Key Insights

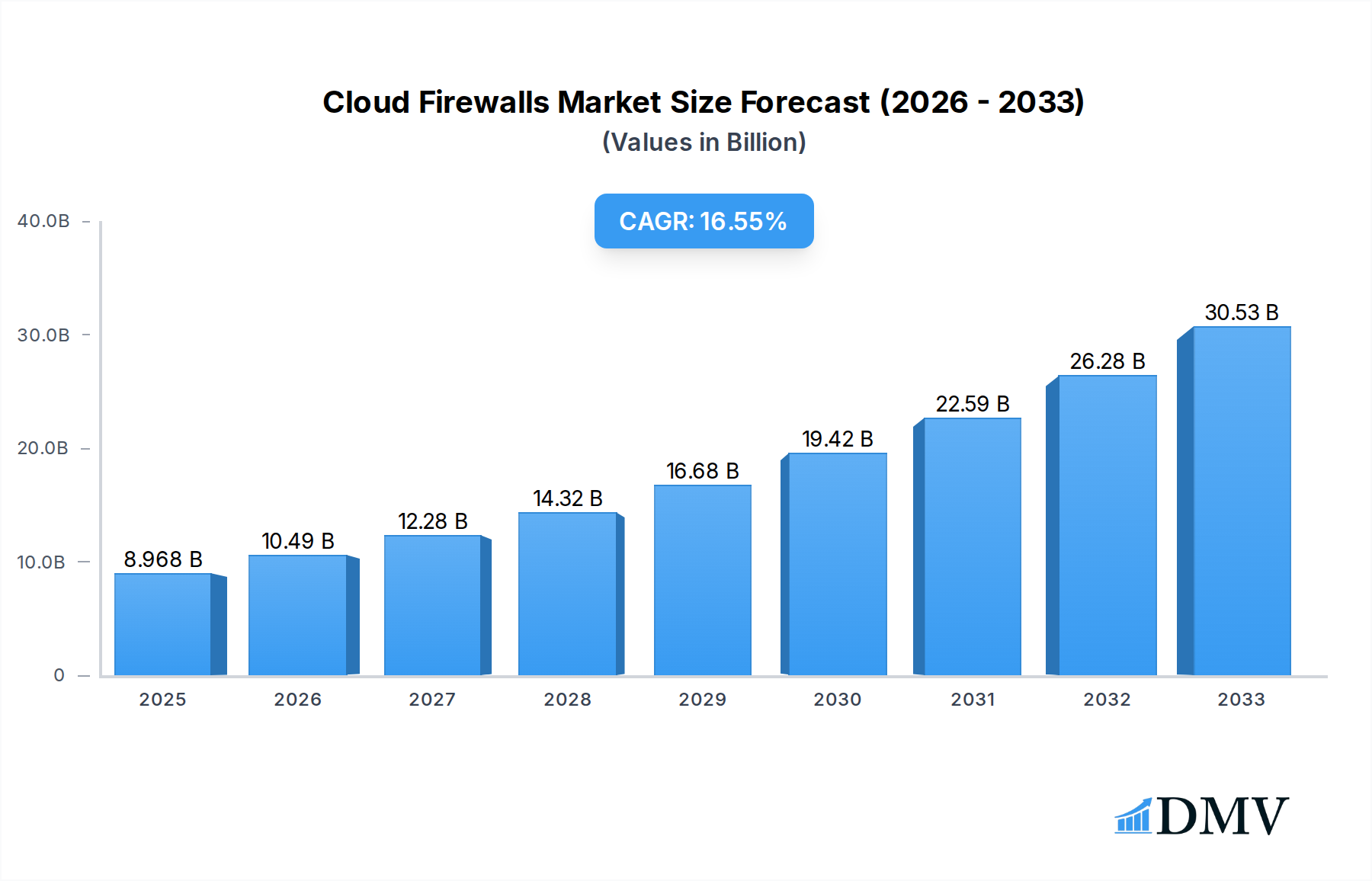

The global Cloud Firewall market is poised for substantial expansion, projected to reach USD 8968 million by 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 17.1% throughout the forecast period of 2025-2033. This robust growth is fueled by the escalating adoption of cloud computing across various industries, necessitating advanced security solutions to protect sensitive data and critical infrastructure. Key market drivers include the increasing frequency and sophistication of cyber threats, stringent regulatory compliance mandates, and the growing demand for scalable and flexible security perimeters that can adapt to dynamic cloud environments. The BFSI, IT and Telecom, and Government sectors are expected to be major contributors to this market expansion, owing to their high reliance on digital platforms and the critical nature of the data they handle.

Cloud Firewalls Market Size (In Billion)

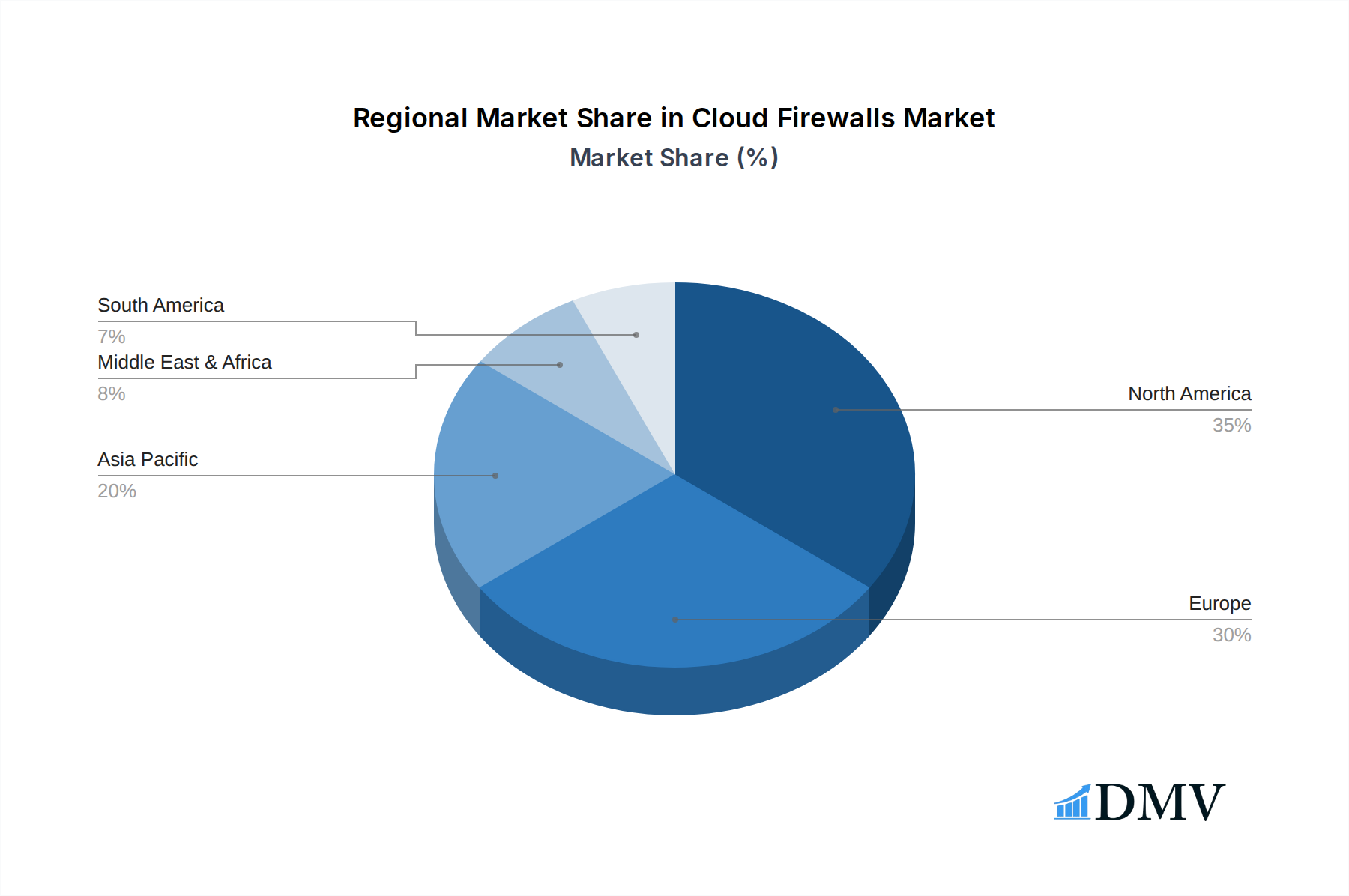

The market segmentation offers diverse opportunities, with "Next Generation Firewalls" and "SaaS Firewalls" representing key technological advancements catering to evolving security needs. While the market benefits from strong growth drivers, certain restraints such as the complexity of integration with existing legacy systems and the shortage of skilled cybersecurity professionals may pose challenges. However, continuous innovation in cloud-native security technologies, the emergence of advanced threat intelligence, and the increasing affordability of cloud firewall solutions are expected to mitigate these challenges. Geographically, North America and Europe are anticipated to dominate the market, followed closely by the Asia Pacific region, which is experiencing rapid digital transformation and a surge in cloud adoption. Emerging economies in Asia Pacific and Latin America present significant untapped potential for market players.

Cloud Firewalls Company Market Share

Cloud Firewalls Market Composition & Trends

The global Cloud Firewalls market is characterized by a dynamic interplay of innovation, regulatory shifts, and evolving end-user demands, projecting a robust growth trajectory. Market concentration is moderately fragmented, with key players like Zscaler, Inc., Barracuda Networks, Inc., Cloudflare, Inc., Fortinet, Inc., and Palo Alto Networks, Inc. spearheading advancements. These companies are investing heavily in research and development, fostering a competitive landscape where continuous innovation is paramount. Regulatory landscapes, particularly concerning data privacy and cybersecurity mandates, are acting as significant catalysts, compelling organizations across all sectors to enhance their cloud security posture. The emergence of advanced threat detection capabilities, AI-driven security analytics, and zero-trust network access models are redefining the value proposition of cloud firewalls. Substitute products, while present in the form of traditional on-premises firewalls, are increasingly being overshadowed by the agility, scalability, and cost-effectiveness of cloud-native solutions. End-user profiles span a wide spectrum, with the BFSI, IT and Telecom, and Government segments leading adoption due to their stringent security requirements and extensive cloud infrastructure. Mergers and acquisitions (M&A) activities are a notable trend, with estimated deal values reaching several billion dollars, as larger enterprises seek to consolidate their market position and acquire innovative technologies. For instance, recent M&A activities in the past two years have involved transactions valued at approximately $500 million to $2 billion, signaling a strong appetite for strategic consolidation.

- Market Share Distribution: Leading players like Zscaler and Palo Alto Networks are estimated to hold between 10-15% of the market share respectively, with others collectively accounting for the remaining 70-80%.

- M&A Deal Values: Recent strategic acquisitions have ranged from $500 million to $2 billion, reflecting consolidation efforts and a drive for technological integration.

- Innovation Catalysts: Advancements in AI/ML for threat detection, zero-trust architecture integration, and secure access service edge (SASE) frameworks are key drivers.

- Regulatory Impact: Data privacy regulations (e.g., GDPR, CCPA) and industry-specific compliance requirements are major influences on adoption rates.

Cloud Firewalls Industry Evolution

The Cloud Firewalls industry has witnessed a remarkable transformation throughout the historical period of 2019–2024, driven by escalating cybersecurity threats and the pervasive adoption of cloud computing. This evolution is clearly demarcated by significant shifts in technological capabilities and market dynamics, with the base year of 2025 serving as a pivotal point for projected growth. During the historical period, the market experienced a compound annual growth rate (CAGR) of approximately 18%, fueled by initial cloud migration trends and a growing awareness of the limitations of traditional perimeter-based security models. As organizations increasingly shifted their data and applications to cloud environments, the need for integrated, scalable, and intelligent security solutions became paramount. This led to a surge in demand for both SaaS Firewalls and Next Generation Firewalls (NGFWs) deployed in cloud infrastructure. The forecast period, spanning from 2025 to 2033, is anticipated to witness an even more accelerated growth trajectory, with an estimated CAGR of around 22%. This heightened growth is attributable to several factors, including the continued expansion of cloud services, the rise of remote workforces, the increasing sophistication of cyberattacks, and the growing adoption of hybrid and multi-cloud environments. Technological advancements have been central to this evolution. Early cloud firewalls primarily focused on basic packet filtering, but they have rapidly evolved to incorporate advanced features such as intrusion prevention systems (IPS), application awareness, deep packet inspection (DPI), SSL/TLS decryption, and sophisticated threat intelligence feeds. The integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms has further enhanced their efficacy, enabling proactive threat detection, automated response, and predictive analytics. Shifting consumer demands, particularly from enterprises, have emphasized the need for unified security platforms that can manage security policies across diverse cloud deployments and on-premises infrastructure. This has propelled the development of SASE solutions, which converge networking and security functions into a cloud-delivered service, offering a more integrated and agile approach to securing distributed workforces and cloud resources. The market's growth is further bolstered by the increasing implementation of cloud-native security solutions that seamlessly integrate with cloud platforms like AWS, Azure, and Google Cloud. The increasing complexity of the threat landscape, including advanced persistent threats (APTs) and ransomware attacks, necessitates robust and adaptive security measures, positioning cloud firewalls as indispensable components of modern cybersecurity strategies. The market size, which was estimated to be around $5 billion in 2024, is projected to expand significantly, reaching an estimated $30 billion by 2033, underscoring the immense growth potential within this sector.

- Historical Growth (2019-2024): Approximately 18% CAGR.

- Projected Growth (2025-2033): Estimated 22% CAGR.

- Market Size (2024): Estimated $5 billion.

- Market Size (2033): Projected to reach $30 billion.

- Technological Evolution: From basic packet filtering to AI/ML-powered threat intelligence, SASE integration, and deep packet inspection.

- Demand Drivers: Cloud adoption, remote work, sophisticated cyberattacks, and hybrid/multi-cloud environments.

Leading Regions, Countries, or Segments in Cloud Firewalls

The global Cloud Firewalls market demonstrates distinct regional dominance and segment leadership, driven by a confluence of technological adoption, regulatory frameworks, and industry-specific security imperatives. North America currently leads the market, primarily due to its high adoption rates of cloud technologies, robust cybersecurity investments, and a strong presence of leading technology companies. Within North America, the United States stands out as a key contributor, propelled by its extensive IT infrastructure and stringent data protection regulations. The BFSI sector is a dominant application segment, accounting for an estimated 25% of the total market revenue. Financial institutions are compelled by regulatory compliance mandates and the sheer volume of sensitive data they handle to implement advanced cloud firewall solutions for protecting against sophisticated financial fraud and cyber espionage. Following closely is the IT and Telecom sector, representing approximately 20% of the market, as these industries are at the forefront of digital transformation and rely heavily on secure cloud infrastructure to deliver their services. The Government and Public Utilities segment also plays a crucial role, with an increasing focus on national security and critical infrastructure protection driving substantial investments in cloud security, estimated at around 18% of the market.

In terms of product type, SaaS Firewalls are experiencing rapid growth, capturing an estimated 55% of the market share. Their ease of deployment, scalability, and subscription-based pricing model make them highly attractive to businesses of all sizes, particularly SMBs. Next Generation Firewalls (NGFWs), while still significant, are expected to hold around 45% of the market, with a strong emphasis on advanced threat prevention capabilities and integration with broader security ecosystems. Key drivers for this segment dominance include significant government initiatives aimed at enhancing cybersecurity for critical national infrastructure, substantial private sector investments in cloud security solutions, and a proactive approach to regulatory compliance. For instance, government funding for cybersecurity research and development in the US and Canada amounts to billions of dollars annually, directly impacting the adoption of advanced cloud firewall technologies. Furthermore, the increasing trend of digital transformation across all industries in North America necessitates secure and scalable cloud solutions, making cloud firewalls an integral part of their IT architecture. The emphasis on zero-trust security models and the growing threat of sophisticated cyberattacks like ransomware and APTs further amplify the demand for comprehensive cloud firewall solutions in this region.

- Dominant Region: North America, particularly the United States.

- Leading Application Segments:

- BFSI: ~25% market share, driven by regulatory compliance and data sensitivity.

- IT and Telecom: ~20% market share, due to extensive cloud infrastructure and digital transformation.

- Government and Public Utilities: ~18% market share, fueled by national security and critical infrastructure protection.

- Dominant Product Type:

- SaaS Firewalls: ~55% market share, favored for scalability and ease of deployment.

- Next Generation Firewalls (NGFWs): ~45% market share, emphasized for advanced threat prevention.

- Key Drivers for Dominance:

- High cloud adoption rates and robust cybersecurity investments.

- Stringent data protection regulations and compliance mandates.

- Government initiatives for national security and critical infrastructure.

- Increasing threat landscape and adoption of zero-trust architectures.

Cloud Firewalls Product Innovations

Cloud firewall innovation is rapidly advancing, with a strong focus on intelligent threat detection and seamless integration. Next-generation cloud firewalls are now equipped with advanced AI and ML capabilities that enable proactive identification of zero-day threats and sophisticated malware. Unique selling propositions include real-time threat intelligence feeds, automated policy enforcement, and granular application control, offering unparalleled visibility and security for cloud workloads. Performance metrics are continuously improving, with low latency and high throughput becoming standard expectations. Innovations like integrated SASE solutions are further enhancing their value by converging networking and security into a single, cloud-delivered service, providing enhanced agility and simplified management for distributed enterprises.

Propelling Factors for Cloud Firewalls Growth

The growth of the cloud firewalls market is propelled by a confluence of powerful factors. The relentless escalation of sophisticated cyber threats, including ransomware and advanced persistent threats (APTs), is a primary driver, compelling organizations to invest in more robust security solutions. The accelerating pace of cloud adoption across all industries, from BFSI to healthcare, necessitates scalable and agile security infrastructure, for which cloud firewalls are indispensable. Furthermore, the increasing adoption of remote and hybrid work models expands the attack surface, demanding perimeter-less security solutions that cloud firewalls provide. Regulatory mandates for data privacy and compliance, such as GDPR and CCPA, are also playing a significant role, pushing organizations to strengthen their cloud security posture. For instance, increased fines for data breaches are incentivizing proactive security investments.

- Escalating Cyber Threats: The rising sophistication and frequency of attacks.

- Accelerated Cloud Adoption: Pervasive migration of data and applications to cloud environments.

- Remote & Hybrid Workforces: Expansion of the attack surface and need for distributed security.

- Regulatory Compliance: Stringent data privacy laws driving security investments.

- Digital Transformation Initiatives: Demand for secure, scalable IT infrastructure.

Obstacles in the Cloud Firewalls Market

Despite the robust growth, the cloud firewalls market faces several obstacles. The complexity of integrating cloud firewalls with existing legacy IT systems can be a significant challenge for some organizations, leading to extended deployment times and increased costs. Skills shortages in cybersecurity professionals capable of managing and configuring advanced cloud security solutions also pose a restraint. Furthermore, concerns around data privacy and vendor lock-in can deter some potential adopters, particularly smaller enterprises. Supply chain disruptions, although less impactful for software-based solutions, can still affect hardware components for hybrid deployments. The competitive landscape, while driving innovation, can also lead to pricing pressures, impacting profitability for some vendors.

- Integration Complexity: Challenges in merging with existing IT infrastructure.

- Cybersecurity Skills Gap: Shortage of trained professionals for advanced management.

- Data Privacy Concerns: Worries about data security and vendor trustworthiness.

- Vendor Lock-in: Hesitation due to potential long-term dependency on a single provider.

- Pricing Pressures: Intense competition leading to reduced margins.

Future Opportunities in Cloud Firewalls

The future of cloud firewalls presents numerous exciting opportunities. The burgeoning adoption of multi-cloud and hybrid cloud environments creates a demand for unified security management platforms that can seamlessly orchestrate policies across diverse cloud infrastructures. The continued evolution of AI and ML for predictive threat intelligence and automated incident response will open new avenues for advanced security solutions. The growing popularity of edge computing and IoT devices will necessitate specialized cloud firewall solutions tailored for these distributed environments. Emerging markets, particularly in Asia-Pacific and Latin America, are ripe for expansion as cloud adoption accelerates in these regions. The increasing focus on compliance-as-a-service and security orchestration, automation, and response (SOAR) integrations within cloud firewall platforms also represents a significant growth area.

- Multi-cloud & Hybrid Cloud Security: Unified management across diverse platforms.

- AI/ML Advancements: Predictive threat intelligence and automated response.

- Edge Computing & IoT Security: Specialized solutions for distributed environments.

- Emerging Market Expansion: Growth opportunities in Asia-Pacific and Latin America.

- Compliance-as-a-Service & SOAR Integration: Enhanced automation and simplified compliance.

Major Players in the Cloud Firewalls Ecosystem

- Zscaler, Inc.

- Barracuda Networks, Inc.

- Cloudflare, Inc.

- Fortinet, Inc.

- SonicWall

- WatchGuard Technologies

- Cisco

- Juniper

- Palo Alto Networks

- Secucloud

- Check Point

- Allot (Optenet)

- Imperva

- Sophos Technologies Pvt. Ltd

Key Developments in Cloud Firewalls Industry

- January 2024: Palo Alto Networks announced the integration of its Prisma Cloud with major cloud providers, enhancing security for multi-cloud environments.

- November 2023: Zscaler launched new AI-powered threat detection capabilities within its Security Service Edge (SSE) platform.

- August 2023: Cloudflare introduced enhanced DDoS protection for edge computing workloads.

- May 2023: Fortinet expanded its cloud firewall offerings with enhanced support for containerized applications.

- February 2023: Barracuda Networks acquired a cloud security startup specializing in API security.

- October 2022: Cisco unveiled new cloud-native firewall solutions designed for hybrid cloud deployments.

- June 2022: Check Point Software Technologies released advanced SASE solutions for distributed enterprises.

- December 2021: Juniper Networks enhanced its cloud security portfolio with advanced threat intelligence features.

- September 2021: Google Cloud launched new security partnerships to bolster its cloud firewall ecosystem.

- April 2021: Sophos Technologies expanded its cloud security offerings with AI-driven endpoint protection.

Strategic Cloud Firewalls Market Forecast

The strategic forecast for the Cloud Firewalls market is overwhelmingly positive, driven by persistent cybersecurity challenges and the ongoing digital transformation of global enterprises. The increasing adoption of cloud-native security solutions, coupled with the demand for unified SASE frameworks, will be significant growth catalysts. Projections indicate continued innovation in AI and ML integration for proactive threat detection and automated response, further solidifying the indispensable role of cloud firewalls in safeguarding digital assets. Emerging markets and specialized cloud security needs for edge computing will present substantial expansion opportunities, ensuring a robust and dynamic market for years to come.

Cloud Firewalls Segmentation

-

1. Application

- 1.1. BFSI

- 1.2. Retail

- 1.3. IT and Telecom

- 1.4. Government and Public Utilities

- 1.5. Healthcare

- 1.6. Education

- 1.7. Others

-

2. Type

- 2.1. SaaS Firewalls

- 2.2. Next Generation Firewalls

Cloud Firewalls Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cloud Firewalls Regional Market Share

Geographic Coverage of Cloud Firewalls

Cloud Firewalls REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cloud Firewalls Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. BFSI

- 5.1.2. Retail

- 5.1.3. IT and Telecom

- 5.1.4. Government and Public Utilities

- 5.1.5. Healthcare

- 5.1.6. Education

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. SaaS Firewalls

- 5.2.2. Next Generation Firewalls

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Cloud Firewalls Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. BFSI

- 6.1.2. Retail

- 6.1.3. IT and Telecom

- 6.1.4. Government and Public Utilities

- 6.1.5. Healthcare

- 6.1.6. Education

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. SaaS Firewalls

- 6.2.2. Next Generation Firewalls

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Cloud Firewalls Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. BFSI

- 7.1.2. Retail

- 7.1.3. IT and Telecom

- 7.1.4. Government and Public Utilities

- 7.1.5. Healthcare

- 7.1.6. Education

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. SaaS Firewalls

- 7.2.2. Next Generation Firewalls

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Cloud Firewalls Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. BFSI

- 8.1.2. Retail

- 8.1.3. IT and Telecom

- 8.1.4. Government and Public Utilities

- 8.1.5. Healthcare

- 8.1.6. Education

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. SaaS Firewalls

- 8.2.2. Next Generation Firewalls

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Cloud Firewalls Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. BFSI

- 9.1.2. Retail

- 9.1.3. IT and Telecom

- 9.1.4. Government and Public Utilities

- 9.1.5. Healthcare

- 9.1.6. Education

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. SaaS Firewalls

- 9.2.2. Next Generation Firewalls

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Cloud Firewalls Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. BFSI

- 10.1.2. Retail

- 10.1.3. IT and Telecom

- 10.1.4. Government and Public Utilities

- 10.1.5. Healthcare

- 10.1.6. Education

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. SaaS Firewalls

- 10.2.2. Next Generation Firewalls

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Zscaler Inc.

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Barracuda Networks Inc.

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Cloudflare Inc.

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Fortinet Inc.

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SonicWall

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 WatchGuard Technologies

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Cisco

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Juniper

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Palo Alto Networks

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Secucloud

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Check Point

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Allot (Optenet)

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Imperva

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Google

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Sophos Technologies Pvt. Ltd

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Zscaler Inc.

List of Figures

- Figure 1: Global Cloud Firewalls Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Cloud Firewalls Revenue (million), by Application 2025 & 2033

- Figure 3: North America Cloud Firewalls Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cloud Firewalls Revenue (million), by Type 2025 & 2033

- Figure 5: North America Cloud Firewalls Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Cloud Firewalls Revenue (million), by Country 2025 & 2033

- Figure 7: North America Cloud Firewalls Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cloud Firewalls Revenue (million), by Application 2025 & 2033

- Figure 9: South America Cloud Firewalls Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cloud Firewalls Revenue (million), by Type 2025 & 2033

- Figure 11: South America Cloud Firewalls Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Cloud Firewalls Revenue (million), by Country 2025 & 2033

- Figure 13: South America Cloud Firewalls Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cloud Firewalls Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Cloud Firewalls Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cloud Firewalls Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Cloud Firewalls Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Cloud Firewalls Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Cloud Firewalls Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cloud Firewalls Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cloud Firewalls Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cloud Firewalls Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Cloud Firewalls Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Cloud Firewalls Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cloud Firewalls Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cloud Firewalls Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Cloud Firewalls Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cloud Firewalls Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Cloud Firewalls Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Cloud Firewalls Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Cloud Firewalls Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cloud Firewalls Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Cloud Firewalls Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Cloud Firewalls Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Cloud Firewalls Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Cloud Firewalls Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Cloud Firewalls Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Cloud Firewalls Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Cloud Firewalls Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Cloud Firewalls Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Cloud Firewalls Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Cloud Firewalls Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Cloud Firewalls Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Cloud Firewalls Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Cloud Firewalls Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Cloud Firewalls Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Cloud Firewalls Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Cloud Firewalls Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Cloud Firewalls Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cloud Firewalls Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud Firewalls?

The projected CAGR is approximately 17.1%.

2. Which companies are prominent players in the Cloud Firewalls?

Key companies in the market include Zscaler, Inc., Barracuda Networks, Inc., Cloudflare, Inc., Fortinet, Inc., SonicWall, WatchGuard Technologies, Cisco, Juniper, Palo Alto Networks, Secucloud, Check Point, Allot (Optenet), Imperva, Google, Sophos Technologies Pvt. Ltd.

3. What are the main segments of the Cloud Firewalls?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 8968 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cloud Firewalls," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cloud Firewalls report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cloud Firewalls?

To stay informed about further developments, trends, and reports in the Cloud Firewalls, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence