Key Insights

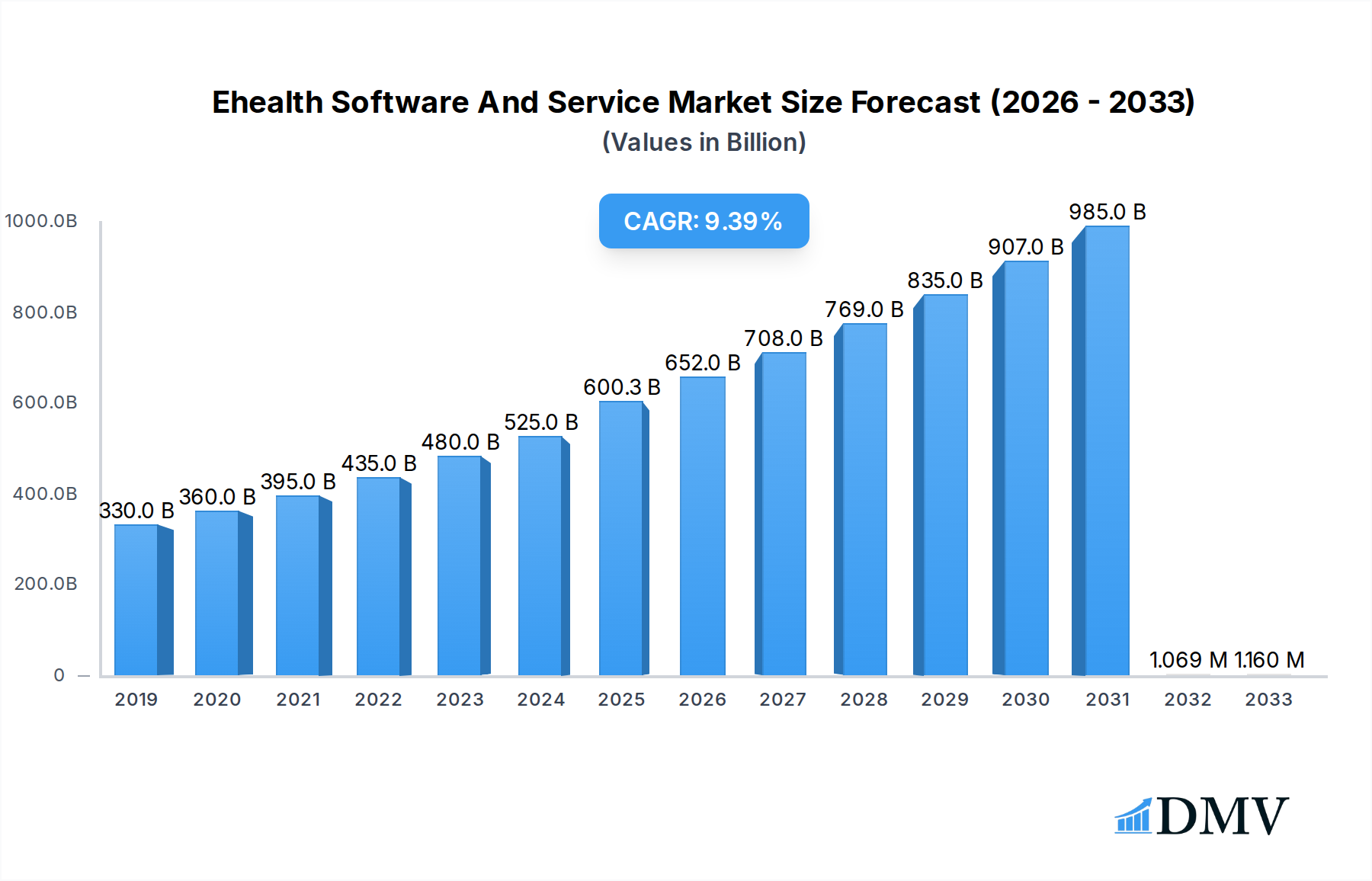

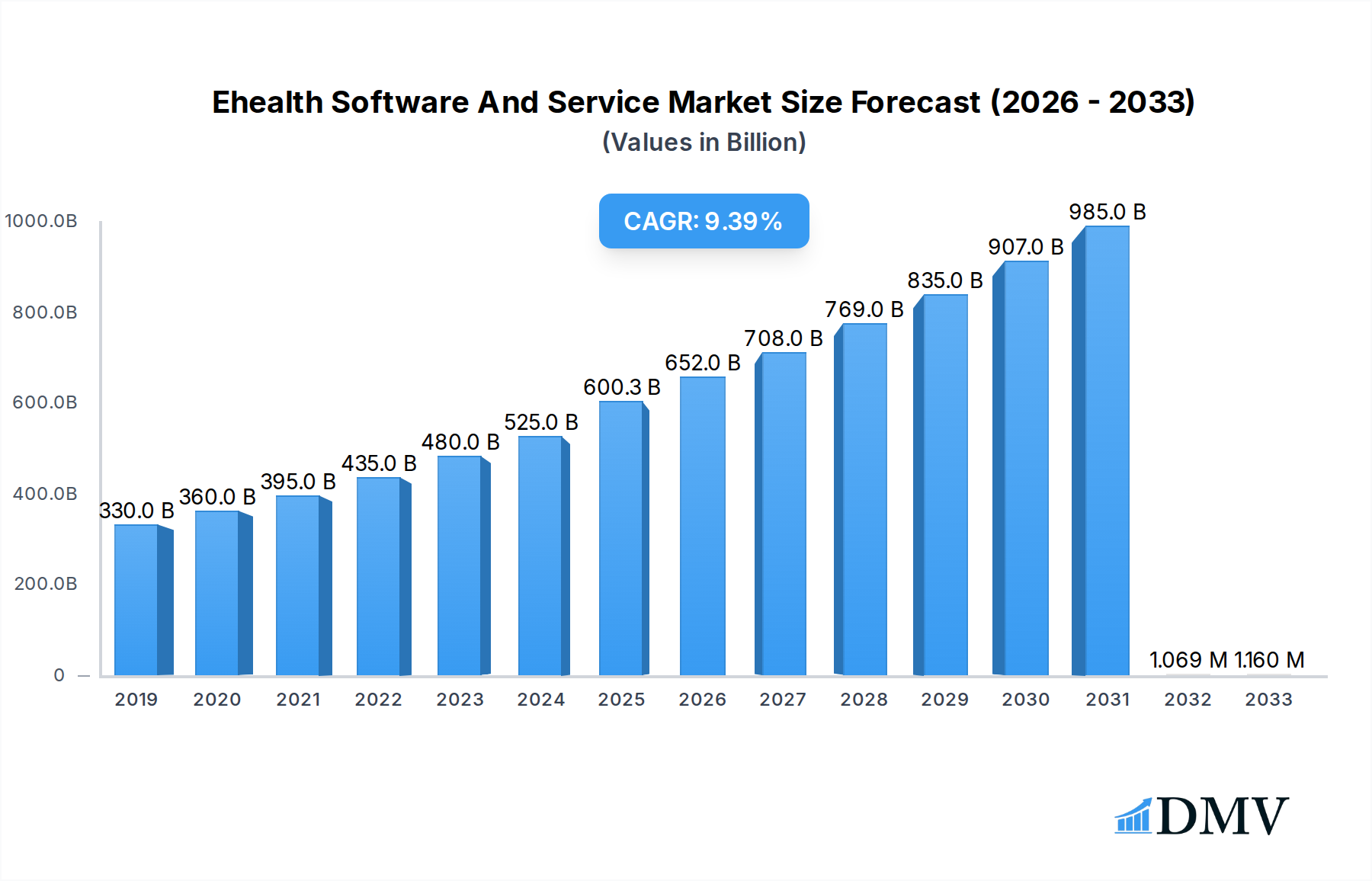

The global Ehealth Software and Services market is poised for significant expansion, projected to reach an estimated USD 600,340 million by 2025, demonstrating a robust Compound Annual Growth Rate (CAGR) of 8.8% over the forecast period of 2025-2033. This substantial growth is underpinned by a confluence of powerful drivers, including the escalating demand for remote patient monitoring and telehealth solutions, the increasing adoption of electronic health records (EHRs) and other digital health platforms across healthcare institutions, and the growing emphasis on personalized medicine and preventive healthcare driven by individual consumers. The COVID-19 pandemic has served as a significant catalyst, accelerating the digital transformation within the healthcare sector and highlighting the critical role of ehealth in ensuring continuous patient care and access to medical services, thereby solidifying its long-term growth trajectory.

Ehealth Software And Service Market Size (In Billion)

The market is segmented into various applications and types, catering to a diverse user base. Applications span across Healthcare Institutions, Physicians, Healthcare Workers, and Individuals, reflecting the widespread integration of ehealth solutions in modern healthcare delivery. By type, the market is divided into eHealth Software and eHealth Services, with both segments experiencing strong growth. Emerging trends such as the integration of artificial intelligence (AI) and machine learning (ML) for diagnostic support and data analytics, the proliferation of wearable devices for health tracking, and the development of patient-centric portals are further fueling market expansion. While the market exhibits immense potential, certain restraints, such as data privacy and security concerns, regulatory hurdles, and the digital divide in underserved regions, need to be strategically addressed to ensure equitable access and continued market development. Leading companies like McKesson Corporation, GE Healthcare, and Apple are at the forefront of innovation, driving the adoption of advanced ehealth solutions globally.

Ehealth Software And Service Company Market Share

Ehealth Software And Service Market: A Comprehensive Analysis and Forecast (2019–2033)

This in-depth report offers a panoramic view of the global eHealth Software and Service market, dissecting its intricate composition, historical evolution, and future trajectory. We delve into critical trends, disruptive innovations, and the competitive landscape, providing actionable insights for stakeholders across healthcare institutions, physicians, healthcare workers, and individuals. The study spans the historical period of 2019–2024, with a base year of 2025 and a comprehensive forecast extending to 2033, offering a robust understanding of market dynamics and potential. With a focus on high-ranking keywords such as "telehealth software," "digital health services," "e-prescription platforms," "remote patient monitoring," "healthcare IT solutions," and "patient engagement apps," this report is meticulously crafted for optimal search visibility and stakeholder engagement.

Ehealth Software And Service Market Composition & Trends

The eHealth Software and Service market is characterized by a dynamic interplay of established giants and agile innovators, with a discernible trend towards market consolidation and strategic alliances. The market concentration is currently moderate, with key players vying for dominance across various segments. Innovation catalysts are primarily driven by the escalating demand for accessible, efficient, and personalized healthcare solutions, fueled by advancements in artificial intelligence, big data analytics, and cloud computing. The regulatory landscape, while evolving, continues to shape market entry and product development, with a growing emphasis on data privacy and security standards like HIPAA and GDPR. Substitute products, such as traditional in-person consultations and fragmented digital tools, are gradually being supplanted by integrated eHealth platforms. End-user profiles are diversifying, encompassing healthcare institutions seeking to optimize operational efficiency and patient care, physicians leveraging remote diagnostics and patient management, healthcare workers benefiting from streamlined workflows, and individuals demanding convenient and proactive health management. Merger and acquisition (M&A) activities are on the rise, with estimated deal values in the hundreds of millions annually, as companies strategically acquire technologies and market share to bolster their offerings.

- Market Share Distribution: While specific figures are proprietary, the top 5 players collectively hold an estimated 40% of the market share, with a steady increase observed over the historical period.

- M&A Deal Values: Recent years have witnessed an average of 5-7 significant M&A deals annually, with transaction values ranging from $50 million to $500 million, underscoring active industry consolidation.

- Innovation Hotspots: Key areas of innovation include AI-powered diagnostic tools, interoperable EHR systems, personalized wellness platforms, and secure telehealth infrastructure.

- Regulatory Focus: Compliance with evolving data protection regulations and the pursuit of certifications for medical device software are paramount for market players.

Ehealth Software And Service Industry Evolution

The eHealth Software and Service industry has undergone a remarkable evolution, transforming from nascent digital health tools to a sophisticated ecosystem of integrated solutions. The market growth trajectory has been consistently upward, significantly accelerated by global health events that underscored the indispensable nature of digital health. Historically, the industry witnessed early adoption focused on electronic health records (EHRs) and basic telemedicine capabilities. However, the study period of 2019–2033 reveals a profound shift towards proactive and preventive healthcare, driven by consumer demand for personalized health insights and convenient access to medical professionals. Technological advancements have been the bedrock of this evolution, with the integration of artificial intelligence (AI) revolutionizing diagnostics, treatment recommendations, and administrative tasks. Machine learning algorithms are now capable of analyzing vast datasets to predict disease outbreaks, identify at-risk patients, and personalize treatment plans. The proliferation of wearable devices and the Internet of Medical Things (IoMT) has facilitated seamless remote patient monitoring, enabling continuous data collection and early intervention for chronic conditions. Cloud computing has provided the scalable infrastructure necessary to support these data-intensive applications, ensuring accessibility and interoperability across diverse healthcare settings.

The forecast period (2025–2033) is poised for even more accelerated growth, with a projected Compound Annual Growth Rate (CAGR) of approximately 18%. This surge is propelled by several key factors: the increasing prevalence of chronic diseases globally, the aging population, and the growing awareness among individuals about the benefits of proactive health management. Furthermore, government initiatives and healthcare reforms worldwide are actively promoting the adoption of digital health solutions to improve healthcare accessibility and reduce costs. The shift in consumer demand is palpable; individuals are no longer content with reactive care. They are actively seeking tools and services that empower them to take control of their health, track their wellness metrics, and engage directly with healthcare providers through user-friendly interfaces. This has led to a surge in the development and adoption of patient portals, mobile health applications, and virtual health platforms. The COVID-19 pandemic acted as a significant inflection point, forcing rapid adoption of telehealth and remote care solutions, solidifying their place in the healthcare landscape. This rapid adoption has not only increased market penetration but also fostered greater trust and familiarity with digital health among both patients and providers. The ongoing development of 5G technology promises to further enhance the capabilities of eHealth services, enabling faster data transfer, lower latency, and more sophisticated real-time applications, particularly in areas like remote surgery and advanced telemedicine. The industry's evolution is a testament to its adaptability and its crucial role in shaping the future of healthcare delivery.

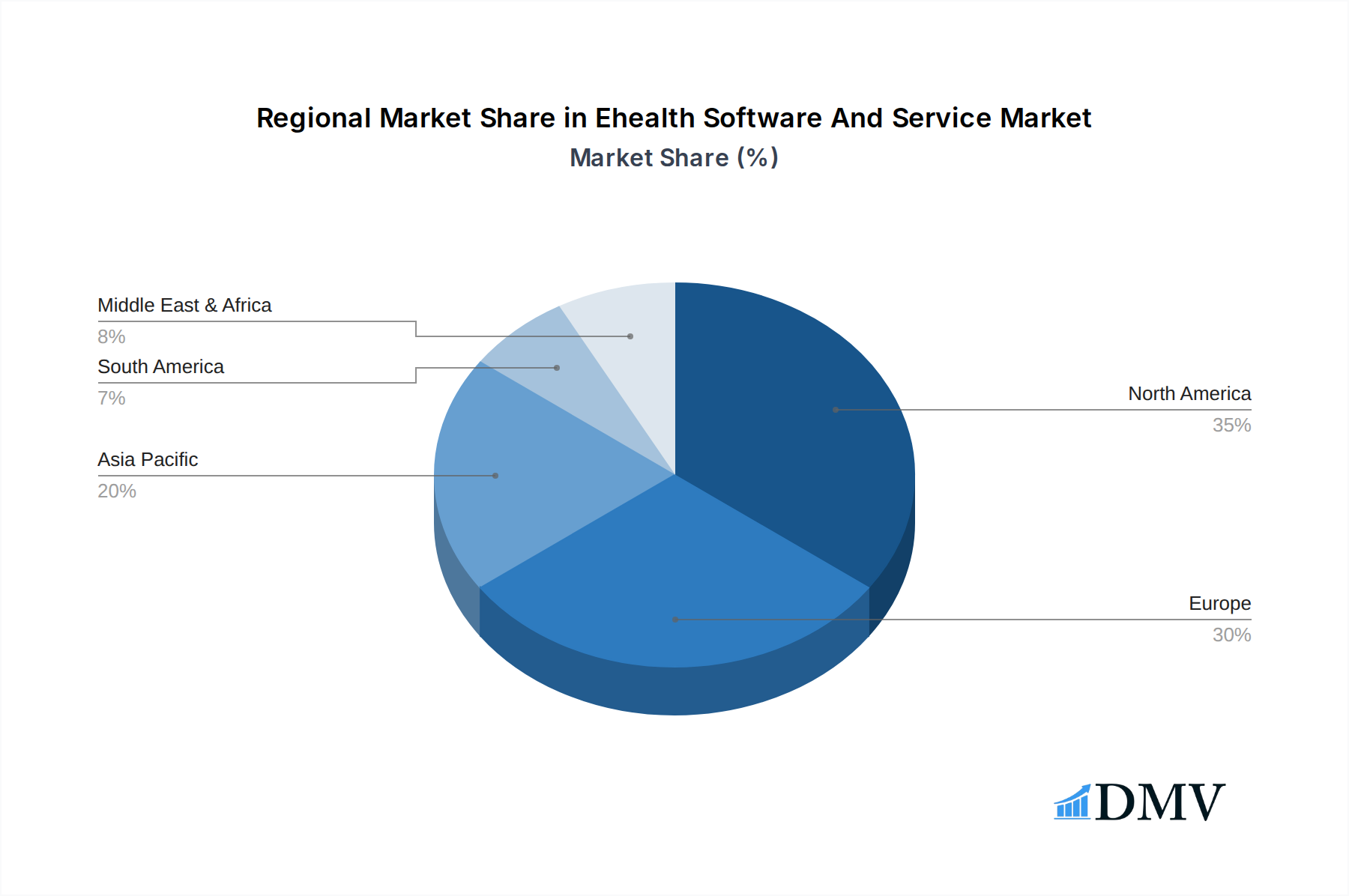

Leading Regions, Countries, or Segments in Ehealth Software And Service

The eHealth Software and Service market is experiencing dynamic growth across various regions and segments, with North America currently leading the charge. This dominance is attributed to a confluence of factors including robust government initiatives supporting digital health adoption, significant private sector investment, and a technologically savvy population readily embracing innovative healthcare solutions. Within North America, the United States stands out as a primary driver, owing to its advanced healthcare infrastructure, high disposable income, and a strong ecosystem of technology companies and healthcare providers collaborating on digital health innovations.

Key Drivers for North America's Dominance:

- Government Investment and Policy Support: Initiatives like the HITECH Act and ongoing telehealth reimbursement policies have provided a strong regulatory and financial impetus for the adoption of eHealth solutions.

- High Healthcare Expenditure: The substantial investment in healthcare in the US translates directly into a larger market for sophisticated eHealth software and services aimed at improving efficiency and patient outcomes.

- Technological Infrastructure: Widespread availability of high-speed internet and advanced mobile penetration facilitate the seamless delivery and adoption of digital health services.

- Venture Capital Funding: North America consistently attracts significant venture capital investment in the digital health sector, fueling innovation and market expansion.

Among the specified applications, Healthcare Institutions represent the largest and fastest-growing segment. These institutions are increasingly investing in eHealth solutions to streamline operations, enhance patient care delivery, improve interoperability between different systems, and reduce administrative burdens. The demand for comprehensive eHealth software and services within hospitals and clinics is driven by the need for efficient patient management, remote diagnostics, telehealth platforms, and data analytics for improved decision-making. Physicians are also a significant segment, leveraging eHealth tools for remote consultations, e-prescriptions, and patient record management. Healthcare workers benefit from eHealth solutions that automate tasks, improve communication, and provide access to real-time patient data. Individuals are increasingly engaging with eHealth through personal health apps, wearable devices, and direct-to-consumer telehealth services, underscoring a growing trend towards patient empowerment and self-management of health.

In terms of eHealth type, eHealth Software, encompassing EHRs, telemedicine platforms, patient portals, and AI-driven diagnostic tools, holds a dominant market share. However, eHealth Services, including consulting, implementation, and maintenance of these software solutions, are also experiencing substantial growth as healthcare organizations seek expert guidance in navigating the complex digital transformation. The synergy between sophisticated software and expert services is crucial for the successful integration and utilization of eHealth technologies within the complex healthcare ecosystem.

Ehealth Software And Service Product Innovations

The eHealth Software and Service market is continuously shaped by groundbreaking product innovations. Key advancements include the development of AI-powered diagnostic tools that can analyze medical images with high accuracy, significantly aiding radiologists and pathologists. Telehealth platforms are evolving beyond simple video calls to offer sophisticated virtual examination capabilities, remote patient monitoring integration, and secure data exchange. Furthermore, personalized wellness applications leveraging gamification and behavioral science are emerging to enhance patient engagement and adherence to treatment plans. The integration of blockchain technology promises to revolutionize health data security and interoperability. Performance metrics showcase improved diagnostic accuracy by up to 20% with AI assistance and a 30% reduction in patient wait times through efficient telehealth scheduling.

Propelling Factors for Ehealth Software And Service Growth

Several critical factors are propelling the growth of the eHealth Software and Service market. The increasing global prevalence of chronic diseases necessitates more efficient and accessible management solutions, which eHealth provides through remote monitoring and personalized care plans. Technological advancements, particularly in AI, big data analytics, and cloud computing, are enabling the development of more sophisticated and integrated eHealth platforms. Government initiatives and favorable reimbursement policies for telehealth and digital health services in various regions are creating a supportive regulatory and financial environment. The growing consumer demand for convenient, accessible, and personalized healthcare experiences, coupled with the increasing adoption of smartphones and wearable devices, further fuels market expansion. For instance, the expansion of 5G networks allows for more robust and real-time telehealth applications, significantly enhancing the capabilities of remote patient monitoring and virtual consultations.

Obstacles in the Ehealth Software And Service Market

Despite its immense potential, the eHealth Software and Service market faces several significant obstacles. Regulatory challenges, including varying data privacy laws across different jurisdictions and the complex process of obtaining approvals for medical devices and software, can slow down market entry and innovation. Interoperability issues between different eHealth systems and legacy healthcare IT infrastructure remain a persistent hurdle, hindering seamless data exchange and integration. High initial implementation costs for comprehensive eHealth solutions can be prohibitive for smaller healthcare providers. Additionally, cybersecurity threats and concerns over patient data breaches can erode trust and adoption. The digital divide, where access to reliable internet and digital literacy is limited in certain populations, also presents a barrier to equitable access to eHealth services. For example, the cost of implementing a fully integrated EHR system can range from $20 million to $100 million for a large hospital, representing a substantial investment.

Future Opportunities in Ehealth Software And Service

The future of the eHealth Software and Service market is replete with promising opportunities. The expansion of telehealth services into remote and underserved areas, leveraging mobile health (mHealth) technologies, presents a significant avenue for growth. The increasing integration of AI and machine learning in predictive analytics and personalized medicine will unlock new diagnostic and treatment possibilities. The growing focus on mental health is driving demand for specialized e-mental health platforms and virtual therapy services. Furthermore, the burgeoning market for remote patient monitoring solutions for an aging global population, coupled with the increasing adoption of wearable technology, offers substantial potential. The development of interoperable health data exchange platforms, potentially utilizing blockchain technology, could revolutionize healthcare data management and research. The proactive approach to preventative care and wellness management, fueled by a growing health-conscious population, will continue to drive demand for user-friendly and engaging eHealth applications.

Major Players in the Ehealth Software And Service Ecosystem

- McKesson Corporation

- eHealth Technologies

- GE Healthcare

- Johnson and Johnson Healthcare Systems

- Aerotel Medical Systems

- Siemens

- Allscripts Healthcare Solutions

- RamSoft

- Apple

- Fitbit

- Sectra

- Doctor on Demand

- eRAD

- AdvancedMD

- KareXpert Technologies

Key Developments in Ehealth Software And Service Industry

- 2023 September: GE Healthcare launches a new AI-powered diagnostic imaging solution, enhancing diagnostic accuracy and efficiency.

- 2023 October: Apple announces enhanced health tracking features on its latest smartwatch, further integrating consumer wearables with health monitoring.

- 2023 November: Allscripts Healthcare Solutions announces a strategic partnership to enhance interoperability between its EHR system and a leading telehealth platform, improving patient care coordination.

- 2024 January: Doctor on Demand reports a 25% increase in patient consultations driven by expanding service offerings and improved platform accessibility.

- 2024 February: McKesson Corporation acquires a key e-prescription platform, solidifying its position in the digital pharmacy solutions market.

- 2024 March: KareXpert Technologies secures $50 million in Series B funding to accelerate the expansion of its integrated hospital management platform.

- 2024 April: Sectra showcases advancements in its digital pathology solutions, demonstrating enhanced image analysis capabilities for cancer diagnostics.

- 2024 May: Fitbit announces new features for remote patient monitoring, focusing on cardiovascular health management.

- 2024 June: Siemens Healthineers unveils a new suite of AI-driven tools for radiology departments, aiming to optimize workflows and improve diagnostic precision.

- 2024 July: eHealth Technologies announces a new partnership with a major hospital network to implement its patient data aggregation and analysis platform, projected to improve patient outcomes by an estimated 15%.

Strategic Ehealth Software And Service Market Forecast

The strategic forecast for the eHealth Software and Service market is exceptionally positive, driven by an accelerating adoption rate and continuous innovation. Key growth catalysts include the ongoing global push towards value-based care models, which heavily rely on digital tools for efficient patient management and outcome tracking. The increasing integration of AI and machine learning will unlock unprecedented capabilities in personalized medicine and predictive diagnostics, further enhancing the value proposition of eHealth solutions. Emerging markets represent a significant opportunity, as developing nations increasingly invest in building digital health infrastructure to improve access to healthcare for their populations. The continuous evolution of wearable technology and the Internet of Medical Things (IoMT) will fuel the demand for advanced remote patient monitoring and proactive health management services. The market is projected to experience robust expansion, with an estimated market size reaching hundreds of billions by 2033, presenting substantial opportunities for both established players and new entrants.

Ehealth Software And Service Segmentation

-

1. Application

- 1.1. Healthcare Institutions

- 1.2. Physicians

- 1.3. Healthcare Workers

- 1.4. Individuals

-

2. Type

- 2.1. eHealth Software

- 2.2. eHealth Services

Ehealth Software And Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ehealth Software And Service Regional Market Share

Geographic Coverage of Ehealth Software And Service

Ehealth Software And Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Healthcare Institutions

- 5.1.2. Physicians

- 5.1.3. Healthcare Workers

- 5.1.4. Individuals

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. eHealth Software

- 5.2.2. eHealth Services

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Ehealth Software And Service Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Healthcare Institutions

- 6.1.2. Physicians

- 6.1.3. Healthcare Workers

- 6.1.4. Individuals

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. eHealth Software

- 6.2.2. eHealth Services

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Ehealth Software And Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Healthcare Institutions

- 7.1.2. Physicians

- 7.1.3. Healthcare Workers

- 7.1.4. Individuals

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. eHealth Software

- 7.2.2. eHealth Services

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Ehealth Software And Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Healthcare Institutions

- 8.1.2. Physicians

- 8.1.3. Healthcare Workers

- 8.1.4. Individuals

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. eHealth Software

- 8.2.2. eHealth Services

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Ehealth Software And Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Healthcare Institutions

- 9.1.2. Physicians

- 9.1.3. Healthcare Workers

- 9.1.4. Individuals

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. eHealth Software

- 9.2.2. eHealth Services

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Ehealth Software And Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Healthcare Institutions

- 10.1.2. Physicians

- 10.1.3. Healthcare Workers

- 10.1.4. Individuals

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. eHealth Software

- 10.2.2. eHealth Services

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Ehealth Software And Service Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Healthcare Institutions

- 11.1.2. Physicians

- 11.1.3. Healthcare Workers

- 11.1.4. Individuals

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. eHealth Software

- 11.2.2. eHealth Services

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 McKesson Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 eHealth Technologies

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 GE Healthcare

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Johnson and Johnson Healthcare Systems

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Aerotel Medical Systems

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Siemens

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Allscripts Healthcare Solutions

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 RamSoft

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Apple

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Fitbit

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sectra

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Doctor on Demand

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 eRAD

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 AdvancedMD

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 KareXpert Technologies

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 McKesson Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ehealth Software And Service Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Ehealth Software And Service Revenue (million), by Application 2025 & 2033

- Figure 3: North America Ehealth Software And Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Ehealth Software And Service Revenue (million), by Type 2025 & 2033

- Figure 5: North America Ehealth Software And Service Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Ehealth Software And Service Revenue (million), by Country 2025 & 2033

- Figure 7: North America Ehealth Software And Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ehealth Software And Service Revenue (million), by Application 2025 & 2033

- Figure 9: South America Ehealth Software And Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Ehealth Software And Service Revenue (million), by Type 2025 & 2033

- Figure 11: South America Ehealth Software And Service Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Ehealth Software And Service Revenue (million), by Country 2025 & 2033

- Figure 13: South America Ehealth Software And Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ehealth Software And Service Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Ehealth Software And Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ehealth Software And Service Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Ehealth Software And Service Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Ehealth Software And Service Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Ehealth Software And Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ehealth Software And Service Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Ehealth Software And Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Ehealth Software And Service Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Ehealth Software And Service Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Ehealth Software And Service Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ehealth Software And Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ehealth Software And Service Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Ehealth Software And Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Ehealth Software And Service Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Ehealth Software And Service Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Ehealth Software And Service Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Ehealth Software And Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ehealth Software And Service Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Ehealth Software And Service Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Ehealth Software And Service Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Ehealth Software And Service Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Ehealth Software And Service Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Ehealth Software And Service Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Ehealth Software And Service Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Ehealth Software And Service Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Ehealth Software And Service Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Ehealth Software And Service Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Ehealth Software And Service Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Ehealth Software And Service Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Ehealth Software And Service Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Ehealth Software And Service Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Ehealth Software And Service Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Ehealth Software And Service Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Ehealth Software And Service Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Ehealth Software And Service Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ehealth Software And Service Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ehealth Software And Service?

The projected CAGR is approximately 8.8%.

2. Which companies are prominent players in the Ehealth Software And Service?

Key companies in the market include McKesson Corporation, eHealth Technologies, GE Healthcare, Johnson and Johnson Healthcare Systems, Aerotel Medical Systems, Siemens, Allscripts Healthcare Solutions, RamSoft, Apple, Fitbit, Sectra, Doctor on Demand, eRAD, AdvancedMD, KareXpert Technologies.

3. What are the main segments of the Ehealth Software And Service?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 600340 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ehealth Software And Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ehealth Software And Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ehealth Software And Service?

To stay informed about further developments, trends, and reports in the Ehealth Software And Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence