Key Insights

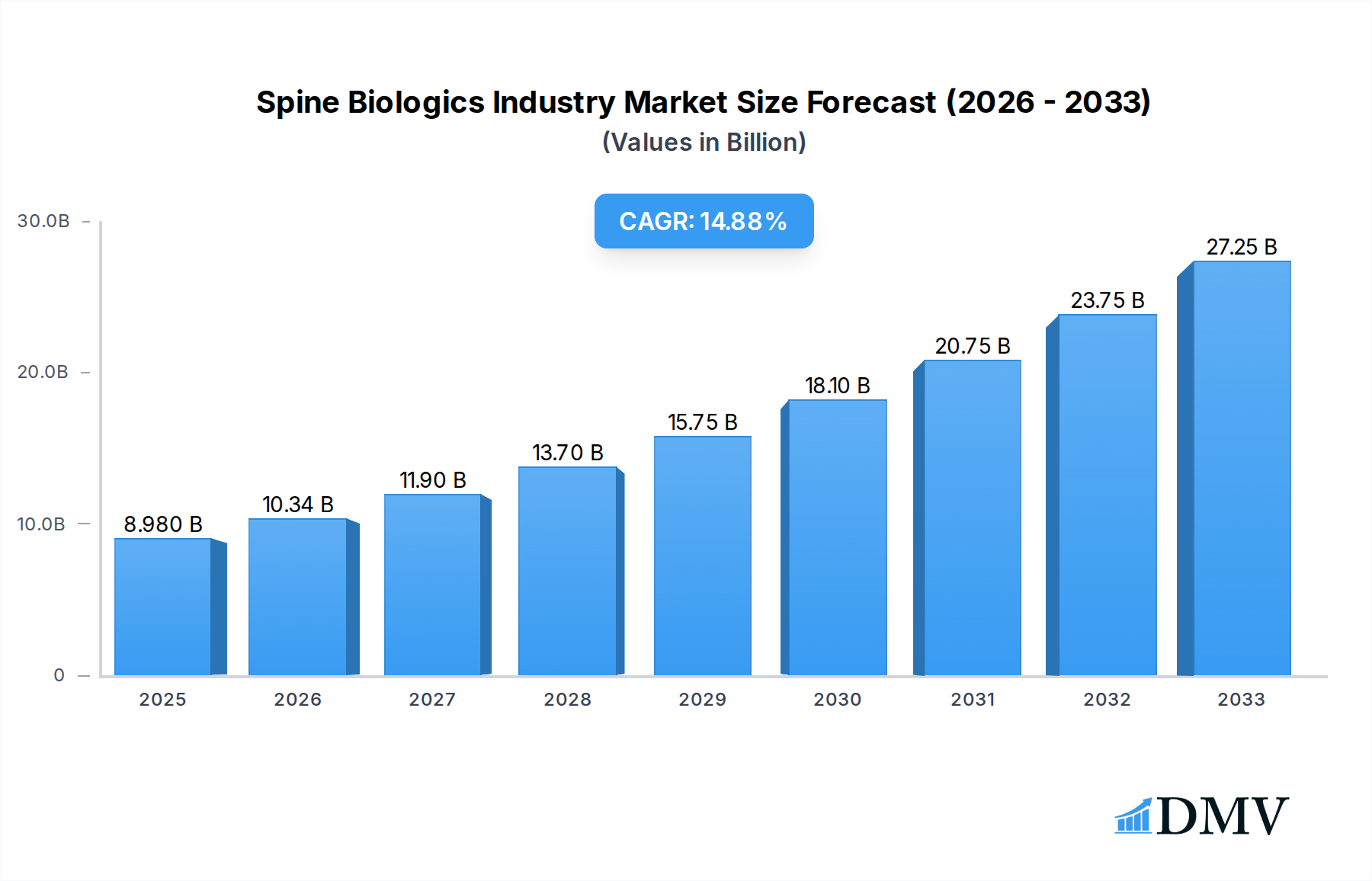

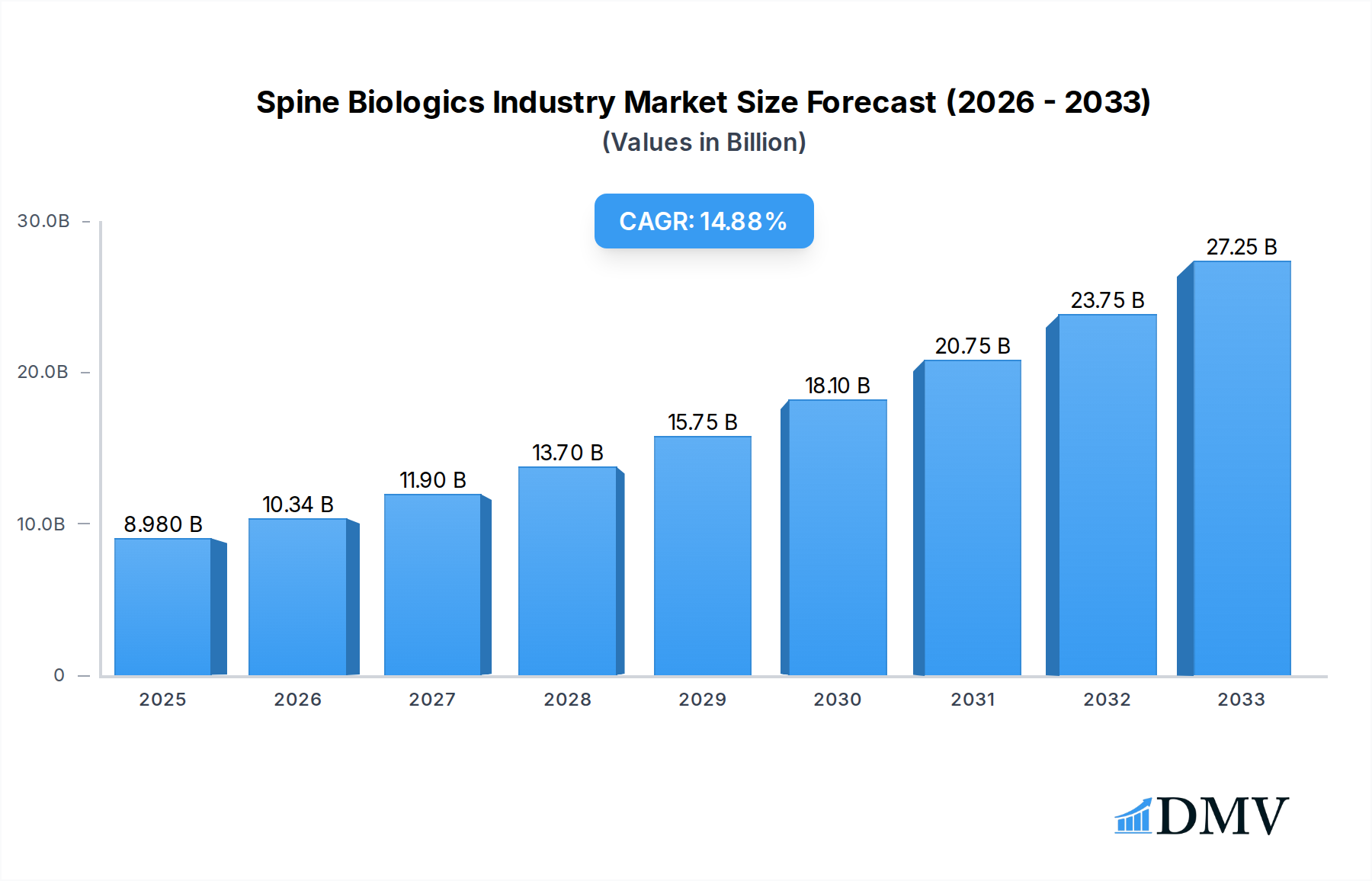

The Spine Biologics Industry is poised for significant expansion, driven by a confluence of technological advancements, an aging global population, and an increasing prevalence of spinal disorders. The market is projected to reach USD 8.98 billion in 2025, demonstrating robust growth at a Compound Annual Growth Rate (CAGR) of 15.24% throughout the forecast period (2025-2033). This surge is primarily fueled by the growing demand for innovative bone graft substitutes and advanced spinal allografts designed to enhance fusion rates and improve patient outcomes in spinal surgeries. The increasing adoption of minimally invasive surgical techniques also contributes to this growth, as these procedures often necessitate the use of specialized biologics for optimal healing and stabilization. Furthermore, rising healthcare expenditure and greater patient awareness regarding treatment options for chronic back pain and spinal deformities are significant contributors to market expansion.

Spine Biologics Industry Market Size (In Billion)

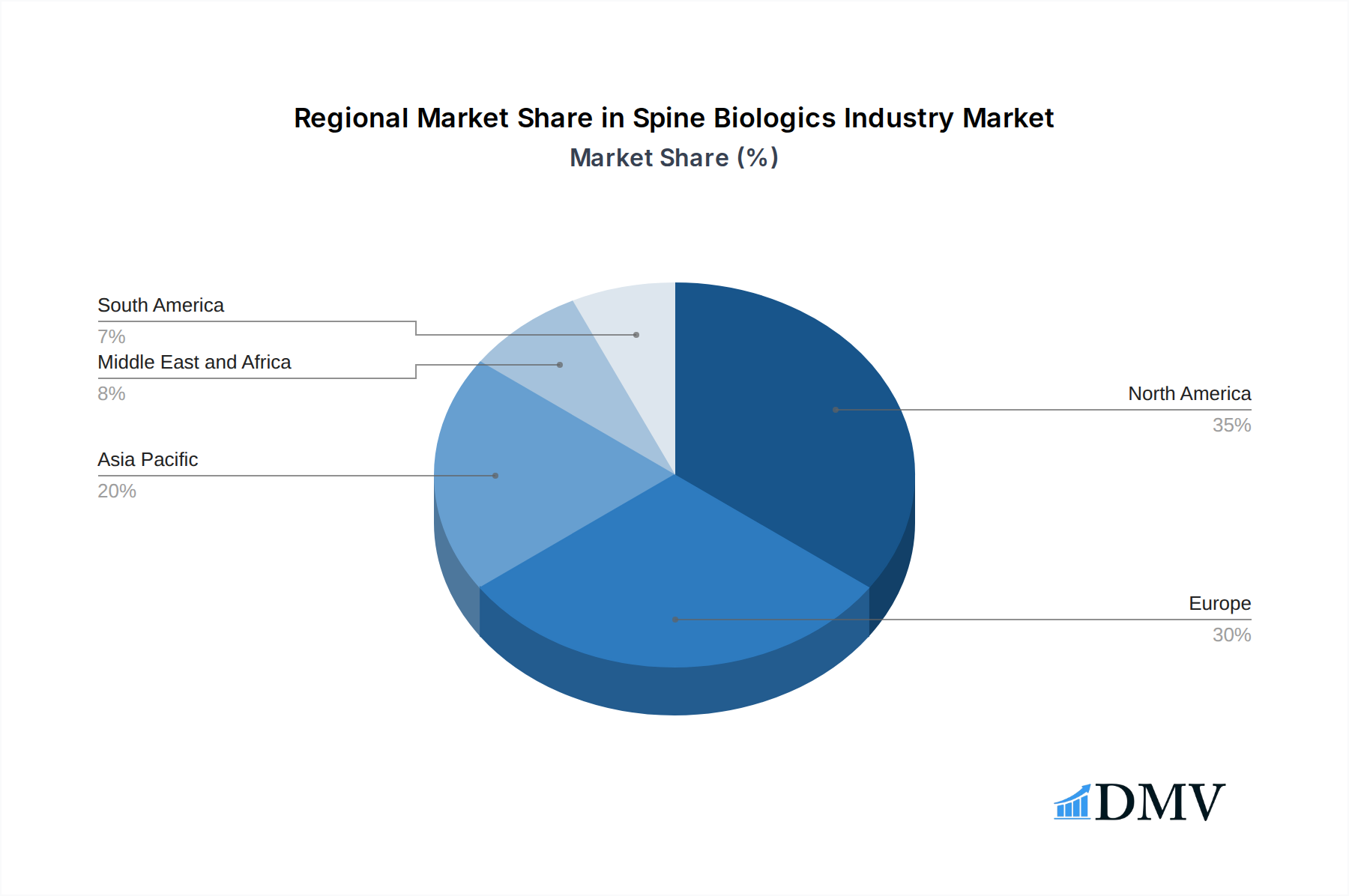

The market segmentation reveals a dynamic landscape, with Bone Graft Substitutes, including Bone Morphogenetic Proteins and Synthetic Bone Grafts, representing a substantial segment. Spinal Allografts, encompassing Machined Bone Allografts and Demineralized Bone Matrix, also hold considerable market share, catering to specific surgical needs. Hospitals and Ambulatory Surgical Centers are the dominant end-users, reflecting the procedural intensity of spinal interventions. Geographically, North America and Europe currently lead the market, driven by established healthcare infrastructure, high adoption rates of advanced medical technologies, and significant R&D investments. However, the Asia Pacific region is expected to witness the fastest growth due to its large patient pool, increasing access to healthcare, and a burgeoning medical device industry. Key players such as Stryker Corporation, Medtronic plc, and Johnson & Johnson (Depuy Synthes) are actively investing in product innovation and strategic partnerships to capitalize on these growth opportunities. While the market is experiencing impressive growth, potential restraints include the high cost of advanced biologics and stringent regulatory hurdles in some regions, which are being addressed through ongoing research and development and market access initiatives.

Spine Biologics Industry Company Market Share

Spine Biologics Industry Market Composition & Trends

The global Spine Biologics Industry is a dynamic and rapidly evolving market, projected to reach a valuation of XXX billion by 2025, with significant growth anticipated through 2033. This comprehensive report delves into the intricate market composition, dissecting its key trends, competitive landscape, and innovative catalysts. We examine the market concentration, noting the presence of major players such as Medtronic plc, Stryker Corporation, Johnson And Johnson (Depuy Synthes), Zimmer Biomet, NuVasive Inc, Arthrex Inc, Orthofix Medical Inc, Exactech Inc, Spine Wave Inc. The report analyzes the interplay between technological advancements, particularly in Bone Morphogenetic Proteins and Synthetic Bone Grafts, and the stringent regulatory frameworks governing this sector.

Key aspects explored include:

- Market Share Distribution: Detailed breakdown of market share among leading companies and product segments.

- Innovation Catalysts: Analysis of R&D investments and breakthroughs driving product development.

- Regulatory Landscapes: Impact of FDA approvals, CE marking, and regional regulations on market access and product launches.

- Substitute Products: Evaluation of alternative treatments and their influence on biologic adoption.

- End-User Profiles: Insights into the purchasing behaviors and demands of Hospitals, Ambulatory Surgical Centers, and other stakeholders.

- M&A Activities: Examination of recent mergers and acquisitions, with an estimated total deal value of XXX billion, highlighting strategic consolidations and market expansion efforts. The report meticulously analyzes the strategic imperatives behind these deals, including portfolio expansion and technological integration, underscoring a strong trend towards consolidation within the spine biologics market to gain competitive advantages.

Spine Biologics Industry Industry Evolution

The evolution of the Spine Biologics Industry is a testament to relentless innovation and a growing understanding of biological healing processes. From its nascent stages, the market has witnessed a remarkable trajectory, driven by the increasing incidence of spinal disorders, an aging global population, and significant advancements in biomaterials and regenerative medicine. The study period spanning 2019–2033, with a base year of 2025, allows for a granular analysis of this transformation. Historically, the market was characterized by limited product offerings and a reliance on traditional bone graft materials. However, the introduction of Bone Morphogenetic Proteins (BMPs) and sophisticated Synthetic Bone Grafts revolutionized surgical outcomes, offering enhanced osteoinductivity and osteoconductivity. This period saw growth rates averaging XX.X% annually, fueled by rising adoption in complex spinal fusion procedures.

Technological advancements have been central to this evolution. The development of advanced delivery systems, improved sterilization techniques for Spinal Allografts, and the exploration of tissue engineering have broadened the application spectrum. Furthermore, a notable shift in consumer demands has been observed, with patients and surgeons increasingly seeking minimally invasive techniques and biologics that promote faster recovery and superior long-term fusion rates. The demand for Machined Bones Allograft and Demineralized Bone Matrix (DBM), while established, has been augmented by the integration of these materials with advanced scaffolds and growth factors, further enhancing their efficacy. The estimated market growth rate for the forecast period 2025–2033 is projected to be XX.X%, indicating sustained momentum. This evolution is not just about new products, but also about a deeper integration of biologics into the standard of care for a wide range of spinal pathologies, from degenerative disc disease to complex deformity corrections. The increasing sophistication of surgical techniques and a greater emphasis on patient-specific solutions will continue to shape the industry's path, pushing the boundaries of what is possible in spinal reconstruction and fusion.

Leading Regions, Countries, or Segments in Spine Biologics Industry

The dominance within the Spine Biologics Industry is multi-faceted, with specific regions, countries, and product segments exhibiting significant leadership. Analyzing the Product segmentation, Bone Graft Substitutes, particularly Bone Morphogenetic Proteins (BMPs) and Synthetic Bone Grafts, have emerged as frontrunners in market share and innovation. These advanced materials offer superior osteoinductive and osteoconductive properties, leading to higher fusion rates and reduced complications, thus driving their widespread adoption.

- North America consistently leads the market, driven by several key factors:

- High Incidence of Spinal Disorders: A large and aging population susceptible to degenerative spinal conditions.

- Advanced Healthcare Infrastructure: Well-established hospital systems and a high density of skilled spine surgeons.

- Strong R&D Ecosystem: Significant investment in research and development by leading medical device companies and academic institutions.

- Reimbursement Policies: Favorable reimbursement for advanced spine surgeries and biologic implants.

Within the Product segment, Bone Graft Substitutes command a substantial market share, estimated at XX.X% of the total market value.

- Bone Morphogenetic Proteins (BMPs): Their ability to stimulate bone formation makes them indispensable in challenging fusion scenarios. The market for BMPs alone is projected to reach XXX billion by 2025.

- Synthetic Bone Grafts: Offer advantages such as consistent availability, reduced risk of disease transmission, and customizable properties, making them a cost-effective and reliable alternative.

The End User segment is primarily dominated by Hospitals, accounting for an estimated XX.X% of market revenue.

- Hospitals: The go-to destination for complex spinal surgeries, equipped with advanced surgical suites and multidisciplinary teams essential for managing intricate spinal procedures.

- Ambulatory Surgical Centers (ASCs): While growing in significance, particularly for less complex procedures, ASCs currently represent a smaller but expanding segment, estimated at XX.X%. Their growth is driven by cost-effectiveness and patient preference for outpatient care.

Conversely, Spinal Allografts, including Machined Bones Allograft and Demineralized Bone Matrix (DBM), though historically significant, now represent a segment where innovation is focused on enhancing their delivery and combination with other biologics. The Others segment for both product and end-user categories encompasses niche applications and emerging healthcare settings. The overarching dominance of North America and the Bone Graft Substitutes segment underscores a global trend towards advanced biological solutions for spinal fusion, propelled by technological advancements and the pursuit of optimal patient outcomes.

Spine Biologics Industry Product Innovations

Product innovation within the Spine Biologics Industry is a relentless pursuit, focused on enhancing osteogenesis and streamlining surgical procedures. Breakthroughs in Bone Morphogenetic Proteins (BMPs) have led to novel formulations with improved efficacy and reduced inflammatory responses, while Synthetic Bone Grafts are increasingly incorporating advanced scaffolding technologies for superior cell integration and bone regeneration. Applications now extend beyond traditional fusion to include regenerative therapies for disc degeneration. Performance metrics such as fusion rates, bone formation speed, and reduced revision surgery rates are consistently improving. Unique selling propositions lie in the development of tunable biomaterials that mimic native bone structure and the integration of growth factors for accelerated healing.

Propelling Factors for Spine Biologics Industry Growth

The Spine Biologics Industry is propelled by a confluence of potent factors. Technological advancements in biomaterials science and regenerative medicine are paramount, leading to more effective and safer products like advanced Bone Morphogenetic Proteins and innovative Synthetic Bone Grafts. The economic factor of an aging global population, coupled with a rise in lifestyle-related spinal conditions, significantly increases the demand for spinal fusion procedures, which biologics enhance. Furthermore, regulatory support from bodies like the FDA, approving novel biologic formulations and enabling their market entry, acts as a significant growth catalyst.

Obstacles in the Spine Biologics Industry Market

Despite robust growth, the Spine Biologics Industry faces notable obstacles. Regulatory challenges, including lengthy approval processes and evolving guidelines for biologics, can impede market entry and product development. Supply chain disruptions, particularly for allografts and sensitive biological components, pose risks to consistent availability. Competitive pressures from established players and the constant influx of new technologies create a challenging market landscape, while the substantial cost of some advanced biologics can limit their adoption, especially in resource-constrained regions.

Future Opportunities in Spine Biologics Industry

The future of the Spine Biologics Industry is ripe with opportunity. Emerging markets in Asia-Pacific and Latin America present significant untapped potential for advanced spinal solutions. The development of next-generation biologics, including personalized regenerative therapies and cell-based treatments, promises to revolutionize spinal care. A growing consumer trend towards less invasive surgical options will drive demand for biologics that facilitate faster recovery and improved outcomes in minimally invasive spine surgery (MIS). Furthermore, increased focus on preventing spinal fusion failure will open doors for preventative biologic applications.

Major Players in the Spine Biologics Industry Ecosystem

- Arthrex Inc

- Exactech Inc

- Spine Wave Inc

- Johnson And Johnson (Depuy Synthes)

- Orthofix Medical Inc

- NuVasive Inc

- Stryker Corporation

- Zimmer Biomet

- Medtronic plc

Key Developments in Spine Biologics Industry Industry

- 2023, Q4: Medtronic plc receives FDA approval for a new synthetic bone graft substitute aimed at improving fusion rates in lumbar procedures.

- 2024, Q1: Stryker Corporation announces a strategic partnership to advance research in osteoinductive growth factors for spinal fusion.

- 2024, Q2: Zimmer Biomet expands its biologics portfolio with the acquisition of a company specializing in allograft processing and preservation techniques.

- 2024, Q3: NuVasive Inc launches a novel combination therapy integrating BMPs with a proprietary DBM product, offering enhanced osteoconductivity.

- 2024, Q4: Orthofix Medical Inc presents promising clinical data on its latest generation of BMPs demonstrating superior bone formation in challenging revision surgeries.

Strategic Spine Biologics Industry Market Forecast

The strategic forecast for the Spine Biologics Industry indicates sustained and robust growth, driven by escalating demand for effective spinal fusion solutions and pioneering technological advancements. The increasing prevalence of spinal disorders globally, coupled with an aging demographic, ensures a continuous need for these critical medical interventions. Future growth will be fueled by innovations in synthetic bone grafts, enhanced bone morphogenetic proteins, and refined spinal allografts, all designed to improve fusion rates and accelerate patient recovery. The expanding role of biologics in minimally invasive procedures and the exploration of regenerative medicine present significant market potential, positioning the industry for continued expansion and greater impact on patient outcomes.

Spine Biologics Industry Segmentation

-

1. Product

-

1.1. Bone Graft Substitutes

- 1.1.1. Bone Morphogenetic Proteins

- 1.1.2. Synthetic Bone Grafts

-

1.2. Spinal Allografts

- 1.2.1. Machined Bones Allograft

- 1.2.2. Demineralized Bone Matrix

- 1.3. Others

-

1.1. Bone Graft Substitutes

-

2. End User

- 2.1. Hospitals

- 2.2. Ambulatory Surgical Centers

- 2.3. Others

Spine Biologics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Spine Biologics Industry Regional Market Share

Geographic Coverage of Spine Biologics Industry

Spine Biologics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.24% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Bone Graft Substitutes

- 5.1.1.1. Bone Morphogenetic Proteins

- 5.1.1.2. Synthetic Bone Grafts

- 5.1.2. Spinal Allografts

- 5.1.2.1. Machined Bones Allograft

- 5.1.2.2. Demineralized Bone Matrix

- 5.1.3. Others

- 5.1.1. Bone Graft Substitutes

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Ambulatory Surgical Centers

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global Spine Biologics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Bone Graft Substitutes

- 6.1.1.1. Bone Morphogenetic Proteins

- 6.1.1.2. Synthetic Bone Grafts

- 6.1.2. Spinal Allografts

- 6.1.2.1. Machined Bones Allograft

- 6.1.2.2. Demineralized Bone Matrix

- 6.1.3. Others

- 6.1.1. Bone Graft Substitutes

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Ambulatory Surgical Centers

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America Spine Biologics Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Bone Graft Substitutes

- 7.1.1.1. Bone Morphogenetic Proteins

- 7.1.1.2. Synthetic Bone Grafts

- 7.1.2. Spinal Allografts

- 7.1.2.1. Machined Bones Allograft

- 7.1.2.2. Demineralized Bone Matrix

- 7.1.3. Others

- 7.1.1. Bone Graft Substitutes

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Ambulatory Surgical Centers

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Europe Spine Biologics Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Bone Graft Substitutes

- 8.1.1.1. Bone Morphogenetic Proteins

- 8.1.1.2. Synthetic Bone Grafts

- 8.1.2. Spinal Allografts

- 8.1.2.1. Machined Bones Allograft

- 8.1.2.2. Demineralized Bone Matrix

- 8.1.3. Others

- 8.1.1. Bone Graft Substitutes

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Ambulatory Surgical Centers

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Asia Pacific Spine Biologics Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Bone Graft Substitutes

- 9.1.1.1. Bone Morphogenetic Proteins

- 9.1.1.2. Synthetic Bone Grafts

- 9.1.2. Spinal Allografts

- 9.1.2.1. Machined Bones Allograft

- 9.1.2.2. Demineralized Bone Matrix

- 9.1.3. Others

- 9.1.1. Bone Graft Substitutes

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals

- 9.2.2. Ambulatory Surgical Centers

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East and Africa Spine Biologics Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Bone Graft Substitutes

- 10.1.1.1. Bone Morphogenetic Proteins

- 10.1.1.2. Synthetic Bone Grafts

- 10.1.2. Spinal Allografts

- 10.1.2.1. Machined Bones Allograft

- 10.1.2.2. Demineralized Bone Matrix

- 10.1.3. Others

- 10.1.1. Bone Graft Substitutes

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals

- 10.2.2. Ambulatory Surgical Centers

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. South America Spine Biologics Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Bone Graft Substitutes

- 11.1.1.1. Bone Morphogenetic Proteins

- 11.1.1.2. Synthetic Bone Grafts

- 11.1.2. Spinal Allografts

- 11.1.2.1. Machined Bones Allograft

- 11.1.2.2. Demineralized Bone Matrix

- 11.1.3. Others

- 11.1.1. Bone Graft Substitutes

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Hospitals

- 11.2.2. Ambulatory Surgical Centers

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Arthrex Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Exactech Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Spine Wave Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Johnson And Johnson (Depuy Synthes)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Orthofix Medical Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NuVasive Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Stryker Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Zimmer Biomet

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Medtronic plc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Arthrex Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Spine Biologics Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Spine Biologics Industry Revenue (billion), by Product 2025 & 2033

- Figure 3: North America Spine Biologics Industry Revenue Share (%), by Product 2025 & 2033

- Figure 4: North America Spine Biologics Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: North America Spine Biologics Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Spine Biologics Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Spine Biologics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Spine Biologics Industry Revenue (billion), by Product 2025 & 2033

- Figure 9: Europe Spine Biologics Industry Revenue Share (%), by Product 2025 & 2033

- Figure 10: Europe Spine Biologics Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: Europe Spine Biologics Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe Spine Biologics Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Spine Biologics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Spine Biologics Industry Revenue (billion), by Product 2025 & 2033

- Figure 15: Asia Pacific Spine Biologics Industry Revenue Share (%), by Product 2025 & 2033

- Figure 16: Asia Pacific Spine Biologics Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Asia Pacific Spine Biologics Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific Spine Biologics Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Spine Biologics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Spine Biologics Industry Revenue (billion), by Product 2025 & 2033

- Figure 21: Middle East and Africa Spine Biologics Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Middle East and Africa Spine Biologics Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Middle East and Africa Spine Biologics Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Middle East and Africa Spine Biologics Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East and Africa Spine Biologics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Spine Biologics Industry Revenue (billion), by Product 2025 & 2033

- Figure 27: South America Spine Biologics Industry Revenue Share (%), by Product 2025 & 2033

- Figure 28: South America Spine Biologics Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: South America Spine Biologics Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: South America Spine Biologics Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: South America Spine Biologics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Spine Biologics Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Global Spine Biologics Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global Spine Biologics Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Spine Biologics Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 5: Global Spine Biologics Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Spine Biologics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Spine Biologics Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 11: Global Spine Biologics Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Spine Biologics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global Spine Biologics Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 20: Global Spine Biologics Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 21: Global Spine Biologics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Japan Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: India Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: South Korea Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Spine Biologics Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 29: Global Spine Biologics Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Spine Biologics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: GCC Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: South Africa Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Global Spine Biologics Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 35: Global Spine Biologics Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 36: Global Spine Biologics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Brazil Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Argentina Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Spine Biologics Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spine Biologics Industry?

The projected CAGR is approximately 15.24%.

2. Which companies are prominent players in the Spine Biologics Industry?

Key companies in the market include Arthrex Inc, Exactech Inc, Spine Wave Inc, Johnson And Johnson (Depuy Synthes), Orthofix Medical Inc, NuVasive Inc , Stryker Corporation, Zimmer Biomet, Medtronic plc.

3. What are the main segments of the Spine Biologics Industry?

The market segments include Product, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.98 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Geriatric Population; Growing Prevalence of Spine Deformities; Technological Advancements.

6. What are the notable trends driving market growth?

Spinal Allografts in Spinal Biologics is Estimated to Witness a Healthy Growth in Future.

7. Are there any restraints impacting market growth?

; Reimbursement Policies.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spine Biologics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spine Biologics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spine Biologics Industry?

To stay informed about further developments, trends, and reports in the Spine Biologics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence