Key Insights

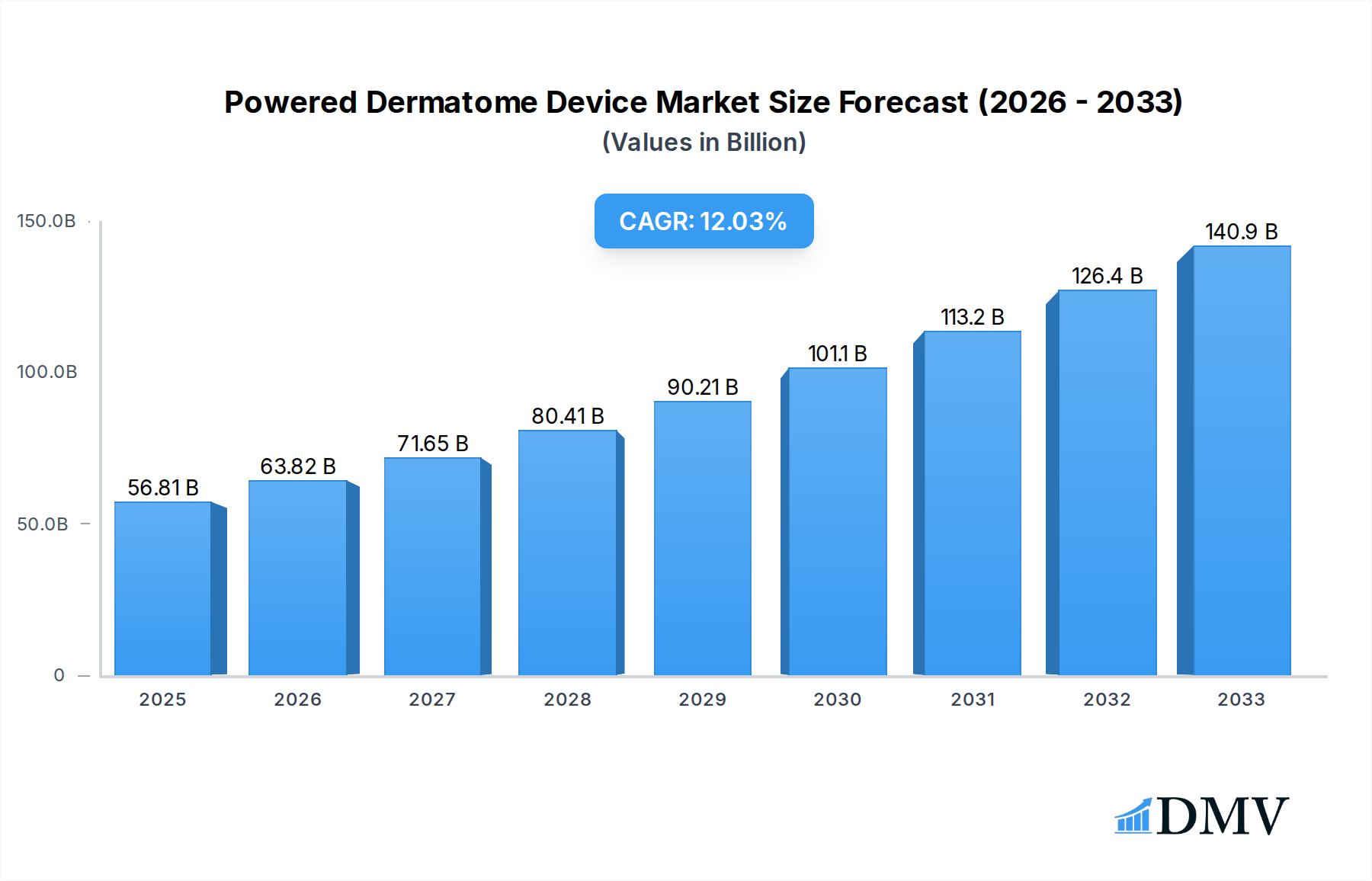

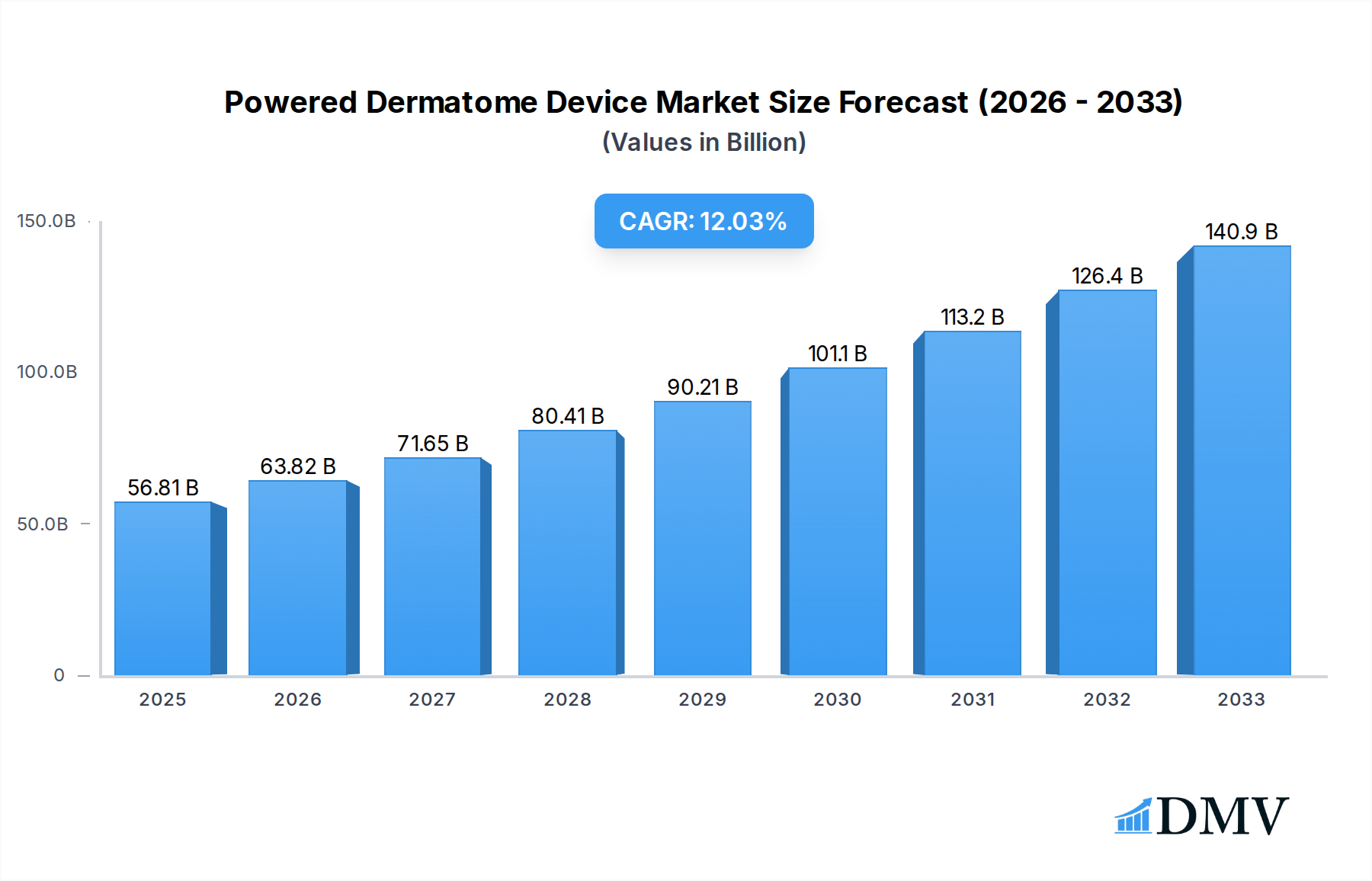

The global Powered Dermatome Device market is poised for significant expansion, projected to reach a substantial $56.81 billion by 2025, driven by a robust CAGR of 12.64% during the forecast period. This impressive growth is underpinned by several key factors. Advancements in surgical technology, leading to more precise and minimally invasive dermatological procedures, are a primary catalyst. The increasing prevalence of skin conditions requiring surgical intervention, such as skin cancer, burns, and reconstructive surgeries, further fuels demand. Furthermore, rising healthcare expenditure, particularly in developing economies, and a growing awareness of aesthetic procedures are contributing to the market's upward trajectory. The convenience and enhanced patient outcomes offered by powered dermatome devices, compared to manual alternatives, are also playing a crucial role in their wider adoption across various healthcare settings.

Powered Dermatome Device Market Size (In Billion)

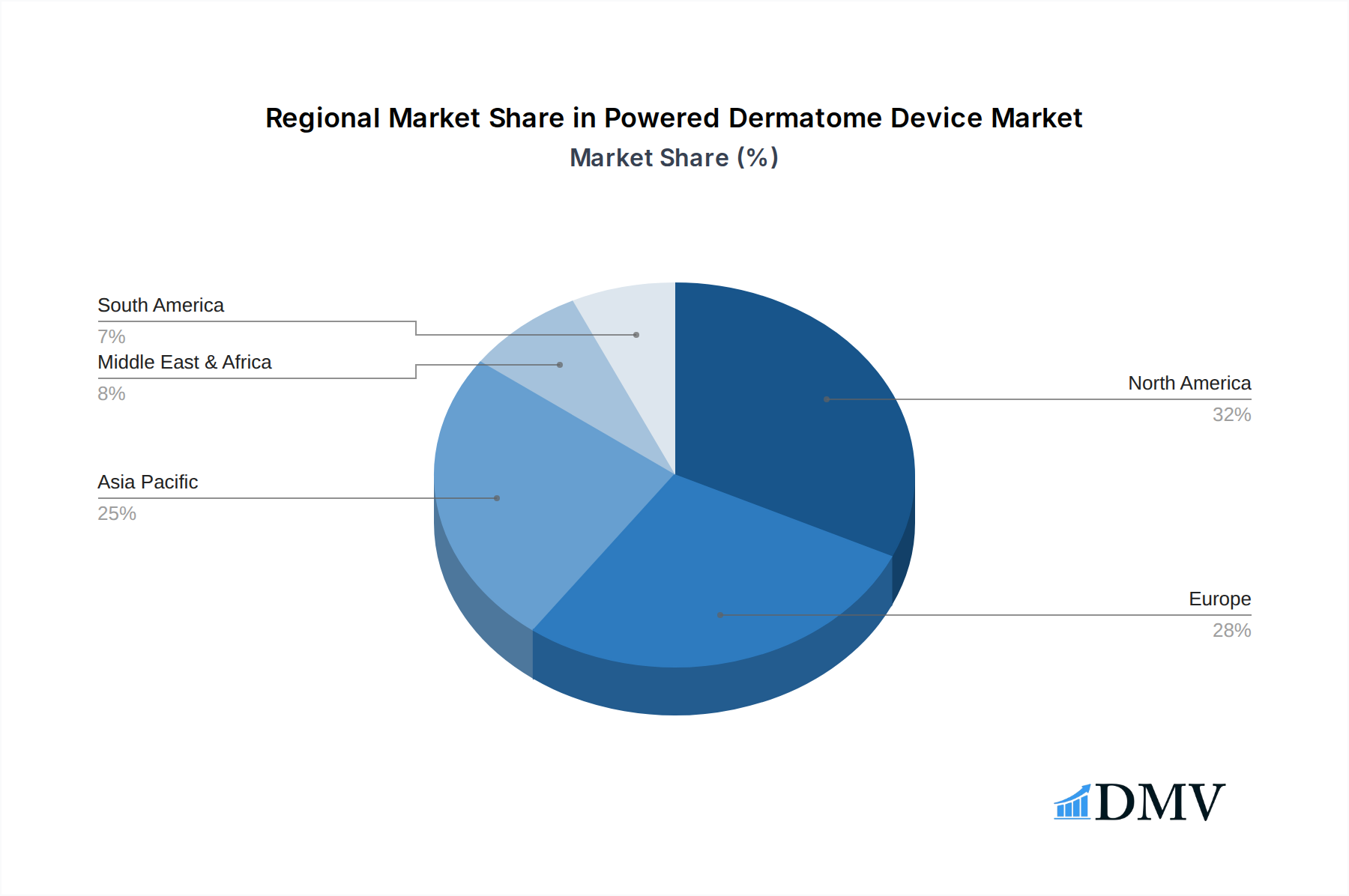

The market is segmented by application into Hospitals, Ambulatory Surgical Centers, and Dermatology Clinics, with Hospitals expected to hold a dominant share due to their comprehensive surgical capabilities. The "Others" segment, likely encompassing specialized wound care facilities and research institutions, is also anticipated to experience steady growth. By type, Pneumatic Dermatome Devices and Electric Dermatome Devices represent the core offerings. While electric devices offer greater power and control, pneumatic devices provide a lighter and more portable option, catering to diverse procedural needs. Geographically, North America and Europe currently lead the market, driven by advanced healthcare infrastructure and high adoption rates of new medical technologies. However, the Asia Pacific region is expected to witness the fastest growth, fueled by a burgeoning patient pool, increasing medical tourism, and government initiatives to enhance healthcare access and quality. Key players such as B. Braun, Zimmer Biomet, and Integra LifeSciences are actively engaged in product innovation and strategic collaborations to capture market share.

Powered Dermatome Device Company Market Share

Powered Dermatome Device Market Composition & Trends

The global powered dermatome device market is characterized by a moderate to high concentration, with a few key players like B. Braun, Zimmer Biomet, and De Soutter Medical holding significant market share. Innovation remains a crucial catalyst, driven by the demand for enhanced precision, reduced patient trauma, and improved workflow efficiency in dermatological and reconstructive surgeries. Regulatory landscapes, while generally supportive of medical device advancements, necessitate rigorous testing and adherence to quality standards. Substitute products, such as manual dermatomes and skin grafting alternatives, pose a degree of competition, though powered devices offer distinct advantages in terms of speed and consistency. End-user profiles range from large hospital networks to specialized dermatology clinics, each with varying purchasing power and technological adoption rates. Mergers and acquisitions (M&A) activities, with an estimated total deal value in the billions, continue to shape the market, allowing established players to expand their product portfolios and geographic reach.

- Market Share Distribution: Dominant players collectively hold an estimated 60% of the market share.

- M&A Deal Values: Recent M&A transactions have aggregated over $5 billion in value.

- Innovation Focus: Emphasis on cordless designs, improved blade technology, and integrated safety features.

- Regulatory Landscape: Strict adherence to FDA, CE Mark, and other regional medical device regulations.

- End-User Segments: Hospitals and ambulatory surgical centers represent the largest segments by volume, estimated at 65% of market demand.

Powered Dermatome Device Industry Evolution

The powered dermatome device industry has witnessed a dynamic evolution, marked by consistent market growth and transformative technological advancements throughout the historical period of 2019–2024 and projected to continue its upward trajectory through 2033. The base year of 2025 sets a crucial benchmark for understanding the current market landscape, with an estimated market size of $1.2 billion. This growth is underpinned by an increasing prevalence of skin conditions requiring surgical intervention, a rising number of elective reconstructive surgeries, and a growing demand for minimally invasive procedures. Technological innovation has been a key driver, with manufacturers continuously developing more sophisticated and user-friendly powered dermatomes. Early iterations focused on improving basic functionality, while recent advancements have introduced features such as variable cutting depths, ergonomic designs, and enhanced blade oscillation for precise tissue harvesting. The adoption of electric dermatome devices has surged, driven by their superior performance, ease of use, and reduced reliance on external power sources compared to pneumatic models. This shift is reflected in the market's segmentation, where electric devices are projected to capture a 70% market share by 2033. Consumer demand has also evolved, with healthcare providers and patients alike prioritizing devices that offer faster procedure times, improved patient outcomes, and quicker recovery periods. The increasing awareness of dermatological procedures and their benefits, coupled with a growing geriatric population susceptible to various skin ailments, further fuels market expansion. The forecast period of 2025–2033 anticipates a Compound Annual Growth Rate (CAGR) of 6.8%, indicating sustained and robust market expansion. This growth is not only attributed to technological leaps but also to the expanding application spectrum of powered dermatomes, extending beyond traditional reconstructive surgery to areas like burn care and cosmetic procedures. The industry's ability to adapt to evolving healthcare needs and integrate cutting-edge technologies will be paramount in maintaining this growth trajectory. The estimated market size for 2033 is projected to reach $2.1 billion.

Leading Regions, Countries, or Segments in Powered Dermatome Device

North America currently dominates the powered dermatome device market, with an estimated 35% market share in 2025, driven by a robust healthcare infrastructure, high healthcare expenditure, and a strong emphasis on adopting advanced medical technologies. The United States, in particular, is a leading contributor, owing to a high incidence of skin-related diseases, a substantial number of surgical procedures, and significant investments in medical research and development. Favorable reimbursement policies for dermatological surgeries and reconstructive procedures further bolster market growth in this region.

Application: Hospital holds the most significant share within the application segment, estimated at 55% of the total market demand. Hospitals, encompassing both general and specialized medical centers, are the primary sites for a vast array of dermatological and reconstructive surgeries. This segment's dominance is fueled by the availability of advanced surgical suites, a high volume of patient admissions for skin grafting, burn treatment, and other related procedures, and the presence of specialized medical professionals who utilize these devices regularly.

The Type: Electric Dermatome Device segment is experiencing the most rapid growth and is projected to capture a leading position, with an estimated 70% market share by 2033. Electric dermatomes offer superior precision, control, and ease of operation compared to their pneumatic counterparts. Their cordless nature enhances portability and reduces setup time, making them highly attractive in busy surgical environments. The continuous innovation in battery technology and motor efficiency further propels the adoption of electric dermatomes.

Key Drivers in North America:

- High Investment in Healthcare: Estimated annual investment in medical devices exceeds $50 billion.

- Technological Adoption: A high propensity to adopt cutting-edge medical technologies, with over 80% of major hospitals equipped with advanced surgical tools.

- Prevalence of Skin Conditions: Rising incidence of skin cancer and reconstructive surgery needs, leading to approximately 2 million skin grafting procedures annually.

- Regulatory Support: Streamlined approval processes for innovative medical devices.

Dominance Factors for Hospitals (Application):

- Procedure Volume: Hospitals perform an estimated 75% of all skin grafting and reconstructive surgeries.

- Infrastructure: Availability of comprehensive surgical facilities and post-operative care units.

- Specialized Personnel: Access to trained dermatologists, plastic surgeons, and surgical technicians.

Growth Trajectory for Electric Dermatome Devices (Type):

- Technological Superiority: Offering better control over skin graft thickness and consistency, estimated to improve graft success rates by 15%.

- Ergonomics and Ease of Use: Reducing surgeon fatigue and improving maneuverability, contributing to shorter procedure times.

- Portability and Wireless Functionality: Eliminating the need for air compressors and hoses, enhancing surgical flexibility.

Powered Dermatome Device Product Innovations

Recent product innovations in powered dermatome devices are revolutionizing surgical precision and patient outcomes. Manufacturers are increasingly focusing on developing ultra-lightweight and ergonomic designs for enhanced surgeon comfort during prolonged procedures. Advancements in battery technology are leading to longer operational times and faster charging capabilities, boosting efficiency in busy operating rooms. Furthermore, innovations in blade oscillation mechanisms and variable cutting depth controls allow for highly precise and consistent skin graft harvesting, minimizing tissue trauma and improving graft take rates. Some devices now incorporate integrated safety features to prevent accidental cuts. The average graft thickness accuracy achieved by leading models is now within 0.1 mm, significantly improving reconstructive surgery results.

Propelling Factors for Powered Dermatome Device Growth

Several factors are propelling the growth of the powered dermatome device market. The increasing global incidence of skin cancer, burns, and traumatic injuries necessitates sophisticated surgical solutions, driving demand for advanced skin grafting techniques. A growing aging population also contributes to the rise in dermatological conditions requiring surgical intervention. Furthermore, technological advancements in powered dermatomes, including enhanced precision, portability, and user-friendliness, are making them more attractive to healthcare providers. The expanding scope of applications, from reconstructive surgery to cosmetic procedures, further fuels market expansion. The estimated number of reconstructive surgeries globally is projected to exceed 10 million annually by 2030.

Obstacles in the Powered Dermatome Device Market

Despite the positive growth trajectory, the powered dermatome device market faces certain obstacles. High initial acquisition costs for sophisticated powered dermatome systems can be a barrier for smaller clinics and healthcare facilities with limited budgets. Stringent regulatory approval processes in various regions, while ensuring safety, can lead to prolonged market entry timelines for new products. Moreover, the availability of less expensive manual dermatomes and the ongoing development of alternative skin regeneration therapies pose a competitive threat. Supply chain disruptions and the need for specialized training for healthcare professionals can also hinder market penetration. The average cost of a high-end powered dermatome can range from $5,000 to $20,000.

Future Opportunities in Powered Dermatome Device

Emerging opportunities in the powered dermatome device market are abundant. The growing demand for minimally invasive surgical techniques presents a significant opportunity for the development of more compact and versatile powered dermatomes suitable for outpatient settings. The increasing adoption of telemedicine and remote surgical assistance could lead to the development of connected dermatome devices with enhanced data logging and remote diagnostics capabilities. Expansion into emerging economies with growing healthcare expenditures and increasing access to advanced medical treatments also offers substantial growth potential. Furthermore, the integration of artificial intelligence for real-time graft thickness monitoring and personalized surgical planning is an exciting area for future innovation.

Major Players in the Powered Dermatome Device Ecosystem

- B. Braun

- Zimmer Biomet

- De Soutter Medical

- Aygun Surgical Instruments

- G. R. Bioure Surgical System

- Humeca

- Integra LifeSciences

- Aesculap

- NOUVAG AG

- Surtex Instruments

- Shaanxi Xingmao Industry

- Exsurco Medical

- Intra Medical Systems

- Jiangsu MJD Medical Technology

Key Developments in Powered Dermatome Device Industry

- 2023 October: De Soutter Medical launches its new cordless electric dermatome, enhancing portability and surgeon flexibility.

- 2023 July: B. Braun announces a strategic partnership with a leading biotechnology firm to develop advanced skin graft material, potentially increasing demand for precise harvesting devices.

- 2022 December: Zimmer Biomet receives FDA clearance for its next-generation powered dermatome, featuring enhanced safety protocols and an improved ergonomic design.

- 2022 April: Integra LifeSciences expands its dermatological product portfolio through a significant acquisition of a smaller device manufacturer.

- 2021 November: Aygun Surgical Instruments introduces a cost-effective pneumatic dermatome model, targeting emerging markets with budget constraints.

Strategic Powered Dermatome Device Market Forecast

The strategic forecast for the powered dermatome device market indicates robust growth driven by technological innovation, increasing surgical procedure volumes, and expanding applications. Key growth catalysts include the ongoing development of more precise, portable, and user-friendly electric dermatome devices, coupled with the rising demand for minimally invasive procedures. The expansion of healthcare infrastructure in emerging economies and a growing emphasis on reconstructive and cosmetic surgery globally will further fuel market potential. The market is poised to witness significant advancements in smart dermatome technology, potentially integrating AI for enhanced surgical precision and data analysis, further solidifying its upward trajectory. The projected market value is expected to reach $2.1 billion by 2033.

Powered Dermatome Device Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Ambulatory Surgical Center

- 1.3. Dermatology Clinic

- 1.4. Others

-

2. Type

- 2.1. Pneumatic Dermatome Device

- 2.2. Electric Dermatome Device

Powered Dermatome Device Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Powered Dermatome Device Regional Market Share

Geographic Coverage of Powered Dermatome Device

Powered Dermatome Device REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.64% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Powered Dermatome Device Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Ambulatory Surgical Center

- 5.1.3. Dermatology Clinic

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Pneumatic Dermatome Device

- 5.2.2. Electric Dermatome Device

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Powered Dermatome Device Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Ambulatory Surgical Center

- 6.1.3. Dermatology Clinic

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Pneumatic Dermatome Device

- 6.2.2. Electric Dermatome Device

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Powered Dermatome Device Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Ambulatory Surgical Center

- 7.1.3. Dermatology Clinic

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Pneumatic Dermatome Device

- 7.2.2. Electric Dermatome Device

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Powered Dermatome Device Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Ambulatory Surgical Center

- 8.1.3. Dermatology Clinic

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Pneumatic Dermatome Device

- 8.2.2. Electric Dermatome Device

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Powered Dermatome Device Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Ambulatory Surgical Center

- 9.1.3. Dermatology Clinic

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Pneumatic Dermatome Device

- 9.2.2. Electric Dermatome Device

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Powered Dermatome Device Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Ambulatory Surgical Center

- 10.1.3. Dermatology Clinic

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Pneumatic Dermatome Device

- 10.2.2. Electric Dermatome Device

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 B. Braun

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Zimmer Biomet

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 De Soutter Medical

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Aygun Surgical Instruments

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 G. R. Bioure Surgical System

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Humeca

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Integra LifeSciences

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Aesculap

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 NOUVAG AG

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Surtex Instruments

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Shaanxi Xingmao Industry

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Exsurco Medical

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Intra Medical Systems

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Jiangsu MJD Medical Technology

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 B. Braun

List of Figures

- Figure 1: Global Powered Dermatome Device Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Powered Dermatome Device Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Powered Dermatome Device Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Powered Dermatome Device Volume (K), by Application 2025 & 2033

- Figure 5: North America Powered Dermatome Device Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Powered Dermatome Device Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Powered Dermatome Device Revenue (billion), by Type 2025 & 2033

- Figure 8: North America Powered Dermatome Device Volume (K), by Type 2025 & 2033

- Figure 9: North America Powered Dermatome Device Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Powered Dermatome Device Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Powered Dermatome Device Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Powered Dermatome Device Volume (K), by Country 2025 & 2033

- Figure 13: North America Powered Dermatome Device Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Powered Dermatome Device Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Powered Dermatome Device Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Powered Dermatome Device Volume (K), by Application 2025 & 2033

- Figure 17: South America Powered Dermatome Device Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Powered Dermatome Device Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Powered Dermatome Device Revenue (billion), by Type 2025 & 2033

- Figure 20: South America Powered Dermatome Device Volume (K), by Type 2025 & 2033

- Figure 21: South America Powered Dermatome Device Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Powered Dermatome Device Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Powered Dermatome Device Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Powered Dermatome Device Volume (K), by Country 2025 & 2033

- Figure 25: South America Powered Dermatome Device Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Powered Dermatome Device Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Powered Dermatome Device Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Powered Dermatome Device Volume (K), by Application 2025 & 2033

- Figure 29: Europe Powered Dermatome Device Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Powered Dermatome Device Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Powered Dermatome Device Revenue (billion), by Type 2025 & 2033

- Figure 32: Europe Powered Dermatome Device Volume (K), by Type 2025 & 2033

- Figure 33: Europe Powered Dermatome Device Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Powered Dermatome Device Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Powered Dermatome Device Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Powered Dermatome Device Volume (K), by Country 2025 & 2033

- Figure 37: Europe Powered Dermatome Device Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Powered Dermatome Device Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Powered Dermatome Device Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Powered Dermatome Device Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Powered Dermatome Device Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Powered Dermatome Device Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Powered Dermatome Device Revenue (billion), by Type 2025 & 2033

- Figure 44: Middle East & Africa Powered Dermatome Device Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Powered Dermatome Device Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Powered Dermatome Device Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Powered Dermatome Device Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Powered Dermatome Device Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Powered Dermatome Device Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Powered Dermatome Device Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Powered Dermatome Device Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Powered Dermatome Device Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Powered Dermatome Device Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Powered Dermatome Device Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Powered Dermatome Device Revenue (billion), by Type 2025 & 2033

- Figure 56: Asia Pacific Powered Dermatome Device Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Powered Dermatome Device Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Powered Dermatome Device Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Powered Dermatome Device Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Powered Dermatome Device Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Powered Dermatome Device Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Powered Dermatome Device Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Powered Dermatome Device Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Powered Dermatome Device Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Powered Dermatome Device Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global Powered Dermatome Device Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Powered Dermatome Device Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Powered Dermatome Device Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Powered Dermatome Device Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Powered Dermatome Device Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Powered Dermatome Device Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Powered Dermatome Device Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Powered Dermatome Device Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Powered Dermatome Device Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Powered Dermatome Device Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Powered Dermatome Device Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Powered Dermatome Device Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Powered Dermatome Device Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Powered Dermatome Device Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Powered Dermatome Device Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Powered Dermatome Device Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Powered Dermatome Device Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Powered Dermatome Device Revenue billion Forecast, by Type 2020 & 2033

- Table 34: Global Powered Dermatome Device Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Powered Dermatome Device Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Powered Dermatome Device Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Powered Dermatome Device Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Powered Dermatome Device Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Powered Dermatome Device Revenue billion Forecast, by Type 2020 & 2033

- Table 58: Global Powered Dermatome Device Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Powered Dermatome Device Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Powered Dermatome Device Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Powered Dermatome Device Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Powered Dermatome Device Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Powered Dermatome Device Revenue billion Forecast, by Type 2020 & 2033

- Table 76: Global Powered Dermatome Device Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Powered Dermatome Device Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Powered Dermatome Device Volume K Forecast, by Country 2020 & 2033

- Table 79: China Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Powered Dermatome Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Powered Dermatome Device Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Powered Dermatome Device?

The projected CAGR is approximately 12.64%.

2. Which companies are prominent players in the Powered Dermatome Device?

Key companies in the market include B. Braun, Zimmer Biomet, De Soutter Medical, Aygun Surgical Instruments, G. R. Bioure Surgical System, Humeca, Integra LifeSciences, Aesculap, NOUVAG AG, Surtex Instruments, Shaanxi Xingmao Industry, Exsurco Medical, Intra Medical Systems, Jiangsu MJD Medical Technology.

3. What are the main segments of the Powered Dermatome Device?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 56.81 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Powered Dermatome Device," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Powered Dermatome Device report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Powered Dermatome Device?

To stay informed about further developments, trends, and reports in the Powered Dermatome Device, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence