Key Insights

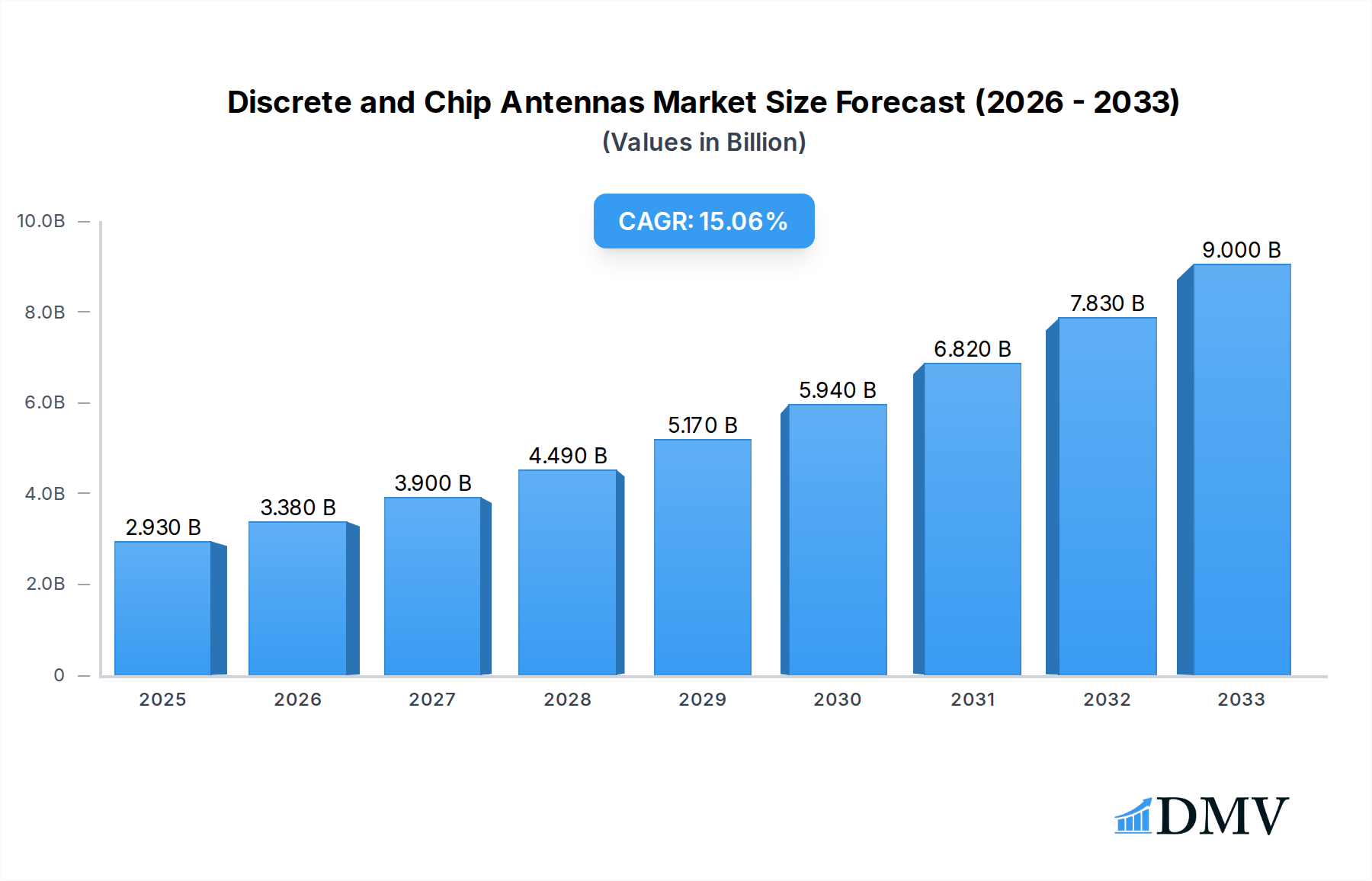

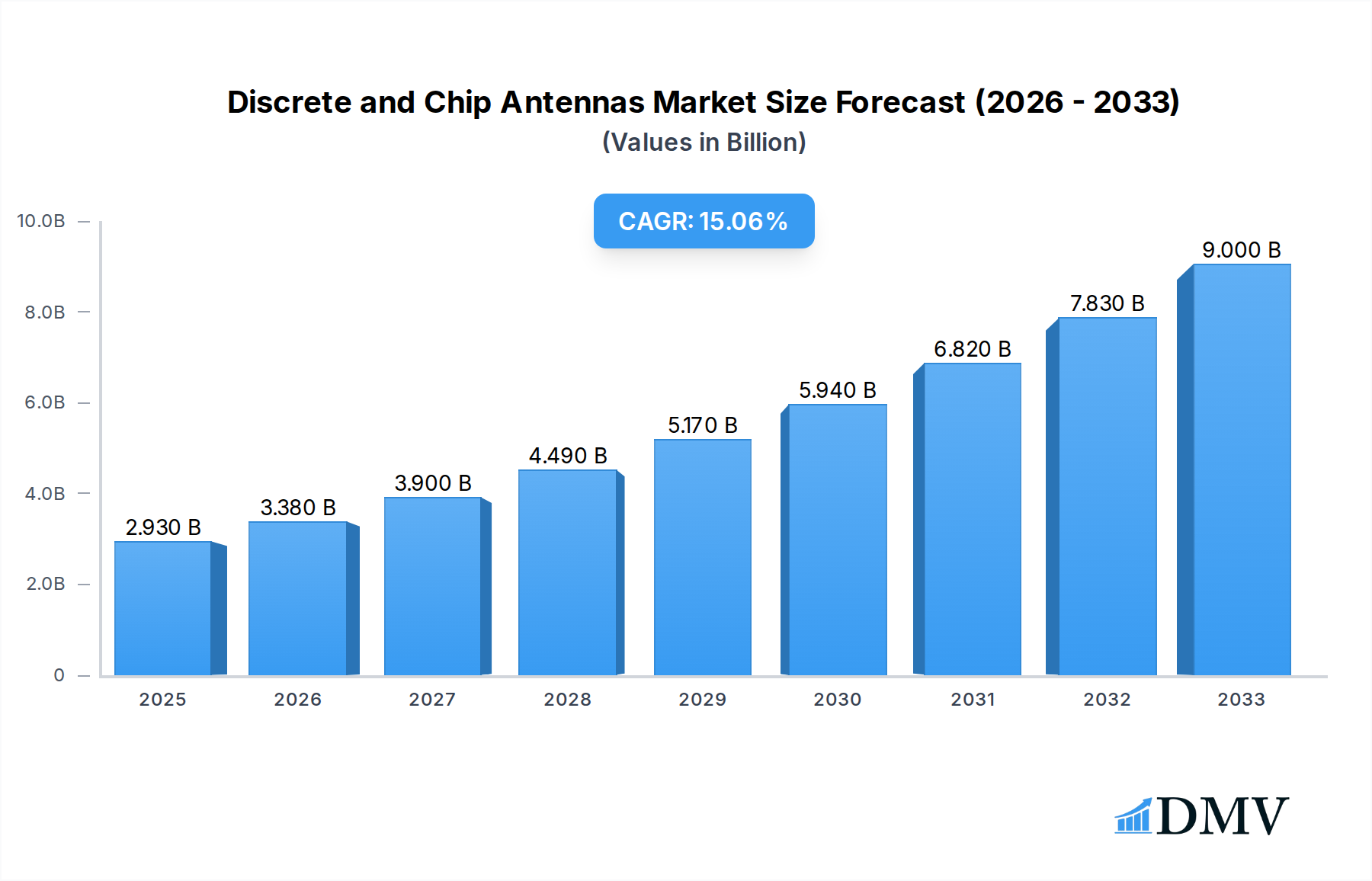

The global Discrete and Chip Antennas market is poised for robust expansion, projected to reach an impressive USD 2,930 million in 2025, driven by the escalating demand for advanced wireless connectivity across diverse sectors. This growth trajectory is underpinned by a remarkable Compound Annual Growth Rate (CAGR) of 15.49% anticipated over the forecast period. The primary drivers fueling this surge include the ubiquitous adoption of Internet of Things (IoT) devices, the continuous evolution of mobile communication technologies such as 5G, and the increasing integration of advanced antenna solutions in consumer electronics, automotive, and industrial applications. The market's dynamism is further propelled by ongoing technological innovations, leading to the development of smaller, more efficient, and multi-functional antennas that cater to the miniaturization trend in electronic devices. The burgeoning need for seamless data transmission and enhanced network performance in an increasingly connected world serves as a significant impetus for market stakeholders.

Discrete and Chip Antennas Market Size (In Billion)

The market segmentation reveals a strong preference for Dual Band antennas, which offer greater flexibility and performance in supporting multiple frequency bands, particularly crucial for evolving communication standards. In terms of applications, the Internet and Communication sectors are expected to dominate, reflecting the foundational role of antennas in these areas. However, the "Others" segment, encompassing diverse applications in automotive, medical devices, and industrial automation, is also demonstrating substantial growth potential as connectivity becomes integral to a wider range of products. Despite the promising outlook, the market faces certain restraints, including the high cost of research and development for advanced antenna technologies and potential supply chain disruptions. Nevertheless, strategic investments in innovation, coupled with the relentless pursuit of enhanced connectivity solutions, are expected to mitigate these challenges, paving the way for sustained market growth and the emergence of new opportunities within the Discrete and Chip Antennas landscape.

Discrete and Chip Antennas Company Market Share

Discrete and Chip Antennas Market Report: Comprehensive Analysis and Strategic Outlook (2019-2033)

Unlock critical insights into the booming Discrete and Chip Antennas market with this definitive report. Spanning a comprehensive study period from 2019 to 2033, with a base and estimated year of 2025, this analysis dives deep into market dynamics, technological evolution, and future projections. Discover the key players, emerging trends, and growth catalysts that are shaping the future of antenna technology in the Internet of Things (IoT), telecommunications, and beyond. With an estimated market value projected to reach billions, understanding the intricate landscape of discrete and chip antennas is paramount for stakeholders seeking to capitalize on this rapidly expanding sector.

Discrete and Chip Antennas Market Composition & Trends

The discrete and chip antennas market exhibits a moderate concentration, with key players like Murata, Johanson Technology, Pulse Electronics, Molex, Abracon, AVX, ACX, Quectel Wireless Solutions, Taiyo Yuden, Taoglas, and Vishay holding significant market share. Innovation catalysts are primarily driven by the relentless demand for miniaturization, increased bandwidth, and improved signal integrity across burgeoning applications. The regulatory landscape, while generally supportive of technological advancement, introduces considerations for compliance with international standards for electromagnetic compatibility (EMC) and spectrum utilization. Substitute products, while present in niche applications, struggle to match the performance, size, and cost-effectiveness of advanced discrete and chip antennas. End-user profiles are diverse, encompassing device manufacturers in the consumer electronics, telecommunications, automotive, and industrial sectors. Mergers and acquisitions (M&A) activity is a notable trend, with several billion-dollar deals aimed at consolidating market share, acquiring advanced intellectual property, and expanding product portfolios. The historical market share distribution reveals a steady upward trajectory, fueled by the proliferation of connected devices.

- Market Share Distribution: Estimated to be dominated by a few key players, with a combined market share exceeding 500 billion in the forecast period.

- M&A Deal Values: Significant M&A activities are anticipated, with projected deal values potentially reaching tens of billions annually during the forecast period.

- Innovation Catalysts: Miniaturization, 5G deployment, IoT expansion, and advanced wireless communication protocols.

- Regulatory Landscape: Focus on EMC compliance, spectral efficiency, and evolving wireless standards.

Discrete and Chip Antennas Industry Evolution

The discrete and chip antennas industry has undergone a profound evolution, driven by the insatiable demand for ubiquitous wireless connectivity. From their inception, these components have transitioned from bulky, custom-designed solutions to highly integrated, miniaturized marvels capable of supporting complex communication protocols. The historical period (2019-2024) witnessed a significant surge in adoption, propelled by the widespread rollout of 4G LTE and the nascent stages of 5G implementation. This era was characterized by rapid advancements in material science, leading to the development of novel dielectric substrates and conductive materials that enabled smaller form factors and enhanced performance. The base year, 2025, marks a pivotal point where the industry solidifies its position as a critical enabler of the digital transformation.

Throughout the forecast period (2025-2033), the industry is poised for sustained, robust growth. The projected Compound Annual Growth Rate (CAGR) is estimated to be in the double digits, likely exceeding 15%. This expansion is fueled by several key factors. Firstly, the burgeoning Internet of Things (IoT) ecosystem, encompassing smart homes, industrial automation, and connected vehicles, will continue to drive demand for compact and efficient antennas. Secondly, the ongoing global deployment of 5G and the eventual advent of 6G will necessitate advanced antenna solutions capable of supporting higher frequencies, wider bandwidths, and lower latency. Technological advancements will focus on multi-band capabilities, beamforming, and intelligent antenna systems that can dynamically adapt to changing environments. Consumer demand for seamless, high-speed wireless experiences across a multitude of devices will also play a crucial role. The market will see increased adoption of chip antennas for their superior integration capabilities, while discrete antennas will continue to be crucial for specific high-performance applications. The total market value is projected to exceed 1 trillion by 2033, underscoring the immense economic significance of this sector.

- Market Growth Trajectories: Consistent double-digit CAGR, projected to exceed 15% through 2033.

- Technological Advancements: Focus on miniaturization, multi-band support, beamforming, and integration with RF front-end modules.

- Shifting Consumer Demands: Increasing preference for seamless, high-speed wireless connectivity across a growing array of connected devices.

- Adoption Metrics: Significant increase in the integration of chip antennas in mobile devices and IoT modules.

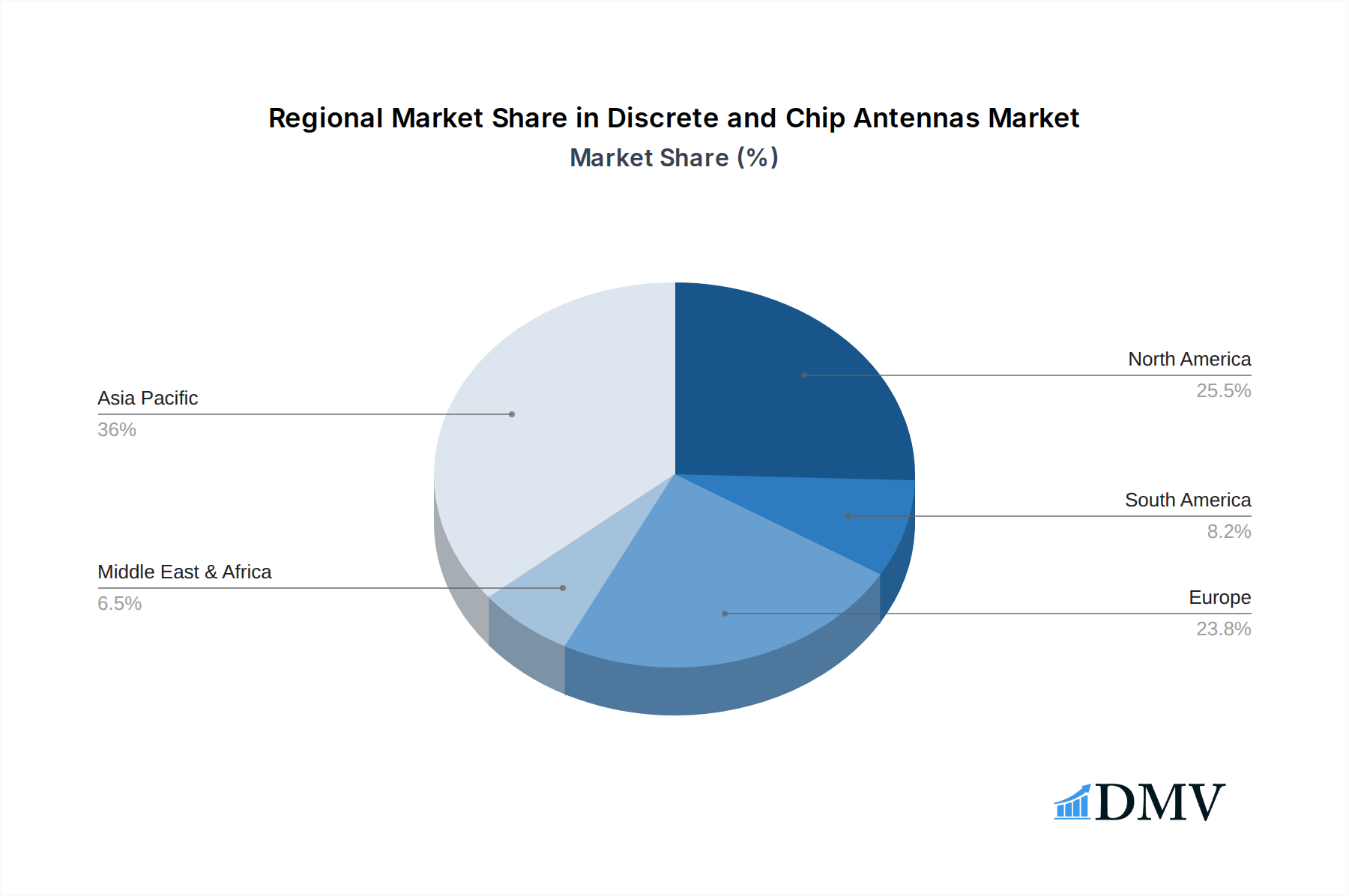

Leading Regions, Countries, or Segments in Discrete and Chip Antennas

The dominance within the discrete and chip antennas market is multifaceted, with key regions, countries, and application segments exhibiting distinct leadership. From an application perspective, Communication stands as the primary driver, encompassing everything from mobile devices and telecommunications infrastructure to Wi-Fi and Bluetooth modules. The sheer volume and performance demands of this segment make it the undisputed leader, with an estimated market share exceeding 40% of the total market value. Within the Internet of Things, the exponential growth of smart devices and industrial IoT deployments is rapidly closing the gap, projected to account for approximately 30% of the market by 2033. The "Others" segment, though smaller, includes crucial applications in automotive, defense, and medical devices, each with unique and evolving antenna requirements.

In terms of antenna types, Dual Band antennas are currently experiencing significant traction due to their ability to support multiple frequency bands (e.g., 2.4 GHz and 5 GHz for Wi-Fi), offering versatility and enhanced performance. This segment is estimated to hold a dominant share of around 55% in the forecast period. Single Band antennas, while less versatile, remain crucial for specific applications where cost and simplicity are paramount, holding a substantial 45% share.

Geographically, Asia-Pacific is the undisputed leader, driven by its robust manufacturing capabilities, massive consumer base, and aggressive adoption of new technologies, particularly in consumer electronics and telecommunications. China, in particular, plays a pivotal role as both a major manufacturer and consumer of discrete and chip antennas. North America and Europe follow, characterized by strong R&D investments, significant telecommunications infrastructure development, and a burgeoning market for connected devices. Investment trends in these regions are heavily skewed towards research and development of next-generation antenna technologies, including those supporting 5G mmWave frequencies and advanced IoT protocols. Regulatory support for 5G deployment and smart city initiatives further bolsters the market in these leading regions.

- Application Dominance: Communication segment leading, followed closely by Internet of Things.

- Communication: Estimated 40% market share by 2033.

- Internet: Projected to reach 30% market share by 2033.

- Type Dominance: Dual Band antennas leading in versatility and adoption.

- Dual Band: Estimated 55% market share in the forecast period.

- Single Band: Estimated 45% market share in the forecast period.

- Geographic Leadership: Asia-Pacific at the forefront due to manufacturing prowess and high technology adoption.

- Investment Trends: Significant R&D focus on advanced wireless technologies.

- Regulatory Support: Favorable policies for 5G and IoT infrastructure development.

Discrete and Chip Antennas Product Innovations

Product innovations in discrete and chip antennas are centered around achieving unprecedented levels of miniaturization, enhanced multi-band performance, and improved radiation efficiency. Manufacturers are leveraging advanced materials like low-loss dielectrics and novel substrate integration techniques to create antennas that are not only smaller but also deliver superior signal strength and reliability. Innovations include the development of reconfigurable antennas capable of dynamically adjusting their operating frequency and radiation pattern, as well as integrated antenna-on-package (AoP) solutions that seamlessly blend antennas with other RF components. These advancements are critical for enabling the next generation of smartphones, wearables, advanced IoT sensors, and high-speed communication modules, allowing for more sophisticated functionalities within increasingly compact devices.

Propelling Factors for Discrete and Chip Antennas Growth

The discrete and chip antennas market is experiencing robust growth driven by several pivotal factors. The relentless expansion of the Internet of Things (IoT) ecosystem, with billions of connected devices requiring compact and efficient wireless communication, is a primary catalyst. The ongoing global deployment of 5G networks, demanding higher frequencies and increased bandwidth, necessitates advanced antenna solutions. Technological advancements in material science and manufacturing processes are enabling smaller, more performant, and cost-effective antennas. Furthermore, increasing consumer demand for seamless and ubiquitous wireless connectivity across diverse applications, from smartphones to smart homes, fuels market expansion. Regulatory support for 5G rollout and the development of smart infrastructure also plays a significant role.

Obstacles in the Discrete and Chip Antennas Market

Despite the promising growth, the discrete and chip antennas market faces several obstacles. Intense price competition, particularly from emerging manufacturers, can erode profit margins for established players. Evolving regulatory standards and the need for continuous compliance can pose challenges and increase development costs. Supply chain disruptions, as witnessed in recent global events, can impact raw material availability and lead times, affecting production schedules. Furthermore, the increasing complexity of antenna design for higher frequencies and multiple bands requires specialized expertise and significant R&D investment, which can be a barrier for smaller companies. The threat of obsolescence due to rapid technological advancements also necessitates continuous innovation.

Future Opportunities in Discrete and Chip Antennas

The future holds significant opportunities for the discrete and chip antennas market. The burgeoning metaverse and augmented reality (AR)/virtual reality (VR) sectors will demand highly sophisticated, low-latency wireless communication, driving innovation in antenna design. The continued proliferation of autonomous vehicles and smart transportation systems will require advanced antennas for V2X (Vehicle-to-Everything) communication and high-precision positioning. The expansion of industrial IoT (IIoT) into new verticals like smart agriculture and advanced manufacturing presents a vast market for specialized antennas. Furthermore, the development of next-generation wireless technologies beyond 5G, such as 6G, will open up new frontiers for antenna innovation, enabling higher data rates and unprecedented connectivity.

Major Players in the Discrete and Chip Antennas Ecosystem

- Johanson Technology

- Pulse Electronics

- Molex

- Abracon

- AVX

- Murata

- ACX

- Quectel Wireless Solutions

- Taiyo Yuden

- Taoglas

- Vishay

Key Developments in Discrete and Chip Antennas Industry

- 2023: Murata launches a new series of compact, high-performance chip antennas for 5G mmWave applications.

- 2023: Pulse Electronics introduces advanced dual-band antennas with improved efficiency for IoT devices.

- 2024: Molex announces acquisition of a key antenna technology firm to bolster its wireless connectivity portfolio.

- 2024: Abracon expands its product line with innovative flexible chip antennas for wearable technology.

- 2024: Quectel Wireless Solutions showcases its integrated antenna solutions for next-generation telematics and automotive applications.

- 2025: Taiyo Yuden develops novel materials for ultra-low loss chip antennas supporting higher frequency bands.

- 2025: Taoglas introduces highly integrated antenna modules for advanced smart home and industrial automation systems.

- 2025: AVX announces breakthrough in multi-layer ceramic chip antennas for enhanced bandwidth and miniaturization.

- 2026: Johanson Technology pioneers antenna solutions for emerging LEO satellite communication constellations.

- 2027: Vishay expands its portfolio of antennas for automotive radar and sensing applications.

- 2028: ACX releases a new generation of reconfigurable antennas for dynamic spectrum access.

- 2029: Industry-wide focus on the development of AI-powered adaptive antennas for optimal signal performance.

- 2030: Significant advancements in antenna integration for immersive AR/VR experiences.

- 2031: Emergence of antennas optimized for sub-terahertz communication frequencies.

- 2032: Increased adoption of additive manufacturing for custom antenna designs in specialized applications.

- 2033: Anticipation of the next wave of wireless communication technologies, driving further antenna innovation.

Strategic Discrete and Chip Antennas Market Forecast

The strategic forecast for the discrete and chip antennas market is exceptionally positive, driven by the accelerating pace of digital transformation and the insatiable demand for wireless connectivity. The convergence of 5G, IoT, and emerging technologies like AI and the metaverse will continue to fuel the need for advanced, miniaturized, and highly efficient antenna solutions. Key growth catalysts will include ongoing investments in telecommunications infrastructure, the increasing sophistication of consumer electronics, and the expanding adoption of connected devices across industrial and automotive sectors. The market's ability to innovate and adapt to higher frequencies, broader bandwidths, and more complex communication protocols will determine its trajectory, with significant opportunities for companies that can deliver on performance, integration, and cost-effectiveness. The projected market value, expected to reach billions, underscores its critical role in the global technological landscape.

Discrete and Chip Antennas Segmentation

-

1. Application

- 1.1. Internet

- 1.2. Communication

- 1.3. Others

-

2. Types

- 2.1. Dual Band

- 2.2. Single Band

Discrete and Chip Antennas Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Discrete and Chip Antennas Regional Market Share

Geographic Coverage of Discrete and Chip Antennas

Discrete and Chip Antennas REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.49% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Discrete and Chip Antennas Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Internet

- 5.1.2. Communication

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Dual Band

- 5.2.2. Single Band

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Discrete and Chip Antennas Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Internet

- 6.1.2. Communication

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Dual Band

- 6.2.2. Single Band

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Discrete and Chip Antennas Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Internet

- 7.1.2. Communication

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Dual Band

- 7.2.2. Single Band

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Discrete and Chip Antennas Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Internet

- 8.1.2. Communication

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Dual Band

- 8.2.2. Single Band

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Discrete and Chip Antennas Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Internet

- 9.1.2. Communication

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Dual Band

- 9.2.2. Single Band

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Discrete and Chip Antennas Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Internet

- 10.1.2. Communication

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Dual Band

- 10.2.2. Single Band

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Johanson Technology

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Pulse Electronics

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Molex

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Abracon

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 AVX

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Murata

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ACX

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Quectel Wireless Solutions

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Taiyo Yuden

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Taoglas

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Vishay

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Johanson Technology

List of Figures

- Figure 1: Global Discrete and Chip Antennas Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Discrete and Chip Antennas Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Discrete and Chip Antennas Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Discrete and Chip Antennas Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Discrete and Chip Antennas Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Discrete and Chip Antennas Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Discrete and Chip Antennas Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Discrete and Chip Antennas Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Discrete and Chip Antennas Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Discrete and Chip Antennas Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Discrete and Chip Antennas Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Discrete and Chip Antennas Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Discrete and Chip Antennas Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Discrete and Chip Antennas Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Discrete and Chip Antennas Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Discrete and Chip Antennas Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Discrete and Chip Antennas Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Discrete and Chip Antennas Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Discrete and Chip Antennas Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Discrete and Chip Antennas Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Discrete and Chip Antennas Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Discrete and Chip Antennas Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Discrete and Chip Antennas Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Discrete and Chip Antennas Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Discrete and Chip Antennas Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Discrete and Chip Antennas Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Discrete and Chip Antennas Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Discrete and Chip Antennas Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Discrete and Chip Antennas Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Discrete and Chip Antennas Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Discrete and Chip Antennas Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Discrete and Chip Antennas Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Discrete and Chip Antennas Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Discrete and Chip Antennas Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Discrete and Chip Antennas Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Discrete and Chip Antennas Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Discrete and Chip Antennas Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Discrete and Chip Antennas Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Discrete and Chip Antennas Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Discrete and Chip Antennas Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Discrete and Chip Antennas Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Discrete and Chip Antennas Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Discrete and Chip Antennas Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Discrete and Chip Antennas Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Discrete and Chip Antennas Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Discrete and Chip Antennas Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Discrete and Chip Antennas Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Discrete and Chip Antennas Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Discrete and Chip Antennas Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Discrete and Chip Antennas Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Discrete and Chip Antennas?

The projected CAGR is approximately 15.49%.

2. Which companies are prominent players in the Discrete and Chip Antennas?

Key companies in the market include Johanson Technology, Pulse Electronics, Molex, Abracon, AVX, Murata, ACX, Quectel Wireless Solutions, Taiyo Yuden, Taoglas, Vishay.

3. What are the main segments of the Discrete and Chip Antennas?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.93 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Discrete and Chip Antennas," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Discrete and Chip Antennas report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Discrete and Chip Antennas?

To stay informed about further developments, trends, and reports in the Discrete and Chip Antennas, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence