Key Insights

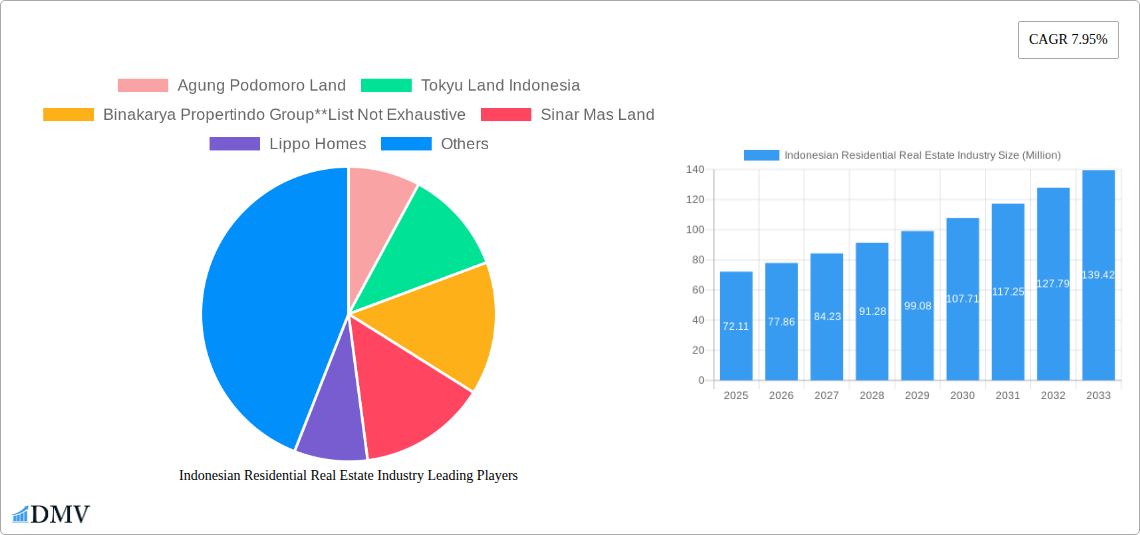

The Indonesian residential real estate market, valued at $72.11 million in 2025, exhibits robust growth potential, projected to expand at a Compound Annual Growth Rate (CAGR) of 7.95% from 2025 to 2033. This growth is driven by several key factors. A burgeoning middle class with increasing disposable income fuels demand for housing across various segments, from affordable apartments and condominiums to luxury villas and landed properties. Urbanization, particularly in major cities like Jakarta, Surabaya, and Semarang, further intensifies this demand, as populations migrate from rural areas seeking better employment opportunities and improved living standards. Government initiatives promoting affordable housing and infrastructure development also contribute positively to market expansion. However, challenges exist. Rising construction costs and fluctuating interest rates could impact affordability and potentially restrain growth. Furthermore, regulatory hurdles and land acquisition complexities can impede project timelines and overall market expansion. The market is segmented by property type (condominiums & apartments, villas & landed houses) and key cities, reflecting varying demand levels and price points across different regions. Leading developers like Agung Podomoro Land, Tokyu Land Indonesia, and Sinar Mas Land are key players shaping the market landscape through their diverse project portfolios and innovative approaches.

The forecast period (2025-2033) anticipates continued market expansion, albeit with potential fluctuations influenced by macroeconomic conditions. The high CAGR suggests a consistently expanding market. The concentration of development in major cities suggests opportunities for developers targeting specific demographics and needs within these urban centers. Understanding the interplay of these driving forces, trends, and restraints is crucial for investors and developers navigating this dynamic market. Strategic planning that accounts for economic shifts and regulatory changes will be critical for success in the Indonesian residential real estate sector over the next decade. The significant growth potential, however, remains attractive for those who can effectively manage risk and capitalize on emerging opportunities.

Indonesian Residential Real Estate Industry: A Comprehensive Market Report (2019-2033)

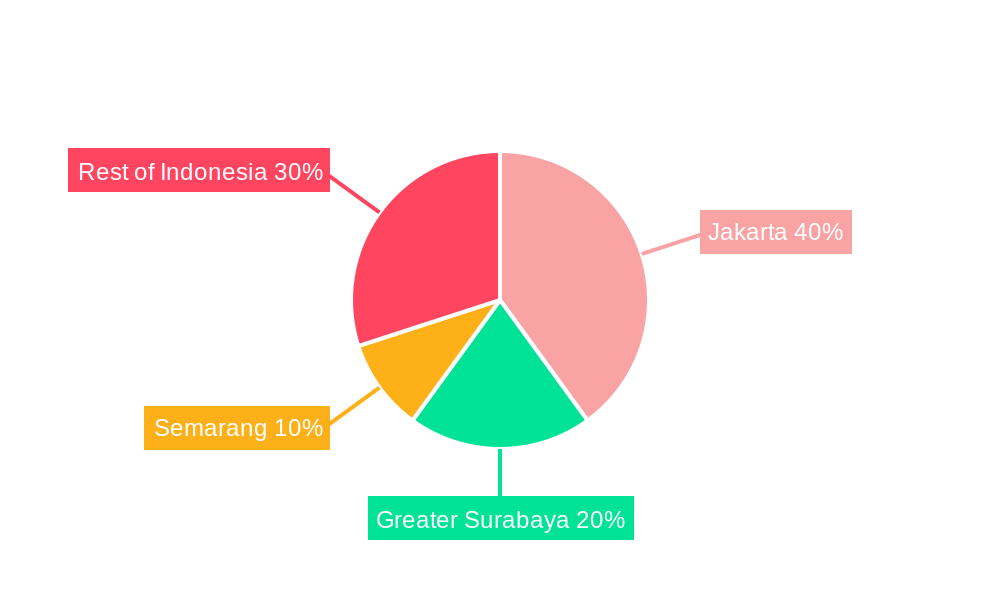

This insightful report provides a detailed analysis of the Indonesian residential real estate market, offering a comprehensive overview of its current state, future trajectory, and key players. With a focus on the period 2019-2033, including a base year of 2025 and a forecast period of 2025-2033, this report is an essential resource for stakeholders seeking to understand and capitalize on opportunities within this dynamic sector. The report analyzes key segments including condominiums and apartments, villas and landed houses, across major cities like Jakarta, Greater Surabaya, Semarang, and the rest of Indonesia. The market's value is projected to reach xx Million by 2033.

Indonesian Residential Real Estate Industry Market Composition & Trends

This section delves into the current market structure of the Indonesian residential real estate industry, evaluating market concentration, innovation catalysts, regulatory landscapes, substitute products, end-user profiles, and M&A activities. We analyze the market share distribution among key players like Agung Podomoro Land, Tokyu Land Indonesia, Binakarya Propertindo Group, Sinar Mas Land, Lippo Homes, JABABEKA, PT Pakuwon Jati, Ciputra Group, PP Properti, and Duta Anggada Realty (list not exhaustive).

Market Concentration: The Indonesian residential real estate market exhibits a moderately concentrated structure, with a few large players holding significant market share. However, a fragmented landscape exists among smaller developers. The top five players collectively hold an estimated xx% market share in 2025.

Innovation Catalysts: Growing urbanization, rising disposable incomes, and government initiatives promoting affordable housing are driving innovation.

Regulatory Landscape: Government policies and regulations significantly influence market dynamics. Changes in building codes, land acquisition processes, and financing regulations impact development timelines and costs.

Substitute Products: The primary substitute for residential properties is renting. However, the increasing preference for homeownership drives market growth.

End-User Profiles: The market caters to a diverse range of end-users, from first-time homebuyers to high-net-worth individuals seeking luxury properties.

M&A Activities: The Indonesian residential real estate sector has witnessed notable M&A activities in recent years, with deal values totaling xx Million in 2024. These mergers and acquisitions have led to increased market consolidation.

Indonesian Residential Real Estate Industry Industry Evolution

This section analyzes the evolution of the Indonesian residential real estate industry, highlighting market growth trajectories, technological advancements, and shifting consumer demands from 2019 to 2033.

The Indonesian residential real estate market experienced significant growth during the historical period (2019-2024), driven by strong economic growth and increasing urbanization. However, the market faced challenges during the pandemic, resulting in a slowdown. The market is anticipated to recover and show robust growth in the forecast period (2025-2033), reaching an estimated xx Million by 2033. Technological advancements, such as the adoption of Building Information Modeling (BIM) and PropTech solutions, are enhancing efficiency and transparency. Consumer preferences are shifting towards sustainable and smart homes, impacting design and construction practices. Growth rates during the historical period averaged approximately xx% annually, with a projected annual growth rate of xx% during the forecast period. Adoption of PropTech solutions, such as online property portals and virtual tours, is estimated to reach xx% by 2033.

Leading Regions, Countries, or Segments in Indonesian Residential Real Estate Industry

This section identifies the dominant regions and segments within the Indonesian residential real estate market.

By Type: Condominiums and apartments are currently the leading segment, driven by high demand in urban centers. However, villas and landed houses remain popular in suburban and rural areas. The condominium and apartment segment is projected to maintain its dominance, with a market share of xx% in 2033.

By Key Cities: Jakarta remains the leading market, followed by Greater Surabaya and Semarang. The rest of Indonesia also shows promising growth potential. Key drivers for Jakarta's dominance include its economic significance, high population density, and robust infrastructure. The Greater Surabaya market is driven by strong industrial and commercial growth, while Semarang benefits from its strategic location and expanding infrastructure.

Indonesian Residential Real Estate Industry Product Innovations

The Indonesian residential real estate market is witnessing a surge in product innovation, with a focus on sustainable, smart, and affordable housing solutions. Developers are incorporating green building materials, implementing energy-efficient technologies, and integrating smart home automation systems. Unique selling propositions include features like rooftop gardens, communal spaces, and co-working areas to enhance the living experience. The adoption of prefabricated construction methods is also gaining traction, reducing construction times and costs.

Propelling Factors for Indonesian Residential Real Estate Industry Growth

Several factors drive the growth of the Indonesian residential real estate market. Government initiatives promoting affordable housing schemes and infrastructure development significantly contribute to market expansion. The burgeoning middle class and rising disposable incomes fuel demand for better housing. Technological advancements, such as the use of BIM and PropTech, enhance efficiency and transparency.

Obstacles in the Indonesian Residential Real Estate Industry Market

Despite its growth potential, the Indonesian residential real estate market faces several challenges. Land acquisition complexities and bureaucratic procedures pose significant hurdles. Fluctuations in the economy and interest rates impact consumer purchasing power. Competition among developers is intense, creating price pressures. Supply chain disruptions and material cost increases impact project timelines and profitability.

Future Opportunities in Indonesian Residential Real Estate Industry

The Indonesian residential real estate market presents numerous opportunities. The expanding middle class and increasing urbanization fuel demand for affordable and sustainable housing. The growing adoption of smart home technologies offers opportunities for innovation and differentiation. Government initiatives focused on infrastructure development open up new markets in previously underserved areas. Demand for eco-friendly and sustainable housing is also expected to rise.

Major Players in the Indonesian Residential Real Estate Industry Ecosystem

- Agung Podomoro Land

- Tokyu Land Indonesia

- Binakarya Propertindo Group

- Sinar Mas Land

- Lippo Homes

- JABABEKA

- PT Pakuwon Jati

- Ciputra Group

- PP Properti

- Duta Anggada Realty

Key Developments in Indonesian Residential Real Estate Industry Industry

- 2021 Q3: Government launches new affordable housing scheme.

- 2022 Q1: Major developer announces strategic partnership to expand into new markets.

- 2023 Q2: New building codes implemented, impacting construction practices.

- 2024 Q4: Significant M&A deal between two prominent developers. (Further details to be added in the full report)

Strategic Indonesian Residential Real Estate Industry Market Forecast

The Indonesian residential real estate market is poised for significant growth in the coming years. Continued urbanization, a growing middle class, and supportive government policies will drive demand. The adoption of innovative technologies and sustainable building practices will shape market dynamics. The market is projected to experience healthy growth, offering attractive investment opportunities. However, challenges related to land acquisition, infrastructure development, and regulatory compliance need to be addressed to ensure sustained growth.

Indonesian Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Condominiums and Apartments

- 1.2. Villas and landed houses

-

2. Key Cities

- 2.1. Jakarta

- 2.2. Greater Surabaya

- 2.3. Semarang

- 2.4. Rest of Indonesia

Indonesian Residential Real Estate Industry Segmentation By Geography

- 1. Indonesia

Indonesian Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.95% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Investment in Infrastructure Projects; The rising popularity of sustainable architecture

- 3.3. Market Restrains

- 3.3.1. Volatility in Raw material prices

- 3.4. Market Trends

- 3.4.1. Jakarta Emerging as a Prime Rental Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Indonesian Residential Real Estate Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Condominiums and Apartments

- 5.1.2. Villas and landed houses

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Jakarta

- 5.2.2. Greater Surabaya

- 5.2.3. Semarang

- 5.2.4. Rest of Indonesia

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Indonesia

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Agung Podomoro Land

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Tokyu Land Indonesia

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Binakarya Propertindo Group**List Not Exhaustive

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Sinar Mas Land

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Lippo Homes

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 JABABEKA

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 PT Pakuwon Jati

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Ciputra Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 PP Properti

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Duta Anggada Realty

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Agung Podomoro Land

List of Figures

- Figure 1: Indonesian Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Indonesian Residential Real Estate Industry Share (%) by Company 2024

List of Tables

- Table 1: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2019 & 2032

- Table 4: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 7: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2019 & 2032

- Table 8: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indonesian Residential Real Estate Industry?

The projected CAGR is approximately 7.95%.

2. Which companies are prominent players in the Indonesian Residential Real Estate Industry?

Key companies in the market include Agung Podomoro Land, Tokyu Land Indonesia, Binakarya Propertindo Group**List Not Exhaustive, Sinar Mas Land, Lippo Homes, JABABEKA, PT Pakuwon Jati, Ciputra Group, PP Properti, Duta Anggada Realty.

3. What are the main segments of the Indonesian Residential Real Estate Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 72.11 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Investment in Infrastructure Projects; The rising popularity of sustainable architecture.

6. What are the notable trends driving market growth?

Jakarta Emerging as a Prime Rental Market.

7. Are there any restraints impacting market growth?

Volatility in Raw material prices.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indonesian Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indonesian Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indonesian Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Indonesian Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence