Key Insights

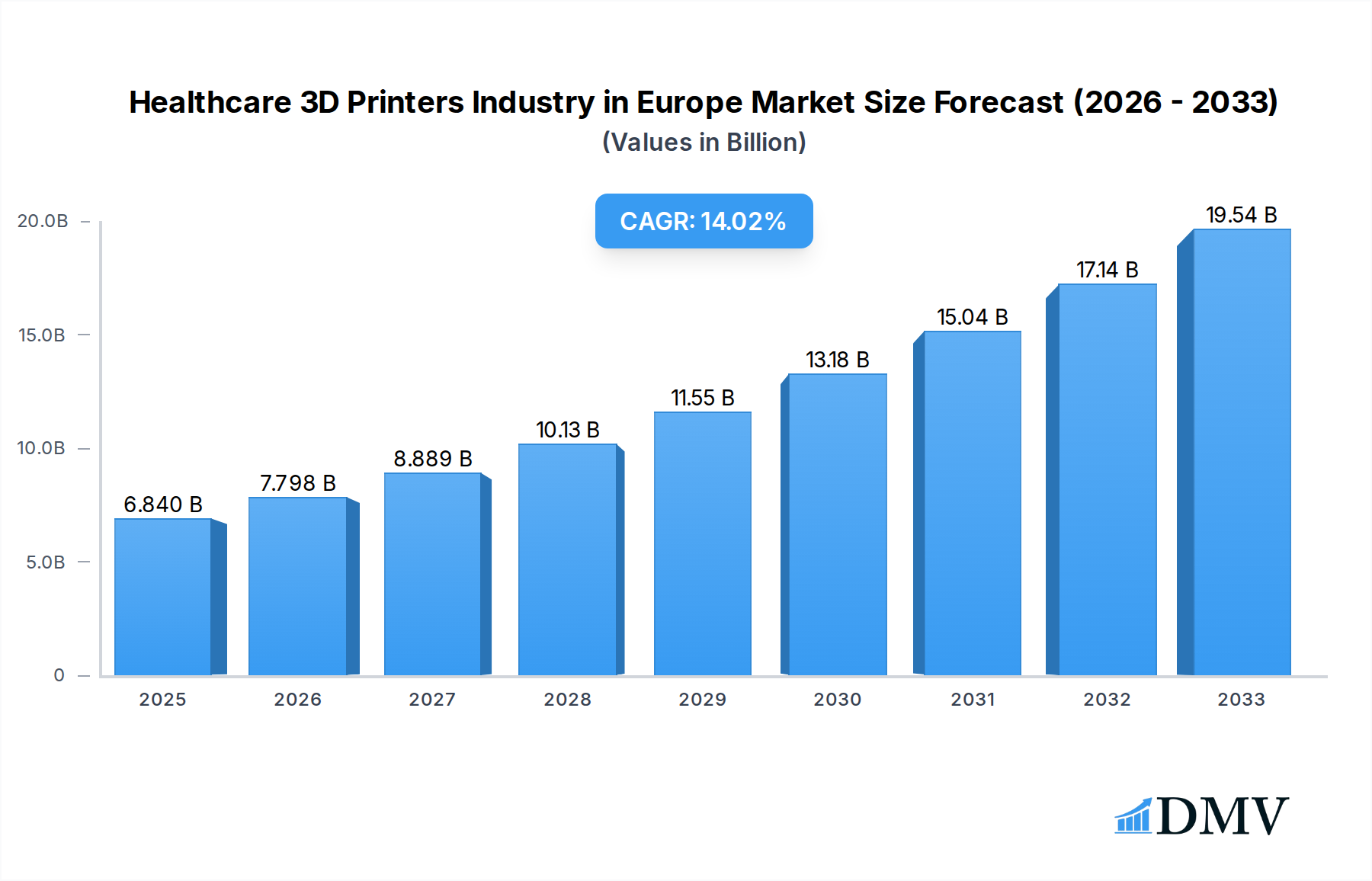

The European market for healthcare 3D printers is poised for substantial expansion, projected to reach an estimated USD 6.84 billion in 2025. This growth is propelled by a robust compound annual growth rate (CAGR) of 14% throughout the forecast period of 2025-2033. The increasing adoption of additive manufacturing in critical healthcare applications like bioprinting, custom implants, and advanced prosthetics is a primary driver. Technological advancements, particularly in areas such as Stereolithography, Electron Beam Melting, and Jetting Technology, are enabling the creation of highly precise and complex medical devices and models. Furthermore, the development of novel biocompatible materials, including advanced polymers, ceramics, and specialized metal alloys, is expanding the scope and efficacy of 3D printing in medical treatments. This combination of technological innovation and material science breakthroughs is fundamentally transforming patient care and driving market demand across Europe.

Healthcare 3D Printers Industry in Europe Market Size (In Billion)

The European healthcare 3D printing landscape is characterized by strong innovation and a growing focus on personalized medicine. Key industry players like Envision TEC GmbH, Renishaw PLC, and General Electric (Arcam AB) are continuously investing in research and development to enhance printer capabilities and material offerings. The market is segmented across various technologies and applications, with bioprinting and implants showing particularly high growth potential due to their direct impact on patient outcomes and the increasing demand for patient-specific solutions. While the market enjoys strong growth drivers, potential restraints such as the high initial investment costs for advanced 3D printing systems and the need for specialized expertise in operating and maintaining these technologies may pose challenges. However, ongoing regulatory support and a growing understanding of the long-term cost-effectiveness of 3D printed medical solutions are expected to mitigate these concerns and foster sustained market growth across all European regions.

Healthcare 3D Printers Industry in Europe Company Market Share

This comprehensive report offers an in-depth analysis of the burgeoning European Healthcare 3D Printers Industry, providing critical market insights and strategic foresight. Covering the period from 2019 to 2033, with a base year of 2025 and a detailed forecast period of 2025–2033, this research is designed to empower stakeholders, including manufacturers, investors, researchers, and healthcare providers, with actionable intelligence. We delve into market composition, industry evolution, regional dynamics, product innovations, growth drivers, obstacles, and future opportunities, all while highlighting the key players and significant developments shaping this transformative sector. The European additive manufacturing market for healthcare is poised for substantial expansion, driven by increasing demand for personalized medicine, advanced prosthetics, and intricate surgical implants.

Healthcare 3D Printers Industry in Europe Market Composition & Trends

The European Healthcare 3D Printers Industry exhibits a dynamic market concentration, with a blend of established industry giants and innovative startups driving technological advancements and application expansion. Innovation catalysts are numerous, ranging from breakthroughs in biomaterials and advanced printer hardware to sophisticated software solutions for design and simulation. The regulatory landscape, while stringent, is gradually adapting to accommodate the unique challenges and opportunities presented by 3D printed medical devices, fostering a more supportive environment for adoption. Substitute products, primarily traditionally manufactured medical devices, face increasing competition from the superior customization and cost-effectiveness offered by 3D printing. End-user profiles are diverse, encompassing hospitals, surgical centers, dental clinics, orthopedic specialists, and academic research institutions, each leveraging 3D printing for distinct applications. Mergers and acquisitions (M&A) activities are a significant trend, with deal values in the billions of Euros, as larger players seek to consolidate market share, acquire novel technologies, and expand their product portfolios. Market share distribution is influenced by technological specialization and application focus, with segments like implants and prosthetics holding substantial portions. The market is characterized by a strong drive towards patient-specific solutions. The estimated market size for healthcare 3D printers in Europe is projected to reach over XX billion by 2033.

- Market Share Distribution: Dominated by leading technology providers and application-specific solutions.

- M&A Deal Values: Significant investment activity, with major acquisitions in the billions.

- Innovation Catalysts: Focus on material science, biocompatibility, and precision engineering.

- Regulatory Landscape: Evolving frameworks for medical device approval and quality control.

- End-User Profiles: Hospitals, clinics, research institutions, and specialist providers.

Healthcare 3D Printers Industry in Europe Industry Evolution

The European Healthcare 3D Printers Industry has witnessed remarkable evolution, marked by consistent market growth trajectories and rapid technological advancements. Over the historical period (2019–2024), the market experienced a compound annual growth rate (CAGR) of approximately XX%, fueled by increasing awareness of 3D printing’s capabilities in healthcare and a growing need for personalized medical solutions. Shifting consumer demands have played a pivotal role, with patients and clinicians alike favoring custom-fit prosthetics, implants, and anatomical models that enhance treatment outcomes and patient comfort. The adoption of 3D printing technology across various medical disciplines, from orthopedics and dentistry to complex surgical planning and bioprinting research, has accelerated significantly. Specifically, the demand for patient-specific implants, such as those for cranial reconstruction or joint replacement, has surged, driving innovation in metal and polymer printing technologies. Furthermore, the development of advanced bioprinting techniques holds immense promise for regenerative medicine and drug testing, attracting substantial research and development investments. The base year, 2025, saw the market value standing at approximately XX billion, with projections indicating a sustained and robust growth into the forecast period (2025–2033). This growth is underpinned by continuous improvements in printer resolution, speed, material versatility, and post-processing capabilities, making 3D printing an increasingly indispensable tool in the modern healthcare ecosystem. The industry's evolution is also characterized by a growing emphasis on workflow integration, enabling seamless transition from patient imaging to final device production. The market’s expansion is further bolstered by strategic partnerships between technology providers and healthcare institutions, fostering collaborative innovation and accelerating the translation of research into clinical applications. The increasing affordability of advanced 3D printing systems and materials is also democratizing access to these transformative technologies.

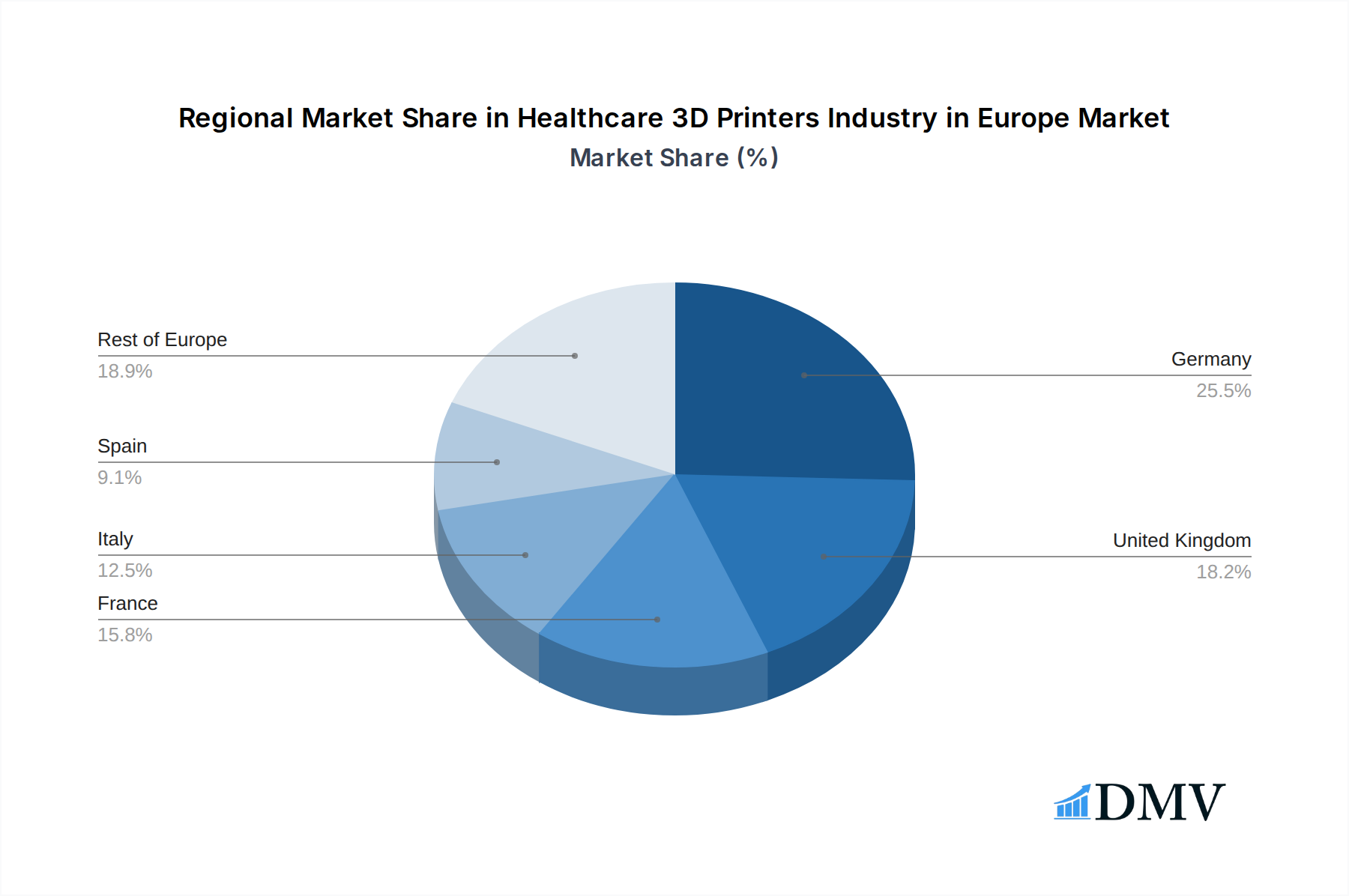

Leading Regions, Countries, or Segments in Healthcare 3D Printers Industry in Europe

Within the European Healthcare 3D Printers Industry, Germany emerges as a dominant country, driven by its robust industrial infrastructure, strong government support for research and development, and a significant presence of leading additive manufacturing companies. The country's advanced healthcare system and high adoption rate of innovative medical technologies contribute to its leading position. In terms of technology segments, Laser Sintering and Stereo Lithography are currently leading the market, owing to their high precision, material compatibility (especially for implants and dental applications), and established track records in medical device manufacturing. However, Jetting Technology is rapidly gaining traction, particularly for creating detailed anatomical models and surgical guides.

Dominant Technology Segment: Laser Sintering

- Key Drivers: Superior material properties for metal implants, high accuracy and repeatability, well-established for producing complex geometries.

- In-depth Analysis: Laser sintering, particularly Selective Laser Melting (SLM) and Electron Beam Melting (EBM) for metals, is crucial for producing biocompatible implants made from titanium alloys and stainless steel. These technologies enable the creation of porous structures for better osseointegration and patient-specific designs that enhance functional outcomes.

Dominant Application Segment: Implants

- Key Drivers: Growing demand for personalized orthopedic and dental implants, advancements in biocompatible materials, and increasing regulatory approvals.

- In-depth Analysis: The ability to fabricate patient-specific implants with intricate designs and optimal mechanical properties offers significant advantages over traditional manufacturing methods. This is driving substantial investment and innovation in this segment, with a projected market value exceeding XX billion by 2033.

Leading Material Segment: Metals and Alloys

- Key Drivers: Essential for orthopedic and dental implants, advancements in biocompatible metal powders, and high demand for durable and strong prosthetics.

- In-depth Analysis: Titanium alloys, cobalt-chrome, and stainless steel are paramount for producing load-bearing implants. The development of new metal alloys with improved biocompatibility and mechanical performance continues to fuel growth in this segment.

The strong performance of these segments is further amplified by substantial investment trends in R&D for novel applications and materials, coupled with favorable regulatory support for approved medical devices. The increasing prevalence of chronic diseases and an aging population also contribute to the sustained demand for advanced medical solutions.

Healthcare 3D Printers Industry in Europe Product Innovations

Product innovation in the European Healthcare 3D Printers Industry is characterized by a relentless pursuit of enhanced precision, speed, and biocompatibility. Companies are developing advanced 3D printers capable of fabricating intricate anatomical models with exceptional detail for pre-surgical planning, leading to improved patient outcomes and reduced operative risks. Innovations in materials science are yielding new biocompatible polymers, ceramics, and metal alloys, expanding the range of treatable conditions and device applications. Performance metrics are consistently improving, with faster printing speeds, higher resolution, and greater material tensile strength becoming standard. For instance, new printer models offer build volumes capable of producing larger implants and prosthetics with unparalleled accuracy. The development of multi-material printing capabilities allows for the creation of devices with integrated functionalities, such as flexible joints or varying material densities within a single print. These advancements are critical for the growing bioprinting sector, where the creation of functional tissues and organs is on the horizon.

Propelling Factors for Healthcare 3D Printers Industry in Europe Growth

The European Healthcare 3D Printers Industry's growth is propelled by several interconnected factors. Technologically, advancements in printer resolution, material science (biocompatible polymers, metals, and ceramics), and software for personalized design are fundamental. Economically, the increasing demand for cost-effective, patient-specific solutions, coupled with the potential for reduced healthcare expenditures through shorter recovery times and fewer revision surgeries, is a significant driver. Regulatory bodies are increasingly establishing frameworks for the approval of 3D printed medical devices, fostering confidence and wider adoption. The aging population and the rising incidence of chronic diseases necessitate advanced and personalized medical interventions, which 3D printing is uniquely positioned to provide. Furthermore, the growing emphasis on personalized medicine and the development of complex surgical techniques are creating a strong demand for customized anatomical models and implants.

- Technological Advancements: Enhanced printer precision, material development, and sophisticated design software.

- Economic Drivers: Cost-effectiveness of personalized devices, reduced healthcare spending.

- Regulatory Support: Evolving frameworks for device approval.

- Demographic Shifts: Aging population and increased prevalence of chronic diseases.

- Personalized Medicine: Demand for bespoke treatments and devices.

Obstacles in the Healthcare 3D Printers Industry in Europe Market

Despite robust growth, the European Healthcare 3D Printers Industry faces several obstacles. Regulatory hurdles remain a significant challenge, as the approval process for 3D printed medical devices can be lengthy and complex, varying across different European Union member states. Supply chain disruptions, particularly concerning the availability and consistent quality of specialized printing materials, can impact production schedules and costs. Furthermore, the initial high investment cost for advanced 3D printing systems and the need for specialized training for healthcare professionals can be a barrier for smaller institutions. Competitive pressures are intensifying as more players enter the market, potentially leading to price wars and margin erosion for some segments. The perception and acceptance of 3D printed medical devices among certain segments of the patient population and older medical practitioners can also present a challenge, requiring continued education and demonstration of efficacy.

- Regulatory Complexities: Varying approval processes across EU nations.

- Supply Chain Vulnerabilities: Material availability and quality control issues.

- High Initial Investment: Cost of advanced equipment and training.

- Market Competition: Increasing number of players and potential price pressures.

- Perception and Acceptance: Need for continued education and validation.

Future Opportunities in Healthcare 3D Printers Industry in Europe

The future opportunities in the European Healthcare 3D Printers Industry are vast and promising. The burgeoning field of bioprinting, with its potential for creating functional tissues and organs for transplantation and drug testing, represents a significant long-term growth area. The increasing adoption of 3D printing in dental applications, from crowns and bridges to clear aligners, will continue to expand. The development of advanced implantable sensors and smart prosthetics, integrating 3D printed components with electronic functionalities, offers new avenues for patient care. Furthermore, the expansion of point-of-care 3D printing within hospitals, enabling on-demand production of customized medical devices, presents a substantial opportunity for streamlining workflows and improving patient accessibility. The growing demand for personalized rehabilitation aids and wearable medical devices also opens new market segments.

- Bioprinting Advancement: Creation of tissues and organs.

- Dental Applications: Expansion in prosthetics and orthodontics.

- Smart Devices: Integration of sensors and electronics in implants.

- Point-of-Care Manufacturing: On-demand production in hospitals.

- Rehabilitation and Wearables: Growing market for personalized aids.

Major Players in the Healthcare 3D Printers Industry in Europe Ecosystem

- Envision TEC GmbH

- Renishaw PLC

- General Electric (Arcam AB)

- Nano 3D Biosciences Inc

- Eos GmbH

- Organovo Holding Inc

- 3D Systems Corporation

- Materialise NV

- Stratasys Ltd

- Oxford Performance Materials

Key Developments in Healthcare 3D Printers Industry in Europe Industry

- July 2022: Sculpteo and Daniel Robert Orthopedic launched a Bio-sourced 3D printed device, a collaboration aimed at producing orthopedic devices from a bio-sourced material, highlighting advancements in sustainable additive manufacturing for healthcare.

- June 2021: Stratasys launched the J5 MediJet Medical 3D printer, enabling the creation of highly detailed 3D anatomical models and drilling/cutting guides with approved third-party 510k-cleared segmentation software, significantly enhancing surgical planning and precision.

Strategic Healthcare 3D Printers Industry in Europe Market Forecast

The strategic forecast for the European Healthcare 3D Printers Industry indicates a period of sustained and robust growth, driven by ongoing technological innovations, increasing healthcare demands, and favorable market dynamics. The market is expected to witness significant expansion, fueled by the rising adoption of personalized medicine, the development of advanced biomaterials, and the increasing integration of 3D printing solutions across a wider range of medical applications, including intricate surgical implants and regenerative therapies. The continuous evolution of printer technologies, promising greater speed, accuracy, and material versatility, will further accelerate this growth. Strategic investments in research and development, coupled with supportive regulatory environments, will pave the way for groundbreaking advancements, particularly in the bioprinting sector and for smart medical devices. The forecast suggests a market value projected to reach over XX billion by 2033, underscoring the transformative impact of 3D printing on the European healthcare landscape.

Healthcare 3D Printers Industry in Europe Segmentation

-

1. Technology

- 1.1. Stereo Lithography

- 1.2. Deposition Modeling

- 1.3. Electron Beam Melting

- 1.4. Laser Sintering

- 1.5. Jetting Technology

- 1.6. Laminated Object Manufacturing

- 1.7. Other Technologies

-

2. Applications

- 2.1. Bioprinting

- 2.2. Implants

- 2.3. Prosthetics

- 2.4. Dentistry

- 2.5. Other Applications

-

3. Materials

- 3.1. Metals and Alloys

- 3.2. Polymers

- 3.3. Ceramics

- 3.4. Other Materials

Healthcare 3D Printers Industry in Europe Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

Healthcare 3D Printers Industry in Europe Regional Market Share

Geographic Coverage of Healthcare 3D Printers Industry in Europe

Healthcare 3D Printers Industry in Europe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Stereo Lithography

- 5.1.2. Deposition Modeling

- 5.1.3. Electron Beam Melting

- 5.1.4. Laser Sintering

- 5.1.5. Jetting Technology

- 5.1.6. Laminated Object Manufacturing

- 5.1.7. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by Applications

- 5.2.1. Bioprinting

- 5.2.2. Implants

- 5.2.3. Prosthetics

- 5.2.4. Dentistry

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Materials

- 5.3.1. Metals and Alloys

- 5.3.2. Polymers

- 5.3.3. Ceramics

- 5.3.4. Other Materials

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Germany

- 5.4.2. United Kingdom

- 5.4.3. France

- 5.4.4. Italy

- 5.4.5. Spain

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Healthcare 3D Printers Industry in Europe Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Stereo Lithography

- 6.1.2. Deposition Modeling

- 6.1.3. Electron Beam Melting

- 6.1.4. Laser Sintering

- 6.1.5. Jetting Technology

- 6.1.6. Laminated Object Manufacturing

- 6.1.7. Other Technologies

- 6.2. Market Analysis, Insights and Forecast - by Applications

- 6.2.1. Bioprinting

- 6.2.2. Implants

- 6.2.3. Prosthetics

- 6.2.4. Dentistry

- 6.2.5. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by Materials

- 6.3.1. Metals and Alloys

- 6.3.2. Polymers

- 6.3.3. Ceramics

- 6.3.4. Other Materials

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. Germany Healthcare 3D Printers Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. Stereo Lithography

- 7.1.2. Deposition Modeling

- 7.1.3. Electron Beam Melting

- 7.1.4. Laser Sintering

- 7.1.5. Jetting Technology

- 7.1.6. Laminated Object Manufacturing

- 7.1.7. Other Technologies

- 7.2. Market Analysis, Insights and Forecast - by Applications

- 7.2.1. Bioprinting

- 7.2.2. Implants

- 7.2.3. Prosthetics

- 7.2.4. Dentistry

- 7.2.5. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by Materials

- 7.3.1. Metals and Alloys

- 7.3.2. Polymers

- 7.3.3. Ceramics

- 7.3.4. Other Materials

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. United Kingdom Healthcare 3D Printers Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. Stereo Lithography

- 8.1.2. Deposition Modeling

- 8.1.3. Electron Beam Melting

- 8.1.4. Laser Sintering

- 8.1.5. Jetting Technology

- 8.1.6. Laminated Object Manufacturing

- 8.1.7. Other Technologies

- 8.2. Market Analysis, Insights and Forecast - by Applications

- 8.2.1. Bioprinting

- 8.2.2. Implants

- 8.2.3. Prosthetics

- 8.2.4. Dentistry

- 8.2.5. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by Materials

- 8.3.1. Metals and Alloys

- 8.3.2. Polymers

- 8.3.3. Ceramics

- 8.3.4. Other Materials

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. France Healthcare 3D Printers Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. Stereo Lithography

- 9.1.2. Deposition Modeling

- 9.1.3. Electron Beam Melting

- 9.1.4. Laser Sintering

- 9.1.5. Jetting Technology

- 9.1.6. Laminated Object Manufacturing

- 9.1.7. Other Technologies

- 9.2. Market Analysis, Insights and Forecast - by Applications

- 9.2.1. Bioprinting

- 9.2.2. Implants

- 9.2.3. Prosthetics

- 9.2.4. Dentistry

- 9.2.5. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by Materials

- 9.3.1. Metals and Alloys

- 9.3.2. Polymers

- 9.3.3. Ceramics

- 9.3.4. Other Materials

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. Italy Healthcare 3D Printers Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. Stereo Lithography

- 10.1.2. Deposition Modeling

- 10.1.3. Electron Beam Melting

- 10.1.4. Laser Sintering

- 10.1.5. Jetting Technology

- 10.1.6. Laminated Object Manufacturing

- 10.1.7. Other Technologies

- 10.2. Market Analysis, Insights and Forecast - by Applications

- 10.2.1. Bioprinting

- 10.2.2. Implants

- 10.2.3. Prosthetics

- 10.2.4. Dentistry

- 10.2.5. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by Materials

- 10.3.1. Metals and Alloys

- 10.3.2. Polymers

- 10.3.3. Ceramics

- 10.3.4. Other Materials

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Spain Healthcare 3D Printers Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 11.1.1. Stereo Lithography

- 11.1.2. Deposition Modeling

- 11.1.3. Electron Beam Melting

- 11.1.4. Laser Sintering

- 11.1.5. Jetting Technology

- 11.1.6. Laminated Object Manufacturing

- 11.1.7. Other Technologies

- 11.2. Market Analysis, Insights and Forecast - by Applications

- 11.2.1. Bioprinting

- 11.2.2. Implants

- 11.2.3. Prosthetics

- 11.2.4. Dentistry

- 11.2.5. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by Materials

- 11.3.1. Metals and Alloys

- 11.3.2. Polymers

- 11.3.3. Ceramics

- 11.3.4. Other Materials

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 12. Rest of Europe Healthcare 3D Printers Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Technology

- 12.1.1. Stereo Lithography

- 12.1.2. Deposition Modeling

- 12.1.3. Electron Beam Melting

- 12.1.4. Laser Sintering

- 12.1.5. Jetting Technology

- 12.1.6. Laminated Object Manufacturing

- 12.1.7. Other Technologies

- 12.2. Market Analysis, Insights and Forecast - by Applications

- 12.2.1. Bioprinting

- 12.2.2. Implants

- 12.2.3. Prosthetics

- 12.2.4. Dentistry

- 12.2.5. Other Applications

- 12.3. Market Analysis, Insights and Forecast - by Materials

- 12.3.1. Metals and Alloys

- 12.3.2. Polymers

- 12.3.3. Ceramics

- 12.3.4. Other Materials

- 12.1. Market Analysis, Insights and Forecast - by Technology

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Envision TEC GmbH

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Renishaw PLC

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 General Electric (Arcam AB)

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Nano 3D Biosciences Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Eos GmbH

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Organovo Holding Inc

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 3D Systems Corporation

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Materialise NV

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Stratasys Ltd

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Oxford Performance Materials

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Envision TEC GmbH

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Healthcare 3D Printers Industry in Europe Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Healthcare 3D Printers Industry in Europe Share (%) by Company 2025

List of Tables

- Table 1: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Technology 2020 & 2033

- Table 2: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Applications 2020 & 2033

- Table 3: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Materials 2020 & 2033

- Table 4: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Technology 2020 & 2033

- Table 6: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Applications 2020 & 2033

- Table 7: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Materials 2020 & 2033

- Table 8: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Technology 2020 & 2033

- Table 10: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Applications 2020 & 2033

- Table 11: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Materials 2020 & 2033

- Table 12: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Technology 2020 & 2033

- Table 14: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Applications 2020 & 2033

- Table 15: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Materials 2020 & 2033

- Table 16: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Technology 2020 & 2033

- Table 18: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Applications 2020 & 2033

- Table 19: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Materials 2020 & 2033

- Table 20: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Technology 2020 & 2033

- Table 22: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Applications 2020 & 2033

- Table 23: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Materials 2020 & 2033

- Table 24: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 25: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Technology 2020 & 2033

- Table 26: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Applications 2020 & 2033

- Table 27: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Materials 2020 & 2033

- Table 28: Healthcare 3D Printers Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Healthcare 3D Printers Industry in Europe?

The projected CAGR is approximately 14%.

2. Which companies are prominent players in the Healthcare 3D Printers Industry in Europe?

Key companies in the market include Envision TEC GmbH, Renishaw PLC, General Electric (Arcam AB), Nano 3D Biosciences Inc, Eos GmbH, Organovo Holding Inc, 3D Systems Corporation, Materialise NV, Stratasys Ltd, Oxford Performance Materials.

3. What are the main segments of the Healthcare 3D Printers Industry in Europe?

The market segments include Technology, Applications, Materials.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.84 billion as of 2022.

5. What are some drivers contributing to market growth?

Technological Advancements Leading to Enhanced Application; Increasing Demand for Customized 3D Printing.

6. What are the notable trends driving market growth?

Metal and Alloy Segment is Dominating the European Healthcare 3D Printing Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of Trained Professionals; Absence of Specific Regulatory Guidelines.

8. Can you provide examples of recent developments in the market?

July 2022: Sculpteo and Daniel Robert Orthopedic launched a Bio-sourced 3D printed device. The collaboration will produce orthopedic devices from a bio-sourced material that will be made possible by 3D printing.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Healthcare 3D Printers Industry in Europe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Healthcare 3D Printers Industry in Europe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Healthcare 3D Printers Industry in Europe?

To stay informed about further developments, trends, and reports in the Healthcare 3D Printers Industry in Europe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence