Key Insights

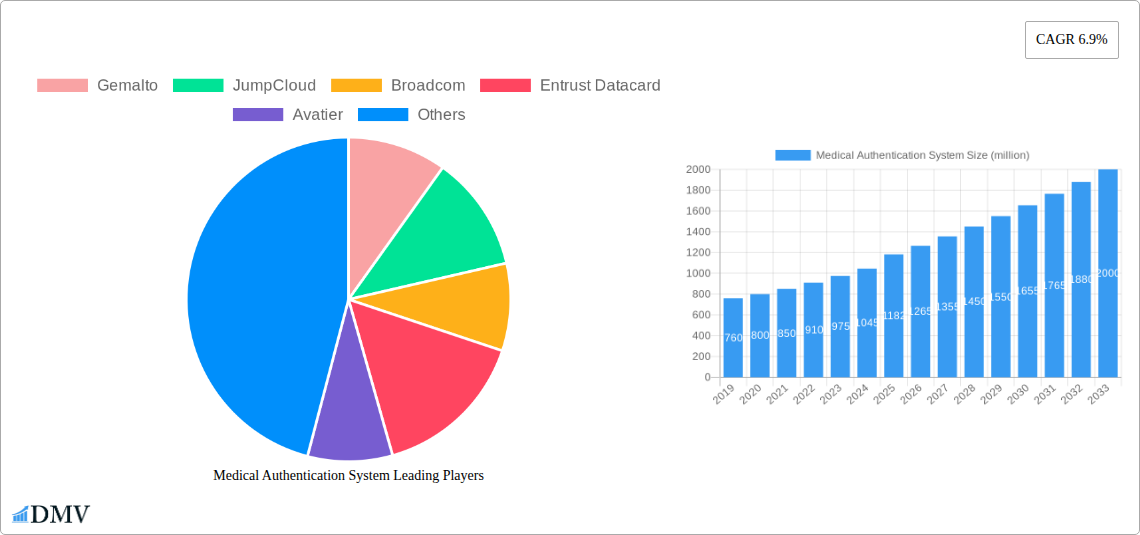

The Medical Authentication System market is poised for substantial growth, projected to reach \$1182 million by 2025, with a Compound Annual Growth Rate (CAGR) of 6.9% expected to propel it through the forecast period of 2025-2033. This robust expansion is primarily driven by an escalating need for enhanced patient data security, stringent regulatory compliance, and the growing adoption of digital health solutions. The increasing digitization of healthcare records and the rise of telemedicine necessitate secure methods for verifying identities and safeguarding sensitive medical information. The market's segmentation reveals a significant focus on applications within Outpatient Departments and Operating Rooms, areas where accurate patient identification is critical for treatment and procedural safety. Doctor's and Patient's Identity Authentication represent the most crucial types, underlining the core function of these systems in ensuring the right person receives the right care and that medical data integrity is maintained. Leading companies like Gemalto, JumpCloud, Broadcom, and Entrust Datacard are actively innovating, introducing advanced authentication technologies to meet the evolving demands of the healthcare sector.

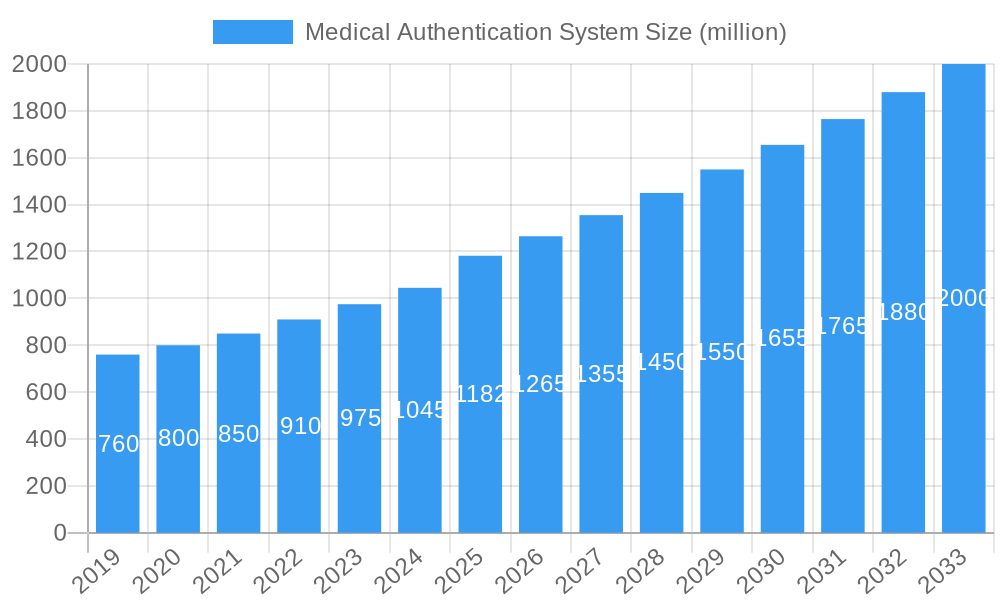

Medical Authentication System Market Size (In Million)

Further bolstering this market are key trends such as the integration of multi-factor authentication (MFA) and biometrics, offering a more secure and user-friendly approach to identity verification. The push towards interoperability of healthcare systems also demands standardized and secure authentication protocols. However, the market faces certain restraints, including the high initial investment costs associated with implementing sophisticated authentication systems and potential challenges in user adoption and training. Geographically, North America and Europe are expected to dominate the market due to their well-established healthcare infrastructures and early adoption of advanced technologies. Asia Pacific, driven by the growing economies of China and India and a burgeoning healthcare sector, presents significant growth opportunities. The continuous evolution of cyber threats targeting healthcare data will undoubtedly spur further innovation and investment in Medical Authentication Systems, solidifying their indispensable role in modern healthcare delivery.

Medical Authentication System Company Market Share

This in-depth report provides a definitive analysis of the Medical Authentication System market, forecasting its trajectory from 2019 to 2033. We delve into the intricate market composition, evolutionary trends, leading regional and segmental dominance, groundbreaking product innovations, critical growth drivers, formidable obstacles, and promising future opportunities. With a base year of 2025 and a forecast period extending to 2033, this report offers actionable insights for stakeholders seeking to navigate the dynamic landscape of secure healthcare access and data protection. Our meticulous research covers key players, historical performance, and projected market shifts, ensuring a holistic understanding of this vital sector.

Medical Authentication System Market Composition & Trends

The Medical Authentication System market exhibits a dynamic and evolving composition, driven by increasing demands for patient data security and regulatory compliance. Market concentration is moderate, with several key players vying for dominance. Innovation is primarily catalyzed by advancements in biometric technologies, cloud-based solutions, and artificial intelligence for threat detection. The regulatory landscape, including HIPAA and GDPR, continues to shape market strategies, emphasizing robust data protection measures. Substitute products, while present in the form of less secure access methods, are increasingly being phased out due to heightened security concerns. End-user profiles range from large hospital networks to specialized clinics, each with unique authentication needs. Merger and acquisition (M&A) activities are on the rise, as larger entities seek to consolidate market share and expand their technology portfolios. Recent M&A deals have seen valuations in the range of hundreds of millions to potentially over a billion dollars, reflecting the strategic importance of secure medical authentication solutions. Market share distribution is highly contested, with leading players holding varying percentages across different segments and regions, often in the tens of millions of dollars annually.

- Market Concentration: Moderate, with a mix of established giants and agile innovators.

- Innovation Catalysts: Biometrics, AI-driven threat intelligence, cloud security, blockchain integration.

- Regulatory Landscapes: HIPAA, GDPR, PIPEDA, and regional data privacy laws are primary drivers.

- Substitute Products: Traditional password-based systems, physical key cards (increasingly obsolete).

- End-User Profiles: Hospitals, clinics, diagnostic labs, telehealth providers, research institutions.

- M&A Activities: Strategic acquisitions to gain market share, acquire new technologies, and expand service offerings.

Medical Authentication System Industry Evolution

The Medical Authentication System industry has undergone significant evolution over the historical period of 2019–2024, charting a course of robust growth and technological sophistication. This evolution is intrinsically linked to the escalating need for robust cybersecurity within healthcare ecosystems, driven by the proliferation of electronic health records (EHRs), the rise of telemedicine, and the increasing threat of sophisticated cyberattacks targeting sensitive patient data. During the historical period, market growth trajectories were consistently upward, with an estimated compound annual growth rate (CAGR) of around 12-15% annually, translating into billions of dollars in market value expansion. Technological advancements have been the cornerstone of this evolution. Early authentication methods, primarily reliant on passwords and basic multi-factor authentication (MFA), have given way to more advanced solutions. The adoption of biometric authentication, including fingerprint scanning, facial recognition, and iris scanning, has surged, offering enhanced security and user convenience. Furthermore, the integration of AI and machine learning has enabled sophisticated anomaly detection and behavioral analytics, proactively identifying and mitigating potential security breaches. Shifting consumer demands, particularly from healthcare professionals and patients alike, have underscored the imperative for seamless, secure, and compliant access to medical information and systems. The pandemic accelerated the adoption of remote access solutions, further solidifying the demand for reliable and secure authentication methods. The market is projected to continue its upward trajectory, with an estimated CAGR of 14-17% during the forecast period of 2025–2033, reaching market sizes well into the tens of billions of dollars. This sustained growth will be fueled by ongoing digital transformation in healthcare, stringent regulatory enforcement, and the continuous innovation pipeline from leading vendors. Adoption metrics for advanced authentication methods, such as biometric solutions, have seen a significant increase, with adoption rates climbing from less than 30% in 2019 to over 60% in 2024 for certain healthcare segments, and are expected to reach over 85% by 2033.

Leading Regions, Countries, or Segments in Medical Authentication System

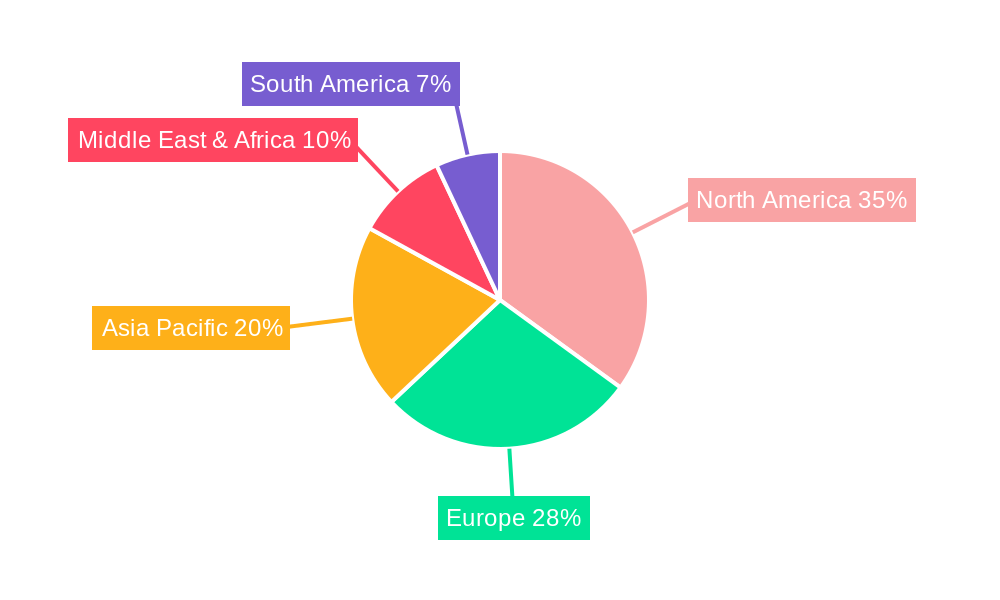

The Medical Authentication System market's dominance is a multifaceted interplay of regional strengths, governmental initiatives, and segment-specific demands. North America, particularly the United States, consistently emerges as a leading region. This is largely attributable to its advanced healthcare infrastructure, substantial investment in digital health technologies, and the stringent regulatory framework mandating robust patient data protection, such as HIPAA. The sheer volume of healthcare providers, coupled with a proactive approach to cybersecurity, positions North America at the forefront of adoption and innovation.

- Dominant Region: North America

- Key Drivers:

- Investment Trends: Significant government and private sector investments in healthcare IT security, estimated in the billions of dollars annually.

- Regulatory Support: Strong enforcement of HIPAA and other data privacy laws drives demand for advanced authentication.

- Technological Adoption: High propensity to adopt new technologies like AI, biometrics, and cloud solutions.

- Healthcare Infrastructure: Extensive network of hospitals, clinics, and research facilities requiring secure access.

- Key Drivers:

Within North America, specific segments showcase exceptional growth and leadership.

Leading Application Segment: Outpatient Department

- Dominance Factors: Outpatient departments handle a vast volume of patient interactions and data. Secure authentication is critical for managing appointments, accessing patient records, and ensuring continuity of care, especially with the rise of telehealth. The estimated market value for authentication solutions in this segment alone is in the hundreds of millions of dollars annually.

- In-depth Analysis: The decentralized nature of outpatient services, often involving multiple locations and a high turnover of patients and staff, necessitates scalable and user-friendly authentication systems. Innovations in mobile authentication and single sign-on (SSO) are particularly impactful here, streamlining access for both clinicians and patients.

Leading Type Segment: Patient Identity Authentication

- Dominance Factors: The accurate and secure authentication of patient identities is paramount to preventing medical identity theft, ensuring correct treatment, and maintaining data integrity. This segment is driven by the need to verify patient demographics, access to personal health information (PHI), and secure prescription fulfillment. The market for patient identity authentication solutions is estimated to be in the billions of dollars across the global market.

- In-depth Analysis: As healthcare systems grapple with increasing instances of medical fraud, the demand for multi-layered patient identity verification, incorporating biometrics and advanced credentialing, is soaring. The integration of patient portals and mobile health applications further amplifies the need for robust, yet accessible, patient authentication.

While North America leads, other regions like Europe (driven by GDPR) and Asia-Pacific (with its rapidly digitizing healthcare sector) are exhibiting substantial growth and present significant market potential, with investments in some of these regions also reaching hundreds of millions of dollars annually.

Medical Authentication System Product Innovations

Product innovations in the Medical Authentication System market are rapidly transforming how healthcare entities secure access to sensitive data and systems. Key advancements include the integration of advanced biometric modalities such as multi-factor biometrics, combining fingerprint, facial, and voice recognition for unparalleled security and convenience. Cloud-native authentication platforms are offering scalability, flexibility, and reduced infrastructure overhead for healthcare providers. Furthermore, AI-powered anomaly detection systems are continuously learning user behavior to proactively identify and flag suspicious activities, preventing unauthorized access. The introduction of passwordless authentication solutions, leveraging secure hardware tokens, FIDO standards, and mobile device biometrics, is enhancing user experience while significantly bolstering security. These innovations are not only improving threat prevention but also streamlining workflows, allowing medical professionals to focus more on patient care. Performance metrics are showing significant improvements in terms of reduced login times and a decrease in successful unauthorized access incidents, with reduction rates often exceeding 99% for well-implemented systems.

Propelling Factors for Medical Authentication System Growth

Several key factors are propelling the growth of the Medical Authentication System market. Firstly, the escalating threat of cyberattacks and data breaches targeting sensitive patient information is a primary driver, compelling healthcare organizations to invest in robust security solutions. Secondly, stringent regulatory mandates, such as HIPAA in the US and GDPR in Europe, impose strict requirements for data privacy and security, pushing for advanced authentication methods. Technological advancements, particularly in biometrics, AI, and cloud computing, are enabling more secure, convenient, and cost-effective authentication solutions. Finally, the widespread adoption of telemedicine and digital health platforms necessitates secure remote access, further fueling the demand for sophisticated authentication systems. The increasing financial penalties for data breaches, often in the millions of dollars, also serve as a significant incentive for investment.

- Escalating Cyber Threats: Increased frequency and sophistication of attacks on healthcare data.

- Regulatory Compliance: Strict data privacy laws mandating secure access.

- Technological Advancements: Innovations in biometrics, AI, and cloud solutions.

- Digital Health Adoption: Growth of telemedicine and EHRs requiring secure remote access.

Obstacles in the Medical Authentication System Market

Despite robust growth, the Medical Authentication System market faces several obstacles. The high cost of implementing advanced authentication solutions, particularly for smaller healthcare providers, can be a significant barrier. Resistance to change from healthcare professionals accustomed to traditional methods and concerns regarding patient privacy and usability of new technologies also present challenges. Furthermore, the fragmented nature of the healthcare IT landscape and interoperability issues between different systems can complicate the integration of new authentication platforms. Supply chain disruptions for hardware components, though less prevalent recently, can still impact deployment timelines and costs. Quantifiable impacts include potential delays in security upgrades, estimated to be several months, and increased implementation costs, potentially 10-20% higher than initially projected.

- High Implementation Costs: Significant upfront investment required for advanced systems.

- User Adoption & Resistance: Overcoming ingrained habits and privacy concerns.

- Interoperability Challenges: Integrating new systems with existing, often legacy, IT infrastructure.

- Regulatory Complexity: Navigating diverse and evolving data privacy laws across jurisdictions.

Future Opportunities in Medical Authentication System

The Medical Authentication System market is ripe with future opportunities. The increasing adoption of the Internet of Medical Things (IoMT) presents a vast untapped market for securing connected medical devices. The burgeoning field of personalized medicine, which relies heavily on secure access to individual genetic and health data, will further drive demand. The expansion of telehealth services into remote and underserved areas offers a significant opportunity for scalable and accessible authentication solutions. Moreover, the development of AI-driven, proactive authentication systems that predict and prevent threats before they occur will be a major growth area. The potential market for IoMT authentication alone is estimated to be in the billions of dollars over the next decade.

- IoMT Security: Securing a rapidly growing ecosystem of connected medical devices.

- Personalized Medicine: Ensuring secure access to highly sensitive genetic and health data.

- Telehealth Expansion: Providing secure and seamless access for remote healthcare delivery.

- AI-Powered Proactive Security: Developing intelligent systems that predict and prevent breaches.

Major Players in the Medical Authentication System Ecosystem

- Gemalto

- JumpCloud

- Broadcom

- Entrust Datacard

- Avatier

- RSA Security

- HID Global

- TrustBuilder

- Duo Security

- Specops Software

- eMudhra

- inWebo Technologies

- RCDevs

- REVE Secure

- Veridium

- OneSpan

- Symantec

Key Developments in Medical Authentication System Industry

- 2023/Q4: Gemalto launched a new suite of biometric authentication solutions tailored for healthcare, enhancing patient identification accuracy.

- 2024/Q1: JumpCloud expanded its identity and access management (IAM) platform to include advanced MFA options specifically for HIPAA-compliant environments.

- 2024/Q2: Broadcom acquired a specialized AI cybersecurity firm, integrating advanced threat detection capabilities into its enterprise security offerings for healthcare.

- 2024/Q3: Entrust Datacard announced a partnership with a leading EHR vendor to streamline secure access for medical professionals.

- 2024/Q4: Duo Security reported a significant reduction in reported security incidents for its healthcare clients following widespread adoption of its mobile MFA solution.

- 2025/Q1: HID Global introduced next-generation contactless biometric readers designed for sterile environments like operating rooms.

- 2025/Q2: RSA Security unveiled its latest identity governance and administration (IGA) solution, providing granular access control for complex healthcare networks.

Strategic Medical Authentication System Market Forecast

The strategic Medical Authentication System market forecast points towards sustained robust growth, driven by an imperative for enhanced patient data security and stringent regulatory compliance. The increasing adoption of advanced technologies like AI-powered anomaly detection and multi-factor biometrics will be pivotal in mitigating sophisticated cyber threats. The expansion of telehealth and IoMT will create new avenues for market penetration, offering significant growth potential in the billions of dollars range. Investments from major players like Gemalto, JumpCloud, and Broadcom in innovation and strategic acquisitions will continue to shape market dynamics. The market is poised to become more integrated, offering comprehensive identity and access management solutions that seamlessly secure every touchpoint within the healthcare ecosystem.

Medical Authentication System Segmentation

-

1. Application

- 1.1. Outpatient Department

- 1.2. Operating Room

- 1.3. Meeting Room

- 1.4. Inpatient Department

- 1.5. Other

-

2. Type

- 2.1. Doctor's Identity Authentication

- 2.2. Patient Identity Authentication

- 2.3. Medical Information Authentication

- 2.4. Other

Medical Authentication System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Authentication System Regional Market Share

Geographic Coverage of Medical Authentication System

Medical Authentication System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Authentication System Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Outpatient Department

- 5.1.2. Operating Room

- 5.1.3. Meeting Room

- 5.1.4. Inpatient Department

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Doctor's Identity Authentication

- 5.2.2. Patient Identity Authentication

- 5.2.3. Medical Information Authentication

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical Authentication System Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Outpatient Department

- 6.1.2. Operating Room

- 6.1.3. Meeting Room

- 6.1.4. Inpatient Department

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Doctor's Identity Authentication

- 6.2.2. Patient Identity Authentication

- 6.2.3. Medical Information Authentication

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical Authentication System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Outpatient Department

- 7.1.2. Operating Room

- 7.1.3. Meeting Room

- 7.1.4. Inpatient Department

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Doctor's Identity Authentication

- 7.2.2. Patient Identity Authentication

- 7.2.3. Medical Information Authentication

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical Authentication System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Outpatient Department

- 8.1.2. Operating Room

- 8.1.3. Meeting Room

- 8.1.4. Inpatient Department

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Doctor's Identity Authentication

- 8.2.2. Patient Identity Authentication

- 8.2.3. Medical Information Authentication

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical Authentication System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Outpatient Department

- 9.1.2. Operating Room

- 9.1.3. Meeting Room

- 9.1.4. Inpatient Department

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Doctor's Identity Authentication

- 9.2.2. Patient Identity Authentication

- 9.2.3. Medical Information Authentication

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical Authentication System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Outpatient Department

- 10.1.2. Operating Room

- 10.1.3. Meeting Room

- 10.1.4. Inpatient Department

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Doctor's Identity Authentication

- 10.2.2. Patient Identity Authentication

- 10.2.3. Medical Information Authentication

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Gemalto

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 JumpCloud

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Broadcom

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Entrust Datacard

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Avatier

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 RSA Security

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 HID Global

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 TrustBuilder

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Duo Security

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Specops Software

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 eMudhra

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 inWebo Technologies

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 RCDevs

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 REVE Secure

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Veridium

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 OneSpan

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Symantec

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Gemalto

List of Figures

- Figure 1: Global Medical Authentication System Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Medical Authentication System Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Medical Authentication System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Authentication System Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Medical Authentication System Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Medical Authentication System Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Medical Authentication System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Authentication System Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Medical Authentication System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Authentication System Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Medical Authentication System Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Medical Authentication System Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Medical Authentication System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Authentication System Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Medical Authentication System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Authentication System Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Medical Authentication System Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Medical Authentication System Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Medical Authentication System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Authentication System Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Authentication System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Authentication System Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Medical Authentication System Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Medical Authentication System Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Authentication System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Authentication System Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Authentication System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Authentication System Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Medical Authentication System Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Medical Authentication System Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Authentication System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Authentication System Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Medical Authentication System Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Medical Authentication System Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Medical Authentication System Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Medical Authentication System Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Medical Authentication System Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Authentication System Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Medical Authentication System Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Medical Authentication System Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Authentication System Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Medical Authentication System Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Medical Authentication System Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Authentication System Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Medical Authentication System Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Medical Authentication System Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Authentication System Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Medical Authentication System Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Medical Authentication System Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Authentication System Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Authentication System?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the Medical Authentication System?

Key companies in the market include Gemalto, JumpCloud, Broadcom, Entrust Datacard, Avatier, RSA Security, HID Global, TrustBuilder, Duo Security, Specops Software, eMudhra, inWebo Technologies, RCDevs, REVE Secure, Veridium, OneSpan, Symantec.

3. What are the main segments of the Medical Authentication System?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Authentication System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Authentication System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Authentication System?

To stay informed about further developments, trends, and reports in the Medical Authentication System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence