Key Insights

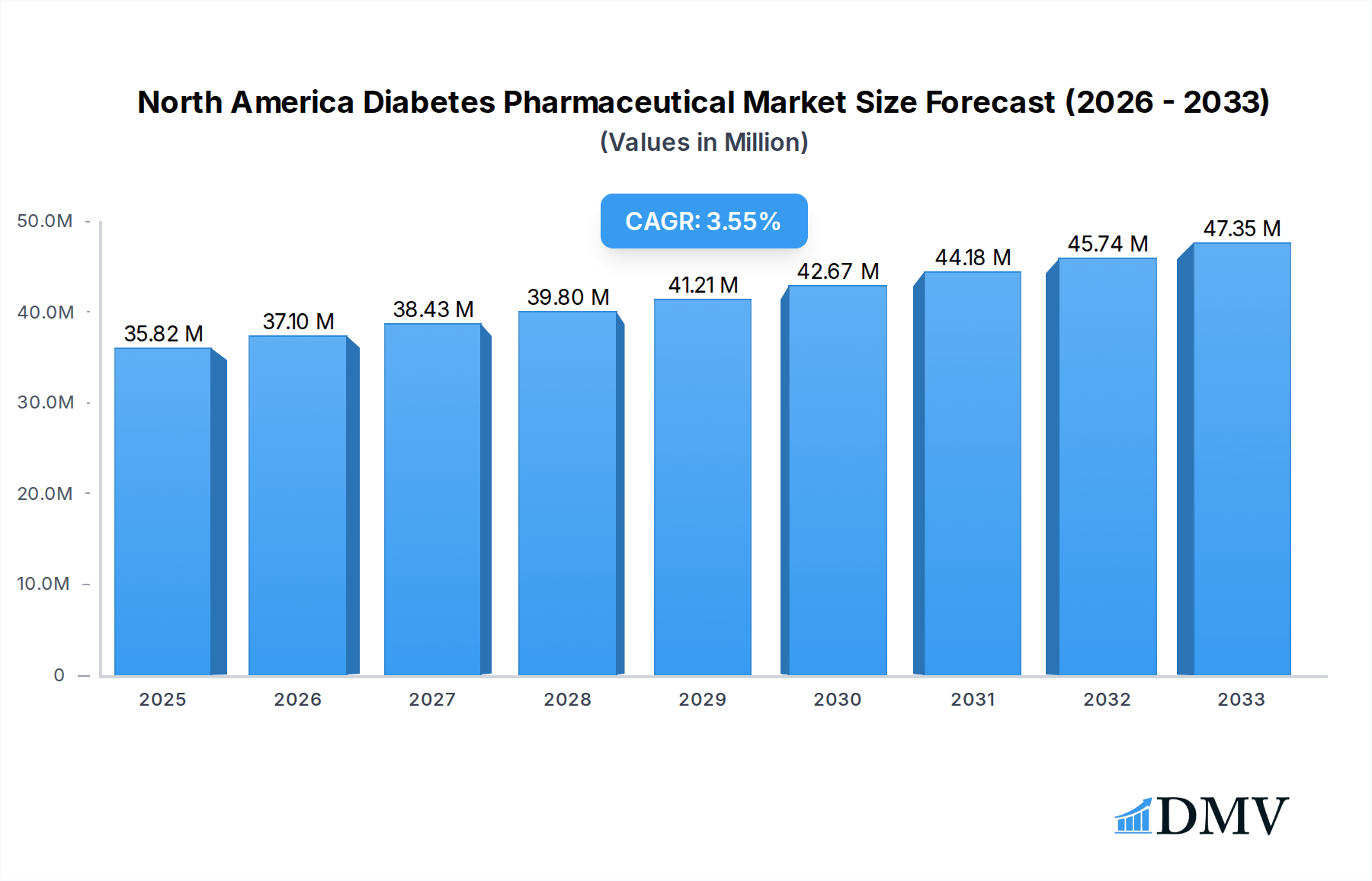

The North America Diabetes Pharmaceutical Market is poised for significant growth, projected to reach a substantial $35.82 million by 2025. This expansion is driven by a confluence of factors, including the escalating prevalence of diabetes across all age groups and the increasing global focus on innovative treatment modalities. The market's Compound Annual Growth Rate (CAGR) is estimated at 3.58% between 2025 and 2033, underscoring a steady and robust upward trajectory. Key market drivers include the rising incidence of type 1 and type 2 diabetes, advancements in pharmaceutical research leading to more effective and patient-friendly therapies, and a growing awareness of diabetes management and its long-term complications. The increasing adoption of newer drug classes, such as SGLT-2 inhibitors and GLP-1 receptor agonists, which offer enhanced glycemic control and cardiovascular benefits, is a prominent trend shaping the market landscape. Furthermore, the growing demand for biosimilar insulins is also contributing to market expansion by offering more affordable treatment options.

North America Diabetes Pharmaceutical Market Market Size (In Million)

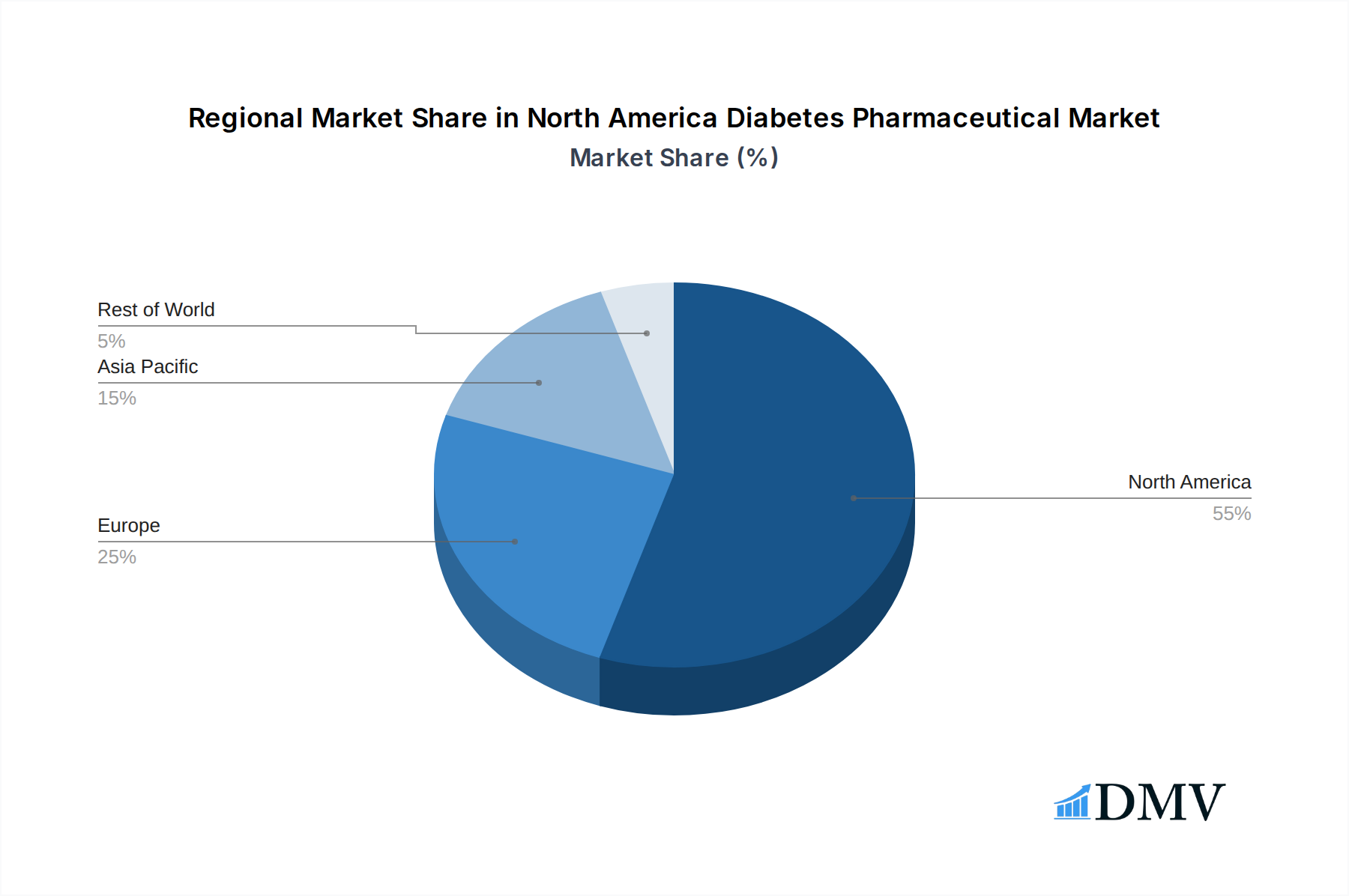

The North America Diabetes Pharmaceutical Market encompasses a diverse range of therapeutic segments, including various types of insulins (basal, bolus, traditional human, and biosimilar), oral anti-diabetic drugs (Biguanides, Alpha-Glucosidase Inhibitors, Dopamine D2 receptor agonists, SGLT-2 inhibitors, DPP-4 inhibitors, Sulfonylureas, Meglitinides), and non-insulin injectable drugs (GLP-1 receptor agonists, Amylin Analogue). The United States dominates the market due to its large patient population, high healthcare spending, and rapid adoption of new technologies. Canada and the rest of North America also represent significant markets. Key industry players like Novo Nordisk A/S, Sanofi Aventis, Eli Lilly, and Merck are actively involved in research and development, product launches, and strategic collaborations to capture market share. Despite the positive outlook, certain restraints, such as the high cost of novel therapies and evolving regulatory landscapes, could pose challenges. However, the overall market sentiment remains optimistic, fueled by an unmet need for advanced diabetes management solutions and a commitment from pharmaceutical companies to address this critical health issue.

North America Diabetes Pharmaceutical Market Company Market Share

North America Diabetes Pharmaceutical Market: Comprehensive Analysis and Forecast (2019-2033)

This in-depth report provides a panoramic view of the North America Diabetes Pharmaceutical Market, a rapidly evolving sector driven by an aging population, rising obesity rates, and significant advancements in therapeutic innovation. Covering the study period of 2019–2033, with 2025 as the base and estimated year, this analysis delves deep into market dynamics, product segments, leading geographies, and the strategic landscape of key players. Stakeholders will gain actionable insights into market composition, industry evolution, growth drivers, and emerging opportunities within the United States, Canada, and the Rest of North America. The report emphasizes the impact of groundbreaking product innovations and critical industry developments, offering a definitive forecast for the North America diabetes drug market.

North America Diabetes Pharmaceutical Market Market Composition & Trends

The North America Diabetes Pharmaceutical Market is characterized by a dynamic interplay of established giants and innovative disruptors, leading to a moderately consolidated yet highly competitive environment. Innovation catalysts are primarily driven by the relentless pursuit of novel drug discovery for diabetes management, focusing on improved efficacy, reduced side effects, and enhanced patient convenience. The regulatory landscape, spearheaded by bodies like the US FDA and Health Canada, plays a crucial role in market access and product approval, influencing the pace of innovation and market entry. Substitute products, including lifestyle modifications and emerging non-pharmacological therapies, are present but currently hold a niche position against the efficacy of pharmaceuticals. End-user profiles are diverse, encompassing individuals with Type 1 and Type 2 diabetes, each with distinct treatment needs and preferences. Merger and acquisition (M&A) activities are strategic moves by leading companies to expand their portfolios, gain market share, and acquire cutting-edge technologies. The market share distribution is influenced by the success of blockbuster drugs, patent expirations, and the introduction of biosimil alternatives. M&A deal values continue to be significant as companies aim to consolidate their positions in this high-growth market.

- Market Concentration: Moderately consolidated, with key players holding significant market share.

- Innovation Catalysts: Novel drug discovery, focus on personalized medicine, and combination therapies.

- Regulatory Landscape: Stringent approval processes by US FDA and Health Canada, influencing R&D and market entry.

- Substitute Products: Lifestyle interventions, bariatric surgery, and digital health solutions are supplementary.

- End-User Profiles: Diverse patient populations with varying disease severity, age groups, and co-morbidities.

- M&A Activities: Strategic acquisitions to broaden therapeutic pipelines and enhance market presence.

North America Diabetes Pharmaceutical Market Industry Evolution

The North America Diabetes Pharmaceutical Market has witnessed a profound evolution, transitioning from a landscape dominated by traditional insulins and oral hypoglycemic agents to one embracing sophisticated biologics and targeted therapies. This evolution is a direct consequence of escalating diabetes prevalence across the region, fueled by sedentary lifestyles and increasing obesity rates, thereby expanding the patient pool requiring pharmaceutical intervention. The industry growth trajectory has been consistently upward, driven by a strong unmet medical need and a favorable reimbursement environment for innovative treatments. Technological advancements have been pivotal, ushering in an era of precision medicine. The development of advanced drug delivery systems, such as continuous glucose monitoring (CGM) devices integrated with insulin pumps, alongside the advent of novel molecular targets, has revolutionized diabetes care. For instance, the rise of SGLT-2 inhibitors and DPP-4 inhibitors has offered new avenues for glycemic control with significant cardiovascular and renal benefits, profoundly shifting treatment paradigms.

Shifting consumer demands are also playing an increasingly crucial role. Patients are no longer solely seeking glycemic control; they are looking for treatments that minimize side effects, improve quality of life, and offer convenience, such as once-daily or once-weekly dosing regimens. This has propelled the demand for innovative formulations and drug classes like GLP-1 receptor agonists, which not only aid in blood sugar management but also contribute to weight loss, a critical factor for many individuals with Type 2 diabetes. The adoption metrics for these newer drug classes have been remarkably high, indicating a strong market receptiveness to therapeutic progress. Furthermore, the increasing awareness and accessibility of biosimilar insulins are contributing to cost-effectiveness and expanding treatment options, particularly within the basal and bolus insulin segments. The historical period from 2019 to 2024 saw a robust CAGR driven by these factors. The forecast period from 2025 to 2033 is expected to maintain this momentum, with an estimated market value reaching several tens of billions of US dollars by 2033, supported by continuous research and development into more effective and patient-centric diabetes medications. The estimated Compound Annual Growth Rate (CAGR) for the forecast period is projected to be around 5-7%.

Leading Regions, Countries, or Segments in North America Diabetes Pharmaceutical Market

The North America Diabetes Pharmaceutical Market is demonstrably led by the United States, a powerhouse of pharmaceutical research, development, and market penetration. This dominance is a confluence of several critical factors that create an exceptionally fertile ground for diabetes drug innovation and adoption. The sheer size of the patient population within the US, coupled with high rates of obesity and type 2 diabetes, provides a substantial market base. Furthermore, the robust healthcare infrastructure, extensive insurance coverage, and a strong emphasis on preventive care contribute to higher prescription rates for advanced therapeutic options. The presence of leading pharmaceutical giants and a vibrant venture capital ecosystem encourages significant investment in R&D, leading to a continuous pipeline of novel treatments.

Within the broader segments, Insulins, particularly Basal or Long Acting Insulins and Bolus or Fast Acting Insulins, continue to command a significant share due to their foundational role in diabetes management. However, the rapid innovation and adoption of Oral Anti-diabetic drugs, especially SGLT-2 inhibitors and DPP-4 inhibitors, are reshaping the market. These drug classes have demonstrated remarkable efficacy not only in glycemic control but also in reducing cardiovascular and renal risks, making them highly preferred therapeutic options for a growing segment of the diabetic population. The emergence of Biosimilar Insulins is also a growing force, offering a more affordable alternative and increasing accessibility for a wider patient demographic. The Non-Insulin Injectable drugs segment, prominently featuring GLP-1 receptor agonists, is experiencing explosive growth due to their dual benefits of glycemic control and weight management, addressing two major co-morbidities associated with diabetes.

Dominant Geography: United States:

- Key Drivers: Large patient population, high prevalence of diabetes and obesity, advanced healthcare infrastructure, robust R&D investment, favorable reimbursement policies.

- Analysis: The US market benefits from a mature healthcare system that readily adopts innovative therapies. Strong patient and physician awareness of diabetes complications fuels demand for effective treatments. Significant government and private sector funding for diabetes research translates into a continuous influx of new drugs.

Leading Segments:

- Oral Anti-diabetic Drugs (SGLT-2 Inhibitors & DPP-4 Inhibitors):

- Key Drivers: Significant cardiovascular and renal protective benefits, improved patient adherence due to oral administration, efficacy in managing hyperglycemia.

- Analysis: These classes have become first-line or early-stage treatments for many Type 2 diabetes patients, driven by compelling clinical trial data demonstrating benefits beyond glucose lowering.

- Non-Insulin Injectable Drugs (GLP-1 Receptor Agonists):

- Key Drivers: Prominent weight loss benefits, potent glycemic control, positive cardiovascular outcomes, and convenient dosing schedules.

- Analysis: The growing obesity epidemic has significantly boosted the appeal of GLP-1 RAs, positioning them as a highly sought-after therapeutic option.

- Insulins (Basal and Bolus):

- Key Drivers: Essential for Type 1 diabetes management and advanced Type 2 diabetes treatment, availability of biosimilar options enhancing affordability.

- Analysis: While newer drug classes are gaining traction, insulins remain critical for a significant portion of the diabetic population, with ongoing innovation in delivery systems and formulations.

- Oral Anti-diabetic Drugs (SGLT-2 Inhibitors & DPP-4 Inhibitors):

North America Diabetes Pharmaceutical Market Product Innovations

The North America diabetes pharmaceutical landscape is defined by a relentless stream of product innovations designed to enhance therapeutic efficacy, patient convenience, and safety. A prime example is the development of single-molecule dual agonists like tirzepatide, which simultaneously targets GIP and GLP-1 receptors, offering superior glycemic control and significant weight loss. Oral insulin formulations are also on the horizon, promising to revolutionize insulin delivery by offering a non-injectable alternative. Furthermore, advancements in biosimilar insulins are expanding treatment access and affordability. These innovations are characterized by unique selling propositions such as improved pharmacokinetics, reduced side effect profiles, and simplified dosing regimens, directly addressing unmet patient needs and driving market growth.

Propelling Factors for North America Diabetes Pharmaceutical Market Growth

Several key factors are propelling the growth of the North America Diabetes Pharmaceutical Market.

- Technological Advancements: Continuous R&D leading to novel drug classes (e.g., GLP-1 receptor agonists, SGLT-2 inhibitors) and improved drug delivery systems.

- Increasing Prevalence of Diabetes: Rising rates of obesity and sedentary lifestyles are significantly expanding the diabetic patient population.

- Aging Population: Older demographics are more susceptible to chronic diseases like diabetes, increasing demand for pharmaceutical interventions.

- Growing Awareness and Diagnosis: Enhanced public health campaigns and improved diagnostic capabilities lead to earlier and more frequent diagnoses.

- Favorable Regulatory Environment: Timely approvals for innovative diabetes therapies by regulatory bodies accelerate market access.

- Expanding Healthcare Coverage: Increased insurance penetration ensures greater access to prescription medications.

Obstacles in the North America Diabetes Pharmaceutical Market Market

Despite robust growth, the North America Diabetes Pharmaceutical Market faces certain obstacles that can impede its progress.

- High Cost of Novel Therapies: The premium pricing of innovative diabetes drugs can create access barriers for some patient populations and strain healthcare budgets.

- Stringent Regulatory Hurdles: While necessary, the lengthy and complex approval processes for new drugs can delay market entry and increase development costs.

- Patent Expirations and Generic Competition: The expiration of patents for blockbuster diabetes drugs leads to the introduction of generics and biosimil, impacting revenue for originator companies.

- Side Effect Concerns and Patient Adherence: Some diabetes medications are associated with side effects that can lead to reduced patient adherence, impacting treatment outcomes.

- Reimbursement Challenges: Navigating diverse and sometimes restrictive reimbursement policies across different insurance providers can be a significant hurdle.

- Supply Chain Disruptions: Global events can disrupt the manufacturing and distribution of essential diabetes medications, leading to shortages.

Future Opportunities in North America Diabetes Pharmaceutical Market

The North America Diabetes Pharmaceutical Market is ripe with future opportunities for growth and innovation.

- Personalized Medicine: Developing targeted therapies based on individual genetic profiles and disease subtypes offers significant potential for improved treatment outcomes.

- Combination Therapies: Innovative combinations of existing and novel drug classes can provide synergistic benefits and address complex diabetes management challenges.

- Digital Health Integration: Leveraging wearable devices, AI-powered platforms, and telehealth for remote patient monitoring, adherence support, and personalized treatment adjustments.

- Emerging Drug Targets: Continued research into novel biological pathways involved in glucose homeostasis and insulin sensitivity.

- Preventive Therapies: Developing interventions that can delay or prevent the onset of Type 2 diabetes in at-risk populations.

- Focus on Comorbidity Management: Drugs that effectively manage diabetes alongside cardiovascular disease, kidney disease, and obesity will see sustained demand.

Major Players in the North America Diabetes Pharmaceutical Market Ecosystem

- Novo Nordisk A/S

- Eli Lilly

- Sanofi Aventis

- Merck

- Astra Zeneca

- Janssen Pharmaceuticals

- Pfizer

- Bristol Myers Squibb

- Takeda

- Boehringer Ingelheim

- Teva

- Astellas

- Other

Key Developments in North America Diabetes Pharmaceutical Market Industry

- May 2022: The US FDA approved Eli Lilly and Company's Mounjaro (tirzepatide) injection as an adjunct to diet and exercise. It is to enhance glycemic control in adult patients with type 2 diabetes. A single molecule, Mounjaro is a once-weekly glucose-dependent insulinotropic polypeptide and glucagon-like peptide-1 receptor agonist.

- March 2022: Oramed announced that ORMD-0801 is being evaluated in two pivotal Phase 3 trials and can be the first oral insulin capsule with the most convenient and safest way to deliver insulin therapy. This drug is expected to be a game-changer in the insulin and oral anti-diabetes drugs markets. Oramed is also developing an oral GLP-1 analog capsule (ORMD-0901).

Strategic North America Diabetes Pharmaceutical Market Market Forecast

The North America Diabetes Pharmaceutical Market is poised for sustained and robust growth, driven by an unyielding demand for effective diabetes management solutions. The strategic focus on developing highly innovative therapies, particularly those addressing the multifaceted nature of diabetes and its co-morbidities, will be a primary growth catalyst. The ongoing advancements in drug discovery, coupled with the increasing adoption of personalized medicine and digital health technologies, will unlock significant market potential. The forecast period of 2025–2033 is expected to witness a substantial expansion, fueled by the unmet needs of a growing diabetic population and the continuous introduction of groundbreaking treatments that promise improved patient outcomes and enhanced quality of life. The market is projected to exceed tens of billions of US dollars in value by the end of the forecast period.

North America Diabetes Pharmaceutical Market Segmentation

-

1. Insulins

- 1.1. Basal or Long Acting Insulins

- 1.2. Bolus or Fast Acting Insulins

- 1.3. Traditional Human Insulins

- 1.4. Biosimilar Insulins

-

2. Oral Anti-diabetic drugs

- 2.1. Biguanides

- 2.2. Alpha-Glucosidase Inhibitors

- 2.3. Dopamine D2 receptor agonist

- 2.4. SGLT-2 inhibitors

- 2.5. DPP-4 inhibitors

- 2.6. Sulfonylureas

- 2.7. Meglitinides

-

3. Non-Insulin Injectable drugs

- 3.1. GLP-1 receptor agonists

- 3.2. Amylin Analogue

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Rest of North America

North America Diabetes Pharmaceutical Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America Diabetes Pharmaceutical Market Regional Market Share

Geographic Coverage of North America Diabetes Pharmaceutical Market

North America Diabetes Pharmaceutical Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.58% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insulins

- 5.1.1. Basal or Long Acting Insulins

- 5.1.2. Bolus or Fast Acting Insulins

- 5.1.3. Traditional Human Insulins

- 5.1.4. Biosimilar Insulins

- 5.2. Market Analysis, Insights and Forecast - by Oral Anti-diabetic drugs

- 5.2.1. Biguanides

- 5.2.2. Alpha-Glucosidase Inhibitors

- 5.2.3. Dopamine D2 receptor agonist

- 5.2.4. SGLT-2 inhibitors

- 5.2.5. DPP-4 inhibitors

- 5.2.6. Sulfonylureas

- 5.2.7. Meglitinides

- 5.3. Market Analysis, Insights and Forecast - by Non-Insulin Injectable drugs

- 5.3.1. GLP-1 receptor agonists

- 5.3.2. Amylin Analogue

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest of North America

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Insulins

- 6. North America Diabetes Pharmaceutical Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insulins

- 6.1.1. Basal or Long Acting Insulins

- 6.1.2. Bolus or Fast Acting Insulins

- 6.1.3. Traditional Human Insulins

- 6.1.4. Biosimilar Insulins

- 6.2. Market Analysis, Insights and Forecast - by Oral Anti-diabetic drugs

- 6.2.1. Biguanides

- 6.2.2. Alpha-Glucosidase Inhibitors

- 6.2.3. Dopamine D2 receptor agonist

- 6.2.4. SGLT-2 inhibitors

- 6.2.5. DPP-4 inhibitors

- 6.2.6. Sulfonylureas

- 6.2.7. Meglitinides

- 6.3. Market Analysis, Insights and Forecast - by Non-Insulin Injectable drugs

- 6.3.1. GLP-1 receptor agonists

- 6.3.2. Amylin Analogue

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Insulins

- 7. United States North America Diabetes Pharmaceutical Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Insulins

- 7.1.1. Basal or Long Acting Insulins

- 7.1.2. Bolus or Fast Acting Insulins

- 7.1.3. Traditional Human Insulins

- 7.1.4. Biosimilar Insulins

- 7.2. Market Analysis, Insights and Forecast - by Oral Anti-diabetic drugs

- 7.2.1. Biguanides

- 7.2.2. Alpha-Glucosidase Inhibitors

- 7.2.3. Dopamine D2 receptor agonist

- 7.2.4. SGLT-2 inhibitors

- 7.2.5. DPP-4 inhibitors

- 7.2.6. Sulfonylureas

- 7.2.7. Meglitinides

- 7.3. Market Analysis, Insights and Forecast - by Non-Insulin Injectable drugs

- 7.3.1. GLP-1 receptor agonists

- 7.3.2. Amylin Analogue

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Insulins

- 8. Canada North America Diabetes Pharmaceutical Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Insulins

- 8.1.1. Basal or Long Acting Insulins

- 8.1.2. Bolus or Fast Acting Insulins

- 8.1.3. Traditional Human Insulins

- 8.1.4. Biosimilar Insulins

- 8.2. Market Analysis, Insights and Forecast - by Oral Anti-diabetic drugs

- 8.2.1. Biguanides

- 8.2.2. Alpha-Glucosidase Inhibitors

- 8.2.3. Dopamine D2 receptor agonist

- 8.2.4. SGLT-2 inhibitors

- 8.2.5. DPP-4 inhibitors

- 8.2.6. Sulfonylureas

- 8.2.7. Meglitinides

- 8.3. Market Analysis, Insights and Forecast - by Non-Insulin Injectable drugs

- 8.3.1. GLP-1 receptor agonists

- 8.3.2. Amylin Analogue

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Insulins

- 9. Rest of North America North America Diabetes Pharmaceutical Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Insulins

- 9.1.1. Basal or Long Acting Insulins

- 9.1.2. Bolus or Fast Acting Insulins

- 9.1.3. Traditional Human Insulins

- 9.1.4. Biosimilar Insulins

- 9.2. Market Analysis, Insights and Forecast - by Oral Anti-diabetic drugs

- 9.2.1. Biguanides

- 9.2.2. Alpha-Glucosidase Inhibitors

- 9.2.3. Dopamine D2 receptor agonist

- 9.2.4. SGLT-2 inhibitors

- 9.2.5. DPP-4 inhibitors

- 9.2.6. Sulfonylureas

- 9.2.7. Meglitinides

- 9.3. Market Analysis, Insights and Forecast - by Non-Insulin Injectable drugs

- 9.3.1. GLP-1 receptor agonists

- 9.3.2. Amylin Analogue

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. United States

- 9.4.2. Canada

- 9.4.3. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Insulins

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Pfizer

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Other

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Teva

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Janssen Pharmaceuticals

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Eli Lilly

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Merck

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Astra Zeneca

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Sanofi Aventis

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Bristol Myers Squibb

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Novo Nordisk A/S

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 Takeda

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 Boehringer Ingelheim

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.13 Astellas

- 10.1.13.1. Company Overview

- 10.1.13.2. Products

- 10.1.13.3. Company Financials

- 10.1.13.4. SWOT Analysis

- 10.1.1 Pfizer

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Diabetes Pharmaceutical Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Diabetes Pharmaceutical Market Share (%) by Company 2025

List of Tables

- Table 1: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Insulins 2020 & 2033

- Table 2: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Insulins 2020 & 2033

- Table 3: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 4: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 5: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 6: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 7: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Geography 2020 & 2033

- Table 9: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Region 2020 & 2033

- Table 10: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Insulins 2020 & 2033

- Table 12: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Insulins 2020 & 2033

- Table 13: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 14: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 15: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 16: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 17: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 18: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Geography 2020 & 2033

- Table 19: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Country 2020 & 2033

- Table 20: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 21: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Insulins 2020 & 2033

- Table 22: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Insulins 2020 & 2033

- Table 23: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 24: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 25: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 26: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 27: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 28: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Geography 2020 & 2033

- Table 29: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Country 2020 & 2033

- Table 30: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Insulins 2020 & 2033

- Table 32: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Insulins 2020 & 2033

- Table 33: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 34: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 35: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 36: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 37: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 38: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Geography 2020 & 2033

- Table 39: North America Diabetes Pharmaceutical Market Revenue Million Forecast, by Country 2020 & 2033

- Table 40: North America Diabetes Pharmaceutical Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Diabetes Pharmaceutical Market?

The projected CAGR is approximately 3.58%.

2. Which companies are prominent players in the North America Diabetes Pharmaceutical Market?

Key companies in the market include Pfizer, Other, Teva, Janssen Pharmaceuticals, Eli Lilly, Merck, Astra Zeneca, Sanofi Aventis, Bristol Myers Squibb, Novo Nordisk A/S, Takeda, Boehringer Ingelheim, Astellas.

3. What are the main segments of the North America Diabetes Pharmaceutical Market?

The market segments include Insulins, Oral Anti-diabetic drugs, Non-Insulin Injectable drugs, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 35.82 Million as of 2022.

5. What are some drivers contributing to market growth?

; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies.

6. What are the notable trends driving market growth?

The Oral anti-diabetic drugs segment is expected to register the highest CAGR in the North America Diabetes Drugs Market.

7. Are there any restraints impacting market growth?

; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures. Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products.

8. Can you provide examples of recent developments in the market?

May 2022: The US FDA approved Eli Lilly and Company's Mounjaro (tirzepatide) injection as an adjunct to diet and exercise. It is to enhance glycemic control in adult patients with type 2 diabetes. A single molecule, Mounjaro is a once-weekly glucose-dependent insulinotropic polypeptide and glucagon-like peptide-1 receptor agonist.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Diabetes Pharmaceutical Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Diabetes Pharmaceutical Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Diabetes Pharmaceutical Market?

To stay informed about further developments, trends, and reports in the North America Diabetes Pharmaceutical Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence