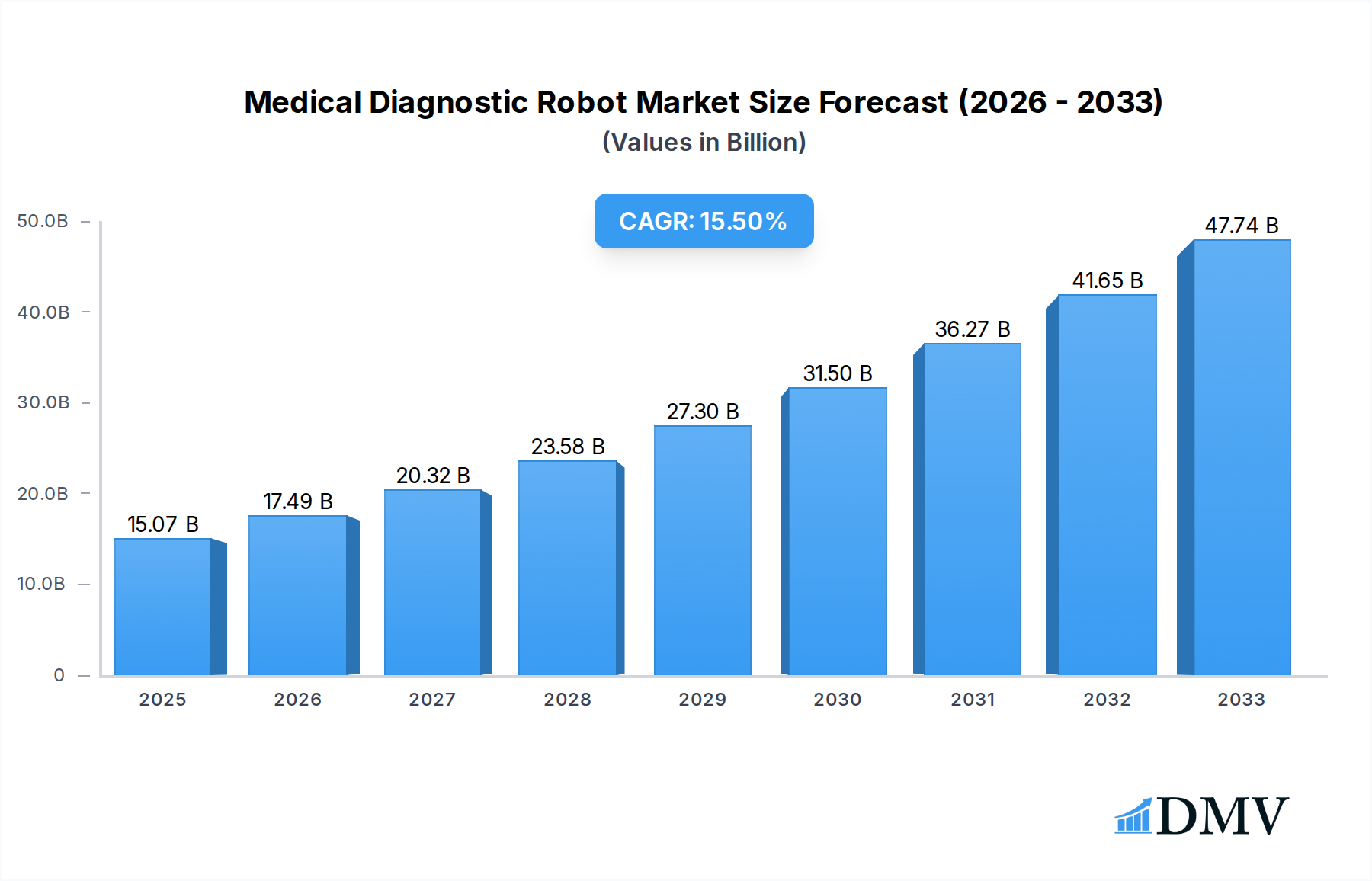

The global Medical Diagnostic Robot market is poised for exceptional growth, projected to reach an impressive $15.07 billion by 2025. This surge is driven by a confluence of technological advancements and the increasing demand for accurate and efficient diagnostic solutions in healthcare. The market is expected to expand at a robust CAGR of 16.1% through the forecast period, signaling a transformative era for medical diagnostics. Key drivers fueling this expansion include the rising prevalence of chronic diseases, necessitating earlier and more precise diagnostic interventions, and the growing adoption of artificial intelligence and machine learning in healthcare, which are enhancing the capabilities of diagnostic robots. Furthermore, the push for improved patient outcomes and reduced healthcare costs is accelerating the integration of these sophisticated robotic systems. The market is segmenting into distinct applications within Hospitals and Clinics, underscoring the broad utility of these technologies across various healthcare settings.

Medical Diagnostic Robot Market Size (In Billion)

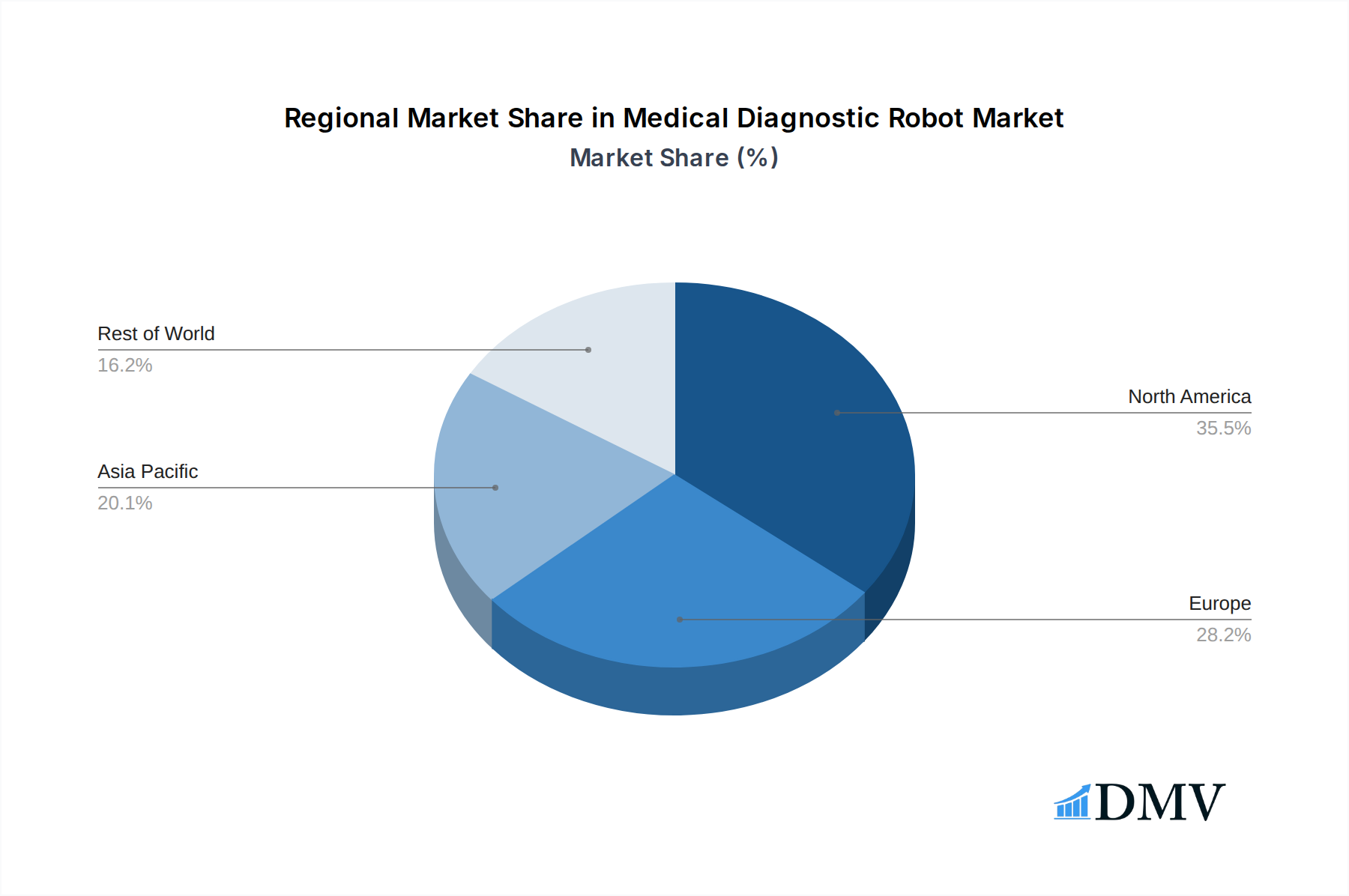

The evolution of diagnostic robotics is also characterized by the emergence of diverse robot types, ranging from External Large Robots designed for sophisticated imaging and analysis to Miniature In Vivo Robots promising minimally invasive diagnostic procedures. This innovation spectrum caters to a wide array of medical needs. While the market is set for substantial growth, potential restraints such as high initial investment costs for advanced robotic systems and the need for specialized training for healthcare professionals may present challenges. However, ongoing research and development, coupled with strategic collaborations among key industry players like Stryker Corporation, Intuitive Surgical, and Medtronic, are expected to mitigate these hurdles. Regional dynamics indicate strong market presence in North America and Europe, with the Asia Pacific region showing immense potential for rapid growth, driven by increasing healthcare expenditure and technological adoption in emerging economies like China and India.

Medical Diagnostic Robot Company Market Share

Medical Diagnostic Robot Market Composition & Trends

This comprehensive report delves into the intricate medical diagnostic robot market, examining its composition, current trends, and future trajectory from 2019 to 2033. The market exhibits a high degree of innovation, driven by relentless technological advancements and a growing demand for precision medicine and remote healthcare solutions. Regulatory landscapes are evolving to accommodate these sophisticated technologies, with bodies like the FDA and EMA actively involved in shaping approval pathways. Substitute products, primarily traditional diagnostic methods and AI-powered software without robotic integration, are present but facing increasing competition from the superior accuracy and efficiency of diagnostic robots. End-user profiles span a wide spectrum, from large hospital networks seeking to optimize patient throughput to specialized clinics focusing on niche diagnostic services. Mergers and acquisitions (M&A) are a significant catalyst for market consolidation and innovation, with deal values estimated to reach billions of dollars. For instance, recent M&A activities in the surgical robotics sector by companies like Stryker Corporation and Intuitive Surgical highlight the strategic importance of acquiring advanced robotic capabilities. The market share distribution, though dynamic, is increasingly influenced by companies demonstrating superior robotic surgical systems and AI-driven diagnostic platforms. The overall market concentration is expected to shift as new players emerge and established entities expand their product portfolios. The influence of key players like Medtronic and Johnson & Johnson in driving market growth is substantial. We anticipate a substantial increase in M&A values as companies vie for market leadership in this rapidly expanding field. The total value of M&A deals is projected to exceed $50 billion within the forecast period.

- Market Share Distribution: While precise figures vary, key players like Intuitive Surgical hold a significant share, with others like Stryker Corporation and Medtronic rapidly expanding their presence.

- Innovation Catalysts: Advancements in AI, machine learning, miniaturization, and sensor technology are primary drivers.

- Regulatory Landscapes: Evolving guidelines from bodies like the FDA, EMA, and other national health authorities are crucial for market access.

- Substitute Products: Traditional diagnostic tools, AI-based software for image analysis, and less sophisticated automated systems.

- End-User Profiles: Large hospitals, specialized clinics, research institutions, and increasingly, home healthcare providers.

- M&A Activities: Strategic acquisitions of innovative startups and companies with complementary technologies to enhance product offerings and market reach. Deal values are expected to climb significantly, exceeding $50 billion.

Medical Diagnostic Robot Industry Evolution

The medical diagnostic robot industry is undergoing a profound transformation, marked by accelerated market growth trajectories, groundbreaking technological advancements, and a significant shift in consumer demands towards more personalized and accessible healthcare. The historical period of 2019-2024 witnessed a steady but discernible rise in the adoption of diagnostic robots, particularly in areas like pathology and radiology. This period saw initial investments in research and development, laying the groundwork for the sophisticated systems we see today. The base year of 2025 marks a pivotal point, with the market poised for exponential expansion, driven by enhanced AI capabilities and increasing clinical validation. Growth rates during the historical period hovered around 10-15% annually, a figure projected to escalate to over 25% in the forecast period of 2025-2033.

Technological advancements have been the primary engine of this evolution. The integration of artificial intelligence (AI) and machine learning (ML) algorithms has revolutionized diagnostic accuracy, enabling robots to identify subtle patterns in medical imaging and biological samples that might elude human observation. Innovations in miniaturization have paved the way for miniature in vivo robots, capable of performing internal diagnostics and targeted interventions with unprecedented precision, thereby reducing invasiveness and improving patient outcomes. Concurrently, the development of external large robots has enhanced efficiency in high-throughput diagnostic laboratories, automating tasks such as sample preparation and analysis.

Shifting consumer demands are also playing a crucial role. Patients are increasingly seeking faster, more accurate, and less invasive diagnostic procedures. The growing acceptance of telehealth and remote patient monitoring further fuels the demand for robotic systems that can facilitate remote diagnostics and consultations. This paradigm shift necessitates a greater emphasis on user-friendly interfaces and seamless integration with existing healthcare IT infrastructure. Companies like Cyberdyne, with its pioneering work in cybernetic medical devices, and Globus, focusing on robotic solutions for spine surgery, are at the forefront of this evolution, demonstrating a commitment to pushing the boundaries of medical robotics. The adoption metrics, which measure the penetration of diagnostic robots across various healthcare settings, are expected to see a significant surge. For instance, the adoption rate in hospitals is projected to increase from approximately 30% in 2024 to over 70% by 2033. This upward trend is supported by substantial investments from both public and private sectors, aiming to improve healthcare accessibility and quality. The global market size, which stood at approximately $5 billion in 2024, is forecasted to reach over $40 billion by 2033, underscoring the immense growth potential of this industry. The continuous drive for improved diagnostic accuracy, reduced procedural times, and enhanced patient safety are key determinants of this impressive growth trajectory.

Leading Regions, Countries, or Segments in Medical Diagnostic Robot

The medical diagnostic robot market is experiencing concentrated growth and innovation across specific regions and application segments, driven by a confluence of factors including robust healthcare infrastructure, significant investment in R&D, and supportive regulatory environments. Among the applications, Hospitals emerge as the dominant segment, accounting for an estimated 70% of the total market share in 2025. This dominance is attributed to the inherent need for advanced diagnostic capabilities within hospital settings to manage a high volume of diverse patient cases, perform complex procedures, and facilitate cutting-edge medical research. The ability of diagnostic robots to improve diagnostic accuracy, reduce turnaround times for critical tests, and enhance operational efficiency makes them indispensable assets for modern healthcare facilities.

In terms of geographical leadership, North America, particularly the United States, stands out as the leading region. This is underpinned by several key drivers. Firstly, substantial government and private sector investment in healthcare technology, including billions allocated to research and development in robotics and AI, fuels innovation and adoption. Secondly, a well-established regulatory framework, albeit stringent, provides clear pathways for the approval and deployment of advanced medical devices. Companies like Johnson & Johnson and Stryker Corporation, with their strong presence and extensive product portfolios, actively contribute to the market's dynamism in this region. The presence of leading research institutions and a highly skilled workforce also plays a pivotal role in driving technological advancements.

Delving deeper into the types of diagnostic robots, the External Large Robot segment is currently leading, driven by its widespread application in automated laboratory diagnostics, robotic surgery assistance, and imaging analysis. These robots are crucial for high-throughput screening and complex procedures, offering unparalleled precision and consistency. For instance, robots used in pathology labs for sample processing and analysis are transforming the speed and accuracy of disease detection. The demand for these robots is projected to continue its upward trajectory, reaching billions in market value by 2033. The growing emphasis on early disease detection and personalized treatment plans further propels the adoption of these sophisticated external systems.

Conversely, the Miniature in Vivo Robot segment, while still in its nascent stages, presents the most significant future growth potential, with its market size projected to experience a compound annual growth rate exceeding 30% from 2025 to 2033. These microscopic robots are poised to revolutionize internal diagnostics, offering minimally invasive procedures for targeted biopsies, drug delivery, and internal imaging. Early-stage research and development efforts by companies like Cyberdyne are indicative of the transformative impact these robots will have on treating conditions previously requiring extensive surgery. The ability of these tiny machines to navigate the human body, perform intricate tasks, and transmit real-time data opens up unprecedented possibilities in interventional medicine, with potential market impacts running into billions.

- Dominant Application Segment: Hospitals, accounting for approximately 70% of the market share in 2025, due to their need for high-throughput diagnostics and complex procedures.

- Leading Geographical Region: North America, specifically the United States, driven by substantial investment, a favorable regulatory environment, and a strong R&D ecosystem.

- Leading Robot Type: External Large Robots, owing to their established applications in laboratory automation, surgical assistance, and imaging analysis.

- High-Growth Robot Type: Miniature in Vivo Robots, with projected growth rates exceeding 30% annually, promising revolutionary internal diagnostic capabilities.

- Key Drivers in Hospitals: Enhanced diagnostic accuracy, reduced turnaround times, operational efficiency, and capacity for complex procedures.

- Investment Trends: Billions of dollars are being invested in healthcare technology and robotics R&D, particularly in North America.

- Regulatory Support: While stringent, regulatory frameworks in leading regions facilitate market entry for validated technologies.

Medical Diagnostic Robot Product Innovations

The medical diagnostic robot landscape is characterized by a rapid pace of product innovation, transforming healthcare delivery with enhanced capabilities and improved patient outcomes. Key advancements include the development of AI-powered robotic platforms capable of analyzing vast datasets from medical imaging, genetic sequencing, and patient records to identify diseases with remarkable accuracy, often surpassing human capabilities. For example, robots equipped with sophisticated computer vision algorithms are now adept at detecting subtle anomalies in mammograms and CT scans, leading to earlier cancer detection. Furthermore, miniaturization technologies are enabling the creation of miniature in vivo robots designed for minimally invasive internal diagnostics, capable of navigating the bloodstream or digestive tract to perform biopsies or deliver targeted therapies with pinpoint precision. These innovations offer unique selling propositions such as reduced invasiveness, faster recovery times, and the potential for personalized diagnostics.

Propelling Factors for Medical Diagnostic Robot Growth

The medical diagnostic robot market is experiencing robust growth propelled by a confluence of potent factors. Technological advancements, particularly in artificial intelligence (AI), machine learning, and miniaturization, are at the forefront, enabling more accurate, faster, and less invasive diagnostic procedures. For instance, AI algorithms can analyze medical images with unparalleled speed and precision, identifying subtle indicators of disease. Economic factors, including increasing healthcare expenditure globally and the growing demand for efficient, cost-effective healthcare solutions, also play a significant role. As populations age and the prevalence of chronic diseases rises, the need for advanced diagnostic tools that can handle high volumes of cases becomes paramount. Regulatory bodies are increasingly streamlining approval processes for innovative medical devices, further incentivizing market growth.

Obstacles in the Medical Diagnostic Robot Market

Despite its immense potential, the medical diagnostic robot market faces several considerable obstacles. High initial investment costs for sophisticated robotic systems can be a significant barrier, particularly for smaller healthcare facilities and clinics. Stringent and evolving regulatory approval processes, while essential for patient safety, can also lead to lengthy development cycles and increased costs. Furthermore, the integration of these complex systems into existing hospital IT infrastructure and workflows presents technical challenges. Public and professional acceptance, requiring extensive training and addressing concerns about job displacement, also needs careful management. The reliance on a global supply chain for specialized components can also lead to disruptions, as witnessed during recent geopolitical events, impacting production and delivery timelines.

Future Opportunities in Medical Diagnostic Robot

The future of the medical diagnostic robot market is brimming with exciting opportunities. The continued advancement of AI and machine learning promises even more sophisticated diagnostic capabilities, enabling personalized medicine at an unprecedented scale. The development of miniature in vivo robots for internal diagnostics and targeted therapies represents a paradigm shift in minimally invasive healthcare, with potential market impacts reaching billions. Expansion into emerging economies with growing healthcare needs and increasing disposable incomes presents a significant untapped market. Furthermore, the integration of diagnostic robots into home healthcare settings, facilitated by advancements in remote monitoring and telehealth, opens up new avenues for accessible and convenient patient care.

Major Players in the Medical Diagnostic Robot Ecosystem

- Stryker Corporation

- Intuitive Surgical

- Medtronic

- Cyberdyne

- Globus

- HollySys

- iRobot

- Johnson & Johnson

- Omron

- Hitachi

- Zora Bots

- Babylon Health

- Ada Health

- Iflytek

- OrionStar

- KUKA

Key Developments in Medical Diagnostic Robot Industry

- 2023: Launch of advanced AI-powered imaging analysis software by Hitachi, enhancing diagnostic accuracy for neurological disorders.

- 2023: Stryker Corporation acquires a leading robotics startup, expanding its surgical robotics portfolio.

- 2024: Intuitive Surgical announces breakthroughs in miniaturized robotic instruments for minimally invasive procedures.

- 2024: Medtronic receives FDA approval for a new generation of diagnostic robots for cardiac monitoring.

- 2024: Cyberdyne demonstrates promising results in clinical trials for its diagnostic cybernetic limbs.

- 2025: HollySys partners with a major hospital network to deploy diagnostic robots across multiple departments.

- 2025: iRobot showcases prototype diagnostic robots for elder care and remote health monitoring.

- 2026: Johnson & Johnson invests billions in a consortium focused on AI-driven precision diagnostics.

- 2027: Omron announces the development of compact diagnostic robots for point-of-care testing.

- 2028: Zora Bots develops specialized diagnostic robots for pediatric care.

- 2029: Babylon Health integrates AI-driven diagnostic capabilities into its telehealth platform.

- 2030: Ada Health expands its AI diagnostic offerings to include complex genetic analysis.

- 2031: Iflytek develops advanced voice-enabled diagnostic robots for remote consultations.

- 2032: OrionStar unveils intelligent robots for automated lab sample processing.

- 2033: KUKA collaborates with medical institutions on the next generation of surgical and diagnostic robots.

Strategic Medical Diagnostic Robot Market Forecast

The strategic forecast for the medical diagnostic robot market indicates a future characterized by rapid expansion and transformative innovation. Growth will be fueled by ongoing technological breakthroughs, particularly in AI and robotics, which will enable more precise and personalized diagnostics. The increasing adoption of external large robots in hospitals and the burgeoning potential of miniature in vivo robots for internal procedures are key growth catalysts. Economic drivers, including rising healthcare expenditures and the demand for efficient healthcare, coupled with supportive regulatory frameworks, will further propel market penetration. Emerging opportunities in untapped markets and the integration of diagnostic robots into telehealth and home healthcare settings promise to unlock significant future market potential, with overall market value projected to reach billions.

Medical Diagnostic Robot Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Clinics

-

2. Types

- 2.1. External Large Robot

- 2.2. Miniature in Vivo Robot

Medical Diagnostic Robot Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Diagnostic Robot Regional Market Share

Geographic Coverage of Medical Diagnostic Robot

Medical Diagnostic Robot REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Diagnostic Robot Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Clinics

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. External Large Robot

- 5.2.2. Miniature in Vivo Robot

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical Diagnostic Robot Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Clinics

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. External Large Robot

- 6.2.2. Miniature in Vivo Robot

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical Diagnostic Robot Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Clinics

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. External Large Robot

- 7.2.2. Miniature in Vivo Robot

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical Diagnostic Robot Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Clinics

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. External Large Robot

- 8.2.2. Miniature in Vivo Robot

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical Diagnostic Robot Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Clinics

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. External Large Robot

- 9.2.2. Miniature in Vivo Robot

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical Diagnostic Robot Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Clinics

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. External Large Robot

- 10.2.2. Miniature in Vivo Robot

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Stryker Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Intuitive Surgical

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Medtronic

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Cyberdyne

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Globus

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 HollySys

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 iRobot

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Johnson & Johnson

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Omron

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Hitachi

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Zora Bots

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Babylon Health

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Ada Health

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Iflytek

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 OrionStar

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 KUKA

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Stryker Corporation

List of Figures

- Figure 1: Global Medical Diagnostic Robot Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Medical Diagnostic Robot Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Medical Diagnostic Robot Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Diagnostic Robot Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Medical Diagnostic Robot Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Medical Diagnostic Robot Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Medical Diagnostic Robot Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Diagnostic Robot Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Medical Diagnostic Robot Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Diagnostic Robot Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Medical Diagnostic Robot Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Medical Diagnostic Robot Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Medical Diagnostic Robot Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Diagnostic Robot Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Medical Diagnostic Robot Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Diagnostic Robot Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Medical Diagnostic Robot Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Medical Diagnostic Robot Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Medical Diagnostic Robot Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Diagnostic Robot Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Diagnostic Robot Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Diagnostic Robot Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Medical Diagnostic Robot Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Medical Diagnostic Robot Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Diagnostic Robot Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Diagnostic Robot Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Diagnostic Robot Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Diagnostic Robot Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Medical Diagnostic Robot Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Medical Diagnostic Robot Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Diagnostic Robot Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Diagnostic Robot Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Medical Diagnostic Robot Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Medical Diagnostic Robot Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Medical Diagnostic Robot Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Medical Diagnostic Robot Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Medical Diagnostic Robot Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Diagnostic Robot Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Medical Diagnostic Robot Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Medical Diagnostic Robot Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Diagnostic Robot Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Medical Diagnostic Robot Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Medical Diagnostic Robot Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Diagnostic Robot Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Medical Diagnostic Robot Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Medical Diagnostic Robot Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Diagnostic Robot Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Medical Diagnostic Robot Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Medical Diagnostic Robot Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Diagnostic Robot Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Diagnostic Robot?

The projected CAGR is approximately 16.1%.

2. Which companies are prominent players in the Medical Diagnostic Robot?

Key companies in the market include Stryker Corporation, Intuitive Surgical, Medtronic, Cyberdyne, Globus, HollySys, iRobot, Johnson & Johnson, Omron, Hitachi, Zora Bots, Babylon Health, Ada Health, Iflytek, OrionStar, KUKA.

3. What are the main segments of the Medical Diagnostic Robot?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Diagnostic Robot," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Diagnostic Robot report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Diagnostic Robot?

To stay informed about further developments, trends, and reports in the Medical Diagnostic Robot, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence