Key Insights

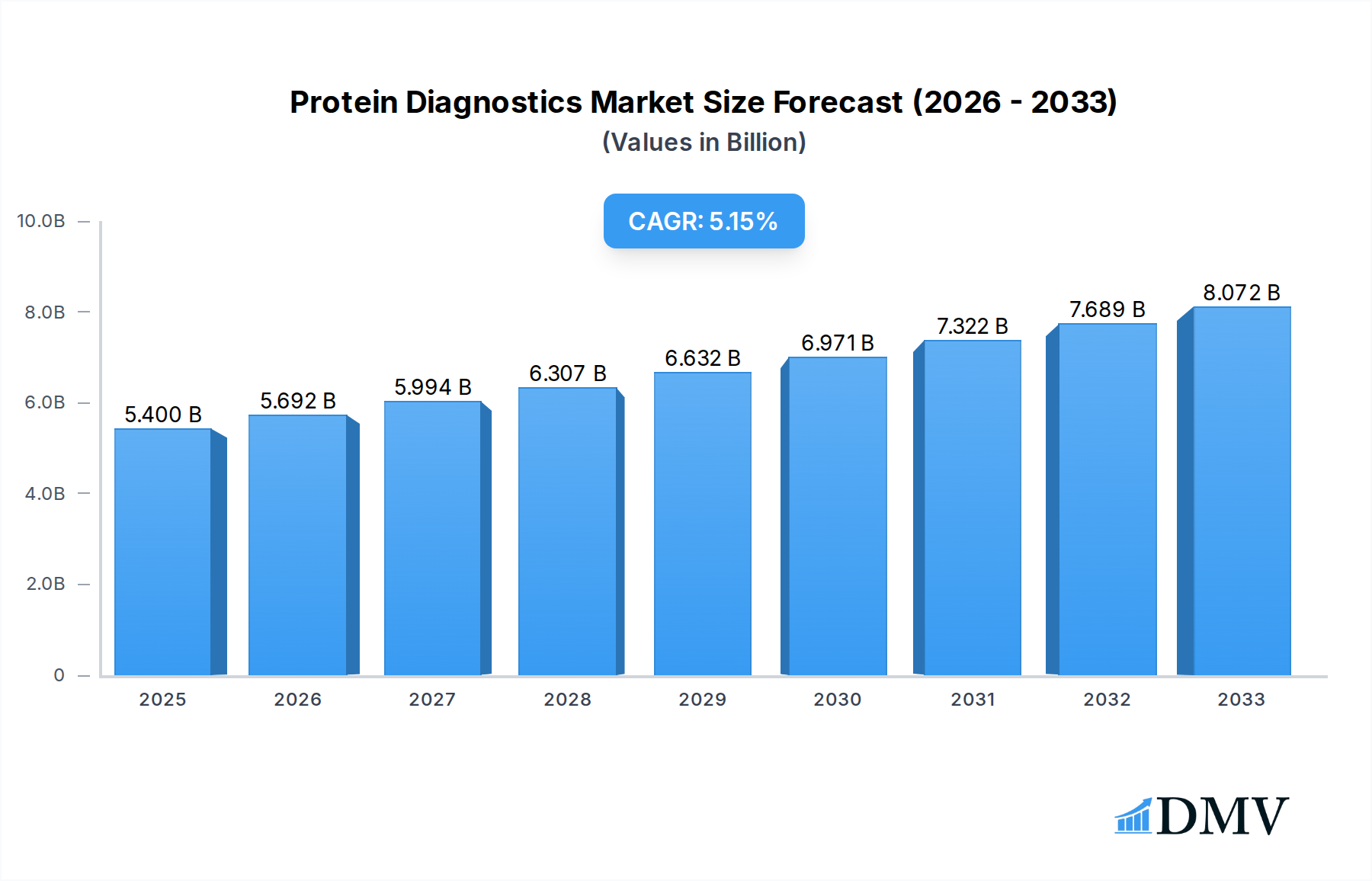

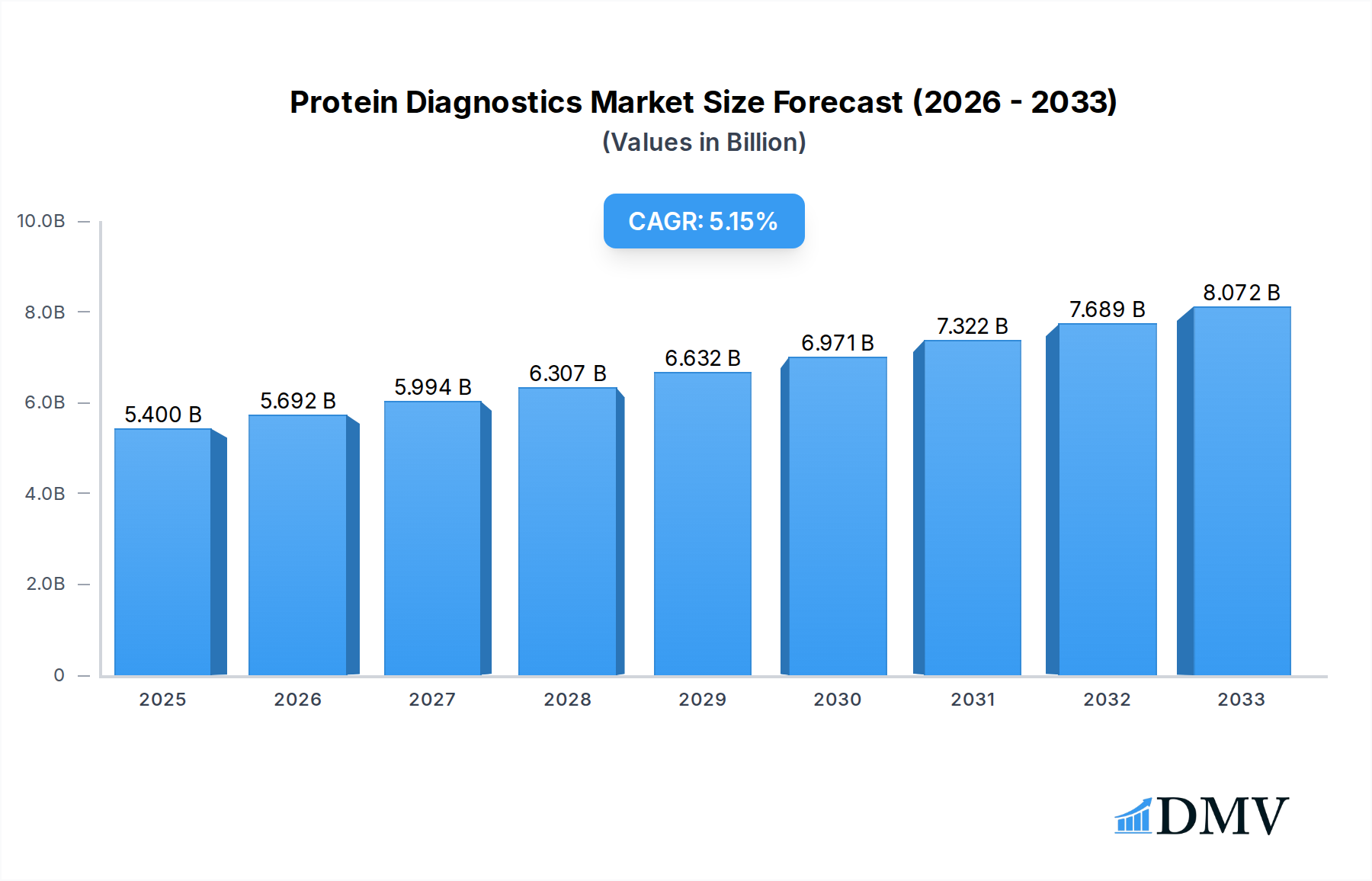

The global Protein Diagnostics market is poised for significant expansion, projected to reach $5.4 billion in 2025 and demonstrating a robust compound annual growth rate (CAGR) of 5.4% through 2033. This dynamic growth is primarily propelled by the increasing prevalence of chronic diseases, such as cancer and cardiovascular disorders, which necessitate advanced diagnostic tools for early detection and effective management. The burgeoning demand for personalized medicine and companion diagnostics further fuels market expansion, as protein-based biomarkers play a crucial role in tailoring treatments to individual patient profiles. Advancements in proteomics research and the development of high-throughput screening technologies are also contributing to the market's upward trajectory. The market is segmented into applications such as Drug Discovery and Development and Disease Diagnosis, with Analyzers and Reagents forming the key product types driving revenue.

Protein Diagnostics Market Size (In Billion)

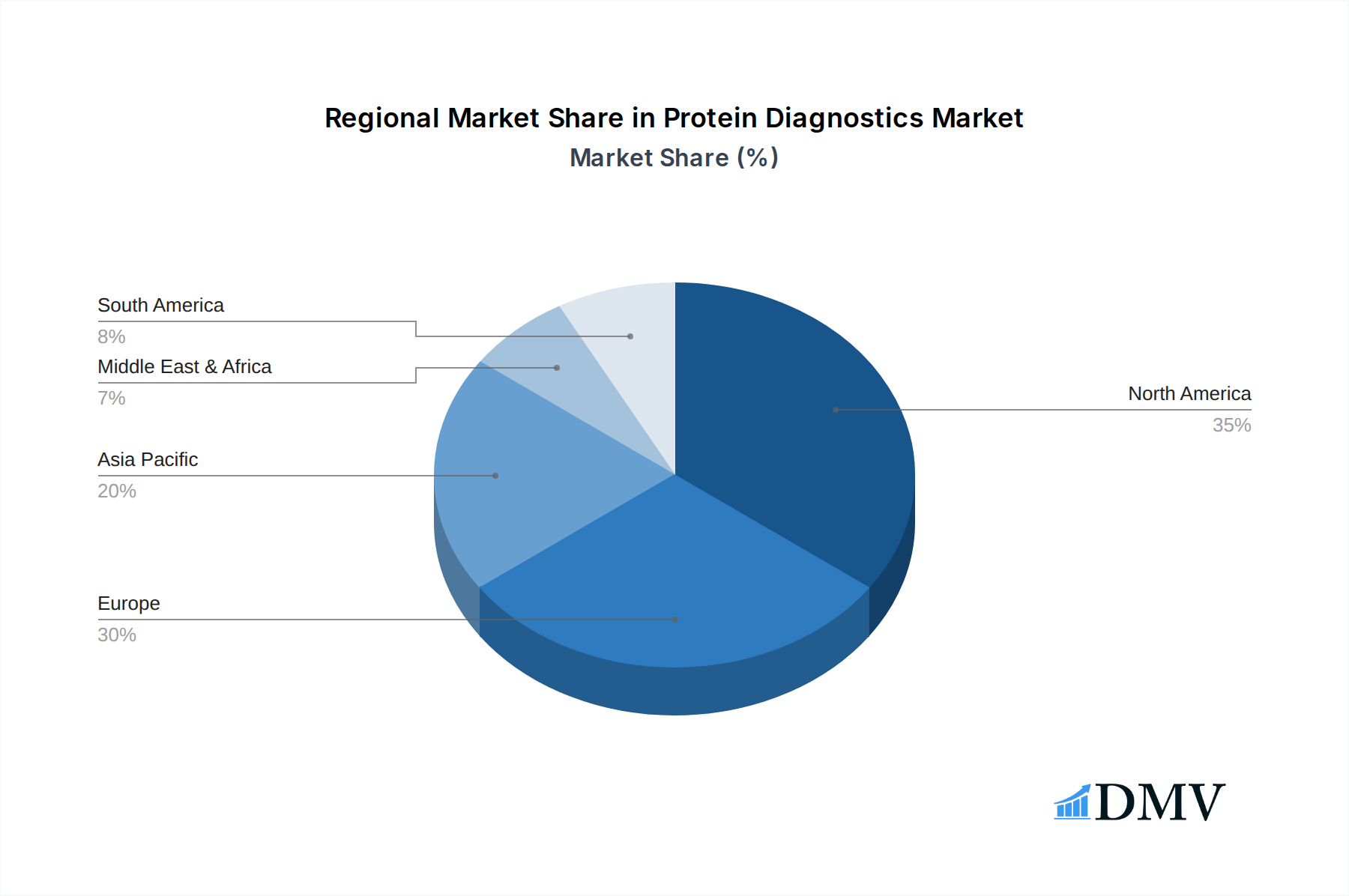

Key trends shaping the Protein Diagnostics market include the integration of artificial intelligence and machine learning in data analysis for biomarker discovery, leading to more accurate and efficient diagnostic outcomes. The growing adoption of point-of-care testing (POCT) devices for protein diagnostics is also a significant trend, enabling rapid results and improved patient accessibility. Geographically, North America and Europe currently dominate the market due to established healthcare infrastructures and high R&D investments. However, the Asia Pacific region is expected to witness the fastest growth, driven by increasing healthcare expenditure, a rising burden of chronic diseases, and a growing number of research initiatives. While market growth is strong, challenges such as the high cost of advanced diagnostic technologies and stringent regulatory approvals for new protein-based assays may present some restraints. Nonetheless, the overall outlook for the Protein Diagnostics market remains highly optimistic.

Protein Diagnostics Company Market Share

Protein Diagnostics Market Composition & Trends

The global protein diagnostics market, a critical sector within in vitro diagnostics (IVD), is projected to experience substantial growth, with market size anticipated to reach one billion in the coming years. This dynamic landscape is characterized by a moderate level of market concentration, with key players like Danaher, Siemens Healthineers, and Roche Ltd. holding significant shares. The drug discovery and development and disease diagnosis segments are the primary application drivers, fueled by an increasing demand for accurate and early detection of diseases and the development of novel therapeutics. Innovation catalysts are abundant, driven by advancements in proteomics, mass spectrometry, and biomarker discovery. The regulatory landscape, while stringent, is progressively adapting to facilitate the approval of innovative protein diagnostic tools. Substitute products, though present in some diagnostic areas, are increasingly being superseded by the superior sensitivity and specificity offered by protein-based assays. End-user profiles are diverse, encompassing academic research institutions, pharmaceutical and biotechnology companies, and clinical laboratories. Mergers and acquisitions (M&A) are strategic maneuvers aimed at consolidating market presence and expanding product portfolios, with recent deals valuing in the billions, signifying robust investor confidence and a drive towards market leadership.

- Market Share Distribution: Danaher, Siemens Healthineers, and Roche Ltd. collectively account for approximately 50% of the market share.

- M&A Deal Values: Recent strategic acquisitions and partnerships have seen valuations exceeding one billion.

- Key Market Drivers: Growth in personalized medicine, rising prevalence of chronic diseases, and increasing R&D investments.

- Innovation Focus: Development of high-throughput screening platforms, advanced immunoassay technologies, and liquid biopsy solutions.

- Regulatory Environment: Harmonization efforts and streamlined approval pathways for novel diagnostic assays.

Protein Diagnostics Industry Evolution

The protein diagnostics industry has undergone a remarkable evolution, transforming from niche research applications to indispensable tools in modern healthcare and life sciences. Over the study period of 2019–2033, with a base year of 2025, the market has witnessed a consistent upward trajectory, driven by an insatiable demand for precise biological insights. The historical period (2019–2024) laid the groundwork, characterized by steady adoption of established protein detection methods like ELISA and Western blotting. However, the true revolution began with the integration of advanced technologies. The estimated year of 2025 marks a pivotal point, where the convergence of artificial intelligence (AI) in data analysis and next-generation sequencing (NGS) for proteogenomics is unlocking unprecedented diagnostic capabilities.

The forecast period (2025–2033) is poised for accelerated growth, with an anticipated Compound Annual Growth Rate (CAGR) exceeding xx%. This expansion is primarily fueled by the burgeoning fields of precision medicine and early disease detection. As our understanding of the proteome – the complete set of proteins expressed by an organism – deepens, so does the ability to identify subtle molecular changes indicative of disease long before overt symptoms appear. For instance, the development of highly sensitive mass spectrometry techniques allows for the quantification of low-abundance protein biomarkers in biological fluids, paving the way for non-invasive diagnostics like liquid biopsies. Companies like Agilent Technologies, Inc. and Shenzhen Mindray Bio-Medical Electronics Co., Ltd. are at the forefront of developing sophisticated analyzers and reagents that enable these complex analyses.

Consumer demand is also shifting significantly. Patients and healthcare providers are increasingly seeking diagnostic solutions that offer not only accuracy but also speed and convenience. This has spurred innovation in point-of-care (POC) protein diagnostics, enabling rapid testing directly at the patient's bedside. The application in drug discovery and development remains a cornerstone, with protein diagnostics playing a crucial role in target identification, validation, and the assessment of drug efficacy and safety. The ability to monitor protein expression levels in response to therapeutic interventions provides invaluable data for optimizing drug regimens. Furthermore, the burgeoning field of companion diagnostics is leveraging protein biomarkers to guide treatment decisions, ensuring that patients receive the most effective therapies tailored to their individual molecular profiles. This integration of protein diagnostics into the clinical workflow is a testament to its evolving significance.

Leading Regions, Countries, or Segments in Protein Diagnostics

The North America region stands as a dominant force in the global protein diagnostics market, driven by a confluence of robust healthcare infrastructure, significant investments in research and development, and a high prevalence of chronic diseases. Within North America, the United States spearheads this dominance, boasting a vibrant ecosystem of leading pharmaceutical companies, cutting-edge research institutions, and a well-established regulatory framework that supports the swift adoption of innovative diagnostic technologies. The Disease Diagnosis segment, particularly for oncological, cardiovascular, and neurological disorders, represents the largest application area, fueled by an aging population and a growing emphasis on preventative healthcare.

Key drivers contributing to North America's leadership include substantial government and private funding for life sciences research, fostering innovation in protein biomarker discovery and assay development. The presence of major players like Danaher, Siemens Healthineers, and Roche Ltd., with their extensive portfolios of analyzers and reagents, further solidifies the region's market position. Furthermore, the increasing demand for personalized medicine, where protein diagnostics play a pivotal role in identifying patient-specific biomarkers for targeted therapies, contributes significantly to market growth. The Type: Analyzers segment, encompassing advanced automated platforms, is particularly strong in this region, enabling high-throughput screening and complex proteomic analyses. The regulatory environment, while rigorous, is designed to encourage the development and commercialization of novel diagnostic solutions, accelerating market penetration.

- Dominant Region: North America, with the United States as the primary contributor.

- Leading Application Segment: Disease Diagnosis, specifically in oncology and cardiovascular diseases.

- Leading Type Segment: Analyzers, due to demand for advanced automation and high-throughput capabilities.

- Key Investment Trends: Significant venture capital funding in proteomics and biomarker discovery startups.

- Regulatory Support: Favorable pathways for the approval and adoption of novel diagnostic devices and assays.

- Impact of Healthcare Policies: Initiatives promoting early disease detection and personalized treatment approaches.

- Technological Advancements: Widespread adoption of mass spectrometry, immunoassay platforms, and next-generation sequencing for proteogenomic analysis.

Protein Diagnostics Product Innovations

The protein diagnostics market is abuzz with groundbreaking product innovations aimed at enhancing sensitivity, specificity, and throughput. Advances in mass spectrometry are enabling the identification and quantification of a vast array of low-abundance protein biomarkers with unparalleled accuracy, revolutionizing fields like cancer diagnostics and drug development. Next-generation immunoassay platforms leverage novel antibody engineering and detection chemistries to achieve detection limits in the femtogram range, crucial for early disease detection. Furthermore, the integration of artificial intelligence and machine learning algorithms into diagnostic software is transforming data interpretation, allowing for more sophisticated pattern recognition and predictive diagnostics. These innovations are driving the development of highly multiplexed assays capable of simultaneously detecting dozens or even hundreds of protein targets from a single sample, offering a comprehensive molecular snapshot.

Propelling Factors for Protein Diagnostics Growth

Several interconnected factors are propelling the growth of the protein diagnostics market. Technological advancements, particularly in proteomics, mass spectrometry, and high-throughput screening, are continuously expanding the capabilities of protein analysis. The increasing prevalence of chronic diseases like cancer, cardiovascular disease, and neurodegenerative disorders necessitates more accurate and early diagnostic tools, creating a sustained demand for protein-based assays. Furthermore, the paradigm shift towards personalized medicine, where treatment decisions are guided by individual molecular profiles, relies heavily on the identification of relevant protein biomarkers. Government initiatives and growing investments in healthcare infrastructure and R&D further catalyze market expansion, fostering innovation and facilitating the adoption of new diagnostic technologies.

Obstacles in the Protein Diagnostics Market

Despite its promising growth, the protein diagnostics market faces several inherent obstacles. The regulatory landscape, while evolving, can still present lengthy and complex approval processes for novel diagnostic tests, delaying market entry. The high cost associated with advanced protein analysis instrumentation and specialized reagents can be a significant barrier, particularly for smaller research institutions and clinics in resource-limited settings. Furthermore, the standardization of protein assays across different platforms and laboratories remains a challenge, impacting reproducibility and comparability of results. Supply chain disruptions, as witnessed in recent global events, can also affect the availability of critical raw materials and components, leading to production delays and increased costs.

Future Opportunities in Protein Diagnostics

Emerging opportunities in the protein diagnostics market are vast and exciting. The burgeoning field of liquid biopsy presents a significant avenue for growth, offering non-invasive methods for early cancer detection, monitoring treatment response, and detecting recurrence. The increasing application of protein diagnostics in infectious disease surveillance and vaccine development is another key area. Furthermore, the integration of AI and machine learning in predictive diagnostics and digital health platforms holds immense potential for personalized risk assessment and proactive health management. Expansion into emerging economies with growing healthcare expenditures and the development of point-of-care protein diagnostics for decentralized testing also represent significant future growth avenues.

Major Players in the Protein Diagnostics Ecosystem

Danaher Siemens Healthineers Roche Ltd. Agilent Technologies, Inc. Shenzhen Mindray Bio-Medical Electronics Co., Ltd. Elabscience Biotechnology Inc. Goldsite Diagnostics Inc. Getein Biotech, Inc. Randox Laboratories Ltd. Hipro Biotechnology Co., Ltd. Beijing Strong Biotechnologies

Key Developments in Protein Diagnostics Industry

- 2024 (Q1): Elabscience Biotechnology Inc. launched a new line of highly sensitive ELISA kits for key cancer biomarkers, enhancing early detection capabilities.

- 2023 (Q4): Siemens Healthineers announced a strategic partnership with a leading AI firm to integrate advanced analytics into their protein diagnostic platforms, improving diagnostic accuracy.

- 2023 (Q3): Agilent Technologies, Inc. expanded its proteomics portfolio with the acquisition of a novel mass spectrometry technology company, strengthening its position in high-resolution protein analysis.

- 2023 (Q2): Roche Ltd. received FDA approval for a companion diagnostic test based on protein biomarkers, aiding in personalized cancer therapy selection.

- 2022 (Q4): Shenzhen Mindray Bio-Medical Electronics Co., Ltd. unveiled a new automated immunoassay analyzer with significantly reduced turnaround times for critical protein tests.

- 2022 (Q3): Randox Laboratories Ltd. reported significant progress in developing multiplex protein assays for the detection of Alzheimer's disease markers.

- 2022 (Q1): Danaher completed a major acquisition of a company specializing in liquid biopsy technologies, reinforcing its commitment to advanced cancer diagnostics.

- 2021 (Q4): Goldsite Diagnostics Inc. introduced an innovative point-of-care protein diagnostic device for cardiovascular risk assessment.

- 2021 (Q2): Getein Biotech, Inc. launched a new generation of chemiluminescence immunoassay reagents, offering enhanced sensitivity and stability.

- 2020 (Q4): Hipro Biotechnology Co., Ltd. focused on developing novel protein detection methods for emerging infectious diseases.

- 2019 (Q3): Beijing Strong Biotechnologies expanded its production capacity for critical protein diagnostic reagents to meet rising global demand.

Strategic Protein Diagnostics Market Forecast

The strategic protein diagnostics market forecast is overwhelmingly positive, driven by a potent combination of technological innovation, increasing healthcare expenditure, and a global drive towards precision medicine. Anticipated advancements in proteomics, liquid biopsy, and AI-driven diagnostics are poised to unlock new frontiers in disease detection and therapeutic intervention. The growing understanding of complex protein interactions and their role in disease pathogenesis will fuel the development of more accurate and personalized diagnostic solutions. Strategic investments in R&D, coupled with favorable regulatory environments in key markets, will continue to propel market expansion. The growing demand for early and accurate diagnosis across a spectrum of diseases, from cancer to infectious diseases, ensures a sustained and robust market trajectory for protein diagnostics in the coming years.

Protein Diagnostics Segmentation

-

1. Application

- 1.1. Drug Discovery and Development

- 1.2. Disease Diagnosis

- 1.3. Other

-

2. Type

- 2.1. Analyzers

- 2.2. Reagents

Protein Diagnostics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Protein Diagnostics Regional Market Share

Geographic Coverage of Protein Diagnostics

Protein Diagnostics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Drug Discovery and Development

- 5.1.2. Disease Diagnosis

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Analyzers

- 5.2.2. Reagents

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Protein Diagnostics Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Drug Discovery and Development

- 6.1.2. Disease Diagnosis

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Analyzers

- 6.2.2. Reagents

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Protein Diagnostics Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Drug Discovery and Development

- 7.1.2. Disease Diagnosis

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Analyzers

- 7.2.2. Reagents

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Protein Diagnostics Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Drug Discovery and Development

- 8.1.2. Disease Diagnosis

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Analyzers

- 8.2.2. Reagents

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Protein Diagnostics Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Drug Discovery and Development

- 9.1.2. Disease Diagnosis

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Analyzers

- 9.2.2. Reagents

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Protein Diagnostics Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Drug Discovery and Development

- 10.1.2. Disease Diagnosis

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Analyzers

- 10.2.2. Reagents

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Protein Diagnostics Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Drug Discovery and Development

- 11.1.2. Disease Diagnosis

- 11.1.3. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Analyzers

- 11.2.2. Reagents

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Danaher

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Siemens Healthineers

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Roche Ltd.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Agilent Technologies Inc.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Shenzhen Mindray Bio-Medical Electronics Co. Ltd.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Elabscience Biotechnology Inc.

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Goldsite Diagnostics Inc.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Getein Biotech Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Randox Laboratories Ltd.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Hipro Biotechnology Co. Ltd.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Beijing Strong Biotechnologies

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Danaher

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Protein Diagnostics Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Protein Diagnostics Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Protein Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Protein Diagnostics Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Protein Diagnostics Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Protein Diagnostics Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Protein Diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Protein Diagnostics Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Protein Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Protein Diagnostics Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Protein Diagnostics Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Protein Diagnostics Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Protein Diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Protein Diagnostics Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Protein Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Protein Diagnostics Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Protein Diagnostics Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Protein Diagnostics Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Protein Diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Protein Diagnostics Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Protein Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Protein Diagnostics Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Protein Diagnostics Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Protein Diagnostics Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Protein Diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Protein Diagnostics Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Protein Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Protein Diagnostics Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Protein Diagnostics Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Protein Diagnostics Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Protein Diagnostics Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Protein Diagnostics Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Protein Diagnostics Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Protein Diagnostics Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Protein Diagnostics Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Protein Diagnostics Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Protein Diagnostics Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Protein Diagnostics Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Protein Diagnostics Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Protein Diagnostics Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Protein Diagnostics Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Protein Diagnostics Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Protein Diagnostics Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Protein Diagnostics Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Protein Diagnostics Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Protein Diagnostics Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Protein Diagnostics Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Protein Diagnostics Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Protein Diagnostics Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Protein Diagnostics Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Protein Diagnostics?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the Protein Diagnostics?

Key companies in the market include Danaher, Siemens Healthineers, Roche Ltd., Agilent Technologies, Inc., Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Elabscience Biotechnology Inc., Goldsite Diagnostics Inc., Getein Biotech, Inc., Randox Laboratories Ltd., Hipro Biotechnology Co., Ltd., Beijing Strong Biotechnologies.

3. What are the main segments of the Protein Diagnostics?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.4 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Protein Diagnostics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Protein Diagnostics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Protein Diagnostics?

To stay informed about further developments, trends, and reports in the Protein Diagnostics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence