Key Insights

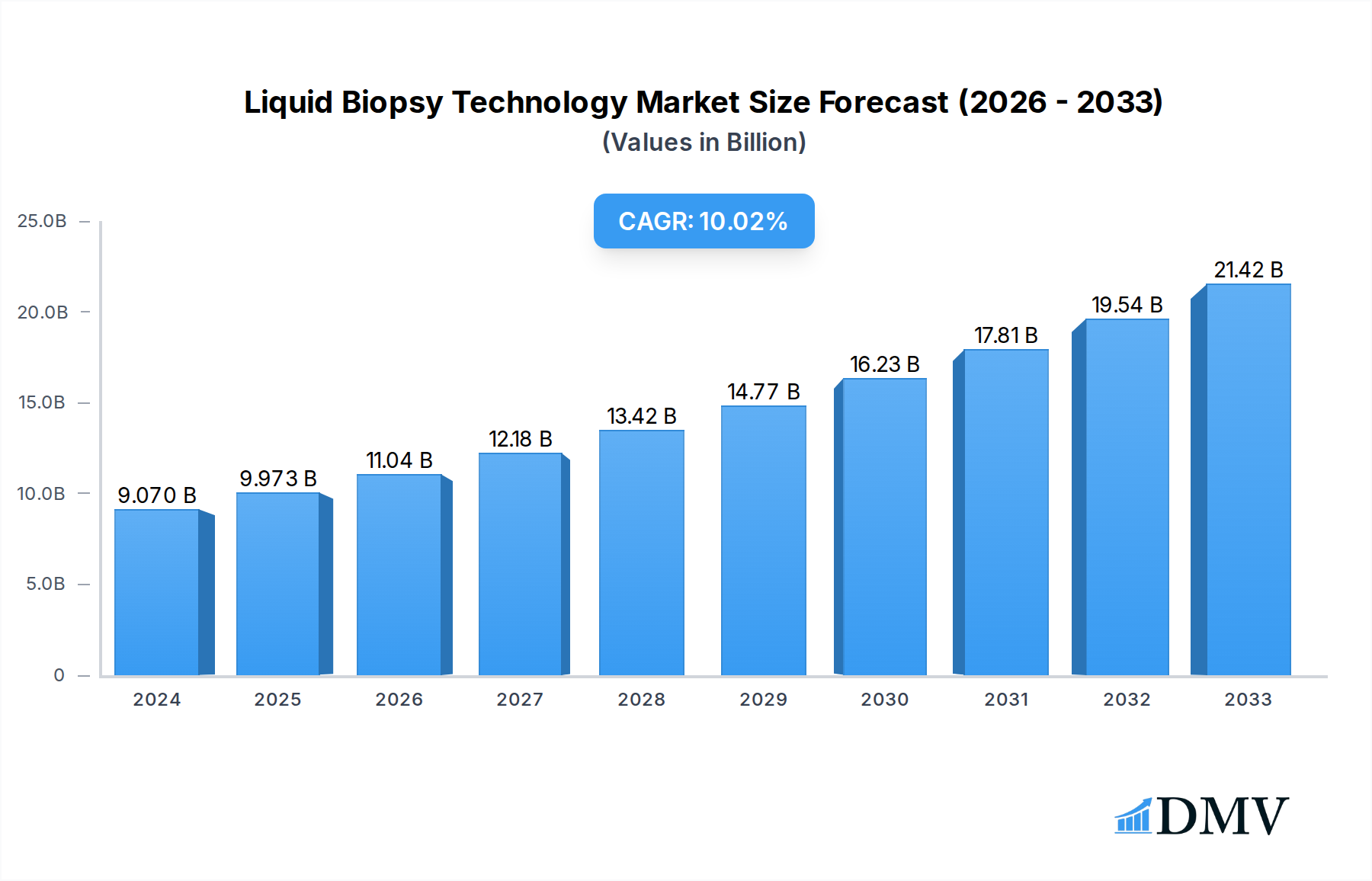

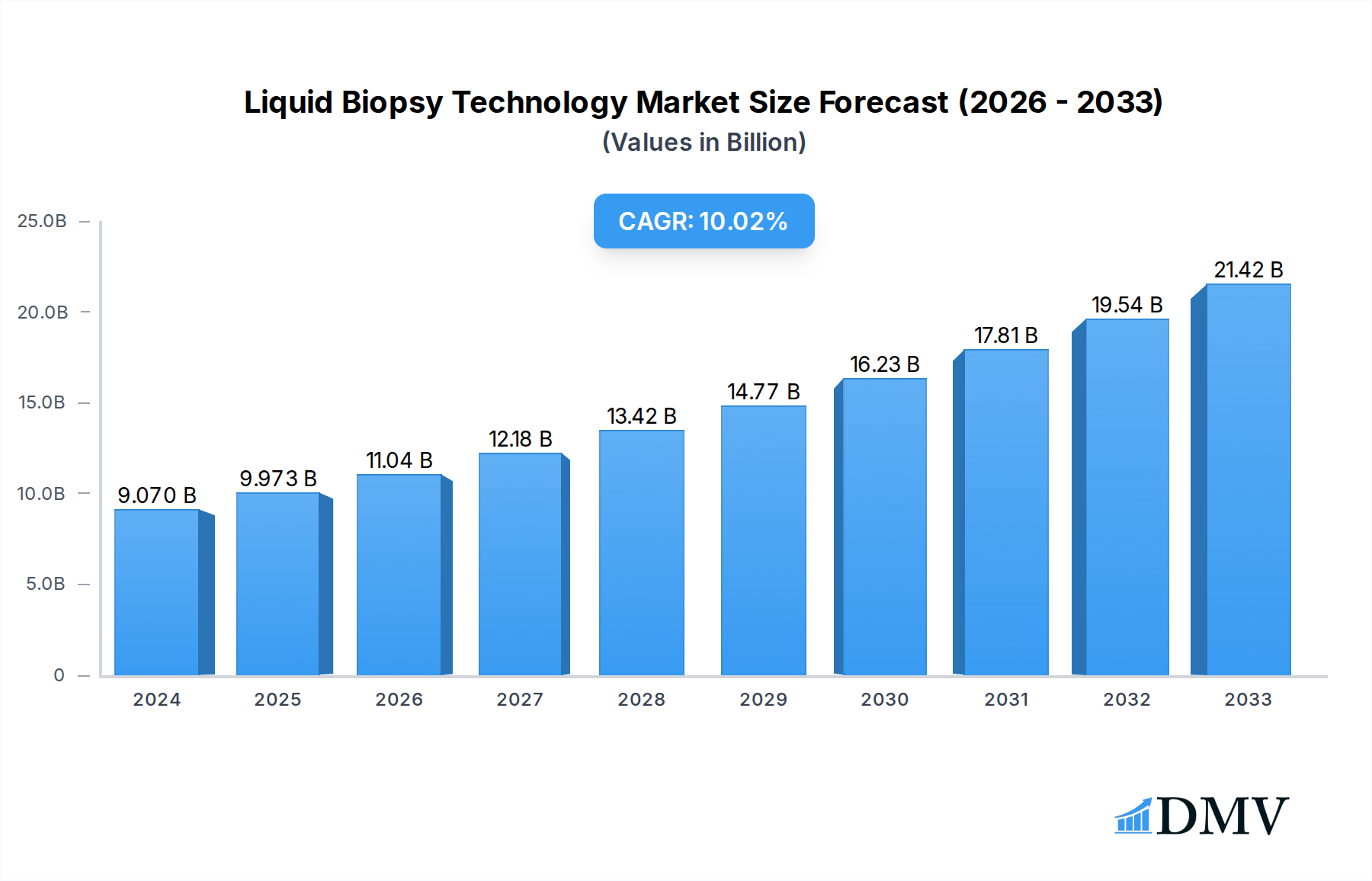

The global Liquid Biopsy Technology market is poised for significant expansion, reaching an estimated USD 9.07 billion in 2024 and projected to grow at a robust CAGR of 10.7% through 2033. This remarkable growth is fueled by the increasing adoption of liquid biopsy for early cancer detection, non-invasive disease monitoring, and personalized treatment strategies. The technology's ability to detect circulating tumor cells (CTCs), cell-free DNA (ctDNA), and exosomes from blood, urine, and other biofluids offers a less invasive and more convenient alternative to traditional tissue biopsies. This has led to its burgeoning application across various medical disciplines, particularly in oncology for diagnosing and managing a wide spectrum of cancers. The increasing prevalence of cancer globally, coupled with advancements in genomic sequencing and bioinformatics, further propels the demand for these sophisticated diagnostic tools.

Liquid Biopsy Technology Market Size (In Billion)

Key drivers for this market surge include a growing awareness among clinicians and patients regarding the benefits of liquid biopsies, such as reduced patient discomfort, faster turnaround times, and the ability to capture tumor heterogeneity. Furthermore, ongoing research and development efforts are continuously expanding the scope of liquid biopsy applications beyond cancer, into areas like prenatal testing and infectious disease diagnostics. While the market is characterized by strong growth, challenges such as the need for standardization of assay methodologies, regulatory hurdles for new applications, and reimbursement policies remain areas of focus. However, the inherent advantages of liquid biopsy in improving patient outcomes and healthcare efficiency are expected to outweigh these challenges, paving the way for widespread integration into routine clinical practice.

Liquid Biopsy Technology Company Market Share

Liquid Biopsy Technology Market Composition & Trends

The global liquid biopsy market is experiencing a dynamic evolution, driven by significant innovation and increasing adoption across various healthcare applications. Market concentration remains moderately fragmented, with key players like Exact Sciences, Guardant Health, and Natera holding substantial influence, particularly in oncology diagnostics. Innovation catalysts are abundant, fueled by advancements in next-generation sequencing (NGS), digital PCR, and microfluidics, enabling higher sensitivity and specificity in detecting circulating tumor DNA (ctDNA) and circulating tumor cells (CTCs). The regulatory landscape is maturing, with increasing FDA approvals for companion diagnostics and early detection tests, which is a significant market share distribution driver. Substitute products, primarily traditional tissue biopsies, are gradually being complemented and in some cases replaced by liquid biopsy due to its less invasive nature and potential for serial monitoring. End-user profiles are expanding beyond oncologists to include pulmonologists, gastroenterologists, and researchers, driven by the versatility of liquid biopsy for cancer screening, diagnosis, treatment selection, and monitoring. Mergers and acquisitions (M&A) are actively shaping the market, with significant deal values recorded as larger companies seek to bolster their liquid biopsy portfolios and technological capabilities. For instance, recent M&A activities have seen valuations in the billions, reflecting the immense growth potential. The overall market share distribution is increasingly favoring companies with robust multi-cancer early detection (MCED) platforms.

- Market Concentration: Moderately fragmented, with leading players in oncology.

- Innovation Catalysts: NGS, digital PCR, microfluidics, AI for data analysis.

- Regulatory Landscape: Maturing with increasing FDA approvals for diagnostics.

- Substitute Products: Traditional tissue biopsies, advanced imaging.

- End-User Profiles: Oncologists, researchers, pulmonologists, gastroenterologists.

- M&A Activities: Active, with significant deal values exceeding billions, focused on platform expansion and technological acquisition.

Liquid Biopsy Technology Industry Evolution

The liquid biopsy technology industry has witnessed an exponential growth trajectory, transforming diagnostic paradigms and patient care pathways over the historical period of 2019-2024, and is projected for sustained expansion through the forecast period of 2025-2033. This evolution is underpinned by relentless technological advancements, particularly in the realm of molecular biology and bio-informatics. The base year of 2025 marks a pivotal point, with estimated market value poised to reach hundreds of billions, reflecting a compound annual growth rate (CAGR) of approximately 20-25%. Early adoption metrics from 2019 to 2024 showed steady progress, primarily in companion diagnostics for targeted therapies in lung and breast cancer, with market penetration increasing from single digits to over 15% in specific indications.

Technological breakthroughs have been the primary engine of this evolution. The advent of highly sensitive next-generation sequencing (NGS) platforms has democratized the detection of low-frequency mutations in circulating tumor DNA (ctDNA), a key biomarker. This advancement has dramatically improved the accuracy of cancer detection and monitoring. Digital droplet PCR (ddPCR) offers unparalleled precision for quantifying specific DNA targets, making it invaluable for minimal residual disease (MRD) detection. Furthermore, advances in exosome isolation and characterization are opening new avenues for biomarker discovery. The development of advanced bioinformatics tools and artificial intelligence (AI) algorithms is crucial for interpreting the vast datasets generated by liquid biopsies, enabling more sophisticated diagnostic and prognostic insights.

Shifting consumer demands, specifically the growing preference for minimally invasive diagnostic procedures, have significantly amplified the market's growth. Patients and clinicians alike are increasingly embracing liquid biopsies over traditional tissue biopsies, which are invasive, carry higher risks, and can be logistically challenging. This shift is particularly pronounced in oncology, where liquid biopsies offer the potential for early cancer detection, personalized treatment selection, and continuous monitoring of treatment response and recurrence. The expanding application of liquid biopsy beyond oncology into areas such as prenatal testing, infectious disease diagnostics, and transplant monitoring further accelerates its adoption and market penetration.

Market growth trajectories have been consistently upward. For instance, the ctDNA segment, the largest by revenue, has seen its market share increase from approximately 50 billion in 2019 to an estimated 150 billion in 2024. Circulating tumor cells (CTCs) and exosomes, while smaller segments, are experiencing robust growth as isolation and analysis technologies mature, with market sizes estimated to reach tens of billions by 2025. The overall market size for liquid biopsy technology, encompassing instruments, reagents, and services, is projected to climb from an estimated 300 billion in 2025 to over 1.2 trillion by 2033. This impressive growth is a testament to the technology's ability to address unmet clinical needs and its increasing integration into routine clinical practice. The industry's evolution is characterized by a continuous cycle of innovation, increasing clinical validation, and expanding market access, solidifying its position as a transformative force in modern healthcare.

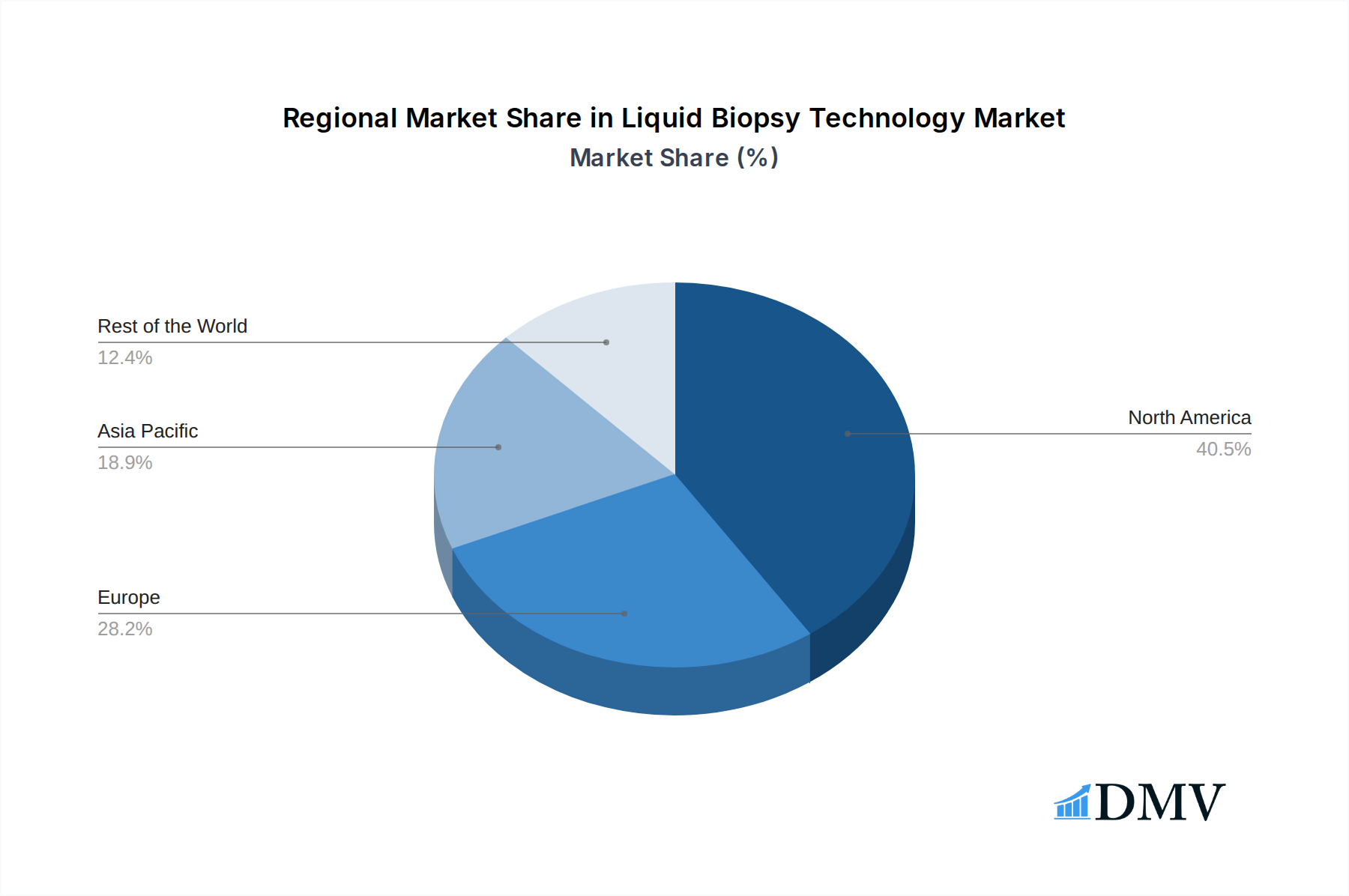

Leading Regions, Countries, or Segments in Liquid Biopsy Technology

The global liquid biopsy technology market is exhibiting robust growth across various regions and segments, driven by a confluence of strategic investments, favorable regulatory support, and escalating demand for advanced diagnostic solutions. From the application perspective, Blood Sample remains the dominant segment, capturing an estimated market share exceeding 70 billion in 2025. This dominance is attributed to its established infrastructure, ease of collection, and the wealth of biomarkers obtainable from blood, including ctDNA, CTCs, and cell-free DNA (cfDNA). Urine samples, while a rapidly growing segment projected to exceed 20 billion by 2025, currently hold a smaller but significant market share, particularly for urological cancers. Other biofluids, encompassing saliva, cerebrospinal fluid (CSF), and pleural fluid, represent niche but emerging applications with significant growth potential as analytical techniques improve.

Within the types of liquid biopsies, ctDNA consistently leads, accounting for over 60% of the market in 2025, with an estimated market value of 80 billion. Its utility in cancer screening, diagnosis, and treatment monitoring makes it the most widely utilized biomarker. Circulating Tumor Cells (CTCs) are another crucial segment, with a market size projected to reach 30 billion by 2025, offering insights into tumor heterogeneity and metastatic potential. Exosomes, though a nascent but rapidly advancing field, are expected to witness substantial growth, reaching an estimated 15 billion by 2025, due to their potential as rich sources of RNA and protein biomarkers.

Geographically, North America stands out as the leading region, driven by substantial investments in R&D, early adoption of novel diagnostic technologies, and a well-established healthcare infrastructure that supports the integration of liquid biopsies into clinical practice. The United States, in particular, is at the forefront of liquid biopsy market expansion, with an estimated market size exceeding 120 billion in 2025. Key drivers in this region include:

- Significant R&D Funding: Government and private sector investments in cancer research and diagnostic innovation.

- Favorable Regulatory Environment: A progressive approach by regulatory bodies like the FDA towards approving novel liquid biopsy tests.

- High Prevalence of Cancer: A substantial patient population with a high demand for advanced cancer diagnostics and treatments.

- Presence of Key Industry Players: Home to major companies like Exact Sciences, Guardant Health, and Thermo Fisher Scientific, fostering innovation and market development.

Europe follows as the second-largest market, with countries like Germany, the UK, and France showing strong growth, supported by increasing healthcare expenditure and a growing awareness of the benefits of liquid biopsies. Asia Pacific is the fastest-growing region, propelled by increasing healthcare infrastructure development, rising disposable incomes, and a growing focus on personalized medicine, with China and India being significant contributors to this growth, projected to exceed 50 billion in market value by 2025.

Liquid Biopsy Technology Product Innovations

Product innovations in liquid biopsy technology are rapidly advancing, offering enhanced sensitivity, specificity, and multiplexing capabilities. Companies are developing novel assay designs for detecting ultra-low frequency mutations in ctDNA, improving the accuracy of early cancer detection and minimal residual disease (MRD) monitoring. Innovations in microfluidics and lab-on-a-chip technologies are enabling faster, more cost-effective sample processing and biomarker isolation, particularly for CTCs and exosomes. Furthermore, the integration of artificial intelligence (AI) into data analysis platforms is revolutionizing the interpretation of complex genomic and proteomic data from liquid biopsies, leading to more actionable clinical insights. Performance metrics are continuously improving, with limit of detection (LoD) for ctDNA now reaching single-digit parts per million (ppm) and CTC enrichment and enumeration achieving greater accuracy. Unique selling propositions include multi-cancer early detection (MCED) capabilities, enabling the screening of multiple cancer types from a single blood draw, and the development of companion diagnostics that guide targeted therapy selection with unprecedented precision.

Propelling Factors for Liquid Biopsy Technology Growth

Several key factors are propelling the growth of the liquid biopsy technology market. Technologically, breakthroughs in next-generation sequencing (NGS) and digital PCR have dramatically increased sensitivity and reduced costs, making these tests more accessible. Economically, the increasing healthcare expenditure globally, coupled with a growing focus on value-based healthcare, favors minimally invasive and cost-effective diagnostic solutions like liquid biopsies. Regulatory approvals, such as those from the FDA for companion diagnostics and early detection tests, are critical catalysts, providing clinical validation and market access. The rising incidence of cancer worldwide also fuels demand for advanced diagnostic tools. Furthermore, the increasing preference for non-invasive procedures among patients and healthcare providers significantly boosts adoption rates, transforming cancer management from diagnosis to post-treatment monitoring.

- Technological Advancements: Increased sensitivity and specificity of NGS and ddPCR platforms.

- Economic Drivers: Growing global healthcare expenditure and focus on value-based care.

- Regulatory Support: FDA approvals for companion diagnostics and early detection tests.

- Rising Cancer Incidence: Increased demand for effective diagnostic and monitoring tools.

- Patient Preference: Growing demand for minimally invasive diagnostic procedures.

Obstacles in the Liquid Biopsy Technology Market

Despite its immense potential, the liquid biopsy market faces several significant obstacles. Regulatory challenges persist, with the complex approval pathways for novel diagnostics and the need for robust clinical validation for widespread adoption. Standardization of pre-analytical and analytical processes across different laboratories remains a hurdle, impacting assay reproducibility and comparability. Reimbursement policies from payers can be inconsistent, leading to access limitations for certain tests. Supply chain disruptions for critical reagents and specialized equipment can also impact production and availability. Furthermore, the high cost of some advanced liquid biopsy tests, particularly for early detection and comprehensive genomic profiling, can be a barrier to broader patient access, especially in resource-limited settings. Competitive pressures from established diagnostic companies and emerging startups also necessitate continuous innovation and cost optimization.

- Regulatory Hurdles: Complex approval processes and need for extensive clinical validation.

- Lack of Standardization: Variability in pre-analytical and analytical methods.

- Reimbursement Issues: Inconsistent payer policies affecting patient access.

- Cost of Advanced Tests: High price points limiting accessibility for some populations.

- Supply Chain Vulnerabilities: Potential disruptions for reagents and specialized equipment.

Future Opportunities in Liquid Biopsy Technology

The future opportunities in liquid biopsy technology are vast and multifaceted, promising significant market expansion. The development of highly accurate multi-cancer early detection (MCED) tests that can screen for a broad spectrum of cancers from a single blood draw represents a major frontier, potentially revolutionizing cancer prevention and saving millions of lives annually, with market potential reaching hundreds of billions. Expanding applications beyond oncology, such as infectious disease diagnostics, transplant rejection monitoring, and neurological disorder assessment, offers new avenues for growth. Technological advancements in areas like artificial intelligence (AI) for predictive analytics and liquid biopsy-based companion diagnostics for novel targeted therapies will further drive innovation. The emergence of new biomarker classes beyond ctDNA and CTCs, such as circulating RNA and epigenetics, also presents significant opportunities for novel test development. Furthermore, the increasing adoption of liquid biopsies in low- and middle-income countries, driven by cost-reduction initiatives and technological advancements, will unlock new market potential.

- Multi-Cancer Early Detection (MCED): Development of highly sensitive and specific tests for early detection of multiple cancers.

- Non-Oncology Applications: Expansion into infectious diseases, transplant monitoring, and neurology.

- AI-Powered Analytics: Advanced interpretation of complex genomic and proteomic data for predictive diagnostics.

- Novel Biomarker Discovery: Exploration of circulating RNA, epigenetics, and other emerging biomarkers.

- Global Market Expansion: Increasing adoption in emerging economies through cost-effective solutions.

Major Players in the Liquid Biopsy Technology Ecosystem

Exact Sciences Guardant Health Natera Bio-Techne LabCorp Endress+Hauser MDxHealth MutantDx Thermo Fisher Scientific Norgen Biotek Nucleix OraSure Technologies Qiagen Bio-Rad Laboratories Biocartis NeoGenomics Sysmex Inostics Menarini Silicon Biosystems Biocept ANGLE plc

Key Developments in Liquid Biopsy Technology Industry

- 2023: Exact Sciences launches advanced ctDNA testing for minimal residual disease (MRD) in colorectal cancer, demonstrating significant clinical impact.

- 2024: Guardant Health receives expanded FDA approval for its Guardant360 CDx test, enabling broader use in treatment selection for lung cancer patients.

- 2023: Natera announces promising results for its multi-cancer early detection test, Signatera, in clinical trials, showcasing high sensitivity and specificity.

- 2024: Bio-Techne enhances its exosome isolation and characterization platforms, enabling researchers to explore novel exosomal biomarkers for various diseases.

- 2023: LabCorp expands its liquid biopsy service offerings, integrating advanced genomic profiling for a wider range of cancers.

- 2024: Thermo Fisher Scientific launches a new high-throughput NGS platform designed for liquid biopsy applications, increasing sample processing capacity.

- 2023: Qiagen introduces an innovative assay for the detection of circulating RNA biomarkers, opening new diagnostic possibilities.

- 2024: Bio-Rad Laboratories develops advanced digital PCR systems optimized for the ultra-sensitive detection of ctDNA.

- 2023: Menarini Silicon Biosystems showcases its advanced CTC enrichment and analysis technology for personalized cancer therapy.

- 2024: ANGLE plc receives regulatory clearance for its Parsortix™ system, a key tool for CTC isolation and analysis.

Strategic Liquid Biopsy Technology Market Forecast

The strategic liquid biopsy technology market forecast indicates sustained robust growth, primarily driven by the increasing clinical utility of ctDNA and CTCs in oncology. Multi-cancer early detection (MCED) will emerge as a significant growth catalyst, with projected market potential reaching hundreds of billions over the forecast period. Advancements in AI and machine learning will further enhance the predictive power of liquid biopsies, enabling more personalized treatment strategies and improved patient outcomes. Expansion into non-oncology applications, coupled with cost reduction initiatives and increased accessibility in emerging markets, will also contribute significantly to market expansion. Strategic partnerships and collaborations among key players will be crucial for navigating the evolving regulatory landscape and accelerating the translation of research into clinical practice, ensuring the liquid biopsy market continues its trajectory towards becoming a cornerstone of modern diagnostics.

Liquid Biopsy Technology Segmentation

-

1. Application

- 1.1. Blood Sample

- 1.2. Urine Sample

- 1.3. Other Bio Fluids

-

2. Types

- 2.1. CTCs

- 2.2. ctDNA

- 2.3. Exosomes

Liquid Biopsy Technology Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Liquid Biopsy Technology Regional Market Share

Geographic Coverage of Liquid Biopsy Technology

Liquid Biopsy Technology REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.52% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Blood Sample

- 5.1.2. Urine Sample

- 5.1.3. Other Bio Fluids

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. CTCs

- 5.2.2. ctDNA

- 5.2.3. Exosomes

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Liquid Biopsy Technology Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Blood Sample

- 6.1.2. Urine Sample

- 6.1.3. Other Bio Fluids

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. CTCs

- 6.2.2. ctDNA

- 6.2.3. Exosomes

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Liquid Biopsy Technology Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Blood Sample

- 7.1.2. Urine Sample

- 7.1.3. Other Bio Fluids

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. CTCs

- 7.2.2. ctDNA

- 7.2.3. Exosomes

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Liquid Biopsy Technology Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Blood Sample

- 8.1.2. Urine Sample

- 8.1.3. Other Bio Fluids

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. CTCs

- 8.2.2. ctDNA

- 8.2.3. Exosomes

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Liquid Biopsy Technology Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Blood Sample

- 9.1.2. Urine Sample

- 9.1.3. Other Bio Fluids

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. CTCs

- 9.2.2. ctDNA

- 9.2.3. Exosomes

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Liquid Biopsy Technology Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Blood Sample

- 10.1.2. Urine Sample

- 10.1.3. Other Bio Fluids

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. CTCs

- 10.2.2. ctDNA

- 10.2.3. Exosomes

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Liquid Biopsy Technology Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Blood Sample

- 11.1.2. Urine Sample

- 11.1.3. Other Bio Fluids

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. CTCs

- 11.2.2. ctDNA

- 11.2.3. Exosomes

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Exact Sciences

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Guardant Health

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Natera

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Bio-Techne

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 LabCorp

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Endress+Hauser

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 MDxHealth

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 MutantDx

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Thermo Fisher Scientific

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Norgen Biotek

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Nucleix

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 OraSure Technologies

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Qiagen

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Bio-Rad Laboratories

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Biocartis

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 NeoGenomics

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Sysmex Inostics

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Menarini Silicon Biosystems

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Biocept

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 ANGLE plc

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.1 Exact Sciences

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Liquid Biopsy Technology Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Liquid Biopsy Technology Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Liquid Biopsy Technology Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Liquid Biopsy Technology Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Liquid Biopsy Technology Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Liquid Biopsy Technology Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Liquid Biopsy Technology Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Liquid Biopsy Technology Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Liquid Biopsy Technology Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Liquid Biopsy Technology Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Liquid Biopsy Technology Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Liquid Biopsy Technology Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Liquid Biopsy Technology Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Liquid Biopsy Technology Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Liquid Biopsy Technology Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Liquid Biopsy Technology Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Liquid Biopsy Technology Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Liquid Biopsy Technology Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Liquid Biopsy Technology Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Liquid Biopsy Technology Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Liquid Biopsy Technology Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Liquid Biopsy Technology Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Liquid Biopsy Technology Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Liquid Biopsy Technology Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Liquid Biopsy Technology Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Liquid Biopsy Technology Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Liquid Biopsy Technology Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Liquid Biopsy Technology Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Liquid Biopsy Technology Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Liquid Biopsy Technology Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Liquid Biopsy Technology Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Liquid Biopsy Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Liquid Biopsy Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Liquid Biopsy Technology Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Liquid Biopsy Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Liquid Biopsy Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Liquid Biopsy Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Liquid Biopsy Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Liquid Biopsy Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Liquid Biopsy Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Liquid Biopsy Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Liquid Biopsy Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Liquid Biopsy Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Liquid Biopsy Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Liquid Biopsy Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Liquid Biopsy Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Liquid Biopsy Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Liquid Biopsy Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Liquid Biopsy Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Liquid Biopsy Technology Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Liquid Biopsy Technology?

The projected CAGR is approximately 11.52%.

2. Which companies are prominent players in the Liquid Biopsy Technology?

Key companies in the market include Exact Sciences, Guardant Health, Natera, Bio-Techne, LabCorp, Endress+Hauser, MDxHealth, MutantDx, Thermo Fisher Scientific, Norgen Biotek, Nucleix, OraSure Technologies, Qiagen, Bio-Rad Laboratories, Biocartis, NeoGenomics, Sysmex Inostics, Menarini Silicon Biosystems, Biocept, ANGLE plc.

3. What are the main segments of the Liquid Biopsy Technology?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.6 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Liquid Biopsy Technology," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Liquid Biopsy Technology report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Liquid Biopsy Technology?

To stay informed about further developments, trends, and reports in the Liquid Biopsy Technology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence