Key Insights

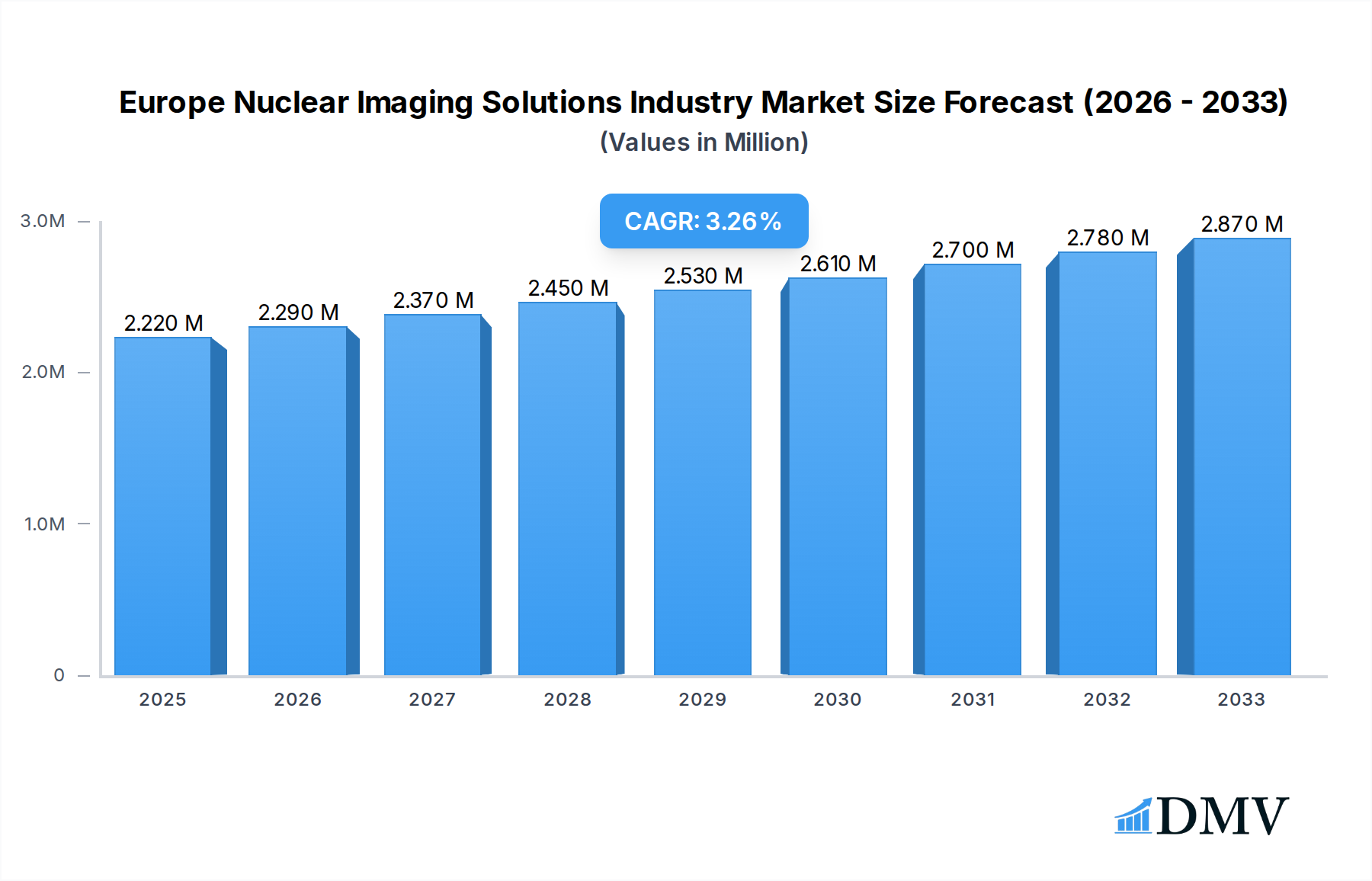

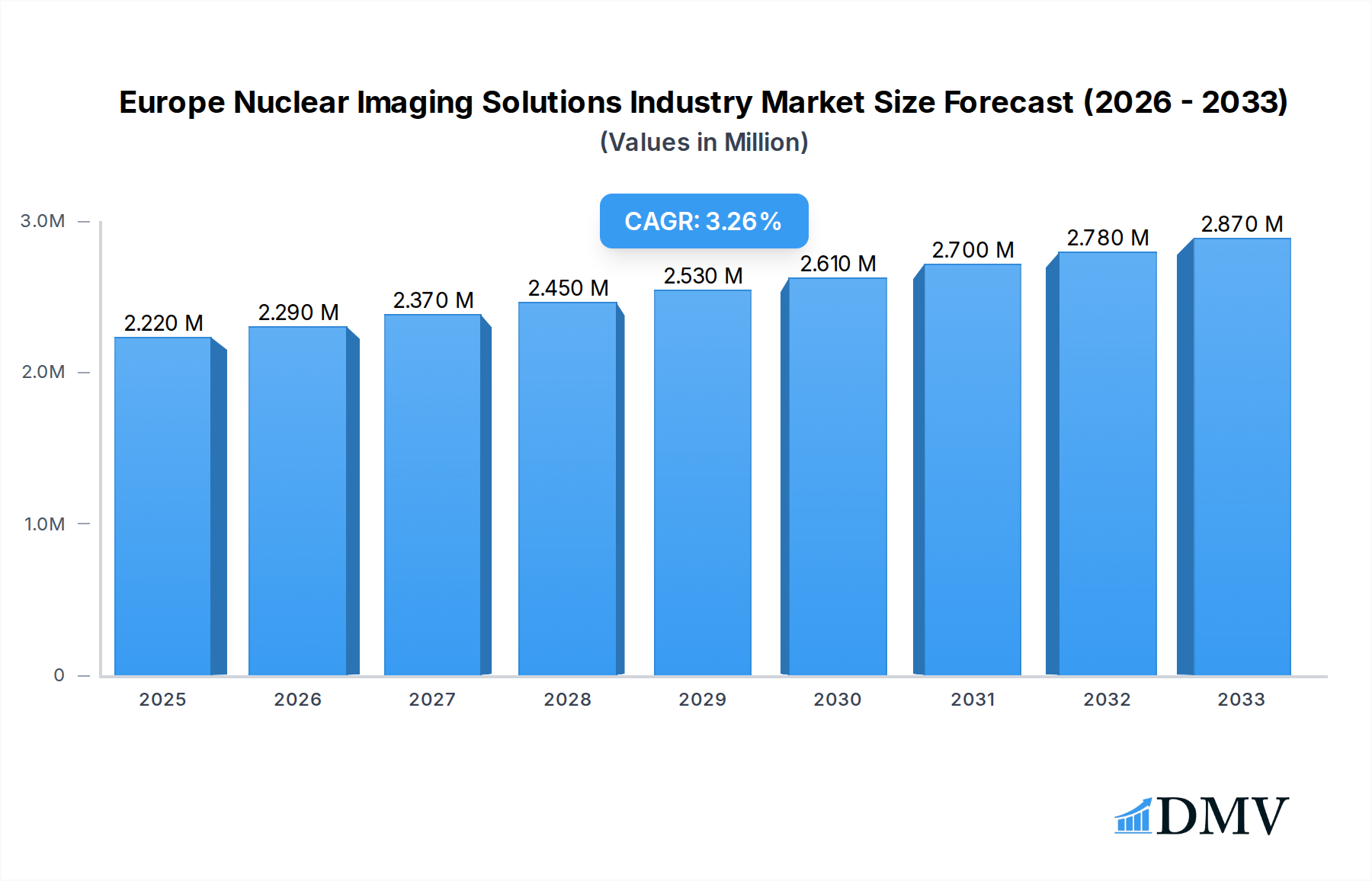

The Europe Nuclear Imaging Solutions market is poised for significant expansion, driven by an increasing prevalence of chronic diseases and the continuous advancement of diagnostic technologies. Valued at 2.22 million in the base year of 2025, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.34% through 2033. Key growth catalysts include the rising demand for advanced imaging techniques like SPECT and PET scans for early and accurate disease detection, particularly in oncology, cardiology, and neurology. The growing adoption of radiopharmaceuticals, including Technetium-99m (TC-99m) and Fluorine-18 (F-18), is fundamental to enhancing diagnostic capabilities. Furthermore, supportive government initiatives and increasing healthcare expenditure across European nations are contributing to market momentum. The market is also experiencing robust growth due to ongoing research and development efforts by leading players, leading to the introduction of innovative equipment and radioisotope solutions.

Europe Nuclear Imaging Solutions Industry Market Size (In Million)

Despite the strong growth trajectory, certain factors may present challenges. High acquisition costs of advanced nuclear imaging equipment and the specialized infrastructure required for handling radioisotopes can act as restraints. Stringent regulatory frameworks governing the use and disposal of radioactive materials also necessitate significant compliance efforts. However, the expanding applications of nuclear imaging beyond traditional diagnostics, such as in therapeutic guidance and personalized medicine, are opening new avenues for growth. The market is segmented by product into Equipment and Radioisotopes, with further sub-segmentation into SPECT and PET radioisotopes. Applications are similarly categorized, encompassing SPECT and PET applications in areas like cardiology, neurology, thyroid disorders, and oncology. Leading companies such as Siemens Healthineers, GE Healthcare, and Nordion Inc. are at the forefront, driving innovation and expanding market reach.

Europe Nuclear Imaging Solutions Industry Company Market Share

This comprehensive report delivers an in-depth analysis of the Europe Nuclear Imaging Solutions Industry, providing critical insights into market dynamics, technological advancements, and growth trajectories from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this study is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving landscape of medical imaging technologies in Europe. We delve into the intricate workings of the nuclear medicine market, examining the segments of SPECT radioisotopes (including Technetium-99m, Thallium-201, Gallium-67) and PET radioisotopes (such as Fluorine-18, Rubidium-82), as well as imaging equipment and applications like cardiology, neurology, oncology, and thyroid imaging. Discover emerging trends, strategic collaborations, and the impact of regulatory frameworks on the radiopharmaceutical market and the broader diagnostic imaging sector.

Europe Nuclear Imaging Solutions Industry Market Composition & Trends

The Europe Nuclear Imaging Solutions Industry is characterized by a dynamic interplay of established players and innovative entrants, with market concentration influenced by significant investments in advanced nuclear medicine equipment and novel radiopharmaceuticals. Innovation catalysts are primarily driven by the relentless pursuit of improved diagnostic accuracy and therapeutic efficacy, fueled by substantial R&D expenditures by leading companies such as Siemens Healthineers, GE Healthcare, and Canon Medical Systems Corporation. The regulatory landscape, overseen by bodies like the European Medicines Agency (EMA), plays a pivotal role in shaping market access and approval pathways for new diagnostic agents and imaging devices. Substitute products, while emerging, currently face challenges in matching the specificity and functional information offered by nuclear imaging techniques. End-user profiles are increasingly sophisticated, with a growing demand for personalized medicine and early disease detection, particularly in oncology and neurology. Merger and acquisition activities are significant, with strategic deals aimed at expanding product portfolios, enhancing technological capabilities, and consolidating market share within the Europe radiopharmacy market. For instance, ongoing consolidations and strategic partnerships underscore a trend towards vertical integration and enhanced supply chain efficiencies for crucial radioisotopes. The market share distribution reflects the dominance of key players in both equipment manufacturing and radioisotope production, with estimated market share values ranging significantly. The M&A deal values are projected to be in the range of tens to hundreds of millions of Euros, signifying substantial strategic investments aimed at capturing a larger share of this growing medical imaging Europe market.

- Market Concentration: Dominated by a few key global players with significant market share in both equipment and radioisotope segments.

- Innovation Catalysts: Advances in detector technology, development of novel radiotracers, and AI integration for image analysis.

- Regulatory Landscapes: Stringent approval processes by EMA and national health authorities influence product launches and market entry.

- Substitute Products: Challenges from advanced MRI and CT technologies, though often complementary rather than direct substitutes in specific diagnostic scenarios.

- End-User Profiles: Hospitals, diagnostic imaging centers, academic research institutions, and pharmaceutical companies seeking advanced diagnostic tools.

- M&A Activities: Frequent consolidation and strategic partnerships to gain competitive advantage and expand geographical reach. Expected M&A deal values in the range of €50 Million - €500 Million.

Europe Nuclear Imaging Solutions Industry Industry Evolution

The evolution of the Europe Nuclear Imaging Solutions Industry has been a narrative of continuous technological advancement, expanding diagnostic capabilities, and increasing adoption across a wider spectrum of medical applications. From its inception, the market has witnessed a steady upward trajectory, driven by an escalating global demand for accurate and early disease detection. The SPECT (Single-Photon Emission Computed Tomography) and PET (Positron Emission Tomography) modalities, integral to nuclear imaging, have undergone significant transformations. Early SPECT systems, primarily relying on Technetium-99m (TC-99m), have been augmented by more advanced SPECT/CT and SPECT/MRI hybrid systems, enhancing anatomical correlation and diagnostic precision. Similarly, PET technology, initially focused on oncology with Fluorine-18 (F-18) labeled tracers, has expanded its reach into neurology, cardiology, and infectious diseases with the development of novel PET radioisotopes like Rubidium-82 (RB-82) for cardiac imaging and Gallium-68 (Ga-68) for targeted therapies.

The growth in adoption metrics is directly linked to the improving understanding of disease pathophysiology and the development of targeted radiopharmaceuticals. For instance, the increased utilization of F-18 FDG PET/CT in oncology has become a standard of care for staging, restaging, and monitoring treatment response in various cancers, contributing to an estimated annual growth rate of 7-10% in the PET tracer market. The development of therapeutic radiopharmaceuticals, such as Novartis's Pluvicto (lutetium (177Lu) vipivotide tetraxetan) for prostate cancer, marks a paradigm shift towards theranostics, further accelerating market growth and fostering a synergistic relationship between diagnostic and therapeutic nuclear medicine. This evolution is also supported by significant investments in infrastructure, including the establishment of more radiopharmacies and cyclotron facilities across Europe, aiming to ensure a stable and accessible supply of short-lived radioisotopes. The forecast period from 2025 to 2033 anticipates continued robust growth, projected at a Compound Annual Growth Rate (CAGR) of approximately 6-8%, driven by technological innovations, expanding clinical indications, and an aging population with a higher incidence of chronic diseases requiring advanced diagnostic interventions. The market size is expected to grow from an estimated €8 Billion in 2025 to over €13 Billion by 2033.

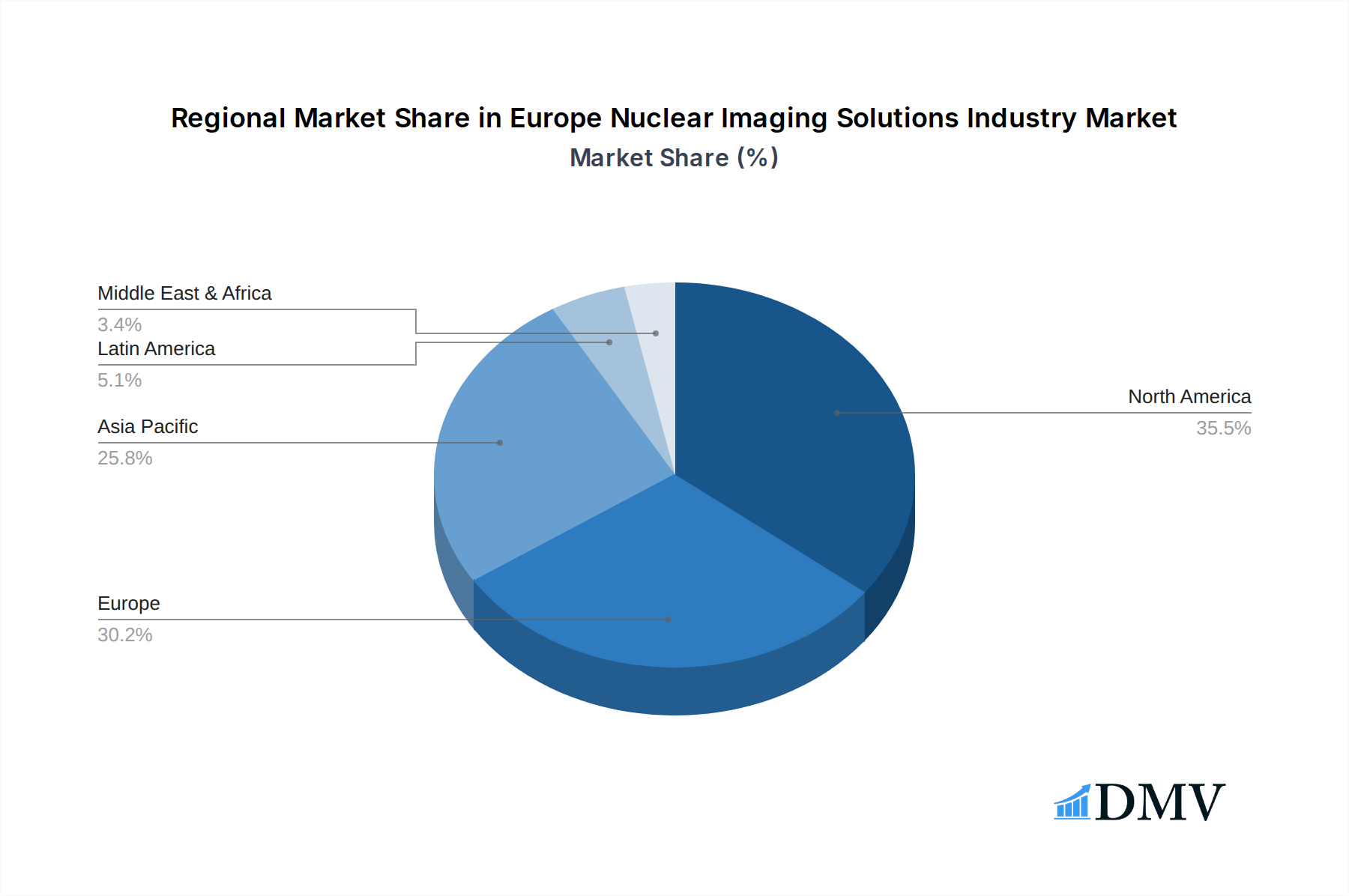

Leading Regions, Countries, or Segments in Europe Nuclear Imaging Solutions Industry

Within the Europe Nuclear Imaging Solutions Industry, Germany stands out as a dominant country, driven by its robust healthcare infrastructure, significant investment in advanced medical technology, and a high concentration of leading research institutions and pharmaceutical companies. The Product: Equipment segment, particularly advanced SPECT and PET/CT scanners, experiences substantial market share in Germany, reflecting a strong demand for cutting-edge diagnostic tools. This dominance is further amplified by the country's proactive approach to adopting new technologies and its favorable reimbursement policies for innovative medical procedures. The Application: PET Applications, with a strong emphasis on Oncology, is another key driver of Germany's leadership. The widespread use of F-18 FDG PET/CT for cancer diagnosis, staging, and treatment monitoring has cemented PET's crucial role in the German healthcare system, contributing significantly to the overall market value.

- Dominant Country: Germany, owing to strong healthcare infrastructure and high adoption of advanced technologies.

- Key Drivers in Germany:

- Investment Trends: Significant government and private sector investments in healthcare R&D and facility upgrades.

- Regulatory Support: Favorable reimbursement policies and streamlined approval processes for novel nuclear medicine devices and radiopharmaceuticals.

- Research & Development: Presence of leading research centers and pharmaceutical companies driving innovation in nuclear imaging.

- Clinical Demand: High prevalence of oncological and neurological diseases necessitating advanced diagnostic imaging.

- Dominant Segment (Application): PET Applications (Oncology). The increasing incidence of cancer and the proven efficacy of PET tracers like F-18 FDG for early detection and treatment management make this segment a primary growth engine. The market value for PET applications in oncology in Germany alone is estimated to exceed €1.5 Billion annually.

- Dominant Segment (Product): Equipment. The continuous upgrade cycle for PET/CT and SPECT/CT scanners, coupled with the introduction of next-generation hybrid imaging systems, fuels consistent demand for advanced imaging hardware. The estimated market value for nuclear imaging equipment in Germany is projected to reach over €1 Billion in 2025.

- Radioisotope Dominance: Technetium-99m (TC-99m) remains the most widely used SPECT radioisotope due to its versatility and established clinical applications in cardiology, neurology, and thyroid imaging. However, PET radioisotopes like Fluorine-18 (F-18) are experiencing rapid growth, particularly in oncology.

Europe Nuclear Imaging Solutions Industry Product Innovations

Product innovations within the Europe Nuclear Imaging Solutions Industry are rapidly advancing the field of diagnostic and therapeutic medicine. Key advancements include the development of novel radiotracers with enhanced specificity for various disease biomarkers, leading to earlier and more accurate diagnoses. For instance, the introduction of new PET tracers targeting specific protein expressions in neurodegenerative diseases like Alzheimer's offers unprecedented diagnostic capabilities. Furthermore, the integration of Artificial Intelligence (AI) into imaging software is revolutionizing image analysis, enabling faster interpretation, improved lesion detection, and more precise quantitative assessments. The development of more compact and cost-effective cyclotron systems is also democratizing access to short-lived PET radioisotopes, allowing for decentralized radiopharmaceutical production closer to patient care. These innovations are driving significant improvements in performance metrics such as spatial resolution, sensitivity, and diagnostic confidence, with new systems offering a xx% increase in lesion detection sensitivity compared to older generations.

Propelling Factors for Europe Nuclear Imaging Solutions Industry Growth

The Europe Nuclear Imaging Solutions Industry is propelled by several key factors. Technological advancements, including the development of more sensitive detectors and novel radiotracers, significantly enhance diagnostic accuracy. The increasing prevalence of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions creates a substantial and growing demand for advanced diagnostic imaging solutions. Furthermore, government initiatives and healthcare reforms across Europe are prioritizing early disease detection and personalized medicine, indirectly boosting the adoption of nuclear imaging. The growing emphasis on theranostics, combining diagnostic imaging with targeted radionuclide therapy, represents a significant growth opportunity, exemplified by the approval of treatments like Pluvicto.

Obstacles in the Europe Nuclear Imaging Solutions Industry Market

Despite robust growth, the Europe Nuclear Imaging Solutions Industry faces certain obstacles. The high cost of nuclear imaging equipment and radiopharmaceuticals can be a barrier to widespread adoption, particularly in resource-constrained healthcare settings. Stringent regulatory hurdles for the approval of new radioactive drugs and devices can lead to lengthy development timelines and significant R&D investments. Supply chain disruptions for key radioisotopes, especially short-lived ones like TC-99m, can impact the availability of diagnostic services. Furthermore, the need for specialized infrastructure, such as cyclotrons and radiopharmacies, presents a challenge for market expansion in certain regions. Competition from other advanced imaging modalities like MRI and CT, although often complementary, can also pose indirect pressures.

Future Opportunities in Europe Nuclear Imaging Solutions Industry

Emerging opportunities in the Europe Nuclear Imaging Solutions Industry are ripe for exploration. The burgeoning field of theranostics, combining diagnosis and therapy using radioligands, holds immense potential for treating diseases like prostate cancer and neuroendocrine tumors. The expansion of PET imaging into new clinical areas beyond oncology, such as cardiology and neurology, driven by the development of specific PET tracers, presents significant growth avenues. The increasing integration of AI and machine learning in image analysis and workflow optimization offers opportunities for enhanced efficiency and diagnostic precision. Furthermore, the growing demand for personalized medicine and precision diagnostics will continue to drive innovation in novel radioisotope and tracer development. The expansion of molecular imaging into rare diseases also represents an underserved market with substantial future potential.

Major Players in the Europe Nuclear Imaging Solutions Industry Ecosystem

- Nordion Inc

- Siemens Healthineers

- GE Healthcare

- Bracco Imaging SpA

- Cardinal Health Inc

- Novartis AG (Advanced Accelerator Applications)

- NTP Radioisotopes SOC

- Koninklijke Philips NV

- Canon Medical Systems Corporation

- Curium

- Merck KGaA (Sigma-Aldrich)

Key Developments in Europe Nuclear Imaging Solutions Industry Industry

- September 2023: Lantheus Holdings, Inc. announced that PYLARIFY AI data will be presented at the upcoming 2023 European Association of Nuclear Medicine (EANM) Annual Meeting in Vienna, Austria. This highlights advancements in AI-driven analysis of radiopharmaceutical imaging, promising enhanced diagnostic capabilities.

- December 2022: The European Commission (EC) approved Novartis's Pluvicto (INN: lutetium (177Lu) vipivotide tetraxetan). This approval for a targeted radioligand therapy in advanced prostate cancer signifies a major step forward in the theranostics revolution, integrating diagnostic imaging with therapeutic intervention and impacting the radiopharmaceutical market significantly.

Strategic Europe Nuclear Imaging Solutions Industry Market Forecast

The strategic Europe Nuclear Imaging Solutions Industry market forecast indicates continued robust growth driven by innovation and unmet clinical needs. The increasing adoption of theranostic approaches and the expansion of PET imaging into new clinical applications will be significant growth catalysts. Investments in advanced nuclear imaging equipment and the development of novel radiopharmaceuticals are expected to fuel market expansion. The focus on early disease detection and personalized medicine will further bolster demand, positioning the market for substantial growth in the coming years, with an estimated market size projected to reach over €13 Billion by 2033.

Europe Nuclear Imaging Solutions Industry Segmentation

-

1. Product

- 1.1. Equipment

-

1.2. Radioisotope

-

1.2.1. SPECT Radioisotopes

- 1.2.1.1. Technetium-99m (TC-99m)

- 1.2.1.2. Thallium-201 (TI-201)

- 1.2.1.3. Gallium(Ga-67)

- 1.2.1.4. Other SPECT Radioisotopes

-

1.2.2. PET Radioisotopes

- 1.2.2.1. Fluorine-18 (F-18)

- 1.2.2.2. Rubidium-82 (RB-82)

- 1.2.2.3. Other PET Radioisotopes

-

1.2.1. SPECT Radioisotopes

-

2. Application

-

2.1. SPECT Applications

- 2.1.1. Cardiology

- 2.1.2. Neurology

- 2.1.3. Thyroid

- 2.1.4. Other SPECT Applications

-

2.2. PET Applications

- 2.2.1. Oncology

- 2.2.2. Other PET Applications

-

2.1. SPECT Applications

Europe Nuclear Imaging Solutions Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

Europe Nuclear Imaging Solutions Industry Regional Market Share

Geographic Coverage of Europe Nuclear Imaging Solutions Industry

Europe Nuclear Imaging Solutions Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.34% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Equipment

- 5.1.2. Radioisotope

- 5.1.2.1. SPECT Radioisotopes

- 5.1.2.1.1. Technetium-99m (TC-99m)

- 5.1.2.1.2. Thallium-201 (TI-201)

- 5.1.2.1.3. Gallium(Ga-67)

- 5.1.2.1.4. Other SPECT Radioisotopes

- 5.1.2.2. PET Radioisotopes

- 5.1.2.2.1. Fluorine-18 (F-18)

- 5.1.2.2.2. Rubidium-82 (RB-82)

- 5.1.2.2.3. Other PET Radioisotopes

- 5.1.2.1. SPECT Radioisotopes

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. SPECT Applications

- 5.2.1.1. Cardiology

- 5.2.1.2. Neurology

- 5.2.1.3. Thyroid

- 5.2.1.4. Other SPECT Applications

- 5.2.2. PET Applications

- 5.2.2.1. Oncology

- 5.2.2.2. Other PET Applications

- 5.2.1. SPECT Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Italy

- 5.3.5. Spain

- 5.3.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Europe Nuclear Imaging Solutions Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Equipment

- 6.1.2. Radioisotope

- 6.1.2.1. SPECT Radioisotopes

- 6.1.2.1.1. Technetium-99m (TC-99m)

- 6.1.2.1.2. Thallium-201 (TI-201)

- 6.1.2.1.3. Gallium(Ga-67)

- 6.1.2.1.4. Other SPECT Radioisotopes

- 6.1.2.2. PET Radioisotopes

- 6.1.2.2.1. Fluorine-18 (F-18)

- 6.1.2.2.2. Rubidium-82 (RB-82)

- 6.1.2.2.3. Other PET Radioisotopes

- 6.1.2.1. SPECT Radioisotopes

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. SPECT Applications

- 6.2.1.1. Cardiology

- 6.2.1.2. Neurology

- 6.2.1.3. Thyroid

- 6.2.1.4. Other SPECT Applications

- 6.2.2. PET Applications

- 6.2.2.1. Oncology

- 6.2.2.2. Other PET Applications

- 6.2.1. SPECT Applications

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Germany Europe Nuclear Imaging Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Equipment

- 7.1.2. Radioisotope

- 7.1.2.1. SPECT Radioisotopes

- 7.1.2.1.1. Technetium-99m (TC-99m)

- 7.1.2.1.2. Thallium-201 (TI-201)

- 7.1.2.1.3. Gallium(Ga-67)

- 7.1.2.1.4. Other SPECT Radioisotopes

- 7.1.2.2. PET Radioisotopes

- 7.1.2.2.1. Fluorine-18 (F-18)

- 7.1.2.2.2. Rubidium-82 (RB-82)

- 7.1.2.2.3. Other PET Radioisotopes

- 7.1.2.1. SPECT Radioisotopes

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. SPECT Applications

- 7.2.1.1. Cardiology

- 7.2.1.2. Neurology

- 7.2.1.3. Thyroid

- 7.2.1.4. Other SPECT Applications

- 7.2.2. PET Applications

- 7.2.2.1. Oncology

- 7.2.2.2. Other PET Applications

- 7.2.1. SPECT Applications

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. United Kingdom Europe Nuclear Imaging Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Equipment

- 8.1.2. Radioisotope

- 8.1.2.1. SPECT Radioisotopes

- 8.1.2.1.1. Technetium-99m (TC-99m)

- 8.1.2.1.2. Thallium-201 (TI-201)

- 8.1.2.1.3. Gallium(Ga-67)

- 8.1.2.1.4. Other SPECT Radioisotopes

- 8.1.2.2. PET Radioisotopes

- 8.1.2.2.1. Fluorine-18 (F-18)

- 8.1.2.2.2. Rubidium-82 (RB-82)

- 8.1.2.2.3. Other PET Radioisotopes

- 8.1.2.1. SPECT Radioisotopes

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. SPECT Applications

- 8.2.1.1. Cardiology

- 8.2.1.2. Neurology

- 8.2.1.3. Thyroid

- 8.2.1.4. Other SPECT Applications

- 8.2.2. PET Applications

- 8.2.2.1. Oncology

- 8.2.2.2. Other PET Applications

- 8.2.1. SPECT Applications

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. France Europe Nuclear Imaging Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Equipment

- 9.1.2. Radioisotope

- 9.1.2.1. SPECT Radioisotopes

- 9.1.2.1.1. Technetium-99m (TC-99m)

- 9.1.2.1.2. Thallium-201 (TI-201)

- 9.1.2.1.3. Gallium(Ga-67)

- 9.1.2.1.4. Other SPECT Radioisotopes

- 9.1.2.2. PET Radioisotopes

- 9.1.2.2.1. Fluorine-18 (F-18)

- 9.1.2.2.2. Rubidium-82 (RB-82)

- 9.1.2.2.3. Other PET Radioisotopes

- 9.1.2.1. SPECT Radioisotopes

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. SPECT Applications

- 9.2.1.1. Cardiology

- 9.2.1.2. Neurology

- 9.2.1.3. Thyroid

- 9.2.1.4. Other SPECT Applications

- 9.2.2. PET Applications

- 9.2.2.1. Oncology

- 9.2.2.2. Other PET Applications

- 9.2.1. SPECT Applications

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Italy Europe Nuclear Imaging Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Equipment

- 10.1.2. Radioisotope

- 10.1.2.1. SPECT Radioisotopes

- 10.1.2.1.1. Technetium-99m (TC-99m)

- 10.1.2.1.2. Thallium-201 (TI-201)

- 10.1.2.1.3. Gallium(Ga-67)

- 10.1.2.1.4. Other SPECT Radioisotopes

- 10.1.2.2. PET Radioisotopes

- 10.1.2.2.1. Fluorine-18 (F-18)

- 10.1.2.2.2. Rubidium-82 (RB-82)

- 10.1.2.2.3. Other PET Radioisotopes

- 10.1.2.1. SPECT Radioisotopes

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. SPECT Applications

- 10.2.1.1. Cardiology

- 10.2.1.2. Neurology

- 10.2.1.3. Thyroid

- 10.2.1.4. Other SPECT Applications

- 10.2.2. PET Applications

- 10.2.2.1. Oncology

- 10.2.2.2. Other PET Applications

- 10.2.1. SPECT Applications

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Spain Europe Nuclear Imaging Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Equipment

- 11.1.2. Radioisotope

- 11.1.2.1. SPECT Radioisotopes

- 11.1.2.1.1. Technetium-99m (TC-99m)

- 11.1.2.1.2. Thallium-201 (TI-201)

- 11.1.2.1.3. Gallium(Ga-67)

- 11.1.2.1.4. Other SPECT Radioisotopes

- 11.1.2.2. PET Radioisotopes

- 11.1.2.2.1. Fluorine-18 (F-18)

- 11.1.2.2.2. Rubidium-82 (RB-82)

- 11.1.2.2.3. Other PET Radioisotopes

- 11.1.2.1. SPECT Radioisotopes

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. SPECT Applications

- 11.2.1.1. Cardiology

- 11.2.1.2. Neurology

- 11.2.1.3. Thyroid

- 11.2.1.4. Other SPECT Applications

- 11.2.2. PET Applications

- 11.2.2.1. Oncology

- 11.2.2.2. Other PET Applications

- 11.2.1. SPECT Applications

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Rest of Europe Europe Nuclear Imaging Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product

- 12.1.1. Equipment

- 12.1.2. Radioisotope

- 12.1.2.1. SPECT Radioisotopes

- 12.1.2.1.1. Technetium-99m (TC-99m)

- 12.1.2.1.2. Thallium-201 (TI-201)

- 12.1.2.1.3. Gallium(Ga-67)

- 12.1.2.1.4. Other SPECT Radioisotopes

- 12.1.2.2. PET Radioisotopes

- 12.1.2.2.1. Fluorine-18 (F-18)

- 12.1.2.2.2. Rubidium-82 (RB-82)

- 12.1.2.2.3. Other PET Radioisotopes

- 12.1.2.1. SPECT Radioisotopes

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. SPECT Applications

- 12.2.1.1. Cardiology

- 12.2.1.2. Neurology

- 12.2.1.3. Thyroid

- 12.2.1.4. Other SPECT Applications

- 12.2.2. PET Applications

- 12.2.2.1. Oncology

- 12.2.2.2. Other PET Applications

- 12.2.1. SPECT Applications

- 12.1. Market Analysis, Insights and Forecast - by Product

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Nordion Inc

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Siemens Healthineers

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 GE Healthcare

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Bracco Imaging SpA

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Cardinal Health Inc

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Novartis AG (Advanced Accelerator Applications)

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 NTP Radioisotopes SOC

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Koninklijke Philips NV

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Canon Medical Systems Corporation

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Curium

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Merck KGaA (Sigma-Aldrich)*List Not Exhaustive

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.1 Nordion Inc

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Europe Nuclear Imaging Solutions Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Nuclear Imaging Solutions Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 2: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 5: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 8: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 9: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 11: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 14: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 15: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 17: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 18: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 20: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 21: Europe Nuclear Imaging Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Nuclear Imaging Solutions Industry?

The projected CAGR is approximately 3.34%.

2. Which companies are prominent players in the Europe Nuclear Imaging Solutions Industry?

Key companies in the market include Nordion Inc, Siemens Healthineers, GE Healthcare, Bracco Imaging SpA, Cardinal Health Inc, Novartis AG (Advanced Accelerator Applications), NTP Radioisotopes SOC, Koninklijke Philips NV, Canon Medical Systems Corporation, Curium, Merck KGaA (Sigma-Aldrich)*List Not Exhaustive.

3. What are the main segments of the Europe Nuclear Imaging Solutions Industry?

The market segments include Product, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.22 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Prevalence of Cancer and Cardiac Disorders; Growth in Applications of Nuclear Medicine and Imaging and Rising Technological Advancements.

6. What are the notable trends driving market growth?

Equipment Segment Expects to Witness Significant Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Regulatory Issues and Lack of Reimbursement.

8. Can you provide examples of recent developments in the market?

September 2023: Lantheus Holdings, Inc. reported PYLARIFY AI data will be presented at the upcoming 2023 European Association of Nuclear Medicine (EANM) Annual Meeting, which will be held in Vienna, Austria.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Nuclear Imaging Solutions Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Nuclear Imaging Solutions Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Nuclear Imaging Solutions Industry?

To stay informed about further developments, trends, and reports in the Europe Nuclear Imaging Solutions Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence