Key Insights

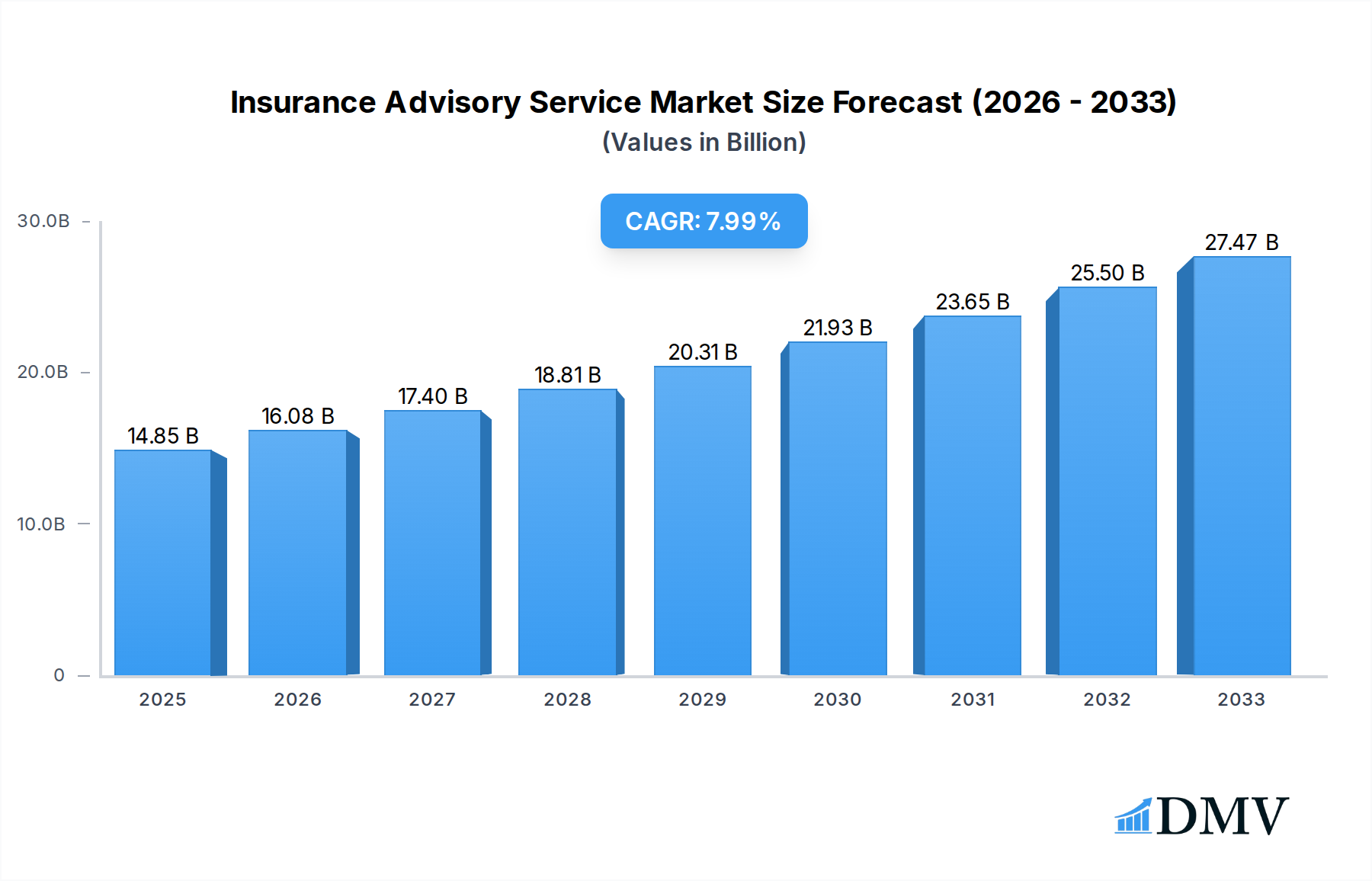

The global Insurance Advisory Service market is poised for robust expansion, projected to reach an estimated USD 14.85 billion in 2025, with a compelling Compound Annual Growth Rate (CAGR) of 8.3% through 2033. This significant growth is propelled by a confluence of evolving consumer needs, increasing complexity in insurance products, and a heightened awareness of risk management among both individuals and enterprises. The rising demand for personalized financial planning and the necessity for expert guidance in navigating diverse insurance options, from life and health to property and casualty, are fundamental drivers. Furthermore, the increasing penetration of digital platforms and technological advancements is reshaping how advisory services are delivered, making them more accessible and efficient. The market is segmented into Enterprise and Individual applications, with Original Insurance Advisors and Reinsurance Advisors forming key functional types. Key industry players, including Insurance Advisory Service (IAS), Financial Designs, WealthPoint, Arthur J. Gallagher & Co., and Aon plc, are actively innovating and expanding their offerings to cater to these dynamic market demands.

Insurance Advisory Service Market Size (In Billion)

The growth trajectory of the Insurance Advisory Service market is further bolstered by significant trends such as the integration of AI and data analytics to provide more sophisticated and predictive insights, a growing emphasis on niche insurance products tailored to specific industries and lifestyles, and the ongoing consolidation within the advisory landscape. Emerging markets, particularly in the Asia Pacific region, are showing substantial promise due to rapid economic development and an expanding middle class seeking financial security. While opportunities abound, the market also faces certain restraints, including intense competition from established and new entrants, evolving regulatory landscapes that can impact service delivery and costs, and the inherent challenges in building and maintaining client trust in a rapidly changing financial environment. Nonetheless, the overarching sentiment is one of sustained growth, driven by the indispensable role of informed advisory services in an increasingly complex financial world.

Insurance Advisory Service Company Market Share

Insurance Advisory Service Market Composition & Trends

The global Insurance Advisory Service market is characterized by a moderately concentrated landscape, with a few key players holding significant market share, projected to be around 65% in the Base Year 2025. Innovation remains a crucial catalyst, with an estimated XXX billion invested in insurtech solutions during the historical period 2019–2024, driving enhanced digital platforms and personalized client experiences. The regulatory environment, while complex, is evolving to foster greater transparency and consumer protection, with new compliance mandates shaping service delivery. Substitute products, primarily direct online insurance purchasing platforms, continue to pose a challenge, though the intrinsic value of expert advice in navigating complex policies remains a key differentiator. End-user profiles are diverse, spanning individual consumers seeking tailored protection plans to large enterprises requiring sophisticated risk management strategies. Mergers and acquisitions (M&A) activities are a notable trend, with XXX billion in disclosed deal values during the historical period, indicating a consolidation phase aimed at expanding service offerings and geographical reach. For instance, the consolidation of Financial Designs with WealthPoint signifies a move towards broader financial planning capabilities.

- Market Share Distribution (Estimated Base Year 2025):

- Top 5 Players: ~65%

- Next 10 Players: ~25%

- Fragmented Market: ~10%

- M&A Deal Values (Historical Period 2019–2024):

- Total Disclosed Value: XXX Billion

- Average Deal Size: XXX Billion

Insurance Advisory Service Industry Evolution

The Insurance Advisory Service industry has undergone a remarkable transformation throughout the historical period 2019–2024 and is poised for continued robust growth, with a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period 2025–2033. This evolution is intrinsically linked to significant technological advancements that have redefined how advisory services are delivered and consumed. The integration of Artificial Intelligence (AI) and Machine Learning (ML) has enabled sophisticated data analytics, leading to more accurate risk assessments, personalized product recommendations, and streamlined claims processing. For instance, adoption of AI-powered underwriting assistance tools has seen a XX% increase in the last two years alone. Simultaneously, shifting consumer demands have pushed the industry towards greater digital engagement, transparency, and a holistic approach to financial well-being. Clients increasingly seek proactive advice, not just reactive solutions, and value advisors who can seamlessly integrate insurance planning with broader wealth management goals. The rise of the gig economy and evolving life stages also necessitates more flexible and adaptive insurance solutions, pushing advisory services to become more dynamic and customer-centric. The base year 2025 marks a pivotal point where these converging trends are solidifying new service paradigms. The emergence of comprehensive digital advisory platforms, offering end-to-end client management and personalized insights, is a testament to this ongoing evolution. The industry's capacity to adapt to these changes, by embracing new technologies and understanding nuanced consumer needs, will be critical for sustained success in the coming years. The continuous pursuit of customer-centricity, powered by data-driven insights and innovative delivery models, is reshaping the competitive landscape. The estimated market size for Insurance Advisory Services in the Base Year 2025 is projected to reach XXX Billion, underscoring the sector's substantial economic impact.

Leading Regions, Countries, or Segments in Insurance Advisory Service

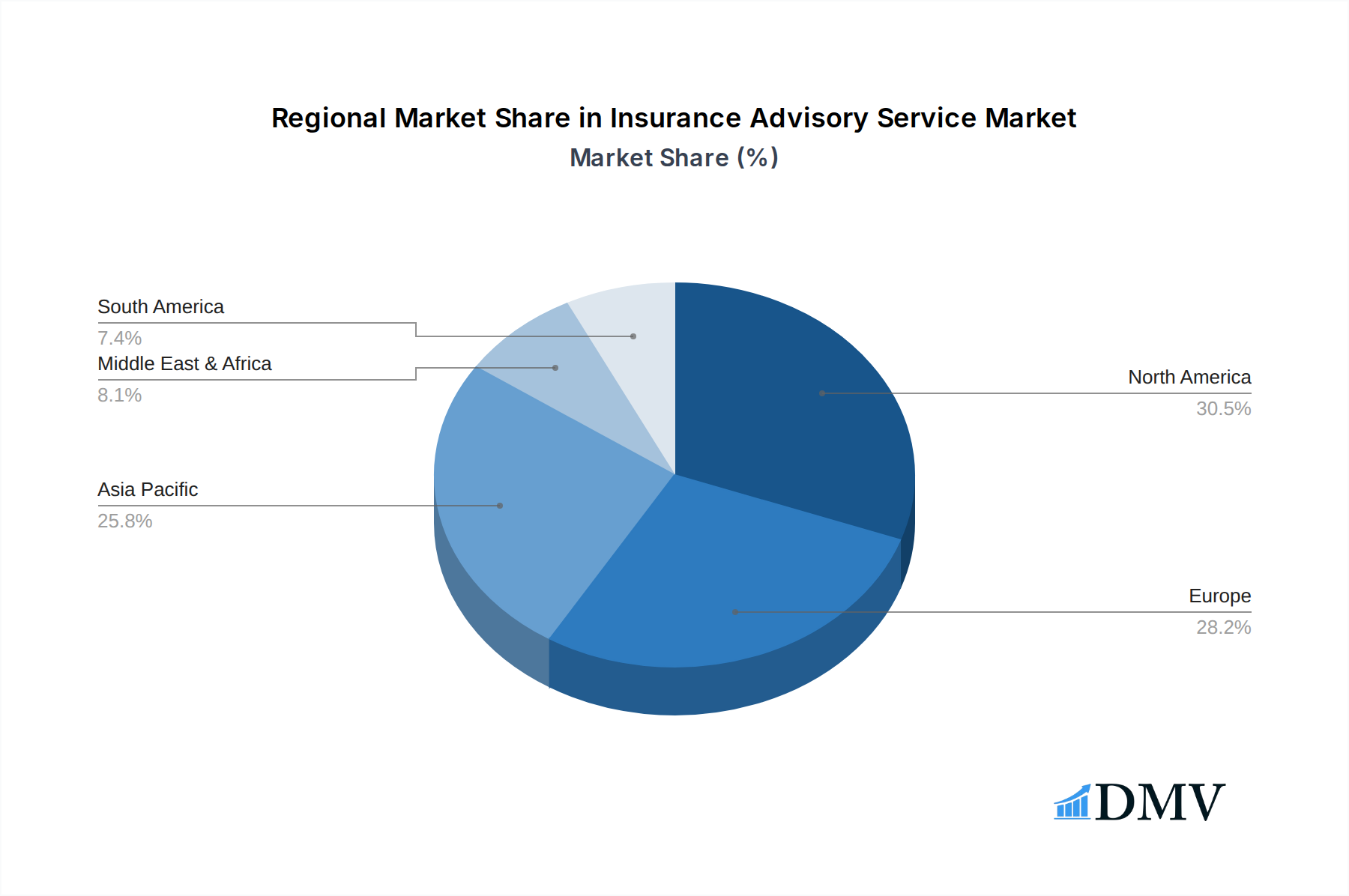

The Insurance Advisory Service market exhibits distinct regional dominance and segment leadership, with the Enterprise application segment showcasing the most significant traction and projected growth. This dominance is driven by a confluence of factors, including the increasing complexity of corporate risk landscapes, stringent regulatory compliance requirements, and the substantial financial implications of inadequate insurance coverage for businesses. Enterprises require sophisticated advisory services for a broad spectrum of risks, from property and casualty to cyber liability and employee benefits. The United States stands out as a leading country within this segment, owing to its mature financial markets, extensive regulatory framework, and a high concentration of large corporations actively seeking specialized insurance solutions. The estimated market share of the Enterprise segment in the Base Year 2025 is projected to be around XX%, surpassing the Individual segment.

Dominant Application Segment: Enterprise

- Key Drivers:

- Increasingly complex corporate risk portfolios (e.g., supply chain disruption, cyber threats).

- Stringent and evolving regulatory compliance demands across industries.

- Higher average contract values and long-term client relationships.

- Growing adoption of specialized insurance products (e.g., D&O, professional liability).

- In-depth Analysis: Large corporations possess intricate operational structures and face a wider array of insurable risks than individual consumers. The need for tailored risk mitigation strategies, comprehensive policy reviews, and expert negotiation with insurers necessitates specialized advisory services. This demand is amplified by global economic uncertainties and the increasing interconnectedness of business operations, making robust insurance advisory indispensable for business continuity and financial stability. The estimated investment in enterprise insurance advisory services in the Base Year 2025 is expected to reach XXX Billion.

- Key Drivers:

Leading Country: United States

- Key Drivers:

- Mature and highly developed insurance market with a wide range of product offerings.

- Robust regulatory oversight ensuring transparency and consumer protection.

- Presence of major global corporations and a strong entrepreneurial ecosystem.

- Significant investment in insurtech innovation driving efficiency and personalized advice.

- In-depth Analysis: The US market benefits from a deep pool of experienced insurance advisors and a sophisticated client base that understands the value of expert guidance. The regulatory environment, while complex, fosters a competitive landscape where advisory firms differentiate themselves through specialized expertise and innovative service delivery models. The forecast period 2025–2033 anticipates continued growth driven by evolving risk management needs and technological integration.

- Key Drivers:

Dominant Type: Original Insurance Advisor

- Key Drivers:

- Fundamental need for guidance in understanding and selecting primary insurance policies.

- Growing awareness of the importance of adequate coverage for life, health, and property.

- Complexity of insurance products requiring expert interpretation.

- In-depth Analysis: While reinsurance advisory plays a critical role in the industry's stability, the direct engagement with end-users primarily falls under original insurance advising. This segment caters to the foundational insurance needs of both individuals and enterprises, making it a consistently high-demand area.

- Key Drivers:

Insurance Advisory Service Product Innovations

Product innovations within the Insurance Advisory Service market are rapidly transforming client engagement and service delivery. The integration of AI-powered personalized risk assessment tools allows advisors to provide hyper-targeted policy recommendations, moving beyond generic offerings. Predictive analytics are now being used to forecast potential claims, enabling proactive intervention and policy adjustments. Furthermore, the development of comprehensive digital platforms, offering seamless policy management, claims tracking, and educational resources, enhances transparency and client convenience. These innovations, driven by a focus on user experience and data-driven insights, aim to democratize access to expert advice and empower clients to make more informed decisions, with a projected adoption rate of XX% for advanced digital advisory tools by 2028.

Propelling Factors for Insurance Advisory Service Growth

The Insurance Advisory Service market is propelled by several key factors. Technologically, the proliferation of AI and big data analytics enables more personalized and efficient advisory services, enhancing risk assessment and policy customization. Economically, increasing wealth creation and a growing awareness of financial security needs, particularly post-pandemic, are driving demand for comprehensive insurance planning. Regulatory landscapes are also playing a crucial role; evolving compliance requirements and a focus on consumer protection necessitate expert guidance, thereby increasing the value proposition of advisory services. For instance, new data privacy regulations require specialized advice for businesses to ensure compliance.

Obstacles in the Insurance Advisory Service Market

Despite robust growth, the Insurance Advisory Service market faces several obstacles. Regulatory challenges persist, with fragmented and evolving legal frameworks across different jurisdictions demanding constant adaptation and expertise. Supply chain disruptions, particularly impacting the availability of certain specialized insurance products, can create gaps in coverage and complicate advisory recommendations. Furthermore, intense competitive pressures from a growing number of advisory firms and the increasing accessibility of DIY online insurance platforms require continuous innovation and demonstrable value to retain clients. The estimated impact of these barriers on market growth is approximately XX%.

Future Opportunities in Insurance Advisory Service

Emerging opportunities for Insurance Advisory Services are abundant. The growing demand for personalized and holistic financial planning, integrating insurance with investment and retirement strategies, presents a significant avenue for growth. The expanding gig economy and the rise of non-traditional workforces create a need for flexible and adaptable insurance solutions, requiring specialized advisory expertise. Furthermore, the increasing focus on environmental, social, and governance (ESG) factors is leading to new insurance products and advisory needs related to sustainable business practices and climate risk management. Advancements in IoT and wearable technology also offer opportunities for data-driven, preventative insurance advisory.

Major Players in the Insurance Advisory Service Ecosystem

- Arthur J. Gallagher & Co.

- Aon plc

- Marsh

- Aditya Birla Capital

- HUATAI Insurance Agency & Consulant Service

- Yingda Chang'an Insurance Brokers Group

- Yongdali Insurance Brokerage

- Mingya Insurance Brokers

- Datong Insurance Brokerage

- Jiang Tai Insurance Brokers

- Insurance Advisory Service(IAS)

- Financial Designs

- WealthPoint

- Greenwood Moreland

- Harbor Group

- SMART Financial Advisory

- Pillsbury Winthrop Shaw Pittman

- CC Advisory

Key Developments in Insurance Advisory Service Industry

- 2023 Q4: Launch of AI-powered personalized risk assessment tools by major advisory firms, enhancing client-specific policy recommendations.

- 2024 Q1: Increased M&A activity focused on acquiring insurtech startups to integrate advanced data analytics capabilities into advisory services.

- 2024 Q2: Introduction of specialized advisory services for cyber insurance and supply chain risk management, reflecting growing enterprise needs.

- 2024 Q3: Enhanced digital platforms offering seamless client onboarding, policy management, and claims tracking are becoming industry standards.

- 2024 Q4: Growing emphasis on ESG-related insurance advisory, particularly for climate risk mitigation and corporate sustainability initiatives.

Strategic Insurance Advisory Service Market Forecast

The strategic Insurance Advisory Service market forecast highlights sustained growth driven by increasing client demand for personalized, data-driven financial guidance. Emerging opportunities in integrating insurance with broader wealth management, catering to evolving workforces, and addressing climate-related risks will be pivotal. Technological advancements, particularly in AI and predictive analytics, will continue to reshape service delivery, enhancing efficiency and client engagement. The market's potential lies in its ability to adapt to these evolving needs, offering sophisticated, tailored solutions that underscore the indispensable value of expert advice in navigating an increasingly complex financial landscape. The projected market size in the Estimated Year 2025 is XXX Billion.

Insurance Advisory Service Segmentation

-

1. Application

- 1.1. Enterprise

- 1.2. Individual

-

2. Type

- 2.1. Original Insurance Advisor

- 2.2. Reinsurance Advisor

Insurance Advisory Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Insurance Advisory Service Regional Market Share

Geographic Coverage of Insurance Advisory Service

Insurance Advisory Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Enterprise

- 5.1.2. Individual

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Original Insurance Advisor

- 5.2.2. Reinsurance Advisor

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Insurance Advisory Service Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Enterprise

- 6.1.2. Individual

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Original Insurance Advisor

- 6.2.2. Reinsurance Advisor

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Insurance Advisory Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Enterprise

- 7.1.2. Individual

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Original Insurance Advisor

- 7.2.2. Reinsurance Advisor

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Insurance Advisory Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Enterprise

- 8.1.2. Individual

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Original Insurance Advisor

- 8.2.2. Reinsurance Advisor

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Insurance Advisory Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Enterprise

- 9.1.2. Individual

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Original Insurance Advisor

- 9.2.2. Reinsurance Advisor

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Insurance Advisory Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Enterprise

- 10.1.2. Individual

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Original Insurance Advisor

- 10.2.2. Reinsurance Advisor

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Insurance Advisory Service Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Enterprise

- 11.1.2. Individual

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Original Insurance Advisor

- 11.2.2. Reinsurance Advisor

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Insurance Advisory Service(IAS)

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Financial Designs

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 WealthPoint

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Arthur J. Gallagher & Co.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Greenwood Moreland

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Harbor Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 SMART Financial Advisory

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Aditya Birla Capital

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Pillsbury Winthrop Shaw Pittman

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 CC Advisory

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Marsh

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Mingya Insurance Brokers

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Aon plc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Yongdali Insurance Brokerage

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Yingda Chang'an Insurance Brokers Group

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Datong Insurance Brokerage

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 HUATAI Insurance Agency & Consulant Service

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Jiang Tai Insurance Brokers

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.1 Insurance Advisory Service(IAS)

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Insurance Advisory Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Insurance Advisory Service Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Insurance Advisory Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Insurance Advisory Service Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Insurance Advisory Service Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Insurance Advisory Service Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Insurance Advisory Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Insurance Advisory Service Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Insurance Advisory Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Insurance Advisory Service Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Insurance Advisory Service Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Insurance Advisory Service Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Insurance Advisory Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Insurance Advisory Service Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Insurance Advisory Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Insurance Advisory Service Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Insurance Advisory Service Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Insurance Advisory Service Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Insurance Advisory Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Insurance Advisory Service Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Insurance Advisory Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Insurance Advisory Service Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Insurance Advisory Service Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Insurance Advisory Service Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Insurance Advisory Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Insurance Advisory Service Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Insurance Advisory Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Insurance Advisory Service Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Insurance Advisory Service Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Insurance Advisory Service Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Insurance Advisory Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Insurance Advisory Service Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Insurance Advisory Service Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Insurance Advisory Service Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Insurance Advisory Service Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Insurance Advisory Service Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Insurance Advisory Service Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Insurance Advisory Service Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Insurance Advisory Service Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Insurance Advisory Service Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Insurance Advisory Service Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Insurance Advisory Service Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Insurance Advisory Service Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Insurance Advisory Service Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Insurance Advisory Service Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Insurance Advisory Service Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Insurance Advisory Service Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Insurance Advisory Service Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Insurance Advisory Service Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Insurance Advisory Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Insurance Advisory Service?

The projected CAGR is approximately 8.3%.

2. Which companies are prominent players in the Insurance Advisory Service?

Key companies in the market include Insurance Advisory Service(IAS), Financial Designs, WealthPoint, Arthur J. Gallagher & Co., Greenwood Moreland, Harbor Group, SMART Financial Advisory, Aditya Birla Capital, Pillsbury Winthrop Shaw Pittman, CC Advisory, Marsh, Mingya Insurance Brokers, Aon plc, Yongdali Insurance Brokerage, Yingda Chang'an Insurance Brokers Group, Datong Insurance Brokerage, HUATAI Insurance Agency & Consulant Service, Jiang Tai Insurance Brokers.

3. What are the main segments of the Insurance Advisory Service?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.85 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Insurance Advisory Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Insurance Advisory Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Insurance Advisory Service?

To stay informed about further developments, trends, and reports in the Insurance Advisory Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence