Key Insights

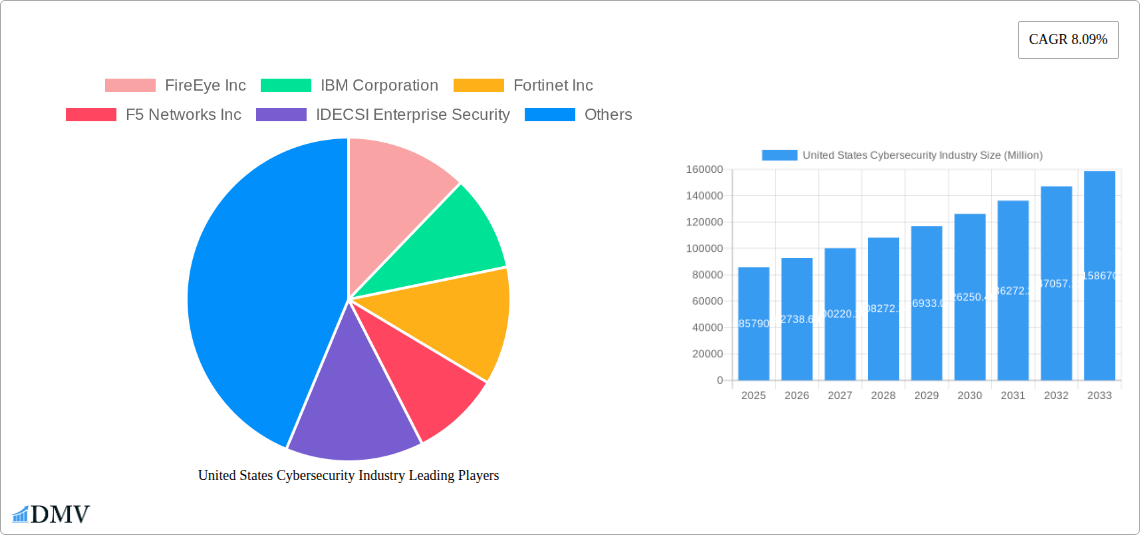

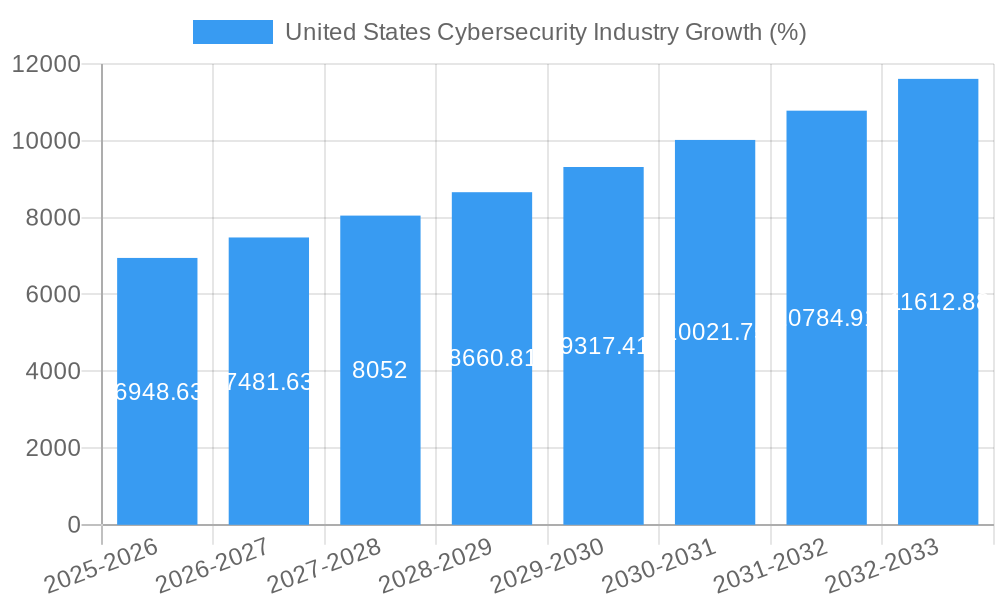

The United States cybersecurity market, a significant segment of the global landscape, is experiencing robust growth, fueled by increasing digitalization, the expanding attack surface from remote work and IoT devices, and stringent government regulations mandating stronger cybersecurity postures. The market, valued at approximately $85.79 billion in 2025, is projected to maintain a Compound Annual Growth Rate (CAGR) of 8.09% from 2025 to 2033. This growth is driven by several key factors. The increasing sophistication and frequency of cyberattacks targeting critical infrastructure, financial institutions (BFSI), healthcare providers, and government entities are compelling organizations to invest heavily in robust security solutions. Furthermore, the shift towards cloud-based deployments and the adoption of advanced security technologies like artificial intelligence (AI) and machine learning (ML) for threat detection and response are accelerating market expansion. Key segments within the US market include cloud-based security solutions, which are experiencing the fastest growth due to their scalability and flexibility, and on-premise solutions, which continue to hold a substantial share, particularly among enterprises with stringent data residency requirements. Major players such as FireEye, IBM, Fortinet, and Cisco are actively competing through innovation and strategic acquisitions, further shaping the market dynamics.

The market's growth is not without its challenges. The skills gap in cybersecurity professionals remains a significant restraint, hindering the effective implementation and management of security solutions. Furthermore, the constantly evolving threat landscape necessitates continuous investment in upgrading security infrastructure and training personnel, posing a considerable financial burden for organizations, particularly small and medium-sized enterprises (SMEs). Despite these challenges, the long-term outlook for the US cybersecurity market remains positive, driven by the unwavering need to protect sensitive data and critical infrastructure from escalating cyber threats. The market segmentation across various end-user industries (BFSI, Healthcare, Manufacturing, Government & Defense, IT & Telecommunication) reflects the diverse needs and vulnerabilities across different sectors, highlighting the broad applicability and continued relevance of robust cybersecurity solutions.

United States Cybersecurity Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the United States cybersecurity industry, encompassing market size, trends, leading players, and future forecasts. From 2019 to 2033, the industry witnessed significant transformation, driven by technological advancements, evolving cyber threats, and increasing regulatory scrutiny. This report offers invaluable insights for stakeholders, including investors, businesses, and policymakers, navigating this dynamic landscape. The study period covers 2019-2033, with 2025 as the base and estimated year. The forecast period spans 2025-2033, and the historical period covers 2019-2024. Market values are expressed in Millions of USD.

United States Cybersecurity Industry Market Composition & Trends

The US cybersecurity market is highly fragmented, yet experiencing significant consolidation through mergers and acquisitions (M&A). Major players like FireEye Inc, IBM Corporation, Fortinet Inc, F5 Networks Inc, IDECSI Enterprise Security, Cisco Systems Inc, AVG Technologies, Intel Security (Intel Corporation), Dell Technologies Inc, and Cyberark Software Ltd compete across various segments, resulting in a dynamic market share distribution. While precise market share figures for each company vary year to year, the market is characterized by a combination of large established players and smaller, specialized firms.

- Market Concentration: Moderately fragmented, with a few dominant players and many niche players.

- Innovation Catalysts: Rising cyber threats, increasing adoption of cloud technologies, and stringent data privacy regulations.

- Regulatory Landscape: Subject to evolving federal and state regulations (e.g., CCPA, GDPR implications), driving investment in compliance solutions.

- Substitute Products: Limited viable substitutes exist, given the critical nature of cybersecurity.

- End-User Profiles: BFSI, healthcare, manufacturing, government & defense, IT & telecommunication, and other end-users all represent significant market segments with varying needs.

- M&A Activities: Significant M&A activity characterized by large acquisitions, such as Google's acquisition of Mandiant for USD 5.4 Billion (March 2022) and HelpSystems' acquisition of AlertLogic (March 2022) - reflecting industry consolidation and the increasing strategic importance of cybersecurity. Total M&A deal value in 2024 estimated at xx Billion.

United States Cybersecurity Industry Industry Evolution

The US cybersecurity market has experienced consistent growth throughout the historical period, driven by several factors. The increasing sophistication and frequency of cyberattacks, coupled with stringent data privacy regulations, have compelled organizations to invest heavily in cybersecurity solutions. Technological advancements, such as AI and machine learning, have enhanced the capabilities of cybersecurity tools, leading to higher adoption rates. The shift towards cloud computing has also created new opportunities for cloud-based security solutions. The market is anticipated to continue its growth trajectory, with an estimated xx% Compound Annual Growth Rate (CAGR) during the forecast period (2025-2033). This is fuelled by the growing adoption of cloud security solutions, the expanding use of Internet of Things (IoT) devices, and the rising demand for managed security services. The rising threat landscape and lack of skilled professionals add further impetus. Key technological advancements include improvements in AI-driven threat detection, enhanced endpoint security, and the expanding adoption of Zero Trust security models.

Leading Regions, Countries, or Segments in United States Cybersecurity Industry

The US cybersecurity market is geographically diverse, with significant demand across various regions. However, certain segments exhibit stronger growth and dominance.

- By Offering: Security Type (e.g., endpoint security, network security, cloud security) - Cloud security is witnessing the fastest growth due to the increasing adoption of cloud-based services. Network security remains a significant segment due to its critical role in protecting organizational infrastructure. Endpoint security, due to increasing endpoint devices, remains crucial and large. Services segment is growing rapidly, driven by managed security services providers (MSSPs) meeting the need for expertise.

- By Deployment: Cloud deployment is experiencing rapid growth, driven by the increasing adoption of cloud computing and the demand for scalable and flexible security solutions. On-premise deployment continues to hold a significant market share due to existing infrastructure and sensitivity concerning data residency.

- By End User: Government & Defense, BFSI, and Healthcare are prominent segments driven by stringent regulatory compliance requirements and the sensitive nature of the data they handle. The IT and Telecommunication sectors are key drivers due to their reliance on robust network security and protection of sensitive data.

Key Drivers:

- Government & Defense: Significant investments in cybersecurity infrastructure, driven by national security concerns and evolving cyber threats. Stringent regulatory compliance mandates.

- BFSI: Increased focus on protecting sensitive financial data from fraud and cyberattacks, leading to substantial cybersecurity investments. Compliance with numerous regulations is driving growth.

- Healthcare: Strict adherence to HIPAA and other regulations, along with the growing incidence of ransomware attacks targeting healthcare providers, is driving demand.

United States Cybersecurity Industry Product Innovations

Recent product innovations focus on AI-driven threat detection, automated security response, and enhanced endpoint protection. The integration of machine learning algorithms enables faster and more accurate threat identification and response. Zero Trust security models are gaining traction, emphasizing verification of every user and device accessing organizational resources. These innovations offer enhanced security, improved efficiency, and reduced reliance on manual intervention.

Propelling Factors for United States Cybersecurity Industry Growth

Several factors propel the growth of the US cybersecurity market. The escalating sophistication and frequency of cyberattacks, coupled with increased data breaches, are driving demand for robust security solutions. The growing adoption of cloud computing, IoT, and big data analytics introduces new security challenges and opportunities. Government regulations and initiatives promoting cybersecurity awareness and investment contribute significantly.

Obstacles in the United States Cybersecurity Industry Market

The US cybersecurity market faces several challenges. The shortage of skilled cybersecurity professionals is a significant barrier, limiting the ability of organizations to effectively manage their security risks. Supply chain disruptions can affect the availability of cybersecurity products and services. Intense competition among vendors also impacts profitability. Regulatory complexity and compliance costs pose additional hurdles.

Future Opportunities in United States Cybersecurity Industry

Emerging opportunities lie in the expansion of cloud security, AI-powered security solutions, and the increasing adoption of IoT security. The development and implementation of Zero Trust architectures and the growth of managed security services (MSSPs) create further opportunities. The increasing focus on securing critical infrastructure further expands the market potential.

Major Players in the United States Cybersecurity Industry Ecosystem

- FireEye Inc

- IBM Corporation

- Fortinet Inc

- F5 Networks Inc

- IDECSI Enterprise Security

- Cisco Systems Inc

- AVG Technologies

- Intel Security (Intel Corporation)

- Dell Technologies Inc

- Cyberark Software Ltd

- *List Not Exhaustive

Key Developments in United States Cybersecurity Industry Industry

- March 2022: Google Cloud acquires Mandiant for USD 5.4 Billion, highlighting the growing importance of proactive, SaaS-based security.

- March 2022: HelpSystems acquires AlertLogic, strengthening its MDR services portfolio in response to the increasing pressure on organizations from cyberattacks.

Strategic United States Cybersecurity Industry Market Forecast

The US cybersecurity market is poised for continued robust growth, driven by persistent cyber threats, increasing adoption of digital technologies, and ongoing regulatory changes. The focus on cloud security, AI-powered solutions, and managed security services will continue to shape the market landscape. The industry is expected to witness significant M&A activity and innovation in the coming years. The market's future is bright, driven by substantial investment and the fundamental need to protect digital assets.

United States Cybersecurity Industry Segmentation

-

1. Offering

-

1.1. Security Type

- 1.1.1. Cloud Security

- 1.1.2. Data Security

- 1.1.3. Identity Access Management

- 1.1.4. Network Security

- 1.1.5. Consumer Security

- 1.1.6. Infrastructure Protection

- 1.1.7. Other Types

- 1.2. Services

-

1.1. Security Type

-

2. Deployment

- 2.1. Cloud

- 2.2. On-premise

-

3. End User

- 3.1. BFSI

- 3.2. Healthcare

- 3.3. Manufacturing

- 3.4. Government & Defense

- 3.5. IT and Telecommunication

- 3.6. Other End Users

United States Cybersecurity Industry Segmentation By Geography

- 1. United States

United States Cybersecurity Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.09% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Demand for Digitalization and Scalable IT Infrastructure; Need to tackle risks from various trends such as third-party vendor risks

- 3.2.2 the evolution of MSSPs

- 3.2.3 and adoption of cloud-first strategy

- 3.3. Market Restrains

- 3.3.1. Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness

- 3.4. Market Trends

- 3.4.1. Need For Identity Access Management is One of the Factor Driving the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. United States Cybersecurity Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Security Type

- 5.1.1.1. Cloud Security

- 5.1.1.2. Data Security

- 5.1.1.3. Identity Access Management

- 5.1.1.4. Network Security

- 5.1.1.5. Consumer Security

- 5.1.1.6. Infrastructure Protection

- 5.1.1.7. Other Types

- 5.1.2. Services

- 5.1.1. Security Type

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. Cloud

- 5.2.2. On-premise

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. BFSI

- 5.3.2. Healthcare

- 5.3.3. Manufacturing

- 5.3.4. Government & Defense

- 5.3.5. IT and Telecommunication

- 5.3.6. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Belgium United States Cybersecurity Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 6.1.1.

- 7. Netherlands United States Cybersecurity Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 7.1.1.

- 8. Luxembourg United States Cybersecurity Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1.

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 FireEye Inc

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 IBM Corporation

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 Fortinet Inc

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 F5 Networks Inc

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 IDECSI Enterprise Security

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 Cisco Systems Inc

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 AVG Technologies

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 Intel Security (Intel Corporation)

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 Dell Technologies Inc

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.10 Cyberark Software Ltd*List Not Exhaustive

- 9.2.10.1. Overview

- 9.2.10.2. Products

- 9.2.10.3. SWOT Analysis

- 9.2.10.4. Recent Developments

- 9.2.10.5. Financials (Based on Availability)

- 9.2.1 FireEye Inc

List of Figures

- Figure 1: United States Cybersecurity Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: United States Cybersecurity Industry Share (%) by Company 2024

List of Tables

- Table 1: United States Cybersecurity Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: United States Cybersecurity Industry Revenue Million Forecast, by Offering 2019 & 2032

- Table 3: United States Cybersecurity Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 4: United States Cybersecurity Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 5: United States Cybersecurity Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: United States Cybersecurity Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States Cybersecurity Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: United States Cybersecurity Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: United States Cybersecurity Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United States Cybersecurity Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: United States Cybersecurity Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United States Cybersecurity Industry Revenue Million Forecast, by Offering 2019 & 2032

- Table 13: United States Cybersecurity Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 14: United States Cybersecurity Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 15: United States Cybersecurity Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Cybersecurity Industry?

The projected CAGR is approximately 8.09%.

2. Which companies are prominent players in the United States Cybersecurity Industry?

Key companies in the market include FireEye Inc, IBM Corporation, Fortinet Inc, F5 Networks Inc, IDECSI Enterprise Security, Cisco Systems Inc, AVG Technologies, Intel Security (Intel Corporation), Dell Technologies Inc, Cyberark Software Ltd*List Not Exhaustive.

3. What are the main segments of the United States Cybersecurity Industry?

The market segments include Offering, Deployment, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 85.79 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Digitalization and Scalable IT Infrastructure; Need to tackle risks from various trends such as third-party vendor risks. the evolution of MSSPs. and adoption of cloud-first strategy.

6. What are the notable trends driving market growth?

Need For Identity Access Management is One of the Factor Driving the Market.

7. Are there any restraints impacting market growth?

Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness.

8. Can you provide examples of recent developments in the market?

March 2022 - Google Cloud announced it is acquiring cybersecurity firm Mandiant, a player in proactive SaaS-based security. In light of the growing impact of cybercrime on all businesses across the country, the acquisition emphasizes the necessity of security for all enterprises, regardless of size. Mandiant will be acquired for an all-cash price of USD 23 per share in a deal worth USD 5.4 billion. Once the necessary stockholder and regulatory clearances are obtained, Mandiant will merge with Google Cloud.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Cybersecurity Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Cybersecurity Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Cybersecurity Industry?

To stay informed about further developments, trends, and reports in the United States Cybersecurity Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence