Key Insights

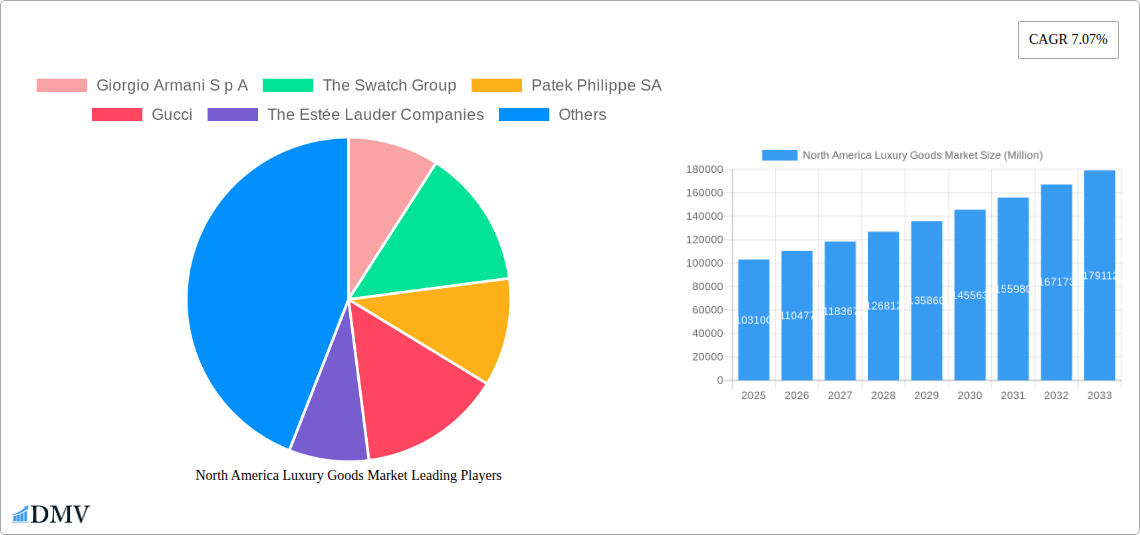

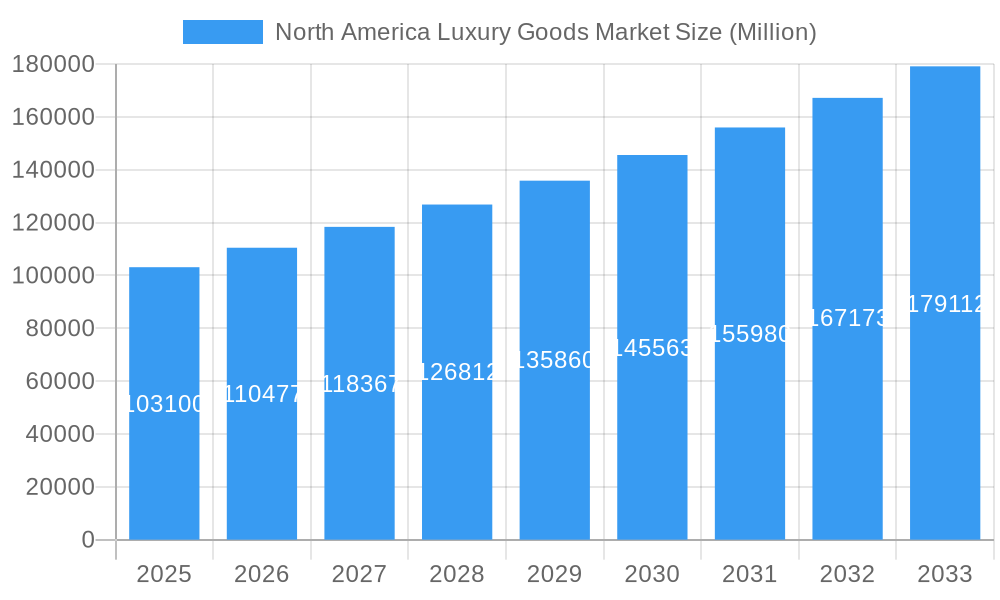

The North American luxury goods market, valued at $103.10 billion in 2025, is projected to experience robust growth, with a compound annual growth rate (CAGR) of 7.07% from 2025 to 2033. This expansion is driven by several key factors. Firstly, a rising affluent population, particularly millennials and Gen Z, with increased disposable income and a penchant for luxury brands, fuels demand. Secondly, the burgeoning e-commerce sector provides convenient access to luxury goods, broadening the market reach beyond traditional brick-and-mortar stores. Thirdly, strategic brand collaborations and marketing campaigns, leveraging social media and influencer marketing, create significant brand awareness and desire among target demographics. Finally, the continuous innovation in product design and technology integration within luxury goods enhances consumer experience and drives sales. The market is segmented across various distribution channels (single-branded stores, multi-brand stores, online stores), product types (clothing & apparel, footwear, bags, jewelry, watches), and countries within North America (United States, Canada, Mexico). Competition within this market is intense, with prominent players like LVMH, Kering, Richemont, and others vying for market share through product diversification, expansion into new markets, and strategic acquisitions.

North America Luxury Goods Market Market Size (In Billion)

The growth trajectory is, however, subject to certain restraints. Economic fluctuations, particularly recessions, can impact consumer spending on luxury goods. Geopolitical instability and supply chain disruptions also pose challenges. Furthermore, increasing concerns about sustainability and ethical sourcing are influencing consumer purchasing decisions, compelling luxury brands to adopt more responsible practices. The market's future success will depend on brands' ability to adapt to these evolving consumer preferences, manage supply chain complexities, and effectively leverage digital channels to reach a growing and discerning customer base. Growth within the North American market will likely be led by the United States, given its larger population and higher concentration of affluent consumers, followed by Canada and Mexico, reflecting their respective economic conditions and consumer trends. The segments with the highest growth potential are likely to be online stores (due to expanding e-commerce) and experiences and services related to luxury goods (personal styling, bespoke items).

North America Luxury Goods Market Company Market Share

North America Luxury Goods Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the North America luxury goods market, offering a comprehensive overview of its current state, future trajectory, and key players. The study period covers 2019-2033, with 2025 serving as the base and estimated year. The forecast period spans 2025-2033, and historical data encompasses 2019-2024. The market is segmented by distribution channel (single-branded stores, multi-brand stores, online stores, other), country (United States, Canada, Mexico, Rest of North America), and product type (clothing and apparel, footwear, bags, jewelry, watches, other). Key players include LVMH Moët Hennessy Louis Vuitton, Hermès International S A, Kering Group, Rolex SA, Richemont, The Estée Lauder Companies, Gucci, Patek Philippe SA, The Swatch Group, and Giorgio Armani S p A. This report is crucial for stakeholders seeking to understand and capitalize on opportunities within this dynamic and lucrative market. The market size in 2025 is estimated at xx Million.

North America Luxury Goods Market Market Composition & Trends

The North American luxury goods market is characterized by a dynamic interplay of concentrated market leadership, relentless innovation, and evolving consumer behaviors. The dominance of key players like LVMH, Kering, and Richemont continues to shape the competitive landscape, with their collective market share representing a significant portion of the industry. Projections for 2025 indicate a continued stronghold for these giants, alongside a growing segment for other luxury brands. Innovation remains a critical differentiator, fueled by cutting-edge advancements in sustainable materials, sophisticated design aesthetics, and highly personalized product offerings. The regulatory environment is increasingly emphasizing environmental responsibility and ethical sourcing, pushing brands towards more conscious business practices. While substitute products from more accessible brands present an ongoing competitive challenge, the resilience of the luxury sector is underscored by its sustained growth trajectory. The end-user profile is becoming increasingly diverse, reflecting shifts in demographics, evolving cultural influences, and a broader spectrum of consumer preferences. Mergers and acquisitions (M&A) remain a pivotal strategy for market consolidation and expansion, with recent deal values in 2022 highlighting active industry restructuring.

- Market Concentration: The market is highly concentrated, with a few dominant global luxury conglomerates holding substantial market share, driving significant industry trends and investment.

- Innovation Catalysts: Technological advancements are at the forefront, driving innovation in novel materials, avant-garde design, and deeply personalized product experiences that resonate with discerning consumers.

- Regulatory Landscape: A growing emphasis on sustainability, circular economy principles, and ethical sourcing is shaping brand strategies and consumer purchasing decisions.

- Substitute Products: The market continually navigates competitive pressure from accessible luxury and premium brands, necessitating a strong focus on brand differentiation and value proposition.

- End-User Profiles: The luxury consumer base is expanding and diversifying, encompassing a wider range of age groups, cultural backgrounds, and lifestyle preferences.

- M&A Activities: Significant merger and acquisition activity continues to shape the market, indicating strategic moves for portfolio expansion, market penetration, and enhanced competitive positioning.

North America Luxury Goods Market Industry Evolution

The North America luxury goods market has experienced consistent growth over the historical period (2019-2024), with an average annual growth rate (AAGR) of xx%. This growth is fueled by several factors: rising disposable incomes among high-net-worth individuals, increasing demand for luxury experiences, and the growing influence of social media in shaping consumer preferences. Technological advancements, such as personalized marketing campaigns and augmented reality (AR) experiences, are enhancing brand engagement. Furthermore, changing consumer demands, including a shift towards sustainable and ethically sourced products, present both challenges and opportunities for the industry. The market is projected to maintain a robust growth trajectory in the forecast period (2025-2033), with an anticipated AAGR of xx%, driven by the factors discussed above, as well as new innovations and the entry of new consumer segments. The adoption rate of luxury goods, driven by increased brand awareness, is increasing year-on-year.

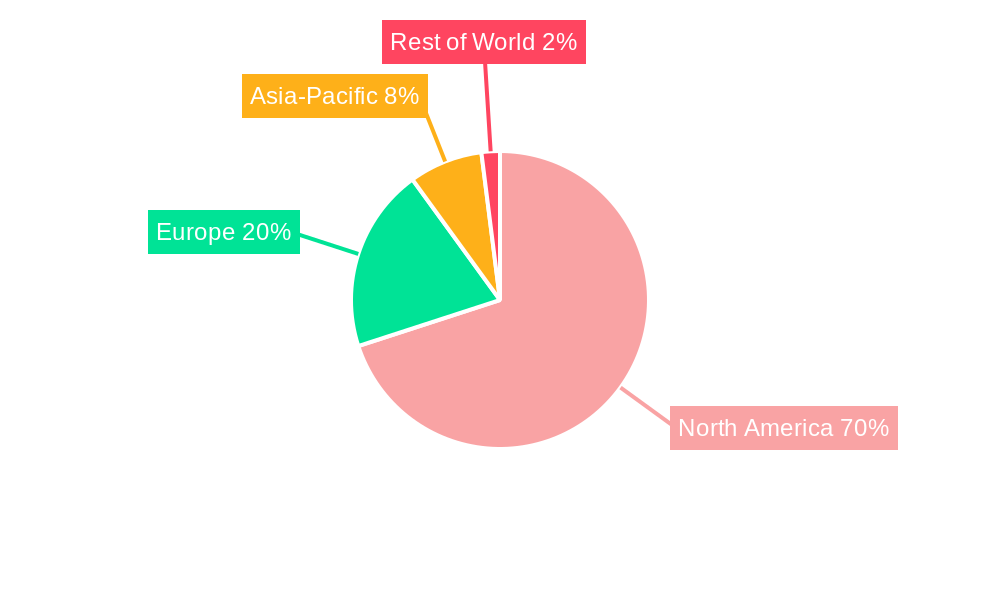

Leading Regions, Countries, or Segments in North America Luxury Goods Market

The United States unequivocally leads the North American luxury goods market, commanding the largest share of revenue and demonstrating robust growth momentum. This preeminence is attributable to a confluence of factors: a substantial and growing affluent consumer base, a generally stable and prosperous economic environment, and a highly developed infrastructure for luxury retail, encompassing flagship stores, high-end department stores, and exclusive boutiques.

- By Country:

- United States: The primary engine of growth, driven by a significant concentration of high-net-worth individuals, strong consumer confidence, and a vibrant luxury retail ecosystem.

- Canada: A developing market characterized by consistent expansion, supported by rising disposable incomes and an increasing appetite for premium products.

- Mexico: A market with considerable untapped potential, benefiting from a growing tourism sector and an expanding middle class with increasing purchasing power for luxury goods.

- Rest of North America: While currently representing a smaller market share, these regions offer nascent opportunities for growth with strategic brand entry and targeted marketing efforts.

- By Distribution Channel:

- Single-branded Stores: Remain the dominant channel, offering an immersive and controlled brand experience, exceptional customer service, and direct access to the latest collections.

- Multi-brand Stores: Continue to play a significant role, providing curated selections from various luxury houses, though facing increasing competition from direct-to-consumer channels and e-commerce.

- Online Stores: Exhibiting rapid and substantial growth, these channels offer unparalleled convenience, global reach, and personalized digital experiences, becoming indispensable for luxury brands.

- Other Distribution Channels: Including pop-up activations, exclusive private sales, and strategic wholesale partnerships, these channels contribute to brand visibility and reach niche consumer segments.

- By Type:

- Watches & Jewelry: A high-value and consistently growing segment, driven by the enduring appeal of craftsmanship, exclusivity, unique collections, and the perception of investment value.

- Clothing & Apparel: A foundational segment with strong brand recognition and a core consumer base, constantly evolving with seasonal collections and designer collaborations.

- Bags: A perennial favorite in the luxury market, characterized by high demand for iconic and artisanal pieces, ensuring consistent sales and strong brand loyalty.

- Footwear: A segment that thrives on brand-specific innovation, collaborations, and the integration of fashion-forward designs with comfort and quality, maintaining steady sales performance.

North America Luxury Goods Market Product Innovations

Product innovation in the North American luxury goods market is increasingly centered around three pivotal pillars: enhanced sustainability, deeply personalized customer experiences, and seamless technological integration. Brands are actively incorporating recycled and ethically sourced materials, championing circularity, and exploring biodegradable alternatives. The demand for bespoke and customizable products is soaring, with brands offering intricate personalization options, from monogramming to made-to-measure services. Furthermore, digital technologies, including Augmented Reality (AR) and Virtual Reality (VR), are being leveraged to create immersive virtual try-ons, exclusive digital showrooms, and engaging storytelling for enhanced customer interaction. Unique selling propositions are built upon rich brand heritage, unparalleled craftsmanship, and exclusive, often limited-edition, designs that amplify desirability and exclusivity. Advances in material science and sophisticated production techniques are enabling the creation of products that are not only aesthetically superior but also more durable, lightweight, and environmentally conscious.

Propelling Factors for North America Luxury Goods Market Growth

The robust growth of the North American luxury goods market is propelled by a confluence of powerful economic and social drivers. A significant increase in disposable incomes among high-net-worth individuals and affluent consumers forms the bedrock of sustained demand. Beyond tangible goods, there is a pronounced shift towards the consumption of luxury experiences, encompassing high-end travel, bespoke services, and exclusive events, thereby broadening the market's scope. Technological advancements are playing a crucial role in transforming how brands connect with consumers, through sophisticated digital marketing strategies, engaging e-commerce platforms, and innovative product design. Favorable and resilient economic conditions, particularly within the United States, foster a climate of consumer confidence that directly translates into continued robust spending on luxury items. The aspirational appeal of luxury brands, coupled with a growing emphasis on self-expression and quality, further fuels this expansion.

Obstacles in the North America Luxury Goods Market Market

Several obstacles hinder market growth. Economic downturns can significantly impact consumer spending on luxury goods. Supply chain disruptions and increased production costs can affect profitability and product availability. Intense competition among established brands and the rise of new entrants present challenges. Regulatory changes impacting import/export and ethical sourcing also add complexity.

Future Opportunities in North America Luxury Goods Market

Future growth lies in several promising areas. Targeting new consumer segments, such as millennials and Gen Z, with digitally-driven marketing and product offerings presents immense potential. Expansion into new markets within North America, especially in emerging affluent communities, holds promise. The adoption of new technologies, such as AI-powered personalization and blockchain for authenticity verification, will reshape the industry landscape. Furthermore, expanding into the pre-owned luxury goods market can increase revenue streams.

Major Players in the North America Luxury Goods Market Ecosystem

Key Developments in North America Luxury Goods Market Industry

- September 2022: Hermès inaugurated a monumental flagship store in New York City, significantly amplifying its brand presence and reinforcing its commitment to the North American market with an enhanced retail experience.

- July 2022: Louis Vuitton strategically expanded its US retail footprint by opening its inaugural men's store in California, catering to a growing male demographic and showcasing its specialized offerings.

- March 2022: Kering Eyewear made a strategic acquisition of Maui Jim, bolstering its portfolio and strengthening its competitive position within the lucrative and expanding luxury eyewear segment.

Strategic North America Luxury Goods Market Market Forecast

The North America luxury goods market is poised for continued growth driven by a confluence of factors: increasing affluence, evolving consumer preferences, technological advancements, and strategic investments by major players. The market is expected to witness robust expansion in the coming years, driven by the factors analyzed throughout this report. Opportunities lie in personalization, sustainable practices, and innovative product offerings that cater to diverse consumer segments. A targeted approach combining digital marketing and traditional luxury retail experiences will be crucial for success.

North America Luxury Goods Market Segmentation

-

1. Type

- 1.1. Clothing and Apparel

- 1.2. Footwear

- 1.3. Bags

- 1.4. Jewelry

- 1.5. Watches

- 1.6. Other Types

-

2. Distribution Channel

- 2.1. Single-branded Stores

- 2.2. Multi-brand Stores

- 2.3. Online Stores

- 2.4. Other Distribution Channels

North America Luxury Goods Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Luxury Goods Market Regional Market Share

Geographic Coverage of North America Luxury Goods Market

North America Luxury Goods Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.07% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Clothing and Apparel

- 5.1.2. Footwear

- 5.1.3. Bags

- 5.1.4. Jewelry

- 5.1.5. Watches

- 5.1.6. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Single-branded Stores

- 5.2.2. Multi-brand Stores

- 5.2.3. Online Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Luxury Goods Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Clothing and Apparel

- 6.1.2. Footwear

- 6.1.3. Bags

- 6.1.4. Jewelry

- 6.1.5. Watches

- 6.1.6. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Single-branded Stores

- 6.2.2. Multi-brand Stores

- 6.2.3. Online Stores

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Giorgio Armani S p A

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 The Swatch Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Patek Philippe SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Gucci

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 The Estée Lauder Companies

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Richemont*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Rolex SA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Kering Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Hermès International S A

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 LVMH Moët Hennessy Louis Vuitton

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Giorgio Armani S p A

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Luxury Goods Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Luxury Goods Market Share (%) by Company 2025

List of Tables

- Table 1: North America Luxury Goods Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: North America Luxury Goods Market Volume K Units Forecast, by Type 2020 & 2033

- Table 3: North America Luxury Goods Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: North America Luxury Goods Market Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 5: North America Luxury Goods Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: North America Luxury Goods Market Volume K Units Forecast, by Region 2020 & 2033

- Table 7: North America Luxury Goods Market Revenue Million Forecast, by Type 2020 & 2033

- Table 8: North America Luxury Goods Market Volume K Units Forecast, by Type 2020 & 2033

- Table 9: North America Luxury Goods Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 10: North America Luxury Goods Market Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 11: North America Luxury Goods Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: North America Luxury Goods Market Volume K Units Forecast, by Country 2020 & 2033

- Table 13: United States North America Luxury Goods Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States North America Luxury Goods Market Volume (K Units) Forecast, by Application 2020 & 2033

- Table 15: Canada North America Luxury Goods Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada North America Luxury Goods Market Volume (K Units) Forecast, by Application 2020 & 2033

- Table 17: Mexico North America Luxury Goods Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico North America Luxury Goods Market Volume (K Units) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Luxury Goods Market?

The projected CAGR is approximately 7.07%.

2. Which companies are prominent players in the North America Luxury Goods Market?

Key companies in the market include Giorgio Armani S p A, The Swatch Group, Patek Philippe SA, Gucci, The Estée Lauder Companies, Richemont*List Not Exhaustive, Rolex SA, Kering Group, Hermès International S A, LVMH Moët Hennessy Louis Vuitton.

3. What are the main segments of the North America Luxury Goods Market?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 103.10 Million as of 2022.

5. What are some drivers contributing to market growth?

Demand for Smartwatches; Popularity of Luxury Watches.

6. What are the notable trends driving market growth?

Rising Number of High-Net-Worth Individuals in the Region.

7. Are there any restraints impacting market growth?

Presence of Fake Brands in the Market.

8. Can you provide examples of recent developments in the market?

In September 2022, at 706 Madison Avenue in the tony shopping corridor of New York, Hermès opened one of its largest flagship stores in the world.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Luxury Goods Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Luxury Goods Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Luxury Goods Market?

To stay informed about further developments, trends, and reports in the North America Luxury Goods Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence