Key Insights

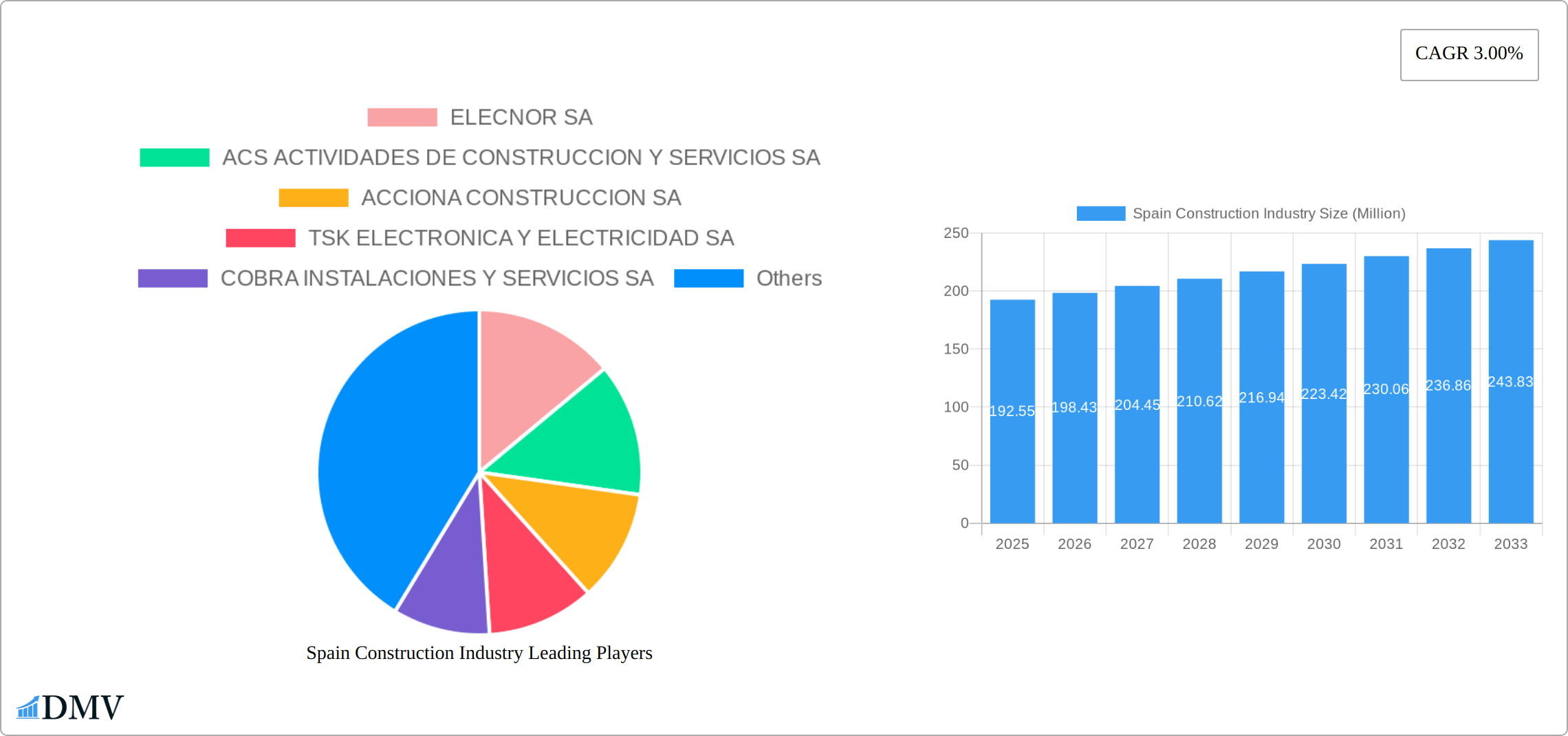

The Spanish construction industry, valued at €192.55 million in 2025, is projected to experience steady growth, driven by several key factors. Government initiatives focused on infrastructure development, particularly in transportation and renewable energy, are significant catalysts. The increasing demand for residential properties fueled by population growth and tourism contributes to the sector's expansion. Furthermore, renovations and refurbishment projects in existing buildings, driven by both environmental concerns and the need for improved energy efficiency, are adding to the market's dynamism. While rising material costs and labor shortages pose challenges, the ongoing recovery of the Spanish economy and consistent investment in infrastructure projects are mitigating these constraints. The sector is segmented into residential, commercial, industrial, infrastructure (transportation), and energy and utilities, with infrastructure projects representing a significant portion of the market’s activity. Major players like Elecnor SA, ACS Actividades de Construcción y Servicios SA, and Acciona Construcción SA hold considerable market share, driving competition and innovation within the industry. The forecast period (2025-2033) anticipates continued growth, albeit at a moderate pace, reflecting both the ongoing economic recovery and the inherent cyclicality of the construction sector.

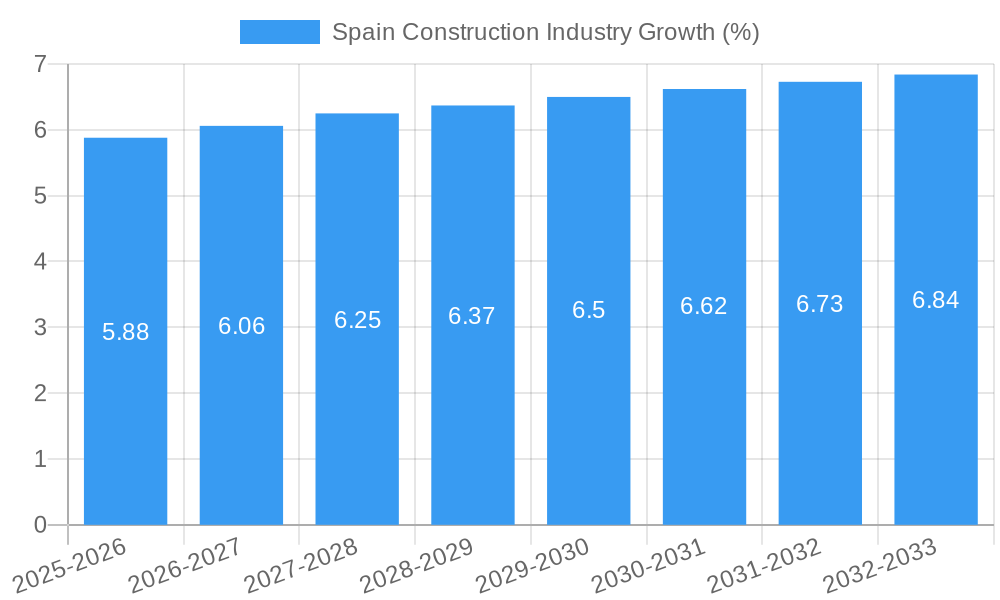

The consistent 3% CAGR indicates a predictable trajectory for growth, although fluctuations may occur based on government policy shifts and broader economic conditions. The strong presence of large, established companies demonstrates the sector's maturity and capacity for handling large-scale projects. However, smaller, specialized firms focused on niche areas, such as sustainable construction or specific building technologies, are also expected to play a increasingly important role, particularly in response to emerging trends in environmentally conscious construction. This healthy mix of established players and agile startups suggests resilience and adaptability within the Spanish construction landscape. The focus on infrastructure projects, particularly transportation and energy, positions the industry for long-term sustainability and aligns with national and EU objectives related to climate change and improved infrastructure.

Spain Construction Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Spain construction industry, offering valuable insights for stakeholders, investors, and industry professionals. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report meticulously examines market trends, leading players, and future growth potential. The report leverages extensive data analysis to deliver actionable intelligence on the Spanish construction landscape, encompassing key segments like residential, commercial, industrial, infrastructure (transportation), and energy & utilities. The total market value in 2025 is estimated at XXX Million, with a projected value of XXX Million by 2033.

Spain Construction Industry Market Composition & Trends

This section delves into the competitive dynamics of the Spanish construction market. We analyze market concentration, revealing the market share distribution amongst key players such as ACS Actividades de Construcción y Servicios SA, Acciona Construcción SA, and Ferrovial Agroman SA. The report also examines the role of innovation, regulatory changes (including the impact of EU directives), and the presence of substitute products impacting the industry's trajectory. Furthermore, we explore end-user profiles across various sectors and provide a detailed overview of M&A activities, including deal values (estimated at XXX Million in total for the period 2019-2024).

- Market Concentration: High concentration with a few dominant players controlling a significant market share. ACS Actividades de Construcción y Servicios SA holds an estimated xx% market share in 2025.

- Innovation Catalysts: Government initiatives promoting sustainable construction practices and technological advancements in building materials.

- Regulatory Landscape: Stringent building codes and environmental regulations influencing project timelines and costs.

- Substitute Products: Growing adoption of prefabricated building components and modular construction methods.

- End-User Profiles: A diverse mix of residential developers, commercial enterprises, and government agencies.

- M&A Activities: Significant M&A activity observed between 2019 and 2024, with a total deal value estimated at XXX Million.

Spain Construction Industry Industry Evolution

This section traces the evolution of the Spain construction industry, analyzing market growth trajectories from 2019 to 2024 and forecasting trends until 2033. We analyze the impact of technological advancements, such as Building Information Modeling (BIM) and the increasing adoption of digital tools, and how they are transforming construction processes. We also examine shifting consumer demands, including the growing preference for sustainable and energy-efficient buildings. The market exhibited a Compound Annual Growth Rate (CAGR) of xx% during 2019-2024, with projections of xx% CAGR during the forecast period. This growth is driven by factors such as increased government investment in infrastructure projects and rising urbanization. Specific data points on technology adoption rates (e.g., BIM software usage) are included.

Leading Regions, Countries, or Segments in Spain Construction Industry

This section identifies the leading segments within the Spain construction market, focusing on residential, commercial, industrial, infrastructure (transportation), and energy & utilities. We analyze the key drivers behind the dominance of each segment, highlighting investment trends, regulatory support, and regional disparities.

- Infrastructure (Transportation): Dominant segment driven by substantial government investments in high-speed rail projects and road infrastructure upgrades.

- Residential: Significant growth fueled by increasing population and demand for housing, particularly in urban areas.

- Key Drivers (Infrastructure):

- Massive investment in high-speed rail projects (ADIF Alta Velocidad plays a significant role).

- Government funding for road and bridge construction and maintenance.

- EU funding for sustainable transportation infrastructure.

- Key Drivers (Residential):

- Rising urbanization and population growth.

- Increased demand for affordable housing.

- Government incentives for sustainable housing developments.

Spain Construction Industry Product Innovations

This section highlights notable product innovations impacting the Spanish construction industry. We focus on new materials, construction techniques, and technologies that offer enhanced performance, sustainability, and cost-effectiveness. Examples include the increasing use of prefabricated components, innovative insulation materials, and the implementation of advanced construction management software. These innovations contribute to increased efficiency, reduced project timelines, and improved building quality.

Propelling Factors for Spain Construction Industry Growth

Several factors fuel the growth of the Spanish construction industry. Government investment in infrastructure projects, particularly in transportation and renewable energy, plays a vital role. Technological advancements, such as BIM and 3D printing, contribute to increased efficiency and productivity. Furthermore, the growing demand for sustainable and energy-efficient buildings presents significant opportunities for market expansion. The recovering economy and supportive regulatory environment further bolster growth.

Obstacles in the Spain Construction Industry Market

The Spain construction industry faces several challenges. Fluctuations in raw material prices and supply chain disruptions can impact project costs and timelines. Stringent regulations and bureaucratic processes can also lead to delays. Furthermore, intense competition among established players and the emergence of new entrants create pressure on profit margins. The impact of these obstacles on overall market growth is quantified where possible.

Future Opportunities in Spain Construction Industry

The future of the Spain construction industry presents exciting opportunities. The growing demand for sustainable building practices creates a market for eco-friendly materials and technologies. Government initiatives promoting digitalization offer potential for innovative solutions. Furthermore, the expanding tourism sector fuels demand for new hotels and infrastructure projects, creating lucrative opportunities for construction companies.

Major Players in the Spain Construction Industry Ecosystem

- Acciona Construcción SA

- ACS Actividades de Construcción y Servicios SA

- ELECNOR SA

- TSK Electrónica y Electricidad SA

- COBRA Instalaciones y Servicios SA

- ADIF Alta Velocidad

- Sacyr Construcción SAU

- Ferrovial Agroman SA

- Dragados Sociedad Anónima

- Obrascón Huarte Lain SA

- Administrador de Infraestructuras Ferroviarias

- FCC Construction SA

Key Developments in Spain Construction Industry Industry

- 2023 Q3: Launch of a new sustainable building material by a major player.

- 2022 Q4: Successful completion of a major infrastructure project (e.g., high-speed rail line).

- 2021 Q2: Merger between two mid-sized construction companies.

Strategic Spain Construction Industry Market Forecast

The Spain construction industry is poised for sustained growth, driven by continuous government investments and technological advancements. The increasing emphasis on sustainable construction presents significant opportunities for companies that can adopt eco-friendly practices. The projected market size of XXX Million in 2033 demonstrates substantial potential for growth and profitability. The forecast takes into account potential economic fluctuations and regulatory changes.

Spain Construction Industry Segmentation

-

1. Sector

- 1.1. Residential

- 1.2. Commercial

- 1.3. Industrial

- 1.4. Infrastructure (Transportation)

- 1.5. Energy and Utilities

Spain Construction Industry Segmentation By Geography

- 1. Spain

Spain Construction Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing demand for Housing; Increasing demand for transportation infrastructure

- 3.3. Market Restrains

- 3.3.1. High Cost of Labour; Rising material costs

- 3.4. Market Trends

- 3.4.1. Increase in housing construction drives the market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Spain Construction Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.1.3. Industrial

- 5.1.4. Infrastructure (Transportation)

- 5.1.5. Energy and Utilities

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 ELECNOR SA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 ACS ACTIVIDADES DE CONSTRUCCION Y SERVICIOS SA

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 ACCIONA CONSTRUCCION SA

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 TSK ELECTRONICA Y ELECTRICIDAD SA

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 COBRA INSTALACIONES Y SERVICIOS SA

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 ADIF ALTA VELOCIDAD

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 SACYR CONSTRUCCION SAU**List Not Exhaustive

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 FERROVIAL AGROMAN SA

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 DRAGADOS SOCIEDAD ANONIMA

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 OBRASCON HUARTE LAIN SA

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 ADMINISTRADOR DE INFRAESTRUCTURAS FERROVIARIAS

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 FCC CONSTRUCTION SA

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 ELECNOR SA

List of Figures

- Figure 1: Spain Construction Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Spain Construction Industry Share (%) by Company 2024

List of Tables

- Table 1: Spain Construction Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Spain Construction Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 3: Spain Construction Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Spain Construction Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Spain Construction Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 6: Spain Construction Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Construction Industry?

The projected CAGR is approximately 3.00%.

2. Which companies are prominent players in the Spain Construction Industry?

Key companies in the market include ELECNOR SA, ACS ACTIVIDADES DE CONSTRUCCION Y SERVICIOS SA, ACCIONA CONSTRUCCION SA, TSK ELECTRONICA Y ELECTRICIDAD SA, COBRA INSTALACIONES Y SERVICIOS SA, ADIF ALTA VELOCIDAD, SACYR CONSTRUCCION SAU**List Not Exhaustive, FERROVIAL AGROMAN SA, DRAGADOS SOCIEDAD ANONIMA, OBRASCON HUARTE LAIN SA, ADMINISTRADOR DE INFRAESTRUCTURAS FERROVIARIAS, FCC CONSTRUCTION SA.

3. What are the main segments of the Spain Construction Industry?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 192.55 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing demand for Housing; Increasing demand for transportation infrastructure.

6. What are the notable trends driving market growth?

Increase in housing construction drives the market.

7. Are there any restraints impacting market growth?

High Cost of Labour; Rising material costs.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Construction Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Construction Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Construction Industry?

To stay informed about further developments, trends, and reports in the Spain Construction Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence