Key Insights

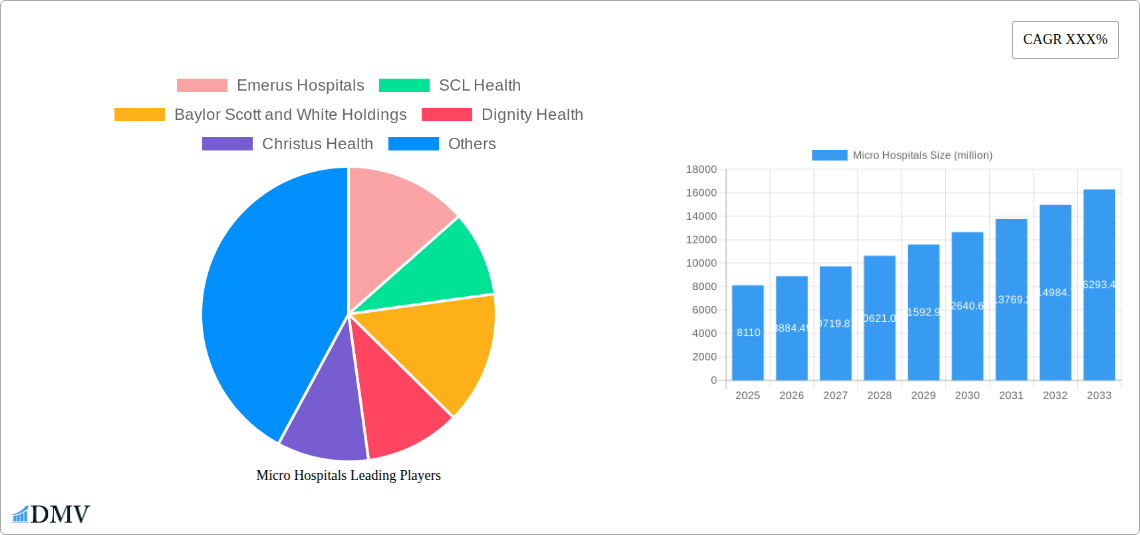

The global Micro Hospitals market is poised for significant expansion, with a projected market size of USD 8.11 billion in 2025. This growth is propelled by a robust Compound Annual Growth Rate (CAGR) of 9.69% expected during the forecast period of 2025-2033. This upward trajectory is primarily driven by the increasing demand for accessible and cost-effective healthcare solutions, particularly in underserved urban and suburban areas. Micro hospitals, with their focused service offerings and reduced overhead, are uniquely positioned to meet this demand. Key drivers include the rising prevalence of chronic diseases necessitating localized care, the growing need for specialized outpatient services that bypass larger, more expensive hospital infrastructures, and the increasing adoption of technology to enhance patient care and operational efficiency within these smaller facilities. Furthermore, government initiatives aimed at improving healthcare access and reducing healthcare costs are also contributing to market momentum.

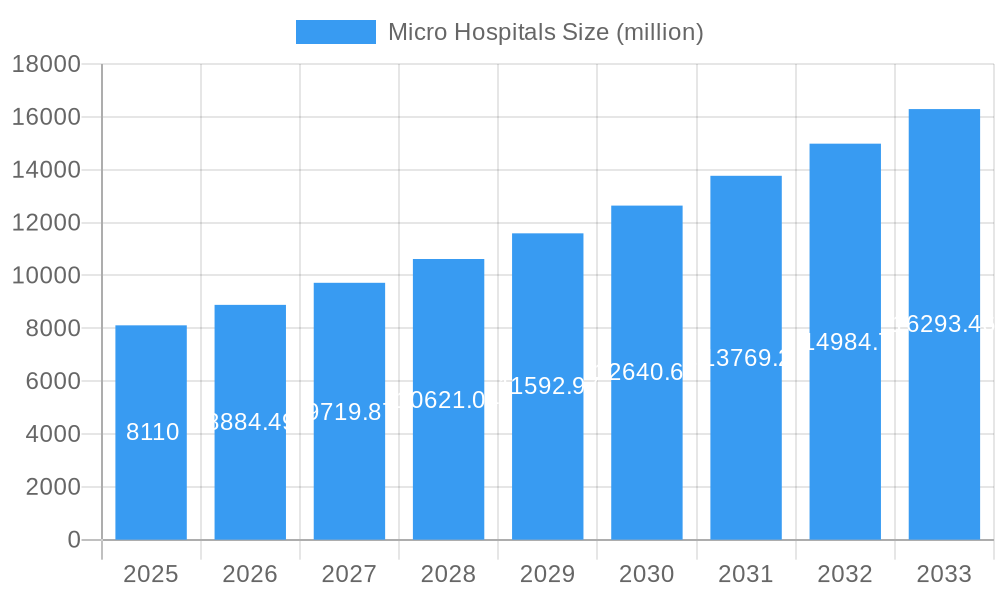

Micro Hospitals Market Size (In Billion)

The market is segmented by application into Individual and Corporate segments, reflecting the diverse patient base and the increasing trend of employers offering localized healthcare options. By type, micro hospitals are categorized across Tier 1, Tier 2, and Tier 3 cities, indicating a strategic focus on penetrating urban centers and expanding into less saturated markets to capture a broader demographic. The competitive landscape features prominent players like Emerus Hospitals, SCL Health, Baylor Scott and White Holdings, Dignity Health, and Christus Health, all vying for market share through strategic expansions, partnerships, and service innovations. While the market demonstrates strong growth potential, challenges such as regulatory hurdles, reimbursement complexities, and the need for skilled medical professionals in remote locations may present some restraints. However, the overarching trend towards patient-centric care and the inherent flexibility of the micro hospital model suggest continued expansion and evolution of this critical healthcare segment.

Micro Hospitals Company Market Share

Micro Hospitals Market Research Report: Unlocking Billion-Dollar Growth Potential

This comprehensive report delves into the dynamic micro hospitals market, analyzing its intricate composition, emerging trends, and significant growth trajectories from the historical period of 2019–2024 through to the forecast period of 2025–2033, with 2025 serving as both the base and estimated year. We explore the burgeoning landscape of these agile healthcare facilities, poised to capture substantial billion-dollar market share by redefining accessibility and efficiency in patient care. With an estimated market size projected to reach trillions of dollars, this report provides unparalleled insights for stakeholders seeking to navigate and capitalize on this transformative sector.

Micro Hospitals Market Composition & Trends

The micro hospitals market exhibits a dynamic yet increasingly concentrated structure, driven by innovation and evolving healthcare needs. Key innovation catalysts include advancements in telemedicine integration, modular construction, and a patient-centric approach to service delivery. The regulatory landscape, while evolving, generally favors the expansion of micro hospitals due to their potential to alleviate pressure on larger facilities and improve rural healthcare access. Substitute products, primarily traditional outpatient clinics and urgent care centers, face increasing competition from the comprehensive, albeit smaller-scale, service offerings of micro hospitals. End-user profiles range from Individuals seeking convenient and immediate care to Corporates looking for cost-effective and localized healthcare solutions for their employees. Mergers and acquisitions (M&A) are a significant trend, with Dignity Health and Baylor Scott and White Holdings actively consolidating their presence and expanding their micro hospital networks. The M&A deal value is projected to reach billions of dollars annually, reflecting the strategic importance of these acquisitions in capturing market share and fostering integrated healthcare systems. Market share distribution is currently fragmented but is seeing increasing consolidation among key players.

- Market Concentration: Increasing consolidation, with major healthcare systems acquiring and developing micro hospital networks.

- Innovation Catalysts: Telemedicine, modular design, AI-driven diagnostics, and patient engagement platforms.

- Regulatory Landscapes: Favorable for expanding access, particularly in underserved areas, with ongoing adjustments to reimbursement models.

- Substitute Products: Traditional outpatient clinics, urgent care centers, and freestanding emergency departments.

- End-User Profiles: Individuals seeking convenient care, employers prioritizing employee wellness, and communities in remote or underserved regions.

- M&A Activities: Active consolidation, with multi-billion dollar deals anticipated as large healthcare providers expand their footprint.

Micro Hospitals Industry Evolution

The micro hospitals industry is on a remarkable upward trajectory, marked by significant market growth trajectories, rapid technological advancements, and a profound shift in consumer demands. Over the study period of 2019–2033, this sector is set to witness exponential expansion, driven by an increasing recognition of micro hospitals as a viable and often superior alternative to traditional healthcare models. The market growth rate is projected to consistently outpace that of conventional hospitals, with an anticipated Compound Annual Growth Rate (CAGR) of XX% during the forecast period. Technological advancements have been instrumental in this evolution. The integration of advanced diagnostic imaging, robotic assistance in minor procedures, and sophisticated electronic health record (EHR) systems has enhanced the capabilities and patient outcomes within micro hospitals. Furthermore, the widespread adoption of telehealth and remote patient monitoring technologies has blurred geographical boundaries, allowing micro hospitals to extend their reach and provide continuous care.

Consumer demands have also played a pivotal role. Patients today prioritize convenience, speed, and personalized care, all of which are hallmarks of the micro hospital model. The desire for reduced wait times, accessible locations (both in Tier 1 Cities and increasingly in Tier 2 Cities and Tier 3 Cities), and a more intimate patient experience are powerful drivers pushing demand. This shift away from the often-impersonal and time-consuming experience of larger hospitals is a fundamental catalyst for micro hospital adoption. Data points such as an increase in patient satisfaction scores for micro hospitals by XX% compared to traditional settings and a XX% reduction in average patient wait times underscore this trend. The investment in new micro hospital facilities is expected to reach tens of billions of dollars annually, reflecting strong investor confidence in the sector's long-term viability and profitability. The focus on specialized services, such as orthopedic procedures, minor surgical interventions, and advanced diagnostic imaging, further contributes to their appeal and market penetration. The industry is moving towards a more integrated and decentralized healthcare delivery system, with micro hospitals at its core, offering a flexible and responsive approach to healthcare needs.

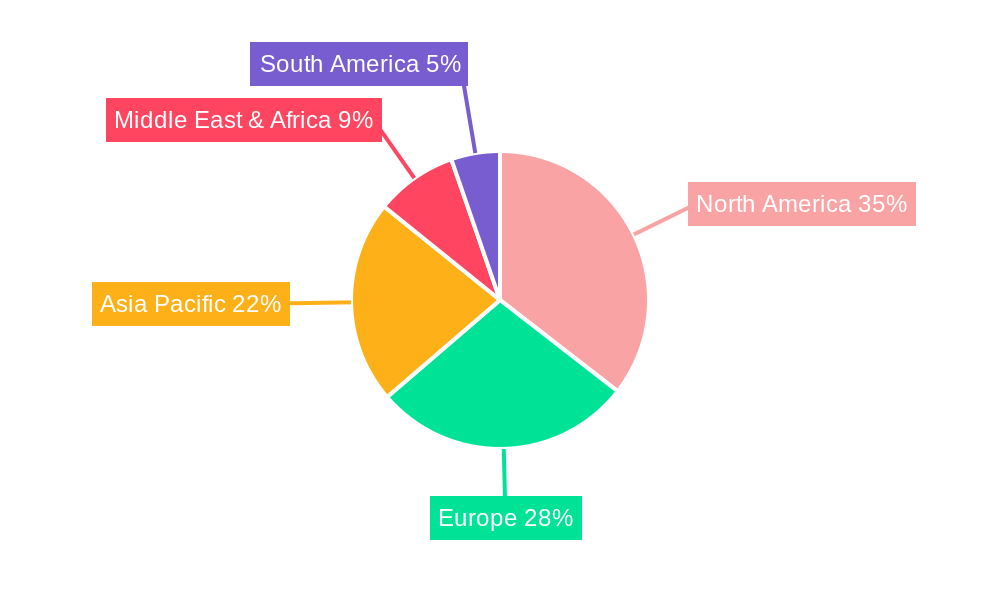

Leading Regions, Countries, or Segments in Micro Hospitals

The dominance within the micro hospitals market is increasingly being shaped by the strategic application of these facilities across different urban tiers and user segments. While Tier 1 Cities continue to be a strong market due to high population density and a greater capacity for early adoption and investment, the growth potential in Tier 2 Cities and Tier 3 Cities is rapidly accelerating, presenting significant opportunities for market leaders.

The Corporate segment is emerging as a particularly powerful driver of micro hospital expansion. Businesses are increasingly recognizing the financial and operational benefits of having readily accessible, high-quality healthcare for their employees. This includes reduced absenteeism, improved employee productivity, and enhanced overall well-being. Investment trends from large corporations indicate a willingness to fund or partner in the development of micro hospitals located near their facilities, particularly in areas with a high concentration of their workforce. This strategic deployment caters to the need for immediate medical attention, pre-employment screenings, and ongoing wellness programs, all of which can be efficiently managed through micro hospital infrastructure.

Furthermore, the Application for Individuals is experiencing substantial growth, driven by a desire for greater convenience and personalized healthcare experiences. Patients are actively seeking out micro hospitals for their shorter wait times, more intimate settings, and specialized services that can be delivered efficiently. The increasing prevalence of chronic diseases and an aging population further bolsters demand for accessible and responsive healthcare solutions. Regulatory support in various regions is also playing a crucial role in the expansion of micro hospitals, particularly in underserved areas. Government initiatives aimed at improving healthcare access and reducing the burden on larger hospitals are creating a fertile ground for micro hospital development. For instance, certain states are offering tax incentives or streamlined permitting processes for the establishment of these facilities, particularly in rural or suburban Tier 2 Cities and Tier 3 Cities. The investment in these regions is projected to reach billions, as healthcare providers and investors identify the unmet needs and significant market potential. The combination of corporate demand, individual preference for convenient care, and supportive regulatory environments is positioning Tier 2 Cities and Tier 3 Cities as future epicenters of micro hospital growth, alongside the established dominance of Tier 1 Cities.

Micro Hospitals Product Innovations

Micro hospitals are at the forefront of healthcare innovation, offering advanced solutions designed for efficiency and patient convenience. Key product innovations include modular construction enabling rapid deployment and scalability, integrated telemedicine platforms that extend care reach, and AI-powered diagnostic tools for faster and more accurate assessments. Applications span from specialized surgical procedures like outpatient orthopedic surgeries to advanced imaging services and urgent care. Performance metrics highlight reduced patient wait times by up to XX%, increased patient satisfaction by XX%, and a XX% improvement in operational efficiency compared to traditional facilities. These advancements underscore the unique selling proposition of micro hospitals: delivering high-quality, accessible, and cost-effective care.

Propelling Factors for Micro Hospitals Growth

The remarkable growth of the micro hospitals market is propelled by a confluence of technological, economic, and regulatory forces. Technologically, the widespread adoption of telehealth, AI-driven diagnostics, and robotic-assisted minimally invasive procedures enables micro hospitals to offer a broader spectrum of services with enhanced efficiency and precision. Economically, the demand for cost-effective healthcare solutions, coupled with the desire for convenient access to care, makes micro hospitals an attractive option for both patients and employers. Corporates, in particular, are investing in micro hospitals to reduce employee healthcare costs and improve productivity. Regulatory bodies are increasingly supportive, recognizing the potential of micro hospitals to improve healthcare access in underserved areas and alleviate strain on larger healthcare systems. For example, favorable reimbursement policies for specific procedures performed in micro hospital settings are a significant growth catalyst. The ongoing trend towards value-based care further incentivizes the adoption of more efficient and patient-centered models like micro hospitals, projected to contribute billions to market growth.

Obstacles in the Micro Hospitals Market

Despite robust growth, the micro hospitals market faces several significant obstacles. Regulatory hurdles remain a primary concern, with varying state and federal regulations regarding licensure, scope of services, and reimbursement models that can create complexity and delays in establishment. Supply chain disruptions for specialized medical equipment and staffing shortages for highly skilled medical professionals can also impact operational efficiency and expansion plans, potentially costing billions in lost revenue. Competitive pressures from established healthcare giants and the ongoing evolution of telehealth technologies that can replicate some micro hospital services also present challenges, requiring continuous innovation and strategic differentiation.

Future Opportunities in Micro Hospitals

The future of the micro hospitals market is brimming with untapped potential. Emerging opportunities lie in expanding into new geographical markets, particularly in rural and suburban Tier 2 Cities and Tier 3 Cities with demonstrated healthcare access gaps. Advancements in remote patient monitoring and AI-powered personalized medicine offer avenues for micro hospitals to deepen their patient engagement and offer more proactive care. Furthermore, partnerships with technology companies to integrate cutting-edge diagnostic and treatment tools, as well as increased collaboration with Corporates for dedicated employee wellness centers, present significant avenues for future growth, potentially adding billions to the market value.

Major Players in the Micro Hospitals Ecosystem

- Emerus Hospitals

- SCL Health

- Baylor Scott and White Holdings

- Dignity Health

- Christus Health

Key Developments in Micro Hospitals Industry

- 2024 March: Emerus Hospitals announced the acquisition of three micro hospitals in Texas, expanding their service footprint and reinforcing their market leadership.

- 2023 December: SCL Health finalized plans for a new micro hospital in Colorado, focusing on orthopedic and general surgical services to address regional demand.

- 2023 October: Baylor Scott and White Holdings launched an innovative mobile micro hospital unit for remote community outreach, enhancing access to primary care.

- 2023 July: Dignity Health revealed significant investment in telemedicine integration across its micro hospital network to improve patient connectivity and post-operative care.

- 2023 April: Christus Health announced a strategic partnership with a technology firm to implement AI-powered diagnostic imaging in its micro hospital facilities, enhancing diagnostic speed and accuracy.

Strategic Micro Hospitals Market Forecast

The micro hospitals market is poised for sustained and substantial growth, driven by an increasing demand for accessible, efficient, and patient-centric healthcare. Strategic forecasting indicates that market expansion will be fueled by technological integrations, favorable regulatory environments, and a growing preference for localized healthcare solutions by both Individuals and Corporates. The market's ability to offer cost-effective alternatives to traditional hospital settings, coupled with the ongoing development of specialized services, ensures a bright future with projected market values reaching trillions of dollars by 2033.

Micro Hospitals Segmentation

-

1. Application

- 1.1. Individual

- 1.2. Corporates

-

2. Type

- 2.1. Tier 1 Cities

- 2.2. Tier 2 Cities

- 2.3. Tier 3 Cities

Micro Hospitals Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Micro Hospitals Regional Market Share

Geographic Coverage of Micro Hospitals

Micro Hospitals REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.69% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Individual

- 5.1.2. Corporates

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Tier 1 Cities

- 5.2.2. Tier 2 Cities

- 5.2.3. Tier 3 Cities

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Micro Hospitals Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Individual

- 6.1.2. Corporates

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Tier 1 Cities

- 6.2.2. Tier 2 Cities

- 6.2.3. Tier 3 Cities

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Micro Hospitals Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Individual

- 7.1.2. Corporates

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Tier 1 Cities

- 7.2.2. Tier 2 Cities

- 7.2.3. Tier 3 Cities

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Micro Hospitals Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Individual

- 8.1.2. Corporates

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Tier 1 Cities

- 8.2.2. Tier 2 Cities

- 8.2.3. Tier 3 Cities

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Micro Hospitals Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Individual

- 9.1.2. Corporates

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Tier 1 Cities

- 9.2.2. Tier 2 Cities

- 9.2.3. Tier 3 Cities

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Micro Hospitals Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Individual

- 10.1.2. Corporates

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Tier 1 Cities

- 10.2.2. Tier 2 Cities

- 10.2.3. Tier 3 Cities

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Micro Hospitals Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Individual

- 11.1.2. Corporates

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Tier 1 Cities

- 11.2.2. Tier 2 Cities

- 11.2.3. Tier 3 Cities

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Emerus Hospitals

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 SCL Health

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Baylor Scott and White Holdings

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Dignity Health

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Christus Health

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.1 Emerus Hospitals

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Micro Hospitals Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Micro Hospitals Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Micro Hospitals Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Micro Hospitals Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Micro Hospitals Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Micro Hospitals Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Micro Hospitals Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Micro Hospitals Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Micro Hospitals Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Micro Hospitals Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Micro Hospitals Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Micro Hospitals Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Micro Hospitals Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Micro Hospitals Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Micro Hospitals Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Micro Hospitals Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Micro Hospitals Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Micro Hospitals Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Micro Hospitals Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Micro Hospitals Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Micro Hospitals Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Micro Hospitals Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Micro Hospitals Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Micro Hospitals Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Micro Hospitals Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Micro Hospitals Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Micro Hospitals Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Micro Hospitals Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Micro Hospitals Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Micro Hospitals Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Micro Hospitals Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Micro Hospitals Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Micro Hospitals Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Micro Hospitals Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Micro Hospitals Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Micro Hospitals Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Micro Hospitals Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Micro Hospitals Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Micro Hospitals Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Micro Hospitals Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Micro Hospitals Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Micro Hospitals Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Micro Hospitals Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Micro Hospitals Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Micro Hospitals Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Micro Hospitals Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Micro Hospitals Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Micro Hospitals Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Micro Hospitals Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Micro Hospitals Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Micro Hospitals?

The projected CAGR is approximately 9.69%.

2. Which companies are prominent players in the Micro Hospitals?

Key companies in the market include Emerus Hospitals, SCL Health, Baylor Scott and White Holdings, Dignity Health, Christus Health.

3. What are the main segments of the Micro Hospitals?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Micro Hospitals," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Micro Hospitals report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Micro Hospitals?

To stay informed about further developments, trends, and reports in the Micro Hospitals, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence