Key Insights

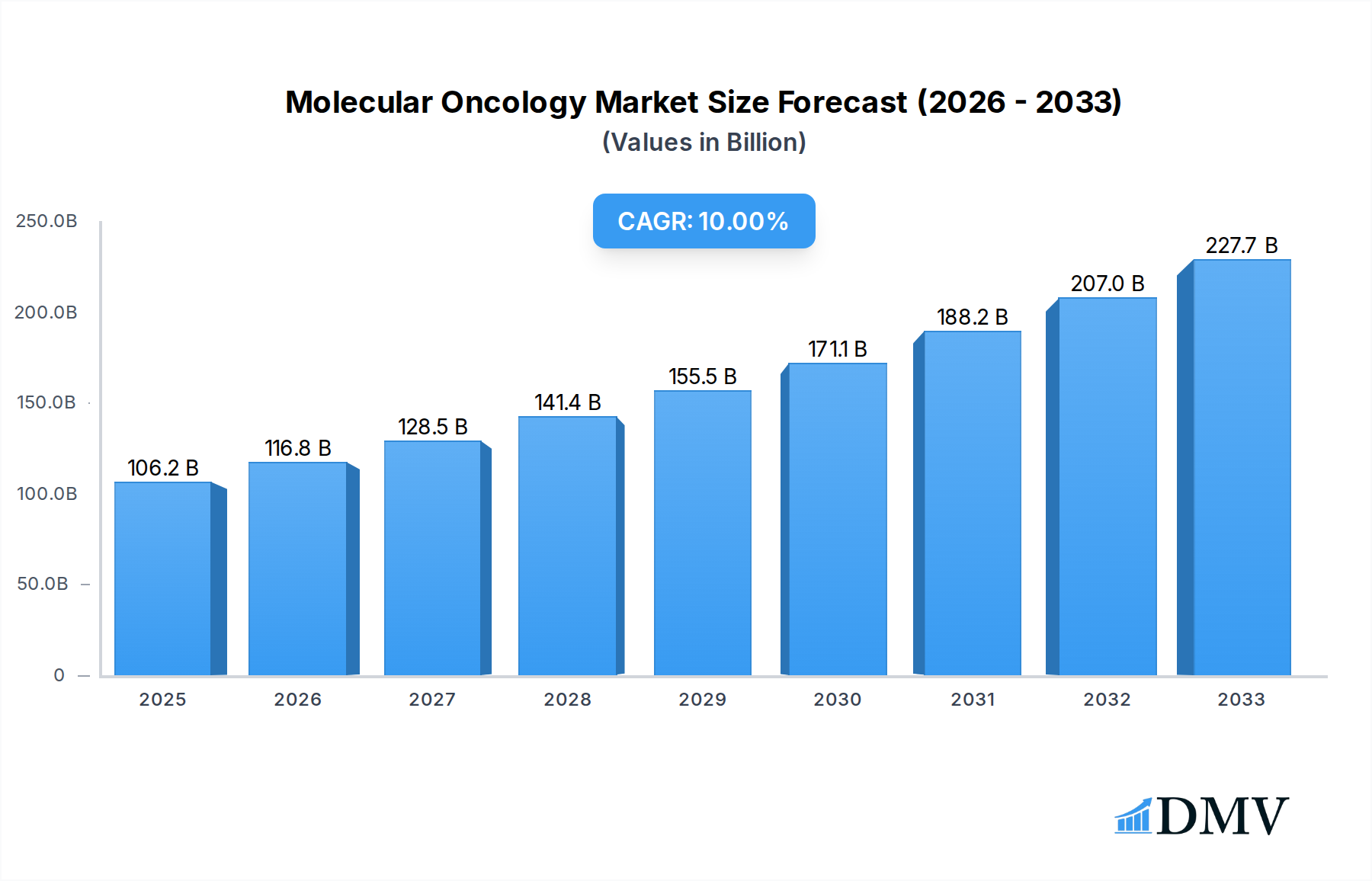

The Molecular Oncology market is poised for substantial expansion, projected to reach an estimated $106.21 billion by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 11% through 2033. This significant growth is fueled by an escalating demand for personalized cancer therapies, driven by advancements in genetic sequencing technologies and a deeper understanding of tumor biology. The increasing prevalence of cancer globally, coupled with a growing emphasis on early detection and targeted treatment strategies, further propels market momentum. Key applications within hospitals and clinics, diagnostic laboratories, and specialized cancer centers are witnessing heightened adoption of molecular diagnostics for precise patient stratification and treatment selection. Innovations in Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), Microarray, and Fluorescence In Situ Hybridization (FISH) are central to this progress, offering enhanced accuracy and efficiency in identifying actionable genetic mutations. The market is also benefiting from supportive government initiatives and rising healthcare expenditure in emerging economies, fostering a more accessible and widespread use of molecular oncology tools.

Molecular Oncology Market Size (In Billion)

Despite the promising outlook, certain factors could present challenges. The high cost associated with advanced molecular diagnostic platforms and associated reagents may limit uptake in resource-constrained settings. Furthermore, the need for skilled personnel to operate and interpret complex molecular data necessitates continuous training and development within the healthcare workforce. Regulatory hurdles and the evolving landscape of reimbursement policies for novel diagnostic tests can also introduce complexities. Nevertheless, the transformative impact of molecular oncology in improving patient outcomes, enabling the development of novel targeted therapies, and contributing to the burgeoning field of precision medicine is undeniable. Major players like Roche Diagnostics, Thermo Fisher Scientific, and Illumina are at the forefront, investing heavily in research and development to introduce innovative solutions and expand their market reach, thereby shaping the future of cancer care.

Molecular Oncology Company Market Share

This in-depth Molecular Oncology market report provides a definitive analysis of the global landscape, offering critical insights for stakeholders in the cancer diagnostics, genomics, and precision medicine sectors. Covering the period from 2019 to 2033, with a base year of 2025, this report delves into market composition, industry evolution, regional dominance, product innovations, growth drivers, obstacles, and future opportunities. Discover the strategic imperative for companies operating within the rapidly expanding oncology diagnostics market, driven by advancements in Next Generation Sequencing (NGS), PCR, and biomarker discovery. We project a robust market size exceeding billions, fueled by increasing cancer incidence and the growing demand for personalized treatment strategies. This report is essential for investors, research institutions, and pharmaceutical companies seeking to capitalize on the burgeoning molecular diagnostics sector.

Molecular Oncology Market Composition & Trends

The molecular oncology market is characterized by a dynamic interplay of innovation, evolving regulatory frameworks, and increasing end-user sophistication. Market concentration is influenced by the strategic acquisitions and partnerships among key players. Innovation catalysts include breakthroughs in liquid biopsy, companion diagnostics, and advanced bioinformatics. Regulatory landscapes, such as those governed by the FDA and EMA, are continuously adapting to ensure the efficacy and safety of novel oncology tests. Substitute products, while emerging, often struggle to match the precision and comprehensiveness offered by advanced molecular techniques. End-user profiles span hospitals and clinics, diagnostic laboratories, and specialized cancer centers, each with distinct needs and adoption rates for molecular oncology solutions. Mergers and acquisitions (M&A) are actively reshaping the market, with deal values reaching billions, indicating strong investor confidence. For instance, M&A activities are estimated to account for over 50 billion in deal value within the last five years. Market share distribution is highly competitive, with leading companies vying for dominance in key segments.

- Market Concentration Drivers:

- High R&D investment requirements for genomic sequencing technologies.

- Intellectual property protection for novel biomarkers and diagnostic assays.

- Strategic alliances to expand testing capabilities and market reach.

- Innovation Catalysts:

- Advancements in AI-powered data analysis for genomic interpretation.

- Development of multiplex assays for simultaneous detection of multiple cancer mutations.

- Increased clinical validation of theranostic approaches.

- Regulatory Landscape:

- Stringent approval processes for in vitro diagnostics (IVDs).

- Focus on data privacy and security in genomic data management.

- Reimbursement policies influencing adoption of molecular diagnostic tests.

- End-User Profiles:

- Hospitals and Clinics: Demand for rapid, actionable diagnostic information for patient management.

- Diagnostic Laboratories: Focus on high-throughput testing and expanding test menus.

- Cancer Centers and Specialty Clinics: Need for comprehensive genomic profiling for personalized therapy selection.

- M&A Activities:

- Consolidation to gain access to new technologies and customer bases.

- Acquisitions aimed at strengthening portfolios in oncology diagnostics.

- Estimated deal values in the billions reflecting market growth potential.

Molecular Oncology Industry Evolution

The molecular oncology industry has undergone a remarkable transformation, evolving from nascent research initiatives to a cornerstone of modern cancer care. The historical period (2019-2024) witnessed a surge in the adoption of Next Generation Sequencing (NGS), driven by its ability to provide comprehensive genomic insights that were previously unattainable. This period saw significant growth in the development and clinical application of PCR-based tests for targeted gene mutations, offering faster turnaround times for specific diagnostic needs. The market growth trajectory has been consistently upward, with an estimated compound annual growth rate (CAGR) of over 15% during the historical period. Technological advancements have been the primary engine of this evolution, with continuous improvements in sequencing accuracy, speed, and cost-effectiveness. The adoption of NGS in routine clinical practice has dramatically increased, moving from specialized academic centers to widespread use in diagnostic laboratories and hospitals. Consumer demand has shifted considerably, with patients and clinicians increasingly recognizing the value of personalized medicine. This has translated into a greater demand for molecular diagnostic tests that can guide treatment decisions, predict prognosis, and monitor treatment response. The estimated market size is projected to reach over 100 billion by 2025, with a further expansion to over 250 billion by the end of the forecast period (2033). This growth is underpinned by robust investment in R&D by leading companies and increasing healthcare expenditure globally dedicated to oncology. The shift towards precision oncology has democratized access to advanced diagnostics, making them more accessible and integrated into the patient journey.

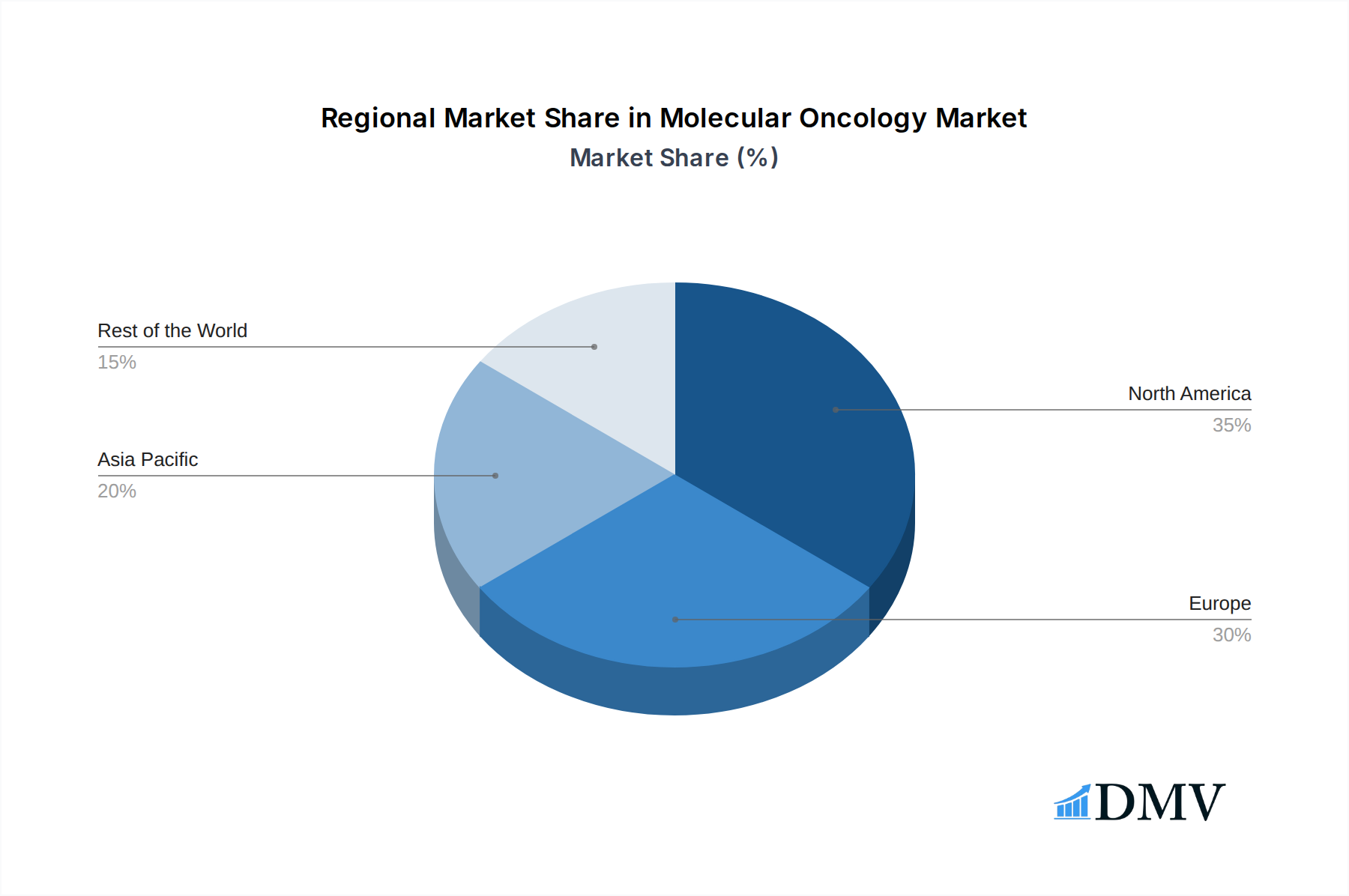

Leading Regions, Countries, or Segments in Molecular Oncology

North America currently stands as the dominant region in the molecular oncology market, driven by a confluence of factors including high healthcare expenditure, advanced research infrastructure, early adoption of novel technologies, and a robust regulatory environment that supports innovation. The United States, in particular, leads in the implementation of NGS (Next Generation Sequencing) for cancer diagnostics and treatment selection.

Dominant Application Segment:

- Hospitals and Clinics: This segment is paramount due to the direct integration of molecular oncology testing into patient care pathways. Clinicians leverage these tests for diagnosis, prognosis, and to guide therapeutic interventions, especially in oncology. The increasing complexity of cancer treatment protocols necessitates rapid and accurate molecular insights, making hospitals and clinics the primary consumers of these advanced diagnostic services. Investments in on-site laboratory capabilities and partnerships with specialized diagnostic providers further solidify their leading position.

Dominant Type Segment:

- NGS (Next Generation Sequencing): While PCR remains a crucial and widely used technology for targeted genetic analysis, NGS has emerged as the most impactful and rapidly growing segment. Its ability to perform comprehensive genomic profiling, identify complex genomic rearrangements, and detect a broad spectrum of biomarkers in a single test makes it indispensable for understanding tumor heterogeneity and developing personalized treatment strategies. The declining cost and increasing throughput of NGS platforms have further accelerated its adoption in both research and clinical settings, positioning it as the future of cancer diagnostics.

Key Drivers of Dominance:

- Investment Trends: Significant venture capital and pharmaceutical investment in genomic research and oncology diagnostics within North America.

- Regulatory Support: Favorable regulatory pathways from agencies like the FDA that expedite the approval of innovative molecular oncology tests.

- Technological Adoption: High uptake rates of cutting-edge technologies such as NGS and liquid biopsy driven by research institutions and leading healthcare providers.

- Cancer Incidence and Awareness: High prevalence of various cancers coupled with heightened public and physician awareness regarding the benefits of precision medicine.

- Reimbursement Policies: Well-established reimbursement frameworks that facilitate the coverage of molecular diagnostic tests, making them accessible to a broader patient population.

The strategic importance of these segments underscores the evolving landscape of cancer care, where molecular insights are no longer an adjunct but a critical component of effective treatment.

Molecular Oncology Product Innovations

Molecular oncology is experiencing a rapid influx of innovative products that are revolutionizing cancer diagnosis and treatment. These innovations include advanced NGS panels designed for comprehensive tumor profiling, identifying actionable mutations, gene fusions, and copy number variations with unprecedented accuracy. Liquid biopsy technologies are gaining significant traction, offering non-invasive methods to detect circulating tumor DNA (ctDNA) for early cancer detection, monitoring treatment response, and detecting resistance mechanisms. Furthermore, multiplex PCR assays continue to evolve, providing faster and more specific detection of key oncogenic drivers. The performance metrics of these new products are marked by improved sensitivity, specificity, and reduced turnaround times, enabling clinicians to make timely and informed decisions. Unique selling propositions often lie in the integration of advanced bioinformatics and AI-powered analytics, which enhance the interpretation of complex genomic data, providing deeper biological insights and clinically relevant recommendations for precision oncology.

Propelling Factors for Molecular Oncology Growth

The molecular oncology market is propelled by a confluence of powerful forces, primarily driven by technological advancements, economic imperatives, and supportive regulatory environments. The relentless progress in genomic sequencing technologies, particularly NGS, has dramatically reduced costs and increased throughput, making comprehensive cancer diagnostics more accessible. Economic factors, including rising healthcare expenditure dedicated to oncology and the long-term cost-effectiveness of early and accurate diagnosis in reducing treatment burdens, further fuel growth. Regulatory bodies are increasingly streamlining approval processes for companion diagnostics and novel molecular tests, recognizing their critical role in precision medicine. The growing prevalence of cancer worldwide and increasing patient and physician demand for personalized treatment strategies are also significant accelerators, creating a robust market for advanced oncology solutions.

Obstacles in the Molecular Oncology Market

Despite its promising trajectory, the molecular oncology market faces several significant obstacles. Regulatory challenges, particularly the lengthy and complex approval processes for novel diagnostic assays, can hinder market entry and slow the adoption of groundbreaking technologies. Supply chain disruptions, exacerbated by global events, can impact the availability of critical reagents and equipment necessary for molecular testing. Competitive pressures from both established players and emerging startups intensify, driving down prices and requiring continuous innovation to maintain market share. Furthermore, the high cost of some advanced molecular diagnostic tests can be a barrier to access for certain patient populations and healthcare systems, particularly in resource-limited settings. The integration of complex genomic data into routine clinical workflows also presents an operational challenge, requiring specialized expertise and infrastructure.

Future Opportunities in Molecular Oncology

The molecular oncology market is ripe with emerging opportunities poised to redefine cancer care. The expansion of liquid biopsy applications into early cancer screening and minimal residual disease (MRD) detection presents a significant growth avenue. Advancements in AI and machine learning offer unparalleled potential for sophisticated genomic data analysis, prediction of treatment response, and drug discovery. The growing emphasis on theranostics, which combines diagnostic and therapeutic components, creates new avenues for integrated treatment approaches. Furthermore, the increasing penetration of molecular diagnostics in emerging markets, coupled with the development of more affordable and accessible testing solutions, opens up vast untapped potential. The ongoing exploration of the tumor microenvironment and the development of tests for immune profiling will also be crucial in the future of precision oncology.

Major Players in the Molecular Oncology Ecosystem

- Roche Diagnostics

- Thermo Fisher Scientific Inc.

- Illumina, Inc.

- Qiagen N.V.

- Agilent Technologies, Inc.

- Abbott Laboratories

- Bio-Rad Laboratories, Inc.

- Myriad Genetics, Inc.

- Genomic Health, Inc.

Key Developments in Molecular Oncology Industry

- 2023: Launch of novel NGS panels for comprehensive profiling of rare cancers, significantly improving diagnostic yield.

- 2023: Increased regulatory approvals for liquid biopsy tests for monitoring treatment efficacy in metastatic cancers.

- 2024: Strategic acquisition of a leading AI-powered bioinformatics company by a major diagnostic player to enhance data interpretation capabilities.

- 2024: Significant advancements in CRISPR-based diagnostic tools showing promise for high-throughput screening of genetic mutations.

- 2024: Expansion of companion diagnostic approvals for new targeted therapies, driving demand for specific molecular tests.

- 2025: Anticipated introduction of multi-cancer early detection (MCED) tests with enhanced accuracy and broader applicability.

- 2025: Growing adoption of digital pathology integrated with genomic data for more holistic cancer assessment.

- 2026: Further reduction in NGS sequencing costs expected to make whole-genome sequencing more feasible for routine oncology.

- 2027: Development of next-generation theranostic agents that combine imaging and therapeutic functionalities guided by molecular profiles.

- 2028: Increased focus on pharmacogenomic testing to optimize drug selection and dosage, minimizing adverse drug reactions.

- 2029: Global rollout of standardized molecular oncology testing protocols across major healthcare systems.

- 2030: Breakthroughs in understanding and targeting the tumor microenvironment leading to new diagnostic and therapeutic strategies.

- 2031: Widespread use of AI algorithms for predictive diagnostics and personalized treatment recommendations in oncology.

- 2032: Advancement of portable and rapid molecular diagnostic devices for point-of-care testing in remote areas.

- 2033: Maturation of the molecular oncology market with highly integrated, multi-omic approaches to cancer management.

Strategic Molecular Oncology Market Forecast

The molecular oncology market is poised for exceptional growth, driven by relentless innovation in genomic technologies and an increasing global imperative for personalized cancer care. Future opportunities are abundant in the expansion of liquid biopsy for early detection and MRD monitoring, coupled with the transformative potential of AI in genomic data analysis. The increasing focus on theranostics and the growing penetration of advanced molecular diagnostics in emerging markets will further amplify market potential. As technological advancements continue to reduce costs and improve accessibility, the market is projected to achieve substantial expansion, offering significant returns for stakeholders invested in the future of precision oncology.

Molecular Oncology Segmentation

-

1. Application

- 1.1. Hospitals and Clinics

- 1.2. Diagnostic Laboratories

- 1.3. Cancer Centers and Specialty Clinics

- 1.4. Others

-

2. Type

- 2.1. PCR

- 2.2. NGS (Next Generation Sequencing)

- 2.3. Microarray

- 2.4. FISH (Fluorescent in situ-hybridization)

- 2.5. Others

Molecular Oncology Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Molecular Oncology Regional Market Share

Geographic Coverage of Molecular Oncology

Molecular Oncology REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals and Clinics

- 5.1.2. Diagnostic Laboratories

- 5.1.3. Cancer Centers and Specialty Clinics

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. PCR

- 5.2.2. NGS (Next Generation Sequencing)

- 5.2.3. Microarray

- 5.2.4. FISH (Fluorescent in situ-hybridization)

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Molecular Oncology Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals and Clinics

- 6.1.2. Diagnostic Laboratories

- 6.1.3. Cancer Centers and Specialty Clinics

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. PCR

- 6.2.2. NGS (Next Generation Sequencing)

- 6.2.3. Microarray

- 6.2.4. FISH (Fluorescent in situ-hybridization)

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Molecular Oncology Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals and Clinics

- 7.1.2. Diagnostic Laboratories

- 7.1.3. Cancer Centers and Specialty Clinics

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. PCR

- 7.2.2. NGS (Next Generation Sequencing)

- 7.2.3. Microarray

- 7.2.4. FISH (Fluorescent in situ-hybridization)

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Molecular Oncology Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals and Clinics

- 8.1.2. Diagnostic Laboratories

- 8.1.3. Cancer Centers and Specialty Clinics

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. PCR

- 8.2.2. NGS (Next Generation Sequencing)

- 8.2.3. Microarray

- 8.2.4. FISH (Fluorescent in situ-hybridization)

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Molecular Oncology Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals and Clinics

- 9.1.2. Diagnostic Laboratories

- 9.1.3. Cancer Centers and Specialty Clinics

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. PCR

- 9.2.2. NGS (Next Generation Sequencing)

- 9.2.3. Microarray

- 9.2.4. FISH (Fluorescent in situ-hybridization)

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Molecular Oncology Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals and Clinics

- 10.1.2. Diagnostic Laboratories

- 10.1.3. Cancer Centers and Specialty Clinics

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. PCR

- 10.2.2. NGS (Next Generation Sequencing)

- 10.2.3. Microarray

- 10.2.4. FISH (Fluorescent in situ-hybridization)

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Molecular Oncology Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals and Clinics

- 11.1.2. Diagnostic Laboratories

- 11.1.3. Cancer Centers and Specialty Clinics

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. PCR

- 11.2.2. NGS (Next Generation Sequencing)

- 11.2.3. Microarray

- 11.2.4. FISH (Fluorescent in situ-hybridization)

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Roche Diagnostics

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Thermo Fisher Scientific Inc.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Illumina Inc.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Qiagen N.V.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Agilent Technologies Inc.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Abbott Laboratories

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Bio-Rad Laboratories Inc.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Myriad Genetics Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Genomic Health Inc.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Roche Diagnostics

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Molecular Oncology Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Molecular Oncology Revenue (million), by Application 2025 & 2033

- Figure 3: North America Molecular Oncology Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Molecular Oncology Revenue (million), by Type 2025 & 2033

- Figure 5: North America Molecular Oncology Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Molecular Oncology Revenue (million), by Country 2025 & 2033

- Figure 7: North America Molecular Oncology Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Molecular Oncology Revenue (million), by Application 2025 & 2033

- Figure 9: South America Molecular Oncology Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Molecular Oncology Revenue (million), by Type 2025 & 2033

- Figure 11: South America Molecular Oncology Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Molecular Oncology Revenue (million), by Country 2025 & 2033

- Figure 13: South America Molecular Oncology Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Molecular Oncology Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Molecular Oncology Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Molecular Oncology Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Molecular Oncology Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Molecular Oncology Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Molecular Oncology Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Molecular Oncology Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Molecular Oncology Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Molecular Oncology Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Molecular Oncology Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Molecular Oncology Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Molecular Oncology Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Molecular Oncology Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Molecular Oncology Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Molecular Oncology Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Molecular Oncology Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Molecular Oncology Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Molecular Oncology Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Molecular Oncology Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Molecular Oncology Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Molecular Oncology Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Molecular Oncology Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Molecular Oncology Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Molecular Oncology Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Molecular Oncology Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Molecular Oncology Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Molecular Oncology Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Molecular Oncology Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Molecular Oncology Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Molecular Oncology Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Molecular Oncology Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Molecular Oncology Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Molecular Oncology Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Molecular Oncology Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Molecular Oncology Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Molecular Oncology Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Molecular Oncology Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Molecular Oncology?

The projected CAGR is approximately 12.13%.

2. Which companies are prominent players in the Molecular Oncology?

Key companies in the market include Roche Diagnostics, Thermo Fisher Scientific Inc., Illumina, Inc., Qiagen N.V., Agilent Technologies, Inc., Abbott Laboratories, Bio-Rad Laboratories, Inc., Myriad Genetics, Inc., Genomic Health, Inc..

3. What are the main segments of the Molecular Oncology?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 810 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Molecular Oncology," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Molecular Oncology report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Molecular Oncology?

To stay informed about further developments, trends, and reports in the Molecular Oncology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence