Key Insights

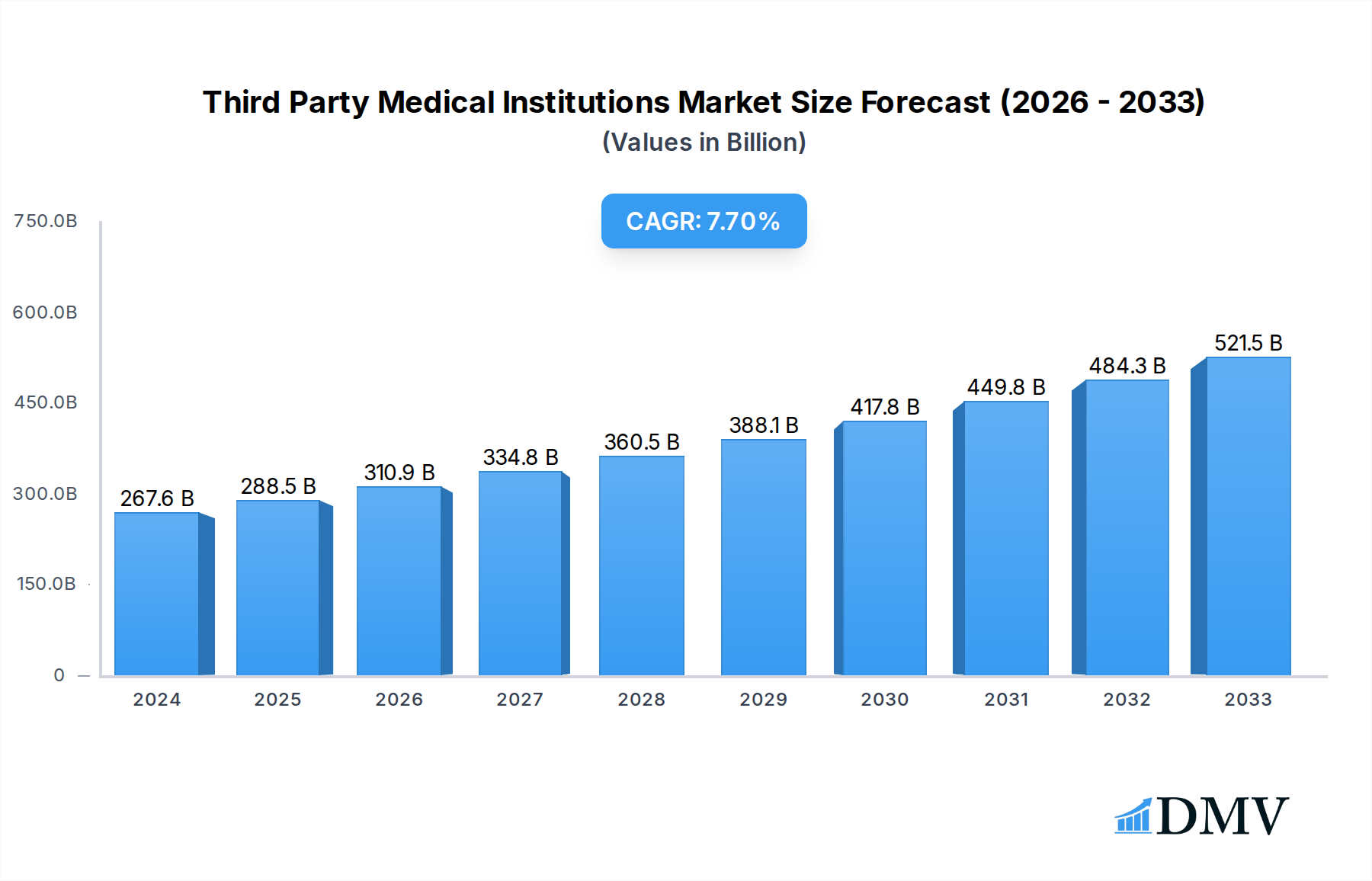

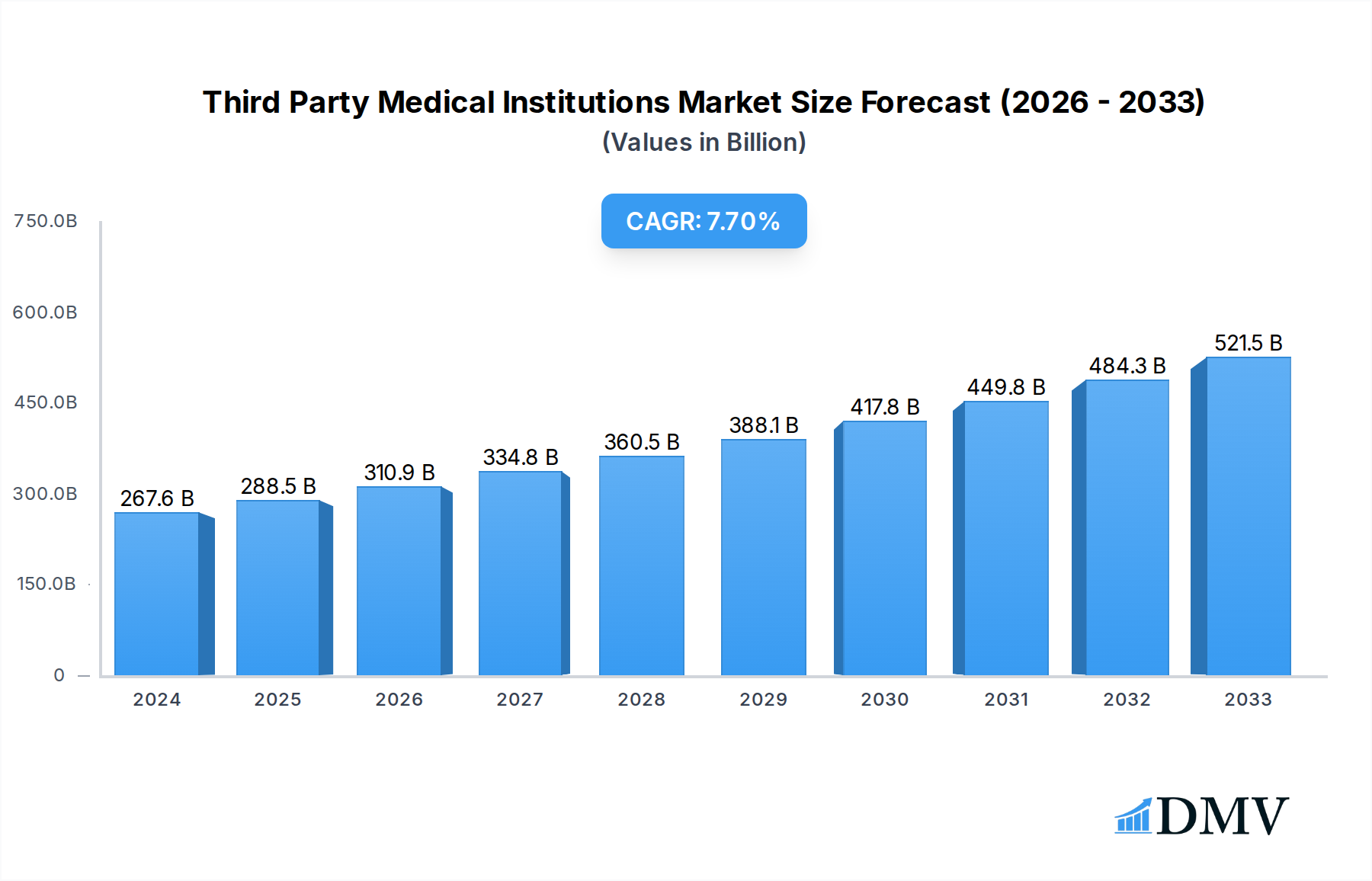

The global market for Third-Party Medical Institutions is experiencing robust growth, projected to reach an estimated $267.59 billion in 2024, expanding at a compelling Compound Annual Growth Rate (CAGR) of 7.8% through 2033. This expansion is primarily fueled by the increasing demand for specialized medical services, diagnostic testing, and sterile processing solutions, which third-party providers excel at delivering with efficiency and cost-effectiveness. Hospitals and clinics are increasingly outsourcing non-core functions to these institutions to optimize resource allocation, enhance patient care quality, and navigate complex regulatory landscapes. The growing emphasis on precision medicine, advanced diagnostics, and the need for stringent sterilization protocols in healthcare settings are significant drivers. Furthermore, technological advancements in medical equipment and diagnostic tools are creating new opportunities for third-party institutions to offer cutting-edge services. The market's trajectory indicates a sustained upward trend driven by outsourcing strategies and the continuous innovation within the medical services sector.

Third Party Medical Institutions Market Size (In Billion)

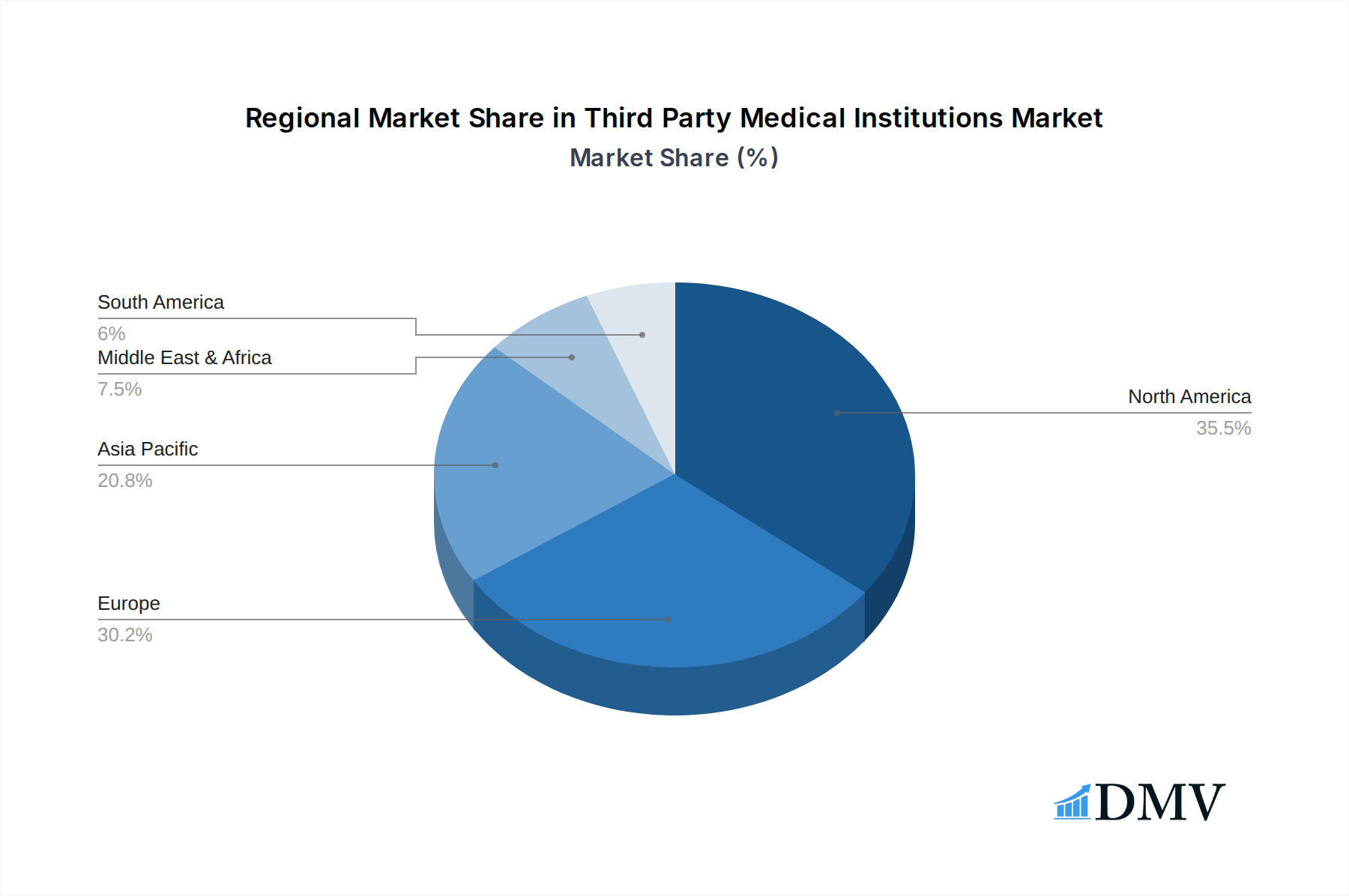

The market segmentation reveals a dynamic landscape with distinct growth trajectories for various applications and types of third-party medical institutions. In terms of application, hospitals are a dominant segment, driven by the high volume of procedures and diagnostic needs. Clinics are also showing significant growth as they expand their service offerings and rely on external expertise for specialized testing. Technically focused third-party institutions, such as those specializing in medical equipment maintenance and sterilization, are witnessing substantial demand due to the increasing complexity and cost of medical technology. Similarly, clinical medical third-party institutions, offering diagnostic and laboratory services, are benefiting from the growing reliance on accurate and timely test results. Geographically, North America and Europe currently hold significant market shares, driven by established healthcare infrastructures and a higher propensity for outsourcing. However, the Asia Pacific region is expected to emerge as a high-growth market, propelled by rapid infrastructure development, increasing healthcare expenditure, and a rising awareness of advanced medical diagnostics and sterilization practices.

Third Party Medical Institutions Company Market Share

Third Party Medical Institutions Market Composition & Trends

This comprehensive report delves into the dynamic Third Party Medical Institutions market, analyzing its intricate composition, emerging trends, and future trajectory. The study encompasses a robust period from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033, building upon a solid historical foundation (2019-2024). We meticulously examine market concentration, identifying key players and their respective market share distributions, which are estimated to be in the hundreds of billions of dollars. Innovation catalysts such as research and development investments, patent filings, and emerging technologies are thoroughly assessed, revealing a significant push towards precision medicine and AI-driven diagnostics. The evolving regulatory landscapes across major economies are analyzed for their impact on market entry and operational compliance, particularly concerning data privacy and international accreditation standards. Substitute products, including in-house laboratory services and alternative diagnostic methods, are evaluated for their competitive influence. End-user profiles, spanning hospitals, clinics, and other healthcare facilities, are profiled to understand their specific needs and adoption patterns for technical medical third-party institutions and clinical medical third-party institutions. Merger and acquisition (M&A) activities are highlighted, with estimated deal values in the tens of billions, indicating a consolidation trend as larger entities acquire specialized service providers to enhance their service portfolios.

- Market Share Distribution: Estimated to be fragmented with key players holding significant portions, contributing to a market value projected to reach trillions of dollars by 2033.

- M&A Deal Values: Anticipated to exceed tens of billions annually throughout the forecast period, signaling strategic consolidation.

- Innovation Catalysts: Focus on advanced molecular diagnostics, digital pathology, and telemedicine integration.

- Regulatory Impact: Stringent quality control measures and data security compliance are paramount.

- End-User Demand: Growing demand for cost-effective, specialized, and rapid diagnostic solutions.

Third Party Medical Institutions Industry Evolution

The Third Party Medical Institutions industry is undergoing a transformative evolution, characterized by sustained market growth trajectories, rapid technological advancements, and a significant shift in consumer demands. Over the historical period from 2019 to 2024, the market witnessed a consistent compound annual growth rate (CAGR) of approximately 8.5%, driven by increasing healthcare expenditure globally and a growing reliance on specialized external service providers for diagnostic and analytical needs. The base year of 2025 marks a pivotal point, with market projections indicating a continued upward trend, expected to reach a valuation in the trillions of dollars by the end of the forecast period in 2033. This expansion is largely fueled by the increasing complexity of medical diagnostics, the need for specialized expertise that many healthcare institutions may not possess in-house, and the cost-effectiveness of outsourcing these services.

Technological advancements are at the forefront of this evolution. The integration of Artificial Intelligence (AI) and Machine Learning (ML) in image analysis and data interpretation is revolutionizing the speed and accuracy of diagnostic processes, leading to earlier disease detection and more personalized treatment plans. Innovations in molecular diagnostics, including next-generation sequencing (NGS) and liquid biopsies, are opening new avenues for cancer detection and management. Furthermore, the adoption of digital pathology and cloud-based platforms is enhancing collaboration among medical professionals and improving the accessibility of diagnostic reports, irrespective of geographical location. The estimated adoption rate of AI in diagnostic imaging alone is projected to surpass 60% by 2028, a testament to its transformative impact.

Shifting consumer demands, particularly from healthcare providers (our primary end-users), are also shaping the industry. There is a growing imperative for faster turnaround times, enhanced accuracy, and cost containment. This has led to increased outsourcing of routine and specialized testing to third-party institutions that can offer economies of scale and advanced technological capabilities. The demand for personalized medicine, driven by a better understanding of genetic predispositions and disease mechanisms, is further propelling the growth of specialized genetic testing and biomarker analysis services. The market for clinical trials support services, a significant segment within third-party medical institutions, is also experiencing robust growth, with an estimated CAGR of 9.2% during the forecast period, as pharmaceutical companies increasingly rely on external expertise for efficient trial management and data analysis. The overall market size is projected to reach $1.8 trillion by 2033, a substantial leap from its estimated $750 billion valuation in 2024.

Leading Regions, Countries, or Segments in Third Party Medical Institutions

The Third Party Medical Institutions market exhibits distinct regional dominance and segment leadership, driven by a confluence of investment trends, robust regulatory frameworks, and evolving healthcare demands. Among the applications, the Hospital segment consistently emerges as the largest and most influential, accounting for an estimated 55% of the total market share in 2025. This dominance is attributed to the sheer volume of diagnostic and analytical needs within hospital settings, encompassing emergency care, surgical support, chronic disease management, and extensive inpatient services. Hospitals rely heavily on third-party institutions for specialized testing, advanced imaging analysis, and comprehensive laboratory services that complement their in-house capabilities, driving an estimated $412.5 billion in spending within this segment in 2025 alone.

When considering the Type of third-party institutions, Clinical Medical Third-Party Institutions are currently leading, capturing approximately 65% of the market. This leadership is underpinned by the widespread demand for routine and specialized clinical laboratory testing, including hematology, biochemistry, immunology, and microbiology. The increasing prevalence of chronic diseases and the growing emphasis on preventive healthcare further bolster the demand for these services. The global market for clinical diagnostics is projected to reach $600 billion by 2033, with third-party providers playing a crucial role in fulfilling this demand.

Geographically, North America is projected to retain its position as the leading region, contributing an estimated 35% to the global market value in 2025, valued at approximately $262.5 billion. This regional dominance is fueled by several key drivers:

- High Healthcare Expenditure: North America, particularly the United States, boasts the highest per capita healthcare spending globally, translating into substantial investment in diagnostic and medical services.

- Advanced Technological Adoption: The region is a pioneer in adopting cutting-edge medical technologies, including AI-powered diagnostics, automation in laboratories, and advanced imaging techniques, creating a strong market for innovative third-party services.

- Favorable Regulatory Environment: While stringent, the regulatory framework in North America (e.g., FDA, CLIA) provides a clear pathway for the establishment and operation of high-quality third-party medical institutions, fostering trust and reliability.

- Presence of Major Players: The region is home to several global leaders in the medical third-party sector, including Quest Diagnostics, LabCorp, and DaVita, whose extensive networks and service offerings significantly contribute to market volume.

- Growing Chronic Disease Burden: The rising incidence of chronic conditions such as diabetes, cardiovascular diseases, and cancer necessitates continuous and specialized diagnostic monitoring, driving consistent demand for third-party services.

In parallel, Asia Pacific is emerging as the fastest-growing region, with an anticipated CAGR of 10.5% over the forecast period, driven by expanding healthcare infrastructure, increasing disposable incomes, and a growing awareness of advanced medical diagnostics. Countries like China and India are witnessing a surge in demand, with government initiatives aimed at improving healthcare access and quality.

Third Party Medical Institutions Product Innovations

The Third Party Medical Institutions sector is witnessing a surge in product innovations aimed at enhancing diagnostic accuracy, speed, and patient outcomes. A significant advancement lies in the development of AI-powered diagnostic algorithms that can analyze complex medical images, such as X-rays, CT scans, and MRIs, with unprecedented speed and precision, often identifying subtle anomalies missed by the human eye. These algorithms are integrated into remote diagnostic platforms, enabling specialists to review cases from anywhere in the world, thereby expanding access to expertise. Furthermore, the evolution of next-generation sequencing (NGS) technologies has revolutionized genetic testing, allowing for comprehensive genomic profiling for personalized cancer therapies and the identification of rare genetic disorders. The performance metrics of these innovations are remarkable, with AI-driven image analysis showing up to 95% accuracy in certain diagnoses, and NGS offering the ability to sequence entire genomes in a matter of days, compared to months previously. The unique selling proposition for these innovations lies in their ability to democratize access to high-quality diagnostics, improve patient stratification for targeted treatments, and significantly reduce diagnostic turnaround times, contributing to more effective and efficient healthcare delivery.

Propelling Factors for Third Party Medical Institutions Growth

Several potent factors are propelling the growth of the Third Party Medical Institutions market. Technological advancements, particularly in AI, machine learning, and advanced molecular diagnostics, are enabling more accurate, faster, and cost-effective testing. The increasing prevalence of chronic diseases globally necessitates continuous monitoring and specialized diagnostics, a demand met by outsourcing to third-party providers. Economic factors, such as the pursuit of cost containment by healthcare providers and the inherent economies of scale offered by specialized third-party institutions, are driving outsourcing decisions. Furthermore, favorable regulatory environments in many regions, coupled with a growing emphasis on outsourcing non-core competencies by healthcare organizations, are creating a conducive ecosystem for growth. The expanding healthcare infrastructure in emerging economies also presents a significant untapped market.

Obstacles in the Third Party Medical Institutions Market

Despite robust growth, the Third Party Medical Institutions market faces several significant obstacles. Stringent and evolving regulatory compliance across different jurisdictions can create complexities and increase operational costs, particularly concerning data privacy (e.g., GDPR, HIPAA) and quality assurance standards. Supply chain disruptions, exacerbated by geopolitical events or global health crises, can impact the availability of essential reagents, equipment, and specialized personnel, leading to delays and increased costs, potentially affecting the market by as much as 5-10% in terms of operational efficiency. Intense competitive pressures among established players and emerging niche providers can lead to price wars and reduced profit margins. Furthermore, cybersecurity threats and the risk of data breaches are major concerns, necessitating substantial investments in robust security infrastructure. The ethical considerations surrounding outsourcing of sensitive patient data also require careful navigation.

Future Opportunities in Third Party Medical Institutions

The future landscape of Third Party Medical Institutions is ripe with opportunities. The burgeoning demand for personalized medicine and companion diagnostics presents a significant avenue for growth, especially in oncology and rare diseases. The increasing adoption of telehealth and remote patient monitoring creates opportunities for third-party institutions to provide remote diagnostic services and data analysis. The expansion of healthcare infrastructure in emerging markets across Asia, Africa, and Latin America offers substantial untapped potential. Furthermore, the integration of blockchain technology for secure and transparent data management holds promise. The growing focus on preventive healthcare and wellness diagnostics also opens new market segments for proactive health assessments.

Major Players in the Third Party Medical Institutions Ecosystem

- Fresenius

- Baxter

- DaVita

- STERIS

- Sterigenics

- Unilabs

- Quest Diagnostics

- Sonic Healthcare

- LabCorp

- Laoken Medical

- Aecssd Medical

- Julikang

- Steriguard Medical

Key Developments in Third Party Medical Institutions Industry

- 2023 August: Quest Diagnostics launches a new suite of advanced genomic testing services to support precision oncology, impacting cancer treatment planning.

- 2023 December: STERIS completes the acquisition of a specialized sterilization services provider, expanding its global footprint and service offerings.

- 2024 January: LabCorp announces significant investments in AI-powered data analytics to enhance diagnostic accuracy and efficiency.

- 2024 March: DaVita expands its kidney dialysis services into new international markets, increasing its global reach.

- 2024 May: Sterigenics enhances its compliance and quality assurance protocols following increased regulatory scrutiny in the sterilization industry.

- 2024 July: Sonic Healthcare reports strong growth driven by an increase in molecular diagnostic testing volume.

- 2024 September: Baxter introduces a new line of advanced renal care products, further solidifying its market position.

- 2024 November: Fresenius highlights advancements in its home dialysis solutions, focusing on patient convenience and autonomy.

- 2025 February: Unilabs expands its laboratory network in Europe, aiming to improve accessibility and turnaround times for diagnostic services.

- 2025 April: Julikang announces strategic partnerships to develop and offer advanced diagnostic kits for infectious diseases.

- 2025 June: Aecssd Medical and Steriguard Medical collaborate on innovative infection control solutions for healthcare settings.

- 2025 August: Laoken Medical unveils a new automated laboratory system designed to increase throughput and reduce errors.

Strategic Third Party Medical Institutions Market Forecast

The strategic forecast for the Third Party Medical Institutions market paints a picture of robust and sustained expansion, driven by an interplay of technological innovation, evolving healthcare needs, and favorable economic undercurrents. The market's growth is intrinsically linked to the increasing demand for specialized, accurate, and cost-effective diagnostic and analytical services across hospitals and clinics. Advancements in AI, molecular diagnostics, and digital health are not merely incremental but transformative, promising to reshape diagnostic paradigms. Furthermore, the ongoing global trend of outsourcing non-core competencies by healthcare providers, coupled with the sheer volume of the patient population requiring sophisticated medical interventions, ensures a consistent demand for the services offered by technical medical third-party institutions and clinical medical third-party institutions. The market potential is immense, with projections indicating a continued upward trajectory, solidifying the indispensable role of these institutions in the modern healthcare ecosystem.

Third Party Medical Institutions Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Other

-

2. Type

- 2.1. Technical Medical Third-Party Institutions

- 2.2. Clinical Medical Third-Party Institutions

Third Party Medical Institutions Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Third Party Medical Institutions Regional Market Share

Geographic Coverage of Third Party Medical Institutions

Third Party Medical Institutions REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Technical Medical Third-Party Institutions

- 5.2.2. Clinical Medical Third-Party Institutions

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Third Party Medical Institutions Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Technical Medical Third-Party Institutions

- 6.2.2. Clinical Medical Third-Party Institutions

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Third Party Medical Institutions Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Technical Medical Third-Party Institutions

- 7.2.2. Clinical Medical Third-Party Institutions

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Third Party Medical Institutions Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Technical Medical Third-Party Institutions

- 8.2.2. Clinical Medical Third-Party Institutions

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Third Party Medical Institutions Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Technical Medical Third-Party Institutions

- 9.2.2. Clinical Medical Third-Party Institutions

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Third Party Medical Institutions Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Technical Medical Third-Party Institutions

- 10.2.2. Clinical Medical Third-Party Institutions

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Third Party Medical Institutions Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospital

- 11.1.2. Clinic

- 11.1.3. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Technical Medical Third-Party Institutions

- 11.2.2. Clinical Medical Third-Party Institutions

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Fresenius

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Baxter

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 DaVita

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 STERIS

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Sterigenics

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Unilabs

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Quest Diagnostics

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sonic Healthcare

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 LabCorp

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Laoken Medical

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Aecssd Medical

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Julikang

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Steriguard Medical

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Fresenius

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Third Party Medical Institutions Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Third Party Medical Institutions Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Third Party Medical Institutions Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Third Party Medical Institutions Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Third Party Medical Institutions Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Third Party Medical Institutions Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Third Party Medical Institutions Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Third Party Medical Institutions Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Third Party Medical Institutions Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Third Party Medical Institutions Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Third Party Medical Institutions Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Third Party Medical Institutions Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Third Party Medical Institutions Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Third Party Medical Institutions Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Third Party Medical Institutions Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Third Party Medical Institutions Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Third Party Medical Institutions Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Third Party Medical Institutions Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Third Party Medical Institutions Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Third Party Medical Institutions Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Third Party Medical Institutions Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Third Party Medical Institutions Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Third Party Medical Institutions Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Third Party Medical Institutions Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Third Party Medical Institutions Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Third Party Medical Institutions Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Third Party Medical Institutions Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Third Party Medical Institutions Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Third Party Medical Institutions Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Third Party Medical Institutions Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Third Party Medical Institutions Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Third Party Medical Institutions Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Third Party Medical Institutions Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Third Party Medical Institutions Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Third Party Medical Institutions Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Third Party Medical Institutions Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Third Party Medical Institutions Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Third Party Medical Institutions Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Third Party Medical Institutions Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Third Party Medical Institutions Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Third Party Medical Institutions Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Third Party Medical Institutions Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Third Party Medical Institutions Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Third Party Medical Institutions Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Third Party Medical Institutions Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Third Party Medical Institutions Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Third Party Medical Institutions Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Third Party Medical Institutions Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Third Party Medical Institutions Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Third Party Medical Institutions Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Third Party Medical Institutions?

The projected CAGR is approximately 7.8%.

2. Which companies are prominent players in the Third Party Medical Institutions?

Key companies in the market include Fresenius, Baxter, DaVita, STERIS, Sterigenics, Unilabs, Quest Diagnostics, Sonic Healthcare, LabCorp, Laoken Medical, Aecssd Medical, Julikang, Steriguard Medical.

3. What are the main segments of the Third Party Medical Institutions?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Third Party Medical Institutions," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Third Party Medical Institutions report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Third Party Medical Institutions?

To stay informed about further developments, trends, and reports in the Third Party Medical Institutions, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence