Key Insights

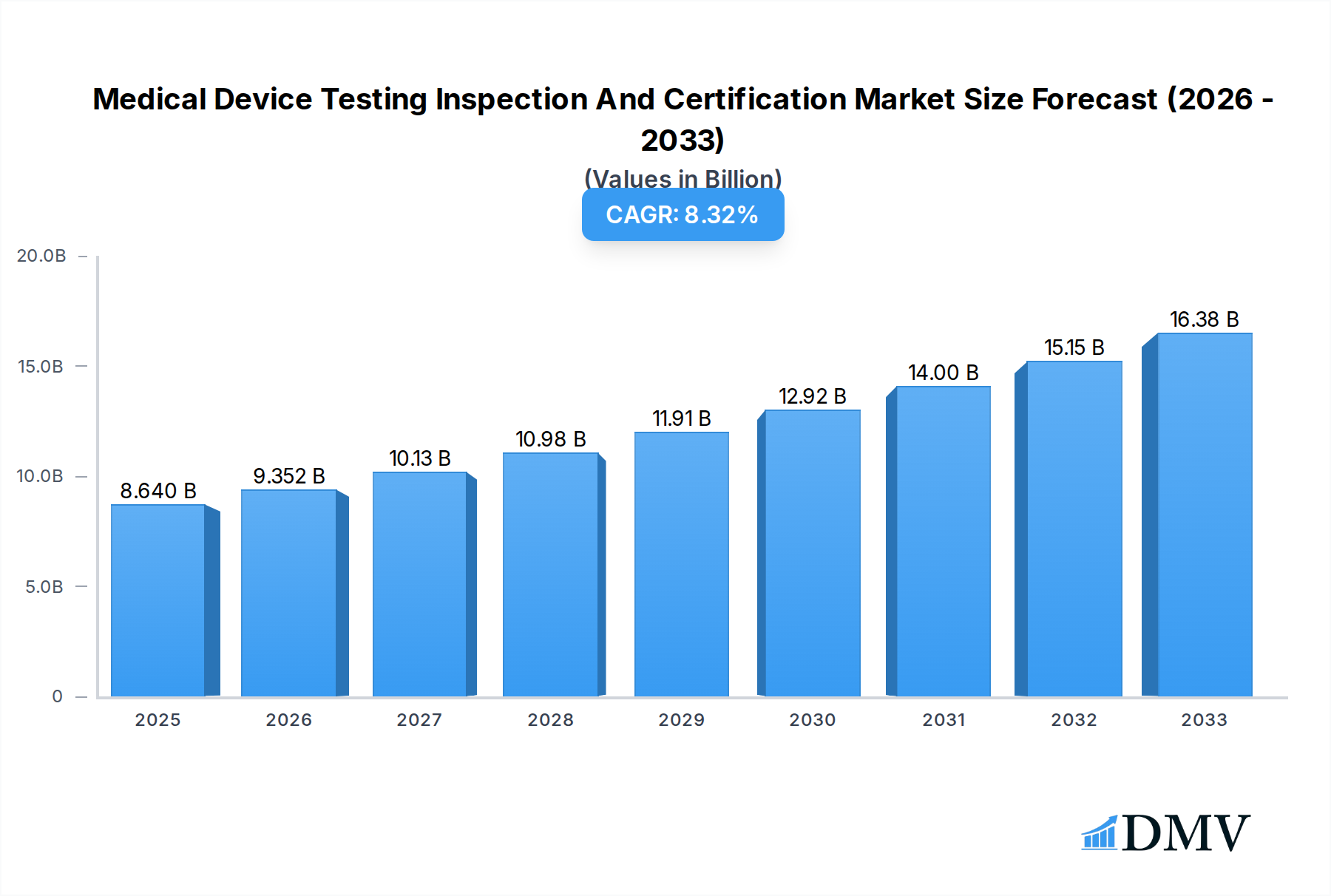

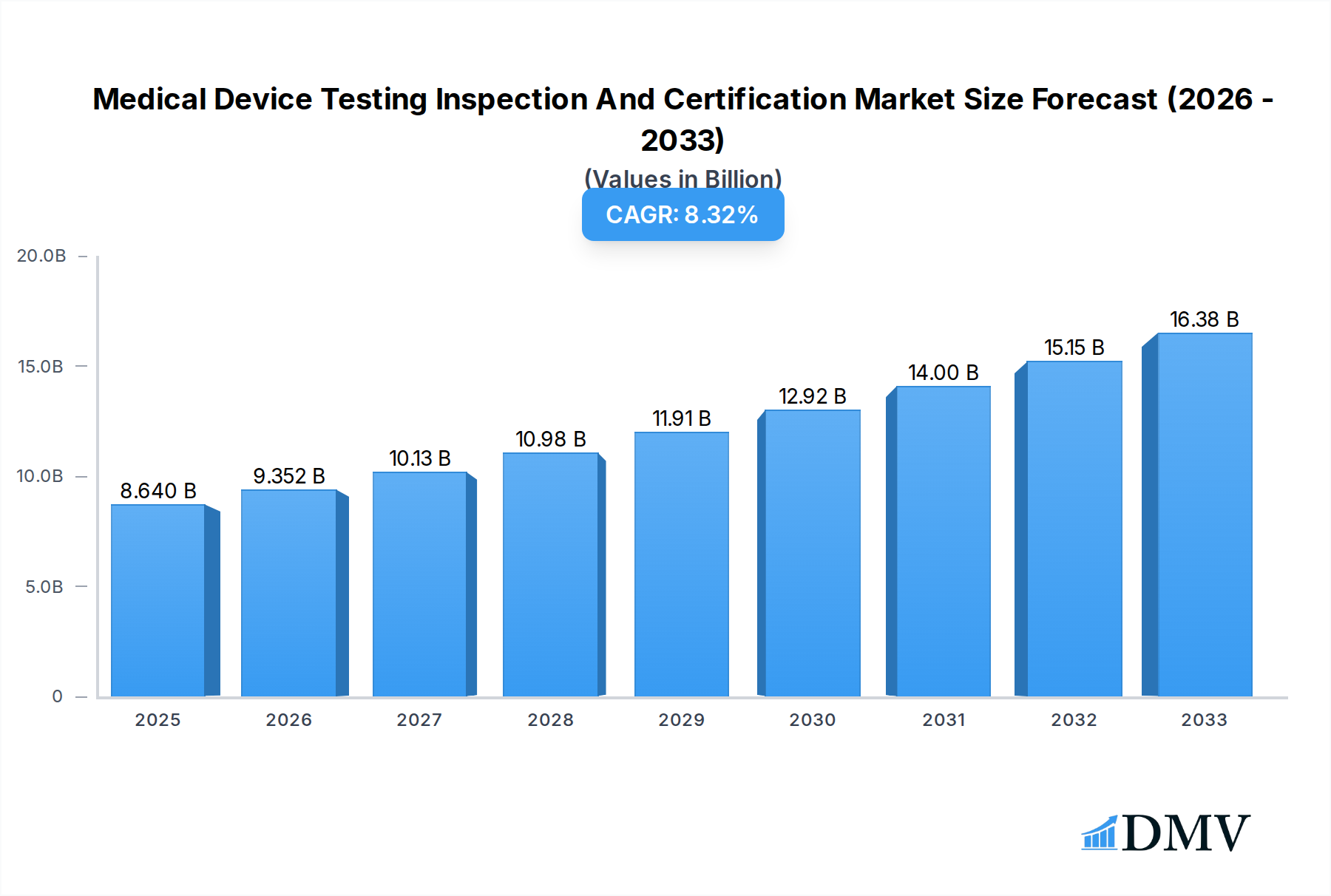

The global Medical Device Testing, Inspection, and Certification (TIC) market is poised for significant expansion, reaching an estimated USD 8.64 billion in 2025 and exhibiting a robust Compound Annual Growth Rate (CAGR) of 8.3%. This growth is propelled by several key drivers, including increasingly stringent regulatory landscapes worldwide, the continuous innovation and introduction of novel medical technologies, and a heightened global focus on patient safety and product quality. As regulatory bodies like the FDA, EMA, and others refine and enforce compliance standards, the demand for comprehensive testing, meticulous inspection, and reliable certification services intensifies. Furthermore, the burgeoning complexity of medical devices, from sophisticated active devices like pacemakers and imaging equipment to non-active devices such as surgical instruments and implants, necessitates specialized expertise and rigorous validation processes to ensure efficacy and safety for end-users.

Medical Device Testing Inspection And Certification Market Size (In Billion)

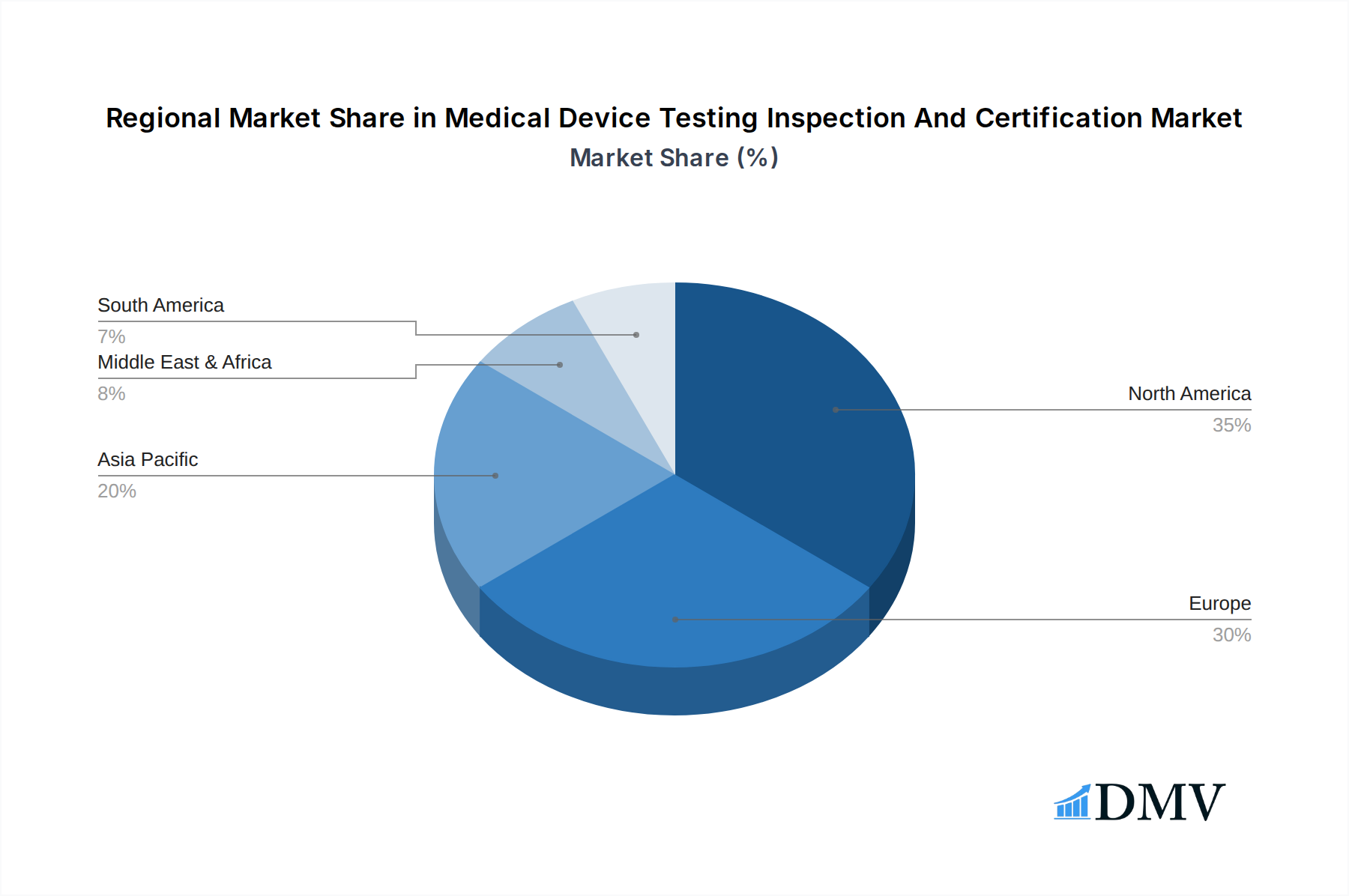

The market segmentation reflects the diverse needs within the medical device industry. The demand for both in-house and outsourced TIC services is substantial, with outsourcing continuing to gain traction as manufacturers seek specialized expertise and cost-efficiencies. Geographically, North America and Europe currently dominate the market due to their established healthcare infrastructures, advanced regulatory frameworks, and high concentration of leading medical device manufacturers. However, the Asia Pacific region is emerging as a high-growth area, driven by a rapidly expanding medical device manufacturing base, increasing healthcare expenditure, and a growing awareness of quality and safety standards. Key restraints, such as the high cost of testing and certification processes and the scarcity of skilled professionals, are being addressed through technological advancements and strategic partnerships. Nonetheless, the overarching commitment to patient well-being and the global drive for reliable and safe medical interventions will continue to fuel the upward trajectory of the Medical Device TIC market.

Medical Device Testing Inspection And Certification Company Market Share

Medical Device Testing Inspection And Certification Market Analysis Report

This comprehensive report delves into the intricate landscape of the Medical Device Testing Inspection and Certification market, providing an in-depth analysis of its current state and future trajectory. With a Study Period spanning from 2019 to 2033, including a Base Year of 2025 and a Forecast Period from 2025 to 2033, this report leverages historical data from 2019 to 2024 to offer unparalleled insights. The Estimated Year for 2025 serves as a crucial benchmark. The market for medical device testing services, medical device certification, and ISO 13485 compliance is projected to witness significant expansion, driven by evolving regulatory frameworks and the increasing demand for safe and effective medical technologies. This report examines market concentration, innovation catalysts, regulatory landscapes, substitute products, end-user profiles, and M&A activities, offering a holistic view of the medical device compliance ecosystem. It is an essential resource for stakeholders seeking to navigate the complexities of medical device regulatory affairs, medical device quality management, and global medical device market access.

Medical Device Testing Inspection And Certification Market Composition & Trends

The medical device testing inspection and certification market exhibits a moderately concentrated structure, with key players like SGS Group, Element Materials Technology Group, Intertek, Dekra Certification, TUV SUD, UL LLC, TUV Rheinland, Merieux NutriSciences, F2 Labs, Eurofins Scientific, Freyr Solutions, and Smithers holding substantial market share. Innovation catalysts are primarily driven by advancements in diagnostic technologies, wearable medical devices, and the increasing integration of artificial intelligence in healthcare, necessitating rigorous medical device testing and validation. The evolving regulatory landscape, including stringent FDA regulations and European Union Medical Device Regulation (EU MDR) compliance, is a paramount driver for medical device certification services. Substitute products are limited due to the critical nature of medical device safety, but advancements in in-vitro diagnostics offer some alternatives in specific testing niches. End-user profiles range from small-scale innovative startups to multinational giants, all requiring robust medical device quality assurance and pre-market notification services. Mergers and acquisitions (M&A) activity is notable, with significant deal values in the hundreds of billions, as larger entities seek to expand their service portfolios and geographical reach in the medical device regulatory consulting domain. For instance, the acquisition of specialized biocompatibility testing firms by broader testing conglomerates underscores the trend towards comprehensive medical device testing solutions.

Medical Device Testing Inspection And Certification Industry Evolution

The medical device testing inspection and certification industry has undergone a remarkable evolution, mirroring the rapid advancements in the medical technology sector. Historically, the focus was primarily on basic safety and efficacy testing. However, the present landscape is characterized by an ever-increasing complexity in product design and functionality, demanding more sophisticated medical device testing solutions. The global medical device market has seen consistent growth, with the medical device testing, inspection, and certification market outpacing it due to heightened regulatory scrutiny and a growing emphasis on patient safety. Market growth trajectories are consistently upward, with an average annual growth rate projected to be in the low double-digit percentages throughout the forecast period. Technological advancements have been a significant evolutionary force, with the adoption of advanced simulation techniques, sophisticated material analysis, and automated testing protocols becoming commonplace for medical device validation. This has led to improved accuracy and efficiency in medical device quality control. Shifting consumer demands, influenced by a greater awareness of healthcare outcomes and a desire for personalized medicine, are also reshaping the industry. Manufacturers are increasingly investing in medical device risk management and post-market surveillance, which in turn fuels the demand for comprehensive medical device testing and compliance services. The rise of connected medical devices and IoT in healthcare has introduced new testing paradigms, particularly in cybersecurity and data integrity, creating new revenue streams for medical device testing companies. Furthermore, the increasing prevalence of chronic diseases and an aging global population are driving demand for a wider array of medical devices, from simple disposables to complex implantable devices, each requiring specialized medical device testing and regulatory support. The medical device regulatory consulting market has also expanded significantly as manufacturers navigate intricate international compliance requirements for FDA clearance and CE marking.

Leading Regions, Countries, or Segments in Medical Device Testing Inspection And Certification

The medical device testing inspection and certification market demonstrates significant regional and segmental variations. In terms of application, Active Medical Devices currently command a larger share, driven by the increasing demand for sophisticated diagnostic equipment, therapeutic devices, and implantable electronics. The development of advanced imaging technologies, robotic surgical systems, and smart wearables contributes significantly to this segment's dominance. Non-Active Medical Devices are also experiencing robust growth, fueled by the widespread use of surgical instruments, implants, and consumables, though their testing requirements are generally less complex than active counterparts.

From a type perspective, the Outsourced segment is leading the market. This trend is propelled by several key drivers:

- Cost-Effectiveness and Expertise: Many medical device manufacturers, especially smaller companies and startups, find it more economical and efficient to outsource their testing, inspection, and certification needs to specialized third-party providers rather than investing in in-house capabilities, which can require substantial capital expenditure and specialized personnel. This access to specialized expertise is invaluable for navigating complex regulatory compliance for medical device registration.

- Regulatory Burden and Specialization: The ever-evolving and increasingly stringent global regulatory landscape (e.g., FDA, EU MDR, Health Canada) necessitates deep expertise in specific testing protocols and documentation requirements. Outsourced providers often possess this specialized knowledge and accreditation, ensuring compliance with stringent standards for ISO 17025 accreditation and medical device approval.

- Focus on Core Competencies: By outsourcing non-core functions like testing and certification, manufacturers can concentrate their resources and efforts on research and development, product innovation, and market expansion, thereby accelerating their time to market for new medical devices.

- Access to Global Markets: Third-party testing and certification bodies are often accredited to conduct testing and issue certificates recognized in multiple international markets, facilitating global market access for medical device companies. This is crucial for navigating international medical device regulations.

- Technological Advancements and Investment: Leading testing organizations continually invest in cutting-edge testing equipment and methodologies, providing manufacturers with access to state-of-the-art testing capabilities that might be prohibitively expensive to maintain in-house. This includes advanced biocompatibility testing, sterilization validation, and electrical safety testing.

The dominance of the outsourced model is further reinforced by the growing complexity of medical device quality management systems and the need for independent verification to ensure product safety and efficacy, thus bolstering confidence in medical device market surveillance. The United States and European Union remain dominant geographical regions due to their large medical device markets and robust regulatory frameworks, driving significant demand for medical device regulatory affairs consulting and product testing services.

Medical Device Testing Inspection And Certification Product Innovations

Product innovations in medical device testing inspection and certification are largely focused on enhancing efficiency, accuracy, and comprehensiveness. Advancements include AI-powered data analysis for faster interpretation of test results, sophisticated simulation software for predictive testing of active medical devices and non-active medical devices, and the development of modular testing platforms for greater flexibility. These innovations aim to reduce time to market for medical devices and ensure robust regulatory compliance, particularly with evolving standards for connected medical devices and cybersecurity. Unique selling propositions lie in the ability to offer end-to-end medical device compliance solutions, from initial design review to post-market surveillance, supported by extensive ISO 13485 certification expertise.

Propelling Factors for Medical Device Testing Inspection And Certification Growth

The medical device testing inspection and certification market is propelled by a confluence of powerful factors. Stringent global regulatory reforms, such as the EU MDR and FDA's evolving requirements, mandate rigorous medical device testing and certification for market entry and continued compliance. Technological advancements in medical devices, including the proliferation of wearable medical devices and AI-driven diagnostics, necessitate advanced testing protocols to ensure safety and efficacy. A growing emphasis on patient safety and product quality, coupled with an aging global population and rising prevalence of chronic diseases, fuels the demand for reliable medical technologies, thereby increasing the need for independent medical device quality assurance. Economic growth in emerging markets also contributes, as these regions expand their healthcare infrastructure and regulatory oversight, creating new opportunities for medical device regulatory consulting and testing services.

Obstacles in the Medical Device Testing Inspection And Certification Market

Despite robust growth, the medical device testing inspection and certification market faces several significant obstacles. The increasing complexity and divergence of international medical device regulations pose substantial challenges for manufacturers seeking global market access. The high cost associated with comprehensive medical device testing and certification, particularly for novel or complex devices, can be a barrier for smaller companies. Supply chain disruptions and geopolitical uncertainties can impact the availability of specialized testing equipment and raw materials, indirectly affecting testing timelines. Intense competition among medical device testing companies also puts pressure on pricing, potentially impacting profitability. Furthermore, the rapid pace of technological innovation often outstrips the development of corresponding standardized testing methodologies, creating uncertainty in the medical device validation process.

Future Opportunities in Medical Device Testing Inspection And Certification

Emerging opportunities in the medical device testing inspection and certification market are abundant. The burgeoning field of digital health, encompassing telehealth, remote patient monitoring, and AI-powered medical applications, presents a significant demand for specialized cybersecurity, data integrity, and interoperability testing. The growing focus on personalized medicine and advanced therapies, such as gene and cell therapies, will require novel biocompatibility testing and safety assessment methodologies. Expansion into underdeveloped and developing markets with improving healthcare infrastructure offers substantial growth potential for medical device regulatory consulting and certification services. Furthermore, the increasing demand for sustainable and environmentally friendly medical devices is opening avenues for medical device environmental testing and lifecycle assessment services.

Major Players in the Medical Device Testing Inspection And Certification Ecosystem

- SGS Group

- Element Materials Technology Group

- Intertek

- Dekra Certification

- TUV SUD

- UL LLC

- TUV Rheinland

- Merieux NutriSciences

- F2 Labs

- Eurofins Scientific

- Freyr Solutions

- Smithers

Key Developments in Medical Device Testing Inspection And Certification Industry

- 2023 July: Introduction of new FDA guidance on cybersecurity for medical devices, intensifying the need for robust medical device cybersecurity testing.

- 2023 September: EU MDR implementation deadline shifts, leading to increased demand for medical device certification services and regulatory affairs consulting to meet compliance.

- 2024 January: Major acquisitions in the testing sector, with leading providers expanding their service offerings in biocompatibility testing and sterilization validation.

- 2024 March: Rise of AI in diagnostic imaging drives demand for specialized medical device testing and validation of AI algorithms and associated hardware.

- 2024 May: Focus on sustainability leads to increased inquiries for medical device environmental testing and lifecycle assessments.

Strategic Medical Device Testing Inspection And Certification Market Forecast

The strategic forecast for the medical device testing inspection and certification market is overwhelmingly positive, driven by an unyielding commitment to patient safety and increasingly stringent global regulations. Future growth will be significantly influenced by the expansion of digital health technologies, necessitating advanced cybersecurity and interoperability testing for connected medical devices. The continuous innovation in active and non-active medical devices, coupled with the demand for their global market access, will sustain robust demand for medical device certification and regulatory compliance services. Emerging economies represent a substantial untapped market, offering opportunities for medical device regulatory consulting and the establishment of accredited testing facilities. Strategic players will focus on expanding their service portfolios to encompass these new technological frontiers and geographical regions, ensuring comprehensive medical device quality assurance and facilitating pre-market notification and approval processes worldwide.

Medical Device Testing Inspection And Certification Segmentation

-

1. Application

- 1.1. Active Medical Devices

- 1.2. Non-Active Medical Devices

-

2. Type

- 2.1. In-house

- 2.2. Outsourced

Medical Device Testing Inspection And Certification Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Device Testing Inspection And Certification Regional Market Share

Geographic Coverage of Medical Device Testing Inspection And Certification

Medical Device Testing Inspection And Certification REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Device Testing Inspection And Certification Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Active Medical Devices

- 5.1.2. Non-Active Medical Devices

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. In-house

- 5.2.2. Outsourced

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical Device Testing Inspection And Certification Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Active Medical Devices

- 6.1.2. Non-Active Medical Devices

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. In-house

- 6.2.2. Outsourced

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical Device Testing Inspection And Certification Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Active Medical Devices

- 7.1.2. Non-Active Medical Devices

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. In-house

- 7.2.2. Outsourced

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical Device Testing Inspection And Certification Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Active Medical Devices

- 8.1.2. Non-Active Medical Devices

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. In-house

- 8.2.2. Outsourced

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical Device Testing Inspection And Certification Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Active Medical Devices

- 9.1.2. Non-Active Medical Devices

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. In-house

- 9.2.2. Outsourced

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical Device Testing Inspection And Certification Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Active Medical Devices

- 10.1.2. Non-Active Medical Devices

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. In-house

- 10.2.2. Outsourced

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 SGS Group

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Element Materials Technology Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Intertek

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Dekra Certification

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 TUV SUD

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 UL LLC

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 TUV Rheinland

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Merieux NutriSciences

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 F2 Labs

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Eurofins Scientific

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Freyr Solutions

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Smithers

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 SGS Group

List of Figures

- Figure 1: Global Medical Device Testing Inspection And Certification Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Medical Device Testing Inspection And Certification Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Medical Device Testing Inspection And Certification Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Device Testing Inspection And Certification Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Medical Device Testing Inspection And Certification Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Medical Device Testing Inspection And Certification Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Medical Device Testing Inspection And Certification Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Device Testing Inspection And Certification Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Medical Device Testing Inspection And Certification Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Device Testing Inspection And Certification Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Medical Device Testing Inspection And Certification Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Medical Device Testing Inspection And Certification Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Medical Device Testing Inspection And Certification Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Device Testing Inspection And Certification Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Medical Device Testing Inspection And Certification Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Device Testing Inspection And Certification Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Medical Device Testing Inspection And Certification Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Medical Device Testing Inspection And Certification Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Medical Device Testing Inspection And Certification Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Device Testing Inspection And Certification Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Device Testing Inspection And Certification Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Device Testing Inspection And Certification Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Medical Device Testing Inspection And Certification Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Medical Device Testing Inspection And Certification Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Device Testing Inspection And Certification Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Device Testing Inspection And Certification Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Device Testing Inspection And Certification Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Device Testing Inspection And Certification Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Medical Device Testing Inspection And Certification Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Medical Device Testing Inspection And Certification Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Device Testing Inspection And Certification Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Medical Device Testing Inspection And Certification Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Device Testing Inspection And Certification Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Device Testing Inspection And Certification?

The projected CAGR is approximately 8.3%.

2. Which companies are prominent players in the Medical Device Testing Inspection And Certification?

Key companies in the market include SGS Group, Element Materials Technology Group, Intertek, Dekra Certification, TUV SUD, UL LLC, TUV Rheinland, Merieux NutriSciences, F2 Labs, Eurofins Scientific, Freyr Solutions, Smithers.

3. What are the main segments of the Medical Device Testing Inspection And Certification?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Device Testing Inspection And Certification," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Device Testing Inspection And Certification report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Device Testing Inspection And Certification?

To stay informed about further developments, trends, and reports in the Medical Device Testing Inspection And Certification, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence