Key Insights

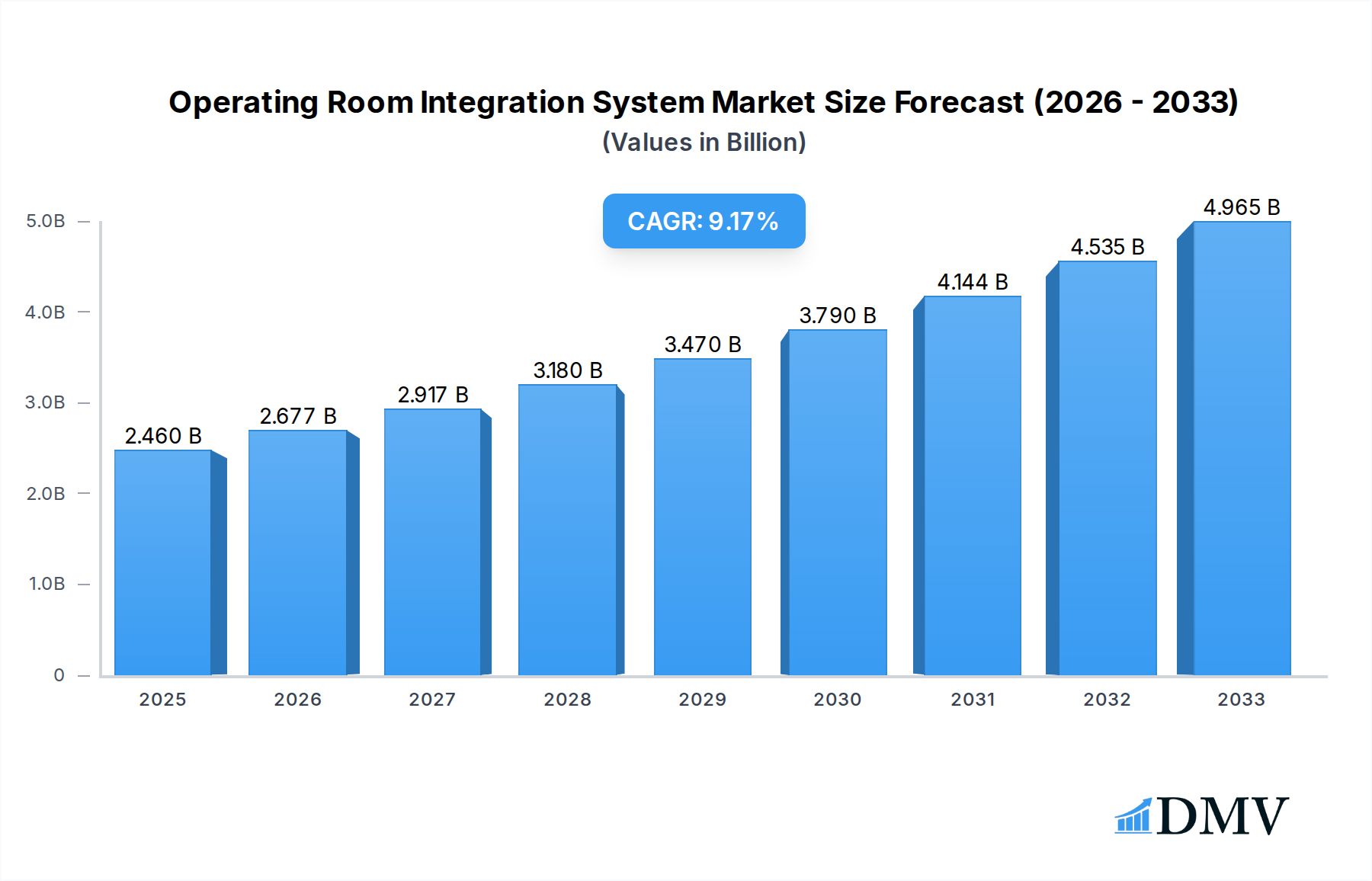

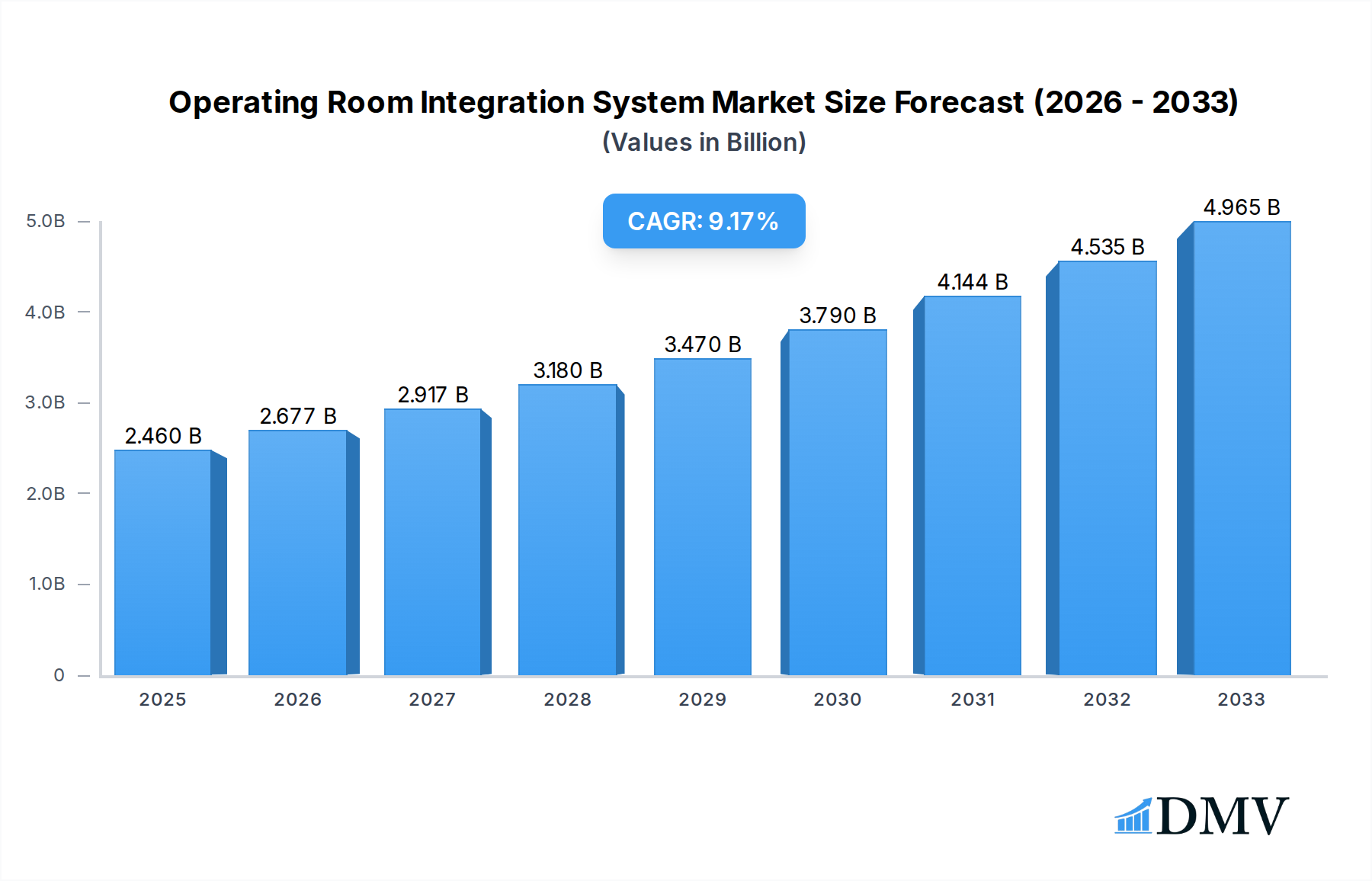

The global Operating Room Integration System market is poised for significant expansion, projected to reach approximately USD 2.46 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 10.8% anticipated between 2025 and 2033. This dynamic growth is fueled by increasing advancements in surgical technology, the rising demand for minimally invasive procedures, and the growing emphasis on enhancing patient safety and surgical efficiency. Key drivers include the escalating adoption of high-definition display systems and advanced audio-video management solutions, which are transforming surgical workflows by providing surgeons with enhanced visualization and real-time data access. Furthermore, the trend towards smart operating rooms equipped with integrated digital solutions is accelerating, enabling seamless communication and collaboration among surgical teams, ultimately leading to improved patient outcomes and reduced recovery times.

Operating Room Integration System Market Size (In Billion)

The market's trajectory is also shaped by the growing preference for hybrid operating rooms that can accommodate both traditional open surgeries and minimally invasive interventions, offering greater procedural flexibility. While the market exhibits strong growth potential, certain factors could influence its pace. These include the substantial initial investment required for implementing sophisticated integration systems and the ongoing need for skilled personnel to operate and maintain these complex technologies. However, the persistent drive for better healthcare infrastructure, coupled with strategic collaborations between technology providers and healthcare institutions, is expected to mitigate these restraints. Prominent players like Stryker, Karl Storz, and Olympus are at the forefront of innovation, continuously introducing cutting-edge solutions that cater to the evolving needs of the surgical landscape, further solidifying the market's upward trajectory across various applications and system types.

Operating Room Integration System Company Market Share

Operating Room Integration System Market Composition & Trends

The global operating room integration system market is characterized by moderate to high concentration, with a significant presence of established players like Stryker, Karl Storz, Olympus, Merivauna, MAQUET Gmb, Skytron, Steris, Brainlab, BD, Doricon Medical Systems, and Synergy Medical. Innovation catalysts are primarily driven by the increasing demand for minimally invasive surgeries, the need for enhanced surgical precision and collaboration, and advancements in digital health technologies. Regulatory landscapes are evolving, with a growing emphasis on data security, interoperability standards, and device efficacy, influencing product development and market entry. Substitute products, though limited in direct replacement capabilities, include standalone surgical equipment and less integrated systems. End-user profiles are diverse, encompassing hospitals, ambulatory surgery centers, and specialized surgical facilities, all seeking to optimize patient outcomes and operational efficiency. Mergers and acquisitions (M&A) activities are prevalent, with significant deal values – estimated to be in the billions – reflecting the strategic importance of consolidating market share and expanding technological portfolios. For instance, a recent M&A deal in the last study period involved a valuation exceeding $1 billion, demonstrating investor confidence. The market share distribution is highly competitive, with top players holding substantial portions, but niche segments offer opportunities for specialized companies.

Operating Room Integration System Industry Evolution

The operating room integration system industry has witnessed a profound evolution over the historical period of 2019-2024, driven by an accelerating trajectory of market growth and transformative technological advancements. This evolution has been underpinned by a discernible shift in consumer demands, with healthcare providers increasingly prioritizing integrated solutions that enhance surgical workflow, improve patient safety, and facilitate better clinical decision-making. During the study period, the market has experienced a compound annual growth rate (CAGR) of approximately 8.5%, projecting a market size that could reach hundreds of billions by 2033. This robust growth can be attributed to the escalating adoption of hybrid operating rooms (Hybrid ORs), which demand sophisticated integration of imaging, navigation, and communication systems. Furthermore, the continuous pursuit of greater surgical accuracy and the reduction of surgical errors have spurred the integration of high-definition display systems, advanced recording and documentation capabilities, and seamless audio-video management solutions. The base year of 2025 serves as a critical juncture, with an estimated market value of $XX billion, poised for significant expansion. The industry's evolution is not merely incremental; it represents a fundamental paradigm shift towards digitally empowered surgical environments. The increasing complexity of surgical procedures necessitates advanced visualization and data management, directly fueling the demand for comprehensive operating room integration systems. Historical data from 2019-2024 indicates a consistent upward trend in investment in these advanced technologies, with a noticeable acceleration in the latter half of this period. The adoption metrics for integrated systems have steadily increased, moving from a niche offering to a standard requirement in modern surgical suites. This evolution is further amplified by the growing emphasis on remote surgical assistance and training, where integrated systems play a pivotal role in facilitating real-time collaboration and knowledge transfer.

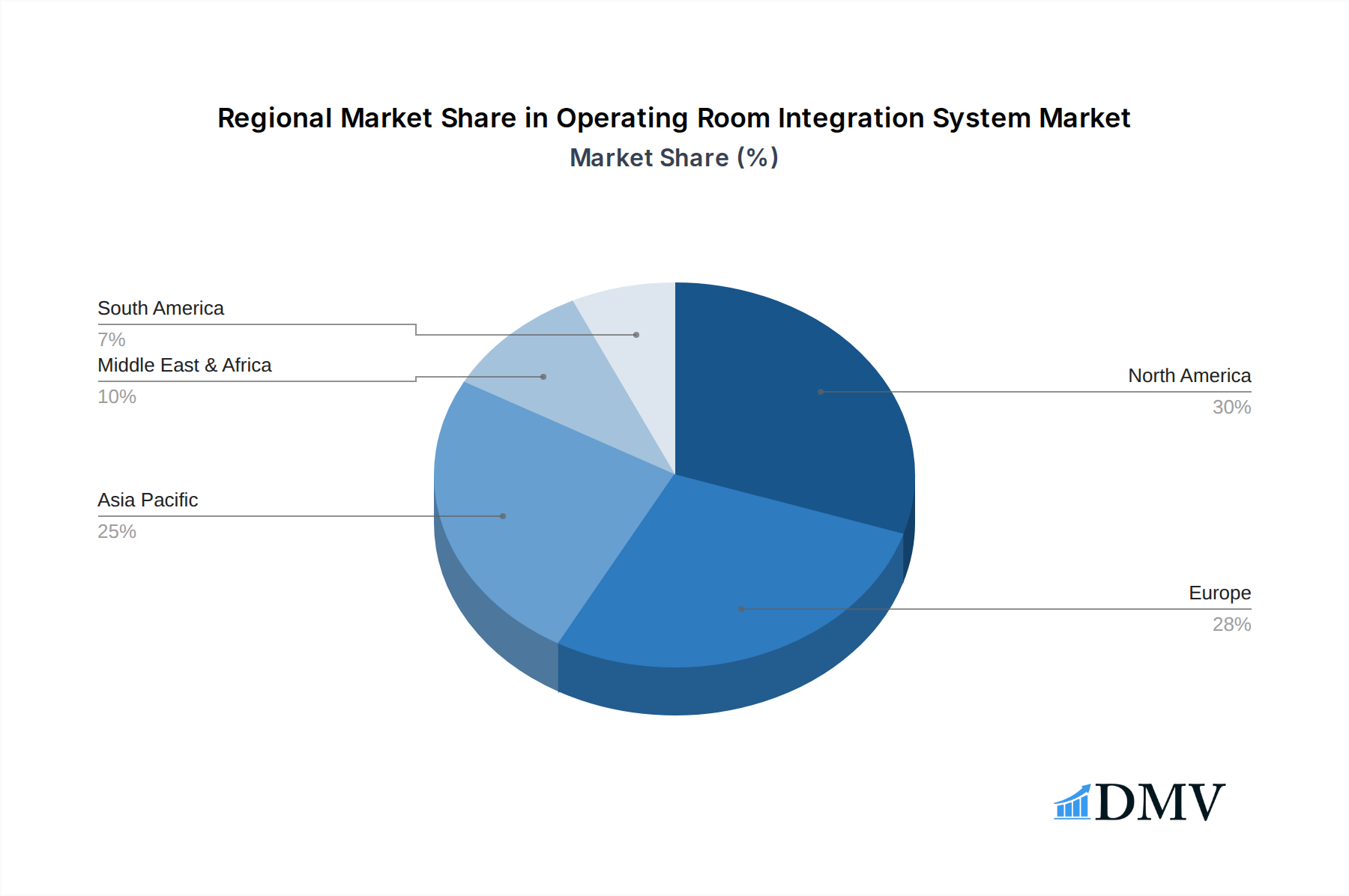

Leading Regions, Countries, or Segments in Operating Room Integration System

North America currently stands as the dominant region in the Operating Room Integration System market, driven by substantial healthcare expenditure, a high concentration of advanced healthcare facilities, and robust adoption of cutting-edge surgical technologies. The United States, in particular, leads this charge, fueled by significant investments in hospital infrastructure and a proactive regulatory environment that encourages innovation.

Key Drivers of Dominance in North America:

- Investment Trends: Hospitals and healthcare systems in North America are consistently investing billions of dollars in upgrading their surgical suites with advanced integration systems. This includes investments in sophisticated Hybrid ORs, which are pivotal in complex cardiac and neurosurgical procedures.

- Regulatory Support: While stringent, the regulatory framework in North America, particularly in the U.S. with bodies like the FDA, fosters the development and adoption of innovative medical technologies, including operating room integration. This has led to increased R&D funding and faster product approvals.

- Technological Adoption: The region exhibits a high propensity for adopting new technologies, such as High Definition Display Systems offering unparalleled visual clarity, and comprehensive Recording and Documentation Systems essential for quality control and legal compliance.

- Surgeon Preference: North American surgeons are often early adopters of advanced tools, seeking systems that enhance precision, reduce fatigue, and facilitate seamless collaboration during complex procedures.

Dominance in Application Segments:

- Hybrid OR: The demand for Hybrid ORs is exceptionally high in North America due to their capability to integrate diagnostic imaging and interventional procedures, allowing for minimally invasive treatments and improved patient outcomes. This segment alone accounts for an estimated $XX billion of the total market.

- General OR: While Hybrid ORs represent a high-growth segment, the General OR remains the largest in terms of volume. The integration of Audio and Video Management Systems, along with High Definition Display Systems, is becoming standard across these settings to improve efficiency and patient care.

Dominance in Type Segments:

- High Definition Display System: The need for superior visualization in minimally invasive and complex surgeries has made High Definition Display Systems a critical component of operating room integration. Their contribution to improved diagnostic accuracy and surgical precision is undeniable, with market penetration reaching an estimated XX% in advanced surgical centers.

- Recording and Documentation System: With increasing emphasis on patient safety, medico-legal compliance, and quality improvement initiatives, Recording and Documentation Systems are indispensable. The market for these systems is projected to reach $XX billion by 2033, driven by the need for comprehensive surgical records.

- Audio and Video Management System: Seamless integration and management of audio and video feeds from multiple sources (endoscopes, cameras, displays) are crucial for effective surgical collaboration and training. This segment is expected to grow robustly, supporting the increasing complexity of surgical interventions.

The robust market in North America, coupled with the specific dominance in Hybrid ORs and the widespread adoption of High Definition Display Systems, underscores the region's leadership in the global Operating Room Integration System market.

Operating Room Integration System Product Innovations

Operating room integration systems are witnessing rapid innovation, with advancements focusing on enhanced imaging fidelity and AI-powered surgical assistance. Companies are introducing ultra-high definition 4K and even 8K displays that provide surgeons with unparalleled visual clarity, crucial for intricate procedures. Innovations in cloud-based recording and documentation systems are streamlining data management and accessibility, enabling seamless retrieval of surgical footage for training and review. Furthermore, smart audio and video management systems are leveraging AI to automatically tag critical surgical events, reducing manual documentation efforts. Performance metrics are demonstrating significant improvements in surgical efficiency and accuracy, with an estimated reduction in procedure times by up to 15% in facilities utilizing advanced integrated systems.

Propelling Factors for Operating Room Integration System Growth

The growth of the operating room integration system market is propelled by several key factors. Technological advancements, particularly in robotics, AI, and high-definition imaging, are driving demand for integrated solutions that can seamlessly incorporate these innovations. The increasing prevalence of chronic diseases and the subsequent rise in the number of surgical procedures globally necessitate more efficient and precise surgical environments. Favorable reimbursement policies and government initiatives promoting healthcare infrastructure development in emerging economies also play a crucial role. Furthermore, the growing emphasis on patient safety and the reduction of surgical errors are compelling healthcare providers to invest in integrated systems that enhance surgical workflow and provide comprehensive data management.

Obstacles in the Operating Room Integration System Market

Despite robust growth, the operating room integration system market faces several obstacles. High initial investment costs associated with implementing comprehensive integration systems can be a significant barrier, particularly for smaller healthcare facilities. The complex interoperability requirements between different medical devices and IT systems pose a technical challenge, often leading to integration issues and delays. Stringent regulatory hurdles and data privacy concerns, especially with the increasing digitization of healthcare, also create a complex landscape for market players. Moreover, a shortage of skilled IT professionals and surgeons trained to operate advanced integrated systems can impede widespread adoption and utilization.

Future Opportunities in Operating Room Integration System

The future of operating room integration systems presents significant opportunities. The expanding adoption of AI and machine learning within surgical workflows, offering predictive analytics and real-time decision support, is a major avenue for growth. The increasing demand for minimally invasive and outpatient surgeries will drive the need for compact, highly integrated systems. Furthermore, the development of personalized medicine approaches will require sophisticated integration capabilities to tailor surgical plans and data management to individual patient needs. Emerging markets in Asia-Pacific and Latin America, with their rapidly growing healthcare sectors, offer substantial untapped potential for market expansion.

Major Players in the Operating Room Integration System Ecosystem

- Stryker

- Karl Storz

- Olympus

- Merivaara

- MAQUET Gmb

- Skytron

- Steris

- Brainlab

- BD

- Doricon Medical Systems

- Synergy Medical

Key Developments in Operating Room Integration System Industry

- 2023: Stryker launches a new generation of integrated surgical platforms with enhanced AI capabilities, aiming to improve surgical outcomes and efficiency.

- 2023: Karl Storz and Olympus announce a strategic partnership to develop interoperable imaging and integration solutions for hybrid ORs, fostering greater collaboration.

- 2023: Merivaara introduces a modular operating room integration system designed for scalability and future-proofing, catering to diverse surgical needs.

- 2024: MAQUET Gmb unveils an advanced patient monitoring and data integration solution for ORs, focusing on real-time data analytics and clinical decision support.

- 2024: Steris completes a major acquisition of a leading surgical navigation company, significantly expanding its portfolio in advanced operating room integration.

- 2024: Skytron announces the integration of advanced cybersecurity features into its OR integration solutions, addressing growing concerns about data breaches.

- 2025: Brainlab introduces a next-generation software platform for enhanced surgical planning and intraoperative guidance, emphasizing AI-driven precision.

- 2025: BD expands its presence in the OR integration market with a focus on connected device solutions for improved workflow efficiency and patient safety.

- 2025: Doricon Medical Systems launches a new series of high-definition displays optimized for augmented reality applications in surgery.

- 2025: Synergy Medical showcases its comprehensive OR integration suite, highlighting seamless workflow management and improved communication capabilities.

Strategic Operating Room Integration System Market Forecast

The strategic outlook for the operating room integration system market is exceptionally positive, driven by the relentless pursuit of enhanced surgical precision, improved patient outcomes, and operational efficiency. The forecast period, 2025–2033, anticipates sustained growth, fueled by ongoing technological innovation and increasing healthcare investments globally. The expansion of hybrid operating rooms, the integration of AI and robotics, and the growing demand for data-driven surgical insights will serve as key growth catalysts. Emerging markets present significant untapped potential, promising substantial expansion opportunities for leading players and innovative solutions. The market's trajectory is set to transform surgical environments into more connected, intelligent, and patient-centric spaces, with an estimated market valuation reaching several hundred billion by the end of the forecast period.

Operating Room Integration System Segmentation

-

1. Application

- 1.1. Hybrid OR

- 1.2. General OR

-

2. Type

- 2.1. High Definition Display System

- 2.2. Recording and Documentation System

- 2.3. Audio and Video Management System

Operating Room Integration System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Operating Room Integration System Regional Market Share

Geographic Coverage of Operating Room Integration System

Operating Room Integration System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hybrid OR

- 5.1.2. General OR

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. High Definition Display System

- 5.2.2. Recording and Documentation System

- 5.2.3. Audio and Video Management System

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Operating Room Integration System Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hybrid OR

- 6.1.2. General OR

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. High Definition Display System

- 6.2.2. Recording and Documentation System

- 6.2.3. Audio and Video Management System

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Operating Room Integration System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hybrid OR

- 7.1.2. General OR

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. High Definition Display System

- 7.2.2. Recording and Documentation System

- 7.2.3. Audio and Video Management System

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Operating Room Integration System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hybrid OR

- 8.1.2. General OR

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. High Definition Display System

- 8.2.2. Recording and Documentation System

- 8.2.3. Audio and Video Management System

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Operating Room Integration System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hybrid OR

- 9.1.2. General OR

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. High Definition Display System

- 9.2.2. Recording and Documentation System

- 9.2.3. Audio and Video Management System

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Operating Room Integration System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hybrid OR

- 10.1.2. General OR

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. High Definition Display System

- 10.2.2. Recording and Documentation System

- 10.2.3. Audio and Video Management System

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Operating Room Integration System Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hybrid OR

- 11.1.2. General OR

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. High Definition Display System

- 11.2.2. Recording and Documentation System

- 11.2.3. Audio and Video Management System

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Stryker

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Karl Storz

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Olympus

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Merivaara

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 MAQUET Gmb

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Skytron

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Steris

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Brainlab

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 BD

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Doricon Medical Systems

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Synergy Medical

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Stryker

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Operating Room Integration System Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Operating Room Integration System Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Operating Room Integration System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Operating Room Integration System Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Operating Room Integration System Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Operating Room Integration System Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Operating Room Integration System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Operating Room Integration System Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Operating Room Integration System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Operating Room Integration System Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Operating Room Integration System Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Operating Room Integration System Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Operating Room Integration System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Operating Room Integration System Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Operating Room Integration System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Operating Room Integration System Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Operating Room Integration System Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Operating Room Integration System Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Operating Room Integration System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Operating Room Integration System Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Operating Room Integration System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Operating Room Integration System Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Operating Room Integration System Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Operating Room Integration System Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Operating Room Integration System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Operating Room Integration System Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Operating Room Integration System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Operating Room Integration System Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Operating Room Integration System Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Operating Room Integration System Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Operating Room Integration System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Operating Room Integration System Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Operating Room Integration System Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Operating Room Integration System Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Operating Room Integration System Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Operating Room Integration System Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Operating Room Integration System Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Operating Room Integration System Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Operating Room Integration System Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Operating Room Integration System Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Operating Room Integration System Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Operating Room Integration System Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Operating Room Integration System Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Operating Room Integration System Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Operating Room Integration System Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Operating Room Integration System Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Operating Room Integration System Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Operating Room Integration System Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Operating Room Integration System Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Operating Room Integration System Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Operating Room Integration System?

The projected CAGR is approximately 10.8%.

2. Which companies are prominent players in the Operating Room Integration System?

Key companies in the market include Stryker, Karl Storz, Olympus, Merivaara, MAQUET Gmb, Skytron, Steris, Brainlab, BD, Doricon Medical Systems, Synergy Medical.

3. What are the main segments of the Operating Room Integration System?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.46 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Operating Room Integration System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Operating Room Integration System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Operating Room Integration System?

To stay informed about further developments, trends, and reports in the Operating Room Integration System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence