Key Insights

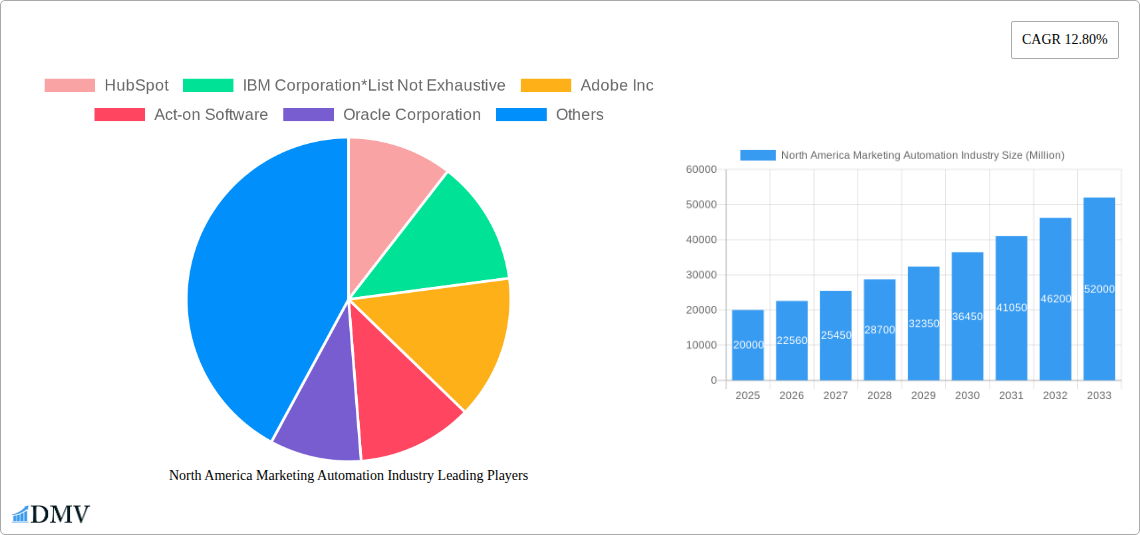

The North American marketing automation market is experiencing robust growth, driven by the increasing adoption of digital marketing strategies across various industries. The market's Compound Annual Growth Rate (CAGR) of 12.80% from 2019 to 2024 suggests a significant expansion, and this momentum is expected to continue throughout the forecast period (2025-2033). Key drivers include the need for enhanced customer engagement, improved lead generation and nurturing, data-driven decision-making, and increasing demand for personalized marketing campaigns. The rise of cloud-based solutions offers scalability and cost-effectiveness, further fueling market expansion. While the exact market size in 2025 is not provided, considering the 12.80% CAGR and extrapolating from a hypothetical 2019 value, we can assume a substantial market size (for example, if the 2019 market was $10 billion, by 2025 it would be approximately $20 billion, considering an average of 12.8% CAGR across the period. This is an estimate, not a projection.) Furthermore, the market is segmented by application (Campaign Management, Social Media Marketing, etc.), end-user industry (Government, Advertising, etc.), and deployment (On-premise, Cloud). The cloud segment is experiencing particularly rapid growth due to its flexibility and accessibility. Major players like HubSpot, IBM, Adobe, Salesforce, and others are intensely competing, driving innovation and expanding the market’s capabilities.

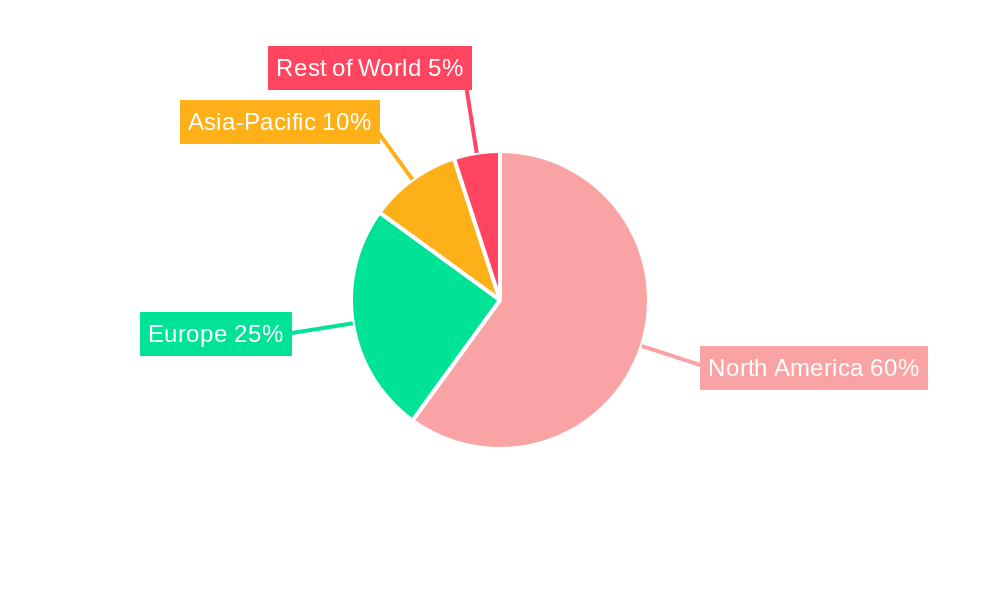

The North American region dominates the market due to factors such as high technological adoption, a developed digital infrastructure, and the presence of numerous large enterprises across various sectors. Within North America, the United States is the largest market, followed by Canada and Mexico. The strong presence of leading technology companies and a digitally savvy population contribute to the region's significant market share. However, potential restraints include the high initial investment costs associated with implementing marketing automation solutions, concerns about data privacy and security, and the need for skilled personnel to manage and utilize these complex systems effectively. Despite these challenges, the continued growth of digital marketing and the rising importance of data-driven strategies point towards a continued upward trajectory for the North American marketing automation market in the coming years.

North America Marketing Automation Industry: A Comprehensive Market Report (2019-2033)

This insightful report provides a detailed analysis of the North America marketing automation industry, covering market size, segmentation, leading players, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and an estimated year of 2025, this report offers a comprehensive overview for stakeholders seeking to understand this dynamic market. The forecast period extends from 2025-2033, encompassing the historical period of 2019-2024. The market is projected to reach xx Million by 2033.

North America Marketing Automation Industry Market Composition & Trends

This section delves into the competitive landscape of the North American marketing automation market, examining market concentration, innovation drivers, regulatory factors, substitute products, end-user profiles, and mergers & acquisitions (M&A) activity. The market is characterized by a combination of established players like HubSpot, IBM Corporation, Adobe Inc, Act-on Software, Oracle Corporation, and Salesforce, and emerging niche players. Market share distribution amongst these companies is currently estimated at xx%, with the top 5 companies holding approximately xx% of the total market share.

- Market Concentration: Highly concentrated with a few dominant players, but significant opportunities for smaller players in niche segments.

- Innovation Catalysts: AI-powered personalization, predictive analytics, and cross-channel campaign management.

- Regulatory Landscape: Compliance with data privacy regulations (e.g., CCPA, GDPR) is a significant factor.

- Substitute Products: Limited direct substitutes, but other marketing tools pose indirect competition.

- End-User Profiles: The market encompasses diverse end-user industries, including BFSI, healthcare, retail, and manufacturing.

- M&A Activity: Significant M&A activity, with deal values ranging from xx Million to xx Million in recent years, driving market consolidation and technological advancement. Examples include the acquisition of Datarati by OSF Digital (January 2022).

North America Marketing Automation Industry Industry Evolution

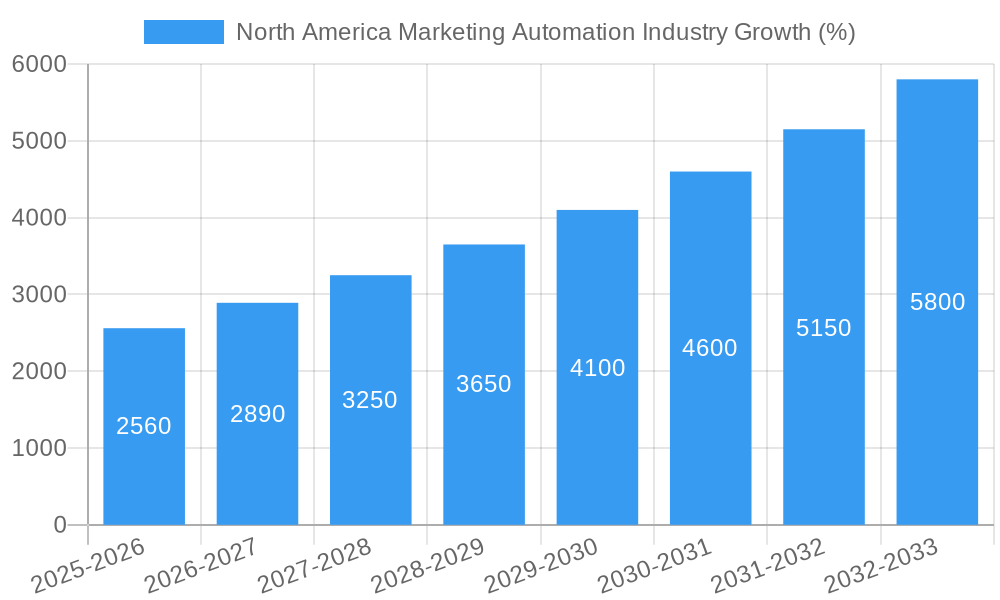

The North American marketing automation industry has witnessed remarkable growth over the past few years, driven by increasing adoption of digital marketing strategies and the need for enhanced customer engagement. From 2019 to 2024, the market experienced a Compound Annual Growth Rate (CAGR) of xx%, reaching xx Million in 2024. This growth is fueled by several key factors: the rising adoption of cloud-based solutions, advancements in artificial intelligence (AI) and machine learning (ML), and the increasing demand for personalized customer experiences. Technological advancements, such as AI-driven predictive analytics and real-time customer journey mapping, are revolutionizing marketing strategies. Shifting consumer demands, particularly the preference for personalized and omnichannel experiences, are also driving the market's evolution. The forecast period (2025-2033) is expected to see continued growth, albeit at a slightly moderated pace, driven by factors such as increasing adoption rates in smaller businesses and continued technological innovations. The projected CAGR for the forecast period is xx%.

Leading Regions, Countries, or Segments in North America Marketing Automation Industry

The North American marketing automation market is geographically diverse, with significant variations in adoption rates and growth potential across different regions and segments.

By Application:

- Email Marketing: Remains the dominant application, driven by high ROI and effectiveness.

- Campaign Management: Growing rapidly due to the need for integrated and automated campaign execution.

- Digital Marketing: Significant growth driven by increasing digital advertising budgets and the need for efficient campaign tracking.

Key Drivers (across segments):

- Increased investments in digital transformation initiatives by enterprises.

- Government regulations promoting digital marketing and data privacy.

By End-user Industry:

- BFSI: High adoption due to the need for personalized customer experiences and efficient customer relationship management.

- Retail: Significant growth driven by the need for targeted marketing campaigns and improved customer retention.

- Healthcare: Adoption is increasing, fueled by the need for personalized patient engagement and improved operational efficiency.

Key Drivers (across industries):

- Growing competition and demand for enhanced customer engagement.

- Government initiatives promoting digital health and financial inclusion.

By Deployment:

- Cloud: The dominant deployment model due to scalability, cost-effectiveness, and ease of access.

- On-premise: Remains relevant for organizations with stringent security requirements and legacy systems.

Key Drivers (across deployment models):

- Cloud adoption driven by cost savings and scalability.

- On-premise solutions cater to security-sensitive industries.

North America Marketing Automation Industry Product Innovations

Recent product innovations include AI-powered features like predictive analytics, real-time campaign optimization, and personalized customer journeys. These advancements enable businesses to deliver highly targeted and relevant marketing messages, improving campaign performance and ROI. The integration of marketing automation platforms with CRM systems provides a holistic view of customer interactions, facilitating more effective customer relationship management. Unique selling propositions (USPs) include ease of use, advanced analytics dashboards, and seamless integration with other marketing tools.

Propelling Factors for North America Marketing Automation Industry Growth

Technological advancements, particularly in AI and machine learning, are key drivers. The increasing need for personalized customer experiences and omnichannel marketing strategies further fuels growth. Government regulations promoting digital marketing and data privacy play a supporting role. Moreover, economic factors like increased investment in digital transformation initiatives by enterprises contribute to market expansion.

Obstacles in the North America Marketing Automation Industry Market

The industry faces challenges such as high implementation costs and the need for skilled professionals. Data privacy concerns and regulatory compliance requirements create significant hurdles. Supply chain disruptions can also impact the availability of essential components or services. Intense competition from existing players and new entrants creates competitive pressure.

Future Opportunities in North America Marketing Automation Industry

Emerging opportunities include expanding into new markets like smaller businesses and integrating with emerging technologies like the metaverse. Advancements in AI and analytics promise improved targeting and personalization capabilities. Growing demand for customer experience (CX) solutions will further drive growth.

Major Players in the North America Marketing Automation Industry Ecosystem

Key Developments in North America Marketing Automation Industry Industry

- October 2022: DXC Technology expanded its partnership with Dynatrace, enhancing its ability to offer AI-powered automated IT management solutions. This strengthens the capabilities of marketing automation platforms in managing and optimizing IT infrastructure supporting marketing activities.

- January 2022: Datarati's acquisition by OSF Digital strengthens OSF Digital's position as a significant Salesforce multi-cloud solution provider, impacting the Salesforce marketing automation ecosystem.

Strategic North America Marketing Automation Industry Market Forecast

The North American marketing automation market is poised for continued growth, driven by technological advancements, increasing demand for personalized customer experiences, and expanding adoption across various industries. Opportunities lie in AI-driven innovation, integration with emerging technologies, and expansion into new market segments. The market's future trajectory is positive, with significant potential for continued expansion in the coming years.

North America Marketing Automation Industry Segmentation

-

1. Deployment

- 1.1. On-premise

- 1.2. Cloud

-

2. Application

- 2.1. Campaign Management

- 2.2. Social Media Marketing

- 2.3. Digital Marketing

- 2.4. E-mail Marketing

- 2.5. Mobile Marketing

- 2.6. Inbound Marketing

- 2.7. Other Applications

-

3. End-user Industry

- 3.1. Government

- 3.2. Advertising

- 3.3. Media and Entertainment

- 3.4. Retail

- 3.5. Manufacturing

- 3.6. BFSI

- 3.7. Healthcare

- 3.8. Other End-user Industries

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Rest of North America

North America Marketing Automation Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America Marketing Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 12.80% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Use of Social Media Platforms for Disseminating Information

- 3.2.2 Creating Brand Image

- 3.2.3 and Reaching Out to Followers; Increasing Adoption of Automation Tools in Retail Sector; Emergence of Large Numbers of Medium and Small Enterprises in Retail and E-commerce Sectors

- 3.3. Market Restrains

- 3.3.1. Intense Competition in the Market; Security Concerns and Presence of Open-Source and Freemium Marketing Tools

- 3.4. Market Trends

- 3.4.1. Increased Adoption of Automation Tools in the Retail Segment to Drive the Market's Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Marketing Automation Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. On-premise

- 5.1.2. Cloud

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Campaign Management

- 5.2.2. Social Media Marketing

- 5.2.3. Digital Marketing

- 5.2.4. E-mail Marketing

- 5.2.5. Mobile Marketing

- 5.2.6. Inbound Marketing

- 5.2.7. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Government

- 5.3.2. Advertising

- 5.3.3. Media and Entertainment

- 5.3.4. Retail

- 5.3.5. Manufacturing

- 5.3.6. BFSI

- 5.3.7. Healthcare

- 5.3.8. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest of North America

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. United States North America Marketing Automation Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. On-premise

- 6.1.2. Cloud

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Campaign Management

- 6.2.2. Social Media Marketing

- 6.2.3. Digital Marketing

- 6.2.4. E-mail Marketing

- 6.2.5. Mobile Marketing

- 6.2.6. Inbound Marketing

- 6.2.7. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Government

- 6.3.2. Advertising

- 6.3.3. Media and Entertainment

- 6.3.4. Retail

- 6.3.5. Manufacturing

- 6.3.6. BFSI

- 6.3.7. Healthcare

- 6.3.8. Other End-user Industries

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. Canada North America Marketing Automation Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. On-premise

- 7.1.2. Cloud

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Campaign Management

- 7.2.2. Social Media Marketing

- 7.2.3. Digital Marketing

- 7.2.4. E-mail Marketing

- 7.2.5. Mobile Marketing

- 7.2.6. Inbound Marketing

- 7.2.7. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Government

- 7.3.2. Advertising

- 7.3.3. Media and Entertainment

- 7.3.4. Retail

- 7.3.5. Manufacturing

- 7.3.6. BFSI

- 7.3.7. Healthcare

- 7.3.8. Other End-user Industries

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Rest of North America North America Marketing Automation Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. On-premise

- 8.1.2. Cloud

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Campaign Management

- 8.2.2. Social Media Marketing

- 8.2.3. Digital Marketing

- 8.2.4. E-mail Marketing

- 8.2.5. Mobile Marketing

- 8.2.6. Inbound Marketing

- 8.2.7. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Government

- 8.3.2. Advertising

- 8.3.3. Media and Entertainment

- 8.3.4. Retail

- 8.3.5. Manufacturing

- 8.3.6. BFSI

- 8.3.7. Healthcare

- 8.3.8. Other End-user Industries

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. United States North America Marketing Automation Industry Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America Marketing Automation Industry Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America Marketing Automation Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of North America North America Marketing Automation Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 HubSpot

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 IBM Corporation*List Not Exhaustive

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Adobe Inc

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Act-on Software

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Oracle Corporation

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Salesforce

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.1 HubSpot

List of Figures

- Figure 1: North America Marketing Automation Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Marketing Automation Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Marketing Automation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Marketing Automation Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 3: North America Marketing Automation Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: North America Marketing Automation Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 5: North America Marketing Automation Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 6: North America Marketing Automation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: North America Marketing Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: United States North America Marketing Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Canada North America Marketing Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Mexico North America Marketing Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Rest of North America North America Marketing Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: North America Marketing Automation Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 13: North America Marketing Automation Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 14: North America Marketing Automation Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 15: North America Marketing Automation Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 16: North America Marketing Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: North America Marketing Automation Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 18: North America Marketing Automation Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 19: North America Marketing Automation Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 20: North America Marketing Automation Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 21: North America Marketing Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: North America Marketing Automation Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 23: North America Marketing Automation Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 24: North America Marketing Automation Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 25: North America Marketing Automation Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: North America Marketing Automation Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Marketing Automation Industry?

The projected CAGR is approximately 12.80%.

2. Which companies are prominent players in the North America Marketing Automation Industry?

Key companies in the market include HubSpot, IBM Corporation*List Not Exhaustive, Adobe Inc, Act-on Software, Oracle Corporation, Salesforce.

3. What are the main segments of the North America Marketing Automation Industry?

The market segments include Deployment, Application, End-user Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Use of Social Media Platforms for Disseminating Information. Creating Brand Image. and Reaching Out to Followers; Increasing Adoption of Automation Tools in Retail Sector; Emergence of Large Numbers of Medium and Small Enterprises in Retail and E-commerce Sectors.

6. What are the notable trends driving market growth?

Increased Adoption of Automation Tools in the Retail Segment to Drive the Market's Growth.

7. Are there any restraints impacting market growth?

Intense Competition in the Market; Security Concerns and Presence of Open-Source and Freemium Marketing Tools.

8. Can you provide examples of recent developments in the market?

October 2022: DXC Technology, one of the leading global technology service providers, announced an expanded partnership with Dynatrace. The Dynatrace Software Intelligence Platform will be the preferred DXC Platform X software for observability and AI-powered automated management of a customer's IT estate. At the same time, the platform is always evolving to provide DXC clients with best-in-class solutions that meet their rapidly changing technological demands and assist them in becoming future-ready with the ability to accomplish their desired business outcomes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Marketing Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Marketing Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Marketing Automation Industry?

To stay informed about further developments, trends, and reports in the North America Marketing Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence