Key Insights

The French agricultural tractor market, valued at approximately €[Estimate based on market size XX and value unit Million – a reasonable estimate might be €800 million] in 2025, exhibits a steady growth trajectory, projected to achieve a compound annual growth rate (CAGR) of 3.20% from 2025 to 2033. This growth is primarily driven by several factors. Firstly, the increasing demand for efficient and high-performance machinery to address labor shortages and optimize farm productivity is a key catalyst. Secondly, government initiatives promoting sustainable agricultural practices and technological advancements, such as precision farming techniques and automation, are boosting market adoption of modern tractors. The segment encompassing tractors with horsepower exceeding 120 HP is anticipated to witness significant growth, reflecting a trend toward larger-scale farming operations and increased mechanization. However, factors such as fluctuating fuel prices and the overall economic climate could pose potential restraints on market expansion. Key players like John Deere, Kubota, and CNH Industrial are actively competing within this market, focusing on innovation and technological enhancements to meet the evolving needs of French farmers.

The segmentation within the French agricultural tractor market showcases varied growth prospects. Tractors in the 50-79 HP and 80-99 HP categories are likely to maintain a substantial market share due to their versatility and suitability for a wide range of farming activities. Competition is fierce, with established international players and regional manufacturers vying for market dominance. The market’s success is intrinsically linked to the broader agricultural economy's performance, with factors like crop yields and pricing influencing demand. Therefore, future projections will require continuous monitoring of both agricultural and economic indicators to maintain accuracy. The integration of smart technologies, including GPS-guided systems and telematics, promises to significantly influence the trajectory of the market in the coming years, driving further efficiency and precision in agricultural operations.

France Agricultural Tractors Industry: A Comprehensive Market Report (2019-2033)

This insightful report provides a detailed analysis of the France agricultural tractors industry, offering a comprehensive overview of market dynamics, key players, technological advancements, and future growth prospects. The study period covers 2019-2033, with 2025 as the base and estimated year. This report is invaluable for stakeholders seeking to understand and capitalize on opportunities within this dynamic sector. The market size is estimated at xx Million in 2025 and is projected to reach xx Million by 2033.

France Agricultural Tractors Industry Market Composition & Trends

The French agricultural tractors market exhibits a moderately concentrated structure, with key players like John Deere SAS, Kubota Europe SAS, and CLAAS Group holding significant market share. The exact distribution is xx% for John Deere, xx% for Kubota, and xx% for CLAAS as of 2025. Innovation is driven by increasing demand for fuel-efficient and technologically advanced tractors, precision farming techniques, and government initiatives promoting sustainable agriculture. Stringent environmental regulations are shaping the industry, favoring manufacturers that prioritize reduced emissions and efficient resource management. Substitute products, such as drones for spraying and automated harvesting systems, present a competitive landscape, while the rise of precision agriculture is driving demand for advanced machinery. The market is also witnessing a rise in M&A activities, with deal values reaching xx Million in the past five years, reflecting consolidation and the expansion of existing players. End-user profiles include large-scale farms, small-to-medium-sized holdings, and agricultural cooperatives.

- Market Concentration: Moderately concentrated, with top three players holding xx% market share.

- Innovation Catalysts: Precision agriculture, fuel efficiency, emission regulations, sustainable farming.

- Regulatory Landscape: Stringent environmental regulations driving adoption of sustainable technologies.

- Substitute Products: Drones, automated harvesting systems.

- End-User Profiles: Large-scale farms, small-to-medium-sized farms, agricultural cooperatives.

- M&A Activities: Significant activity with total deal value of xx Million (2020-2025).

France Agricultural Tractors Industry Industry Evolution

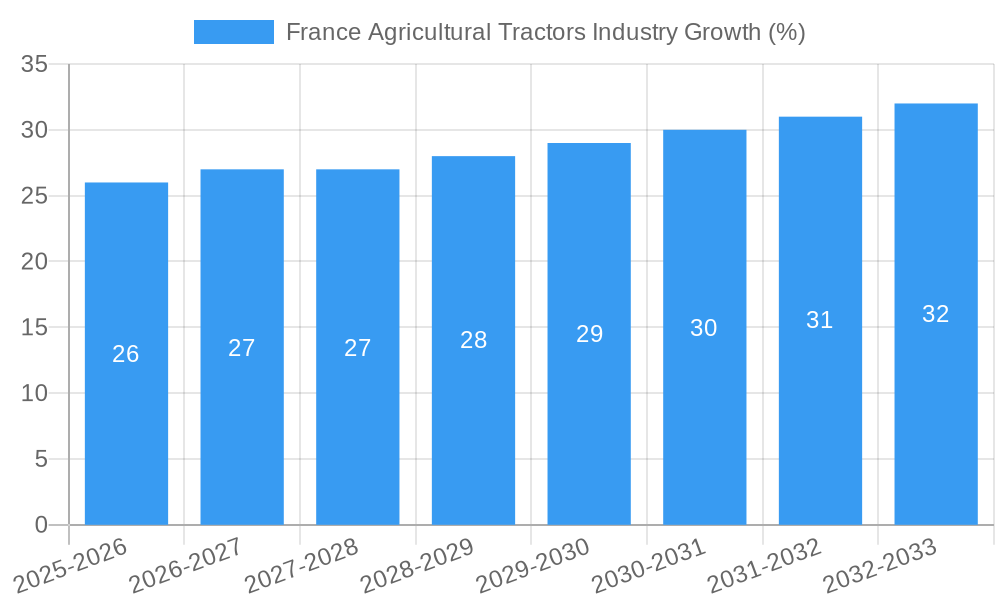

The French agricultural tractors market demonstrated robust growth from 2019 to 2024, exhibiting a [Insert Precise Growth Percentage]% expansion. This surge is significantly attributed to the integration of advanced technologies, including GPS-guided tractors, automated steering systems, and comprehensive telematics solutions. These technological advancements have dramatically enhanced operational efficiency and overall productivity within the agricultural sector. The increasing demand for higher precision farming, improved fuel economy, and reduced labor costs are key drivers fueling this growth. Precision farming technologies are experiencing a rapid adoption rate, with an estimated [Insert Precise Percentage]% of farms utilizing GPS-guided systems by 2025. Furthermore, evolving consumer preferences towards sustainable and environmentally conscious farming practices are significantly shaping market dynamics. Farmers are increasingly adopting environmentally friendly methods, creating a strong preference for tractors with lower emissions and optimized fuel consumption. This trend, coupled with government incentives aimed at promoting sustainable farming practices, is projected to further accelerate market expansion in the forecast period (2025-2033). This period is anticipated to witness a notable focus on autonomous machinery and data-driven decision-making processes within the farming sector. We project a compound annual growth rate (CAGR) of [Insert Precise CAGR Percentage]% for the period 2025-2033.

Leading Regions, Countries, or Segments in France Agricultural Tractors Industry

Within the French agricultural tractor market, the most dominant segments are Tractors (especially those in the 50-79 HP and 80-99 HP ranges), Harvesting Machinery (including Combine Harvesters and Forage Harvesters), and Plowing and Cultivating Machinery (such as Plows and Harrows). These segments exhibit particularly strong performance due to their wide-ranging applicability across various farm sizes and operational needs.

- Tractors: The high demand for tractors within the 50-79 HP and 80-99 HP segments reflects their suitability for a diverse range of farm sizes and operational requirements, making them versatile and indispensable assets for many agricultural operations.

- Harvesting Machinery: Combine Harvesters and Forage Harvesters are indispensable for efficient and timely crop harvesting, resulting in consistently high demand for these essential pieces of equipment.

- Plowing & Cultivating Machinery: Plows and harrows remain fundamental for effective soil preparation, ensuring consistent demand driven by the ongoing need for optimal soil conditions for successful crop cultivation.

Key Drivers:

- Substantial investment in agricultural modernization: Government subsidies and dedicated farm modernization initiatives are acting as powerful catalysts, driving the demand for advanced and technologically sophisticated agricultural equipment.

- Widespread adoption of precision farming techniques: The increasing adoption of precision farming methodologies is consistently fueling demand for high-precision machinery and related technologies.

- Emphasis on sustainable agriculture: Stringent environmental regulations and the growing consumer preference for sustainably produced food are encouraging the adoption of fuel-efficient and eco-friendly tractors, promoting environmentally responsible farming practices.

France Agricultural Tractors Industry Product Innovations

Recent innovations include the introduction of fuel-efficient tractors like the John Deere 6R 185 and KUHN SAS’s 12m Optimer minimum tillage stubble cultivator with Steady Control, enhancing efficiency and precision. These advancements highlight a focus on improved fuel economy, enhanced operational efficiency, and more sustainable farming practices. The unique selling propositions revolve around increased output, reduced operational costs and environmental impact.

Propelling Factors for France Agricultural Tractors Industry Growth

Technological advancements, such as automated guidance systems and telematics, are driving efficiency gains. Government support for sustainable agriculture through subsidies and incentives is also significant. Economic factors, like rising food prices and increasing demand for agricultural products, are also fueling the growth of the sector.

Obstacles in the France Agricultural Tractors Industry Market

The high initial investment costs associated with advanced machinery can present a significant barrier to adoption for smaller farms, potentially limiting their access to these productivity-enhancing technologies. Furthermore, supply chain disruptions stemming from global events can lead to delays in equipment delivery and contribute to increased costs, impacting profitability. The presence of intense competition from both domestic and international players creates considerable pressure on profit margins, demanding efficient operational strategies and innovative product offerings.

Future Opportunities in France Agricultural Tractors Industry

The integration of Artificial Intelligence (AI) and Internet of Things (IoT) technologies presents substantial opportunities for enhanced automation and data-driven decision-making, optimizing resource allocation and operational efficiency. Precision agriculture continues to be a critical area of focus, driving ongoing demand for specialized equipment and associated services. The expansion into sustainable and organic farming presents a significant avenue for growth in the market for specialized machinery designed to meet the unique needs of these environmentally focused agricultural practices.

Major Players in the France Agricultural Tractors Industry Ecosystem

- Kuhn Group

- CNH Industrial Osterreich GmbH

- Netafim Ltd

- Artec Pulverisation (Kuhn Group)

- AGCO Distribution SAS

- CLAAS Group

- Yanmar Co Ltd

- Same Deutz-Fahr France

- Kubota Europe SAS

- John Deere SAS

- Lely France

Key Developments in France Agricultural Tractors Industry Industry

- February 2022: John Deere launched the new 6R 185 tractors, emphasizing fuel efficiency.

- March 2022: KUHN SAS announced a new 12m Optimer minimum tillage stubble cultivator.

- November 2022: AGCO launched the Geo-Bird operational planning tool for farmers in Western Europe, including France.

Strategic France Agricultural Tractors Industry Market Forecast

The French agricultural tractor market is poised for sustained growth driven by technological innovation, government support, and rising demand for efficient and sustainable agricultural practices. The market is expected to benefit from the increasing adoption of precision farming techniques and the ongoing development of autonomous machinery. The forecast period should see a continued trend toward greater efficiency and sustainability within the sector.

France Agricultural Tractors Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

France Agricultural Tractors Industry Segmentation By Geography

- 1. France

France Agricultural Tractors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.20% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Shortage of Skilled Labor; Government Support to Enhance Farm Mechanization

- 3.3. Market Restrains

- 3.3.1. Heavy Initial Procurement Cost and High Expenditure on Maintenance

- 3.4. Market Trends

- 3.4.1. Large-scale Agricultural Production is Driving Mechanization

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. France Agricultural Tractors Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. France

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Kuhn Group

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 CNH Industrial Osterreich GmbH

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Netafim Lt

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Artec Pulverisation (Kuhn Group)

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 AGCO DistributionSAS

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 CLAAS Group

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Yanmar Co Ltd

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Same Deutz-Fahr France

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Kubota Europe SAS

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 John Deere SAS

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Lely France

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.1 Kuhn Group

List of Figures

- Figure 1: France Agricultural Tractors Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: France Agricultural Tractors Industry Share (%) by Company 2024

List of Tables

- Table 1: France Agricultural Tractors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: France Agricultural Tractors Industry Revenue Million Forecast, by Production Analysis 2019 & 2032

- Table 3: France Agricultural Tractors Industry Revenue Million Forecast, by Consumption Analysis 2019 & 2032

- Table 4: France Agricultural Tractors Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2019 & 2032

- Table 5: France Agricultural Tractors Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2019 & 2032

- Table 6: France Agricultural Tractors Industry Revenue Million Forecast, by Price Trend Analysis 2019 & 2032

- Table 7: France Agricultural Tractors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: France Agricultural Tractors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: France Agricultural Tractors Industry Revenue Million Forecast, by Production Analysis 2019 & 2032

- Table 10: France Agricultural Tractors Industry Revenue Million Forecast, by Consumption Analysis 2019 & 2032

- Table 11: France Agricultural Tractors Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2019 & 2032

- Table 12: France Agricultural Tractors Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2019 & 2032

- Table 13: France Agricultural Tractors Industry Revenue Million Forecast, by Price Trend Analysis 2019 & 2032

- Table 14: France Agricultural Tractors Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the France Agricultural Tractors Industry?

The projected CAGR is approximately 3.20%.

2. Which companies are prominent players in the France Agricultural Tractors Industry?

Key companies in the market include Kuhn Group, CNH Industrial Osterreich GmbH, Netafim Lt, Artec Pulverisation (Kuhn Group), AGCO DistributionSAS, CLAAS Group, Yanmar Co Ltd, Same Deutz-Fahr France, Kubota Europe SAS, John Deere SAS, Lely France.

3. What are the main segments of the France Agricultural Tractors Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Shortage of Skilled Labor; Government Support to Enhance Farm Mechanization.

6. What are the notable trends driving market growth?

Large-scale Agricultural Production is Driving Mechanization.

7. Are there any restraints impacting market growth?

Heavy Initial Procurement Cost and High Expenditure on Maintenance.

8. Can you provide examples of recent developments in the market?

November 2022: AGCO Launched a online Free Operational Planning Tool called Geo-Bird for Farmers in Western Europe. In France, this has launched on the Valtra Stand in Paris.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "France Agricultural Tractors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the France Agricultural Tractors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the France Agricultural Tractors Industry?

To stay informed about further developments, trends, and reports in the France Agricultural Tractors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence