Key Insights

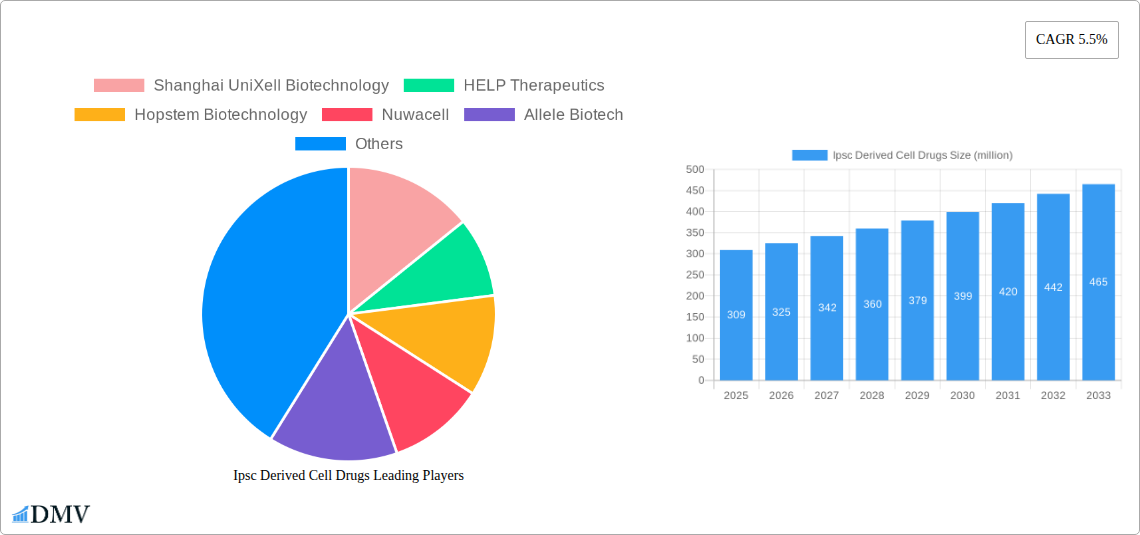

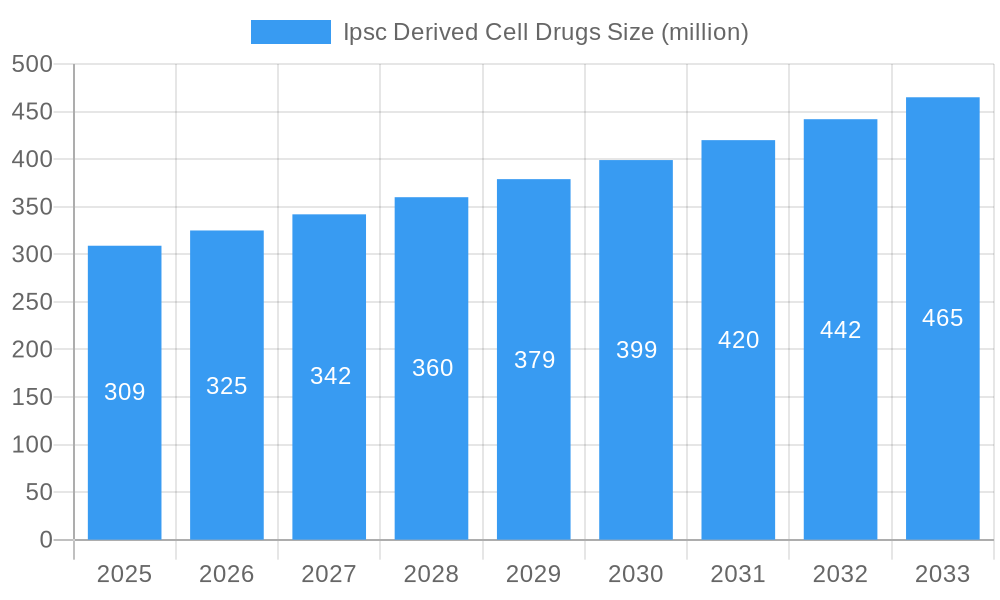

The global iPSC-derived cell drugs market is poised for significant expansion, projected to reach a substantial market size of approximately $309 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.5% anticipated throughout the forecast period of 2025-2033. This growth is primarily fueled by the immense therapeutic potential of induced pluripotent stem cells (iPSCs) in addressing unmet medical needs across various domains. Key drivers include advancements in gene editing technologies, a growing understanding of disease mechanisms at the cellular level, and increasing investment in regenerative medicine research and development. The market is witnessing a paradigm shift towards personalized medicine, where autologous iPSC-derived cell drugs, tailored to individual patients, are gaining traction for their potential to minimize immune rejection and enhance therapeutic efficacy. Simultaneously, the development of universal iPSC-derived cell drugs, derived from healthy donors and engineered for broad applicability, is also a significant trend, promising scalability and accessibility for a wider patient population.

Ipsc Derived Cell Drugs Market Size (In Million)

The applications for iPSC-derived cell drugs are diverse and rapidly evolving. The anti-inflammatory repair segment is a major contributor, leveraging iPSC technology to generate cells that can effectively reduce inflammation and promote tissue regeneration in conditions like autoimmune diseases and injuries. Tumor immunity is another critical area, with iPSC-derived cells being explored for their potential in developing novel cancer immunotherapies. Regenerative medicine applications are vast, encompassing the repair and replacement of damaged tissues and organs, offering hope for patients with chronic diseases and degenerative conditions. While the market exhibits strong growth potential, it also faces certain restraints. These include the high cost of research and development, stringent regulatory hurdles for novel cell therapies, and the need for advanced manufacturing capabilities to ensure consistent quality and scalability. Overcoming these challenges will be crucial for unlocking the full market potential and ensuring widespread patient access to these life-changing therapies. Key players like Shanghai UniXell Biotechnology, HELP Therapeutics, and BlueRock Therapeutics are at the forefront of innovation, driving the development and commercialization of these advanced cell-based therapeutics.

Ipsc Derived Cell Drugs Company Market Share

**Ipsc Derived Cell Drugs Market Report: Comprehensive Analysis & Future Outlook (2019-2033)**

Executive Summary:

This in-depth report delivers a comprehensive analysis of the burgeoning Ipsc Derived Cell Drugs market. Spanning the historical period of 2019–2024, the base year of 2025, and projecting to 2033, this study evaluates market composition, key trends, industry evolution, leading segments, product innovations, growth drivers, inherent challenges, and future opportunities. With an estimated market size projected to reach $XXX million by 2033, this report is an indispensable resource for stakeholders seeking to navigate and capitalize on the transformative potential of induced pluripotent stem cell (iPSC) derived cell therapies. We delve into the intricate dynamics, from regulatory landscapes to groundbreaking product developments, offering actionable insights for strategic decision-making.

Ipsc Derived Cell Drugs Market Composition & Trends

The Ipsc Derived Cell Drugs market is characterized by dynamic growth and increasing investor interest, driven by significant advancements in regenerative medicine and oncology. Market concentration is moderate, with a growing number of innovative players emerging. Key innovation catalysts include breakthroughs in iPSC reprogramming efficiency, directed differentiation protocols, and advanced manufacturing techniques, enabling the production of high-quality, scalable cell therapies. The regulatory landscape, while evolving, is becoming more conducive to the approval and commercialization of these novel treatments, with agencies worldwide establishing pathways for advanced therapy medicinal products. Substitute products primarily consist of traditional pharmaceuticals and conventional cell therapies, but iPSC-derived therapies offer distinct advantages in terms of patient-specific potential and broad applicability. End-user profiles range from academic research institutions and hospitals to pharmaceutical and biotechnology companies investing in R&D and clinical trials. Mergers and Acquisitions (M&A) activities are on the rise as larger pharmaceutical companies seek to acquire promising iPSC technology platforms and clinical-stage assets. For instance, M&A deal values in this sector are estimated to reach $XXX million during the forecast period. The market share distribution is currently fragmented, with early leaders establishing strong positions in niche applications.

- Market Share Distribution: Projected to shift significantly with increased clinical trial success and commercial approvals.

- M&A Deal Values: Anticipated to increase by an estimated XX% annually as consolidation efforts intensify.

- Innovation Catalysts: Improved reprogramming, directed differentiation, and GMP manufacturing.

- Regulatory Pathways: Streamlining of approval processes for cell and gene therapies.

- End-User Segments: Pharmaceutical/Biotech, Research Institutions, Hospitals.

Ipsc Derived Cell Drugs Industry Evolution

The Ipsc Derived Cell Drugs industry has witnessed a remarkable evolution, transforming from nascent research concepts to tangible therapeutic candidates with the potential to revolutionize patient care. Over the historical period (2019–2024), the industry has experienced a compound annual growth rate (CAGR) of approximately XX%, a testament to the rapid advancements in both scientific understanding and clinical translation. This growth trajectory has been fueled by sustained investment in fundamental research, leading to a deeper comprehension of cellular reprogramming and differentiation mechanisms. Technological advancements have been paramount, with the development of more efficient and safer iPSC generation techniques, refined directed differentiation protocols to produce specific cell lineages (e.g., cardiomyocytes, dopaminergic neurons, hepatocytes), and the establishment of Good Manufacturing Practice (GMP) compliant manufacturing processes crucial for large-scale production.

Shifting consumer demands, particularly from patients and healthcare providers seeking more effective and personalized treatment options for chronic and debilitating diseases, have also played a significant role. The inherent promise of iPSC-derived cell drugs to regenerate damaged tissues, replace diseased cells, and modulate immune responses offers a compelling alternative to conventional therapies that often only manage symptoms. Early clinical trial successes in areas like spinal cord injury, Parkinson's disease, age-related macular degeneration, and certain cancers have validated the therapeutic potential, further accelerating industry development. The estimated market growth rate for Ipsc Derived Cell Drugs is projected to be XX% from 2025 to 2033, with adoption metrics for approved therapies expected to rise substantially as manufacturing scales and treatment accessibility improves. The transition from preclinical research to advanced clinical trials and the eventual commercialization of these therapies mark critical milestones in the industry's evolution. The robust pipeline of iPSC-derived cell drug candidates across various therapeutic areas, coupled with increasing regulatory support for these innovative modalities, underpins this optimistic outlook. The industry is moving towards a paradigm of personalized regenerative medicine, where patient-derived iPSCs can be engineered into bespoke therapeutic cells, minimizing immunogenicity and maximizing efficacy.

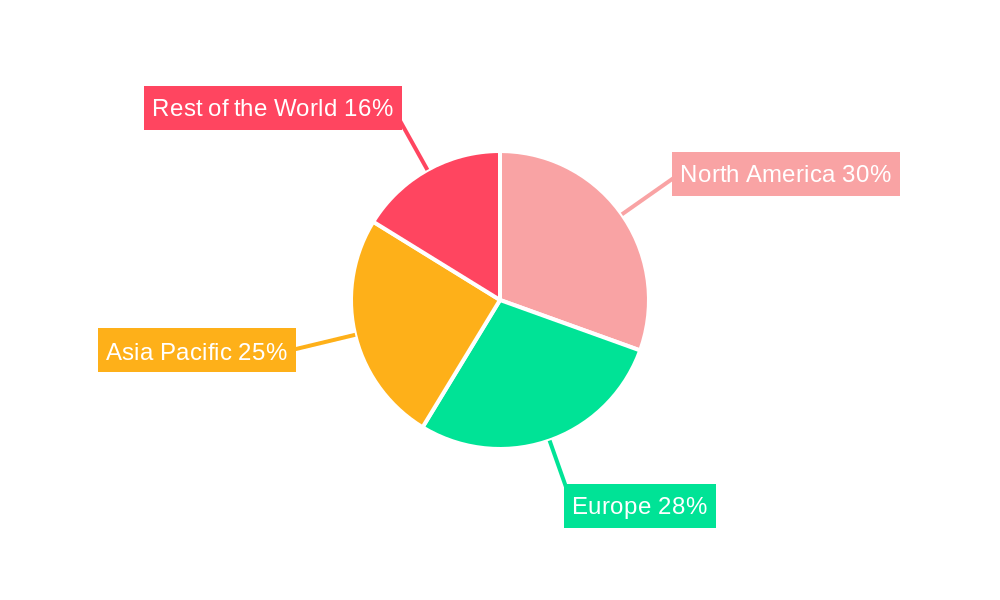

Leading Regions, Countries, or Segments in Ipsc Derived Cell Drugs

The Ipsc Derived Cell Drugs market exhibits significant regional and segment-specific dominance, driven by a confluence of factors including research infrastructure, investment, regulatory frameworks, and disease prevalence. Currently, North America stands out as the leading region, propelled by a robust ecosystem of academic research institutions, venture capital funding, and supportive regulatory bodies like the U.S. Food and Drug Administration (FDA), which has established pathways for cell and gene therapies. The United States, in particular, leads in the number of clinical trials and patent filings related to iPSC-derived cell drugs.

Within the Applications segment, Regenerative Medicine is the primary driver of market growth. This is due to the broad applicability of iPSC-derived cells in repairing or replacing damaged tissues across a wide spectrum of diseases, including cardiovascular conditions, neurological disorders, and orthopedic injuries. The potential for iPSC-derived therapies to address previously untreatable conditions is a key factor in its dominance.

In terms of Type, Autologous iPSC Derived Cell Drugs have shown early leadership, particularly in applications where immune rejection is a significant concern. The ability to generate patient-specific cells minimizes the risk of graft-versus-host disease and reduces the need for immunosuppressive drugs. However, Universal iPSC Derived Cell Drugs, derived from healthy donor iPSCs and engineered for broad compatibility, are rapidly gaining traction due to their potential for scalability and off-the-shelf availability, which can significantly reduce manufacturing costs and improve patient access. The development of gene-editing technologies like CRISPR-Cas9 to enhance the safety and efficacy of universal iPSC-derived cells further bolsters their future market potential.

- Leading Region: North America (primarily the United States)

- Key Drivers:

- High levels of R&D investment and funding.

- Established regulatory frameworks for advanced therapies.

- Presence of leading biotechnology and pharmaceutical companies.

- Strong academic research base and clinical trial infrastructure.

- Key Drivers:

- Dominant Application Segment: Regenerative Medicine

- Key Drivers:

- Potential to treat a wide range of degenerative and chronic diseases.

- Promise of tissue repair and functional restoration.

- Advancements in differentiation protocols for various cell types.

- Key Drivers:

- Emerging Type Dominance: While Autologous iPSC Derived Cell Drugs have early traction, Universal iPSC Derived Cell Drugs are poised for significant growth.

- Key Drivers for Universal iPSC:

- Scalability and potential for off-the-shelf availability.

- Reduced manufacturing costs per dose.

- Advancements in immunomodulation and gene editing for broader compatibility.

- Key Drivers for Universal iPSC:

Ipsc Derived Cell Drugs Product Innovations

Product innovation in Ipsc Derived Cell Drugs is rapidly advancing, focusing on enhancing therapeutic efficacy, improving manufacturing scalability, and ensuring patient safety. Key innovations include the development of highly pure and functional cell populations derived from iPSCs, such as functional cardiomyocytes for cardiac repair and dopaminergic neurons for Parkinson's disease. Researchers are also exploring advanced differentiation techniques to generate more complex tissue structures and cellular microenvironments. Unique selling propositions include the potential for patient-specific therapies with reduced immunogenicity and the capacity to address a wide range of unmet medical needs. Technological advancements in directed differentiation protocols, gene editing for disease correction or immune evasion, and novel biomaterial scaffolds for cell delivery are driving these innovations forward, promising significant improvements in treatment outcomes.

Propelling Factors for Ipsc Derived Cell Drugs Growth

The growth of the Ipsc Derived Cell Drugs market is propelled by a synergistic interplay of technological, economic, and regulatory factors. Technologically, breakthroughs in iPSC reprogramming efficiency, directed differentiation into various cell lineages, and advanced manufacturing techniques (like bioreactors and automation) enable the production of clinical-grade cell therapies at scale. Economically, increasing venture capital funding and strategic investments from major pharmaceutical companies are fueling R&D pipelines and clinical trial progression. Regulatory bodies are actively creating specialized pathways and providing guidance for the approval of these novel cell-based therapies, fostering a more predictable path to market. Furthermore, the growing recognition of the limitations of conventional treatments for chronic and degenerative diseases creates a strong demand for innovative solutions like iPSC-derived cell drugs. For example, the successful completion of Phase II trials for a particular iPSC-derived therapy in $XX million worth of investment.

Obstacles in the Ipsc Derived Cell Drugs Market

Despite its immense potential, the Ipsc Derived Cell Drugs market faces several significant obstacles. Regulatory hurdles remain a considerable challenge, with complex and evolving approval processes requiring extensive preclinical and clinical data to demonstrate safety and efficacy. High manufacturing costs associated with generating patient-specific or highly purified cell populations, coupled with the need for specialized facilities and expertise, limit scalability and increase treatment prices, impacting market accessibility. Supply chain complexities in sourcing raw materials, ensuring cold chain logistics, and managing the ex vivo culture and delivery of living cells present logistical challenges. Immune rejection of allogeneic (donor-derived) cells, although mitigated by advancements, can still be a concern, necessitating ongoing research into immunomodulatory strategies. The competitive pressure from established therapies and other emerging biotechnologies also requires continuous innovation and demonstration of superior clinical outcomes, representing an estimated XX% of R&D expenditure.

Future Opportunities in Ipsc Derived Cell Drugs

The future of Ipsc Derived Cell Drugs is replete with promising opportunities, driven by ongoing scientific innovation and expanding therapeutic applications. The development of off-the-shelf universal iPSC-derived cell therapies holds immense potential to democratize access and reduce costs, overcoming the limitations of autologous treatments. Emerging technologies like CRISPR-Cas9 gene editing offer the ability to correct genetic defects in iPSCs or engineer them for enhanced therapeutic function and immune evasion, opening doors for treating a wider range of genetic disorders. Advancements in tissue engineering and 3D bioprinting could lead to the development of more complex, functional organoids and tissues for transplantation. Furthermore, exploring novel applications beyond current targets, such as in autoimmune diseases and metabolic disorders, presents significant untapped market potential, estimated to reach $XXX million in value.

Major Players in the Ipsc Derived Cell Drugs Ecosystem

- Shanghai UniXell Biotechnology

- HELP Therapeutics

- Hopstem Biotechnology

- Nuwacell

- Allele Biotech

- BlueRock Therapeutics

- Century Therapeutics

- Fate Therapeutics

- Cellino

- Xellsmart

Key Developments in Ipsc Derived Cell Drugs Industry

- 2019: Launch of pivotal clinical trials for iPSC-derived retinal pigment epithelial cells in Age-Related Macular Degeneration.

- 2020: Significant advancements in CRISPR-Cas9 integration for iPSC-derived therapies, enhancing safety and efficacy.

- 2021: Major pharmaceutical company acquires an iPSC-focused biotech, signaling growing industry consolidation and investment, with the deal valued at approximately $XXX million.

- 2022: First iPSC-derived therapy progresses to Phase III clinical trials for Parkinson's disease.

- 2023: Development of novel bioreactor systems enabling the scaled-up manufacturing of iPSC-derived cells to meet potential commercial demands.

- 2024: Regulatory agency provides updated guidance for the expedited review of iPSC-derived cell therapies.

Strategic Ipsc Derived Cell Drugs Market Forecast

The strategic outlook for Ipsc Derived Cell Drugs is exceptionally positive, driven by a convergence of accelerating research, robust clinical pipelines, and a growing appetite for transformative healthcare solutions. The increasing success of clinical trials, particularly in regenerative medicine and oncology, is validating the therapeutic potential and paving the way for regulatory approvals. Continued investment in advanced manufacturing technologies and gene-editing capabilities will further enhance the scalability, safety, and efficacy of these therapies. As regulatory pathways become more defined and predictable, market entry for iPSC-derived cell drugs is expected to accelerate. The growing demand for personalized medicine and the limitations of existing treatments for many chronic and debilitating diseases create a fertile ground for the widespread adoption of iPSC-derived cell therapies, positioning the market for significant growth and impact on patient outcomes. The market is projected to reach an estimated $XXX million by 2033.

Ipsc Derived Cell Drugs Segmentation

-

1. Application

- 1.1. Anti-Inflammatory Repair

- 1.2. Tumor Immunity

- 1.3. Regenerative Medicine

- 1.4. Others

-

2. Type

- 2.1. Autologous iPSC Derived Cell Drugs

- 2.2. Universal iPSC Derived Cell Drugs

Ipsc Derived Cell Drugs Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ipsc Derived Cell Drugs Regional Market Share

Geographic Coverage of Ipsc Derived Cell Drugs

Ipsc Derived Cell Drugs REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Anti-Inflammatory Repair

- 5.1.2. Tumor Immunity

- 5.1.3. Regenerative Medicine

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Autologous iPSC Derived Cell Drugs

- 5.2.2. Universal iPSC Derived Cell Drugs

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Ipsc Derived Cell Drugs Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Anti-Inflammatory Repair

- 6.1.2. Tumor Immunity

- 6.1.3. Regenerative Medicine

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Autologous iPSC Derived Cell Drugs

- 6.2.2. Universal iPSC Derived Cell Drugs

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Ipsc Derived Cell Drugs Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Anti-Inflammatory Repair

- 7.1.2. Tumor Immunity

- 7.1.3. Regenerative Medicine

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Autologous iPSC Derived Cell Drugs

- 7.2.2. Universal iPSC Derived Cell Drugs

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Ipsc Derived Cell Drugs Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Anti-Inflammatory Repair

- 8.1.2. Tumor Immunity

- 8.1.3. Regenerative Medicine

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Autologous iPSC Derived Cell Drugs

- 8.2.2. Universal iPSC Derived Cell Drugs

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Ipsc Derived Cell Drugs Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Anti-Inflammatory Repair

- 9.1.2. Tumor Immunity

- 9.1.3. Regenerative Medicine

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Autologous iPSC Derived Cell Drugs

- 9.2.2. Universal iPSC Derived Cell Drugs

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Ipsc Derived Cell Drugs Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Anti-Inflammatory Repair

- 10.1.2. Tumor Immunity

- 10.1.3. Regenerative Medicine

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Autologous iPSC Derived Cell Drugs

- 10.2.2. Universal iPSC Derived Cell Drugs

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Ipsc Derived Cell Drugs Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Anti-Inflammatory Repair

- 11.1.2. Tumor Immunity

- 11.1.3. Regenerative Medicine

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Autologous iPSC Derived Cell Drugs

- 11.2.2. Universal iPSC Derived Cell Drugs

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Shanghai UniXell Biotechnology

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 HELP Therapeutics

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Hopstem Biotechnology

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Nuwacell

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Allele Biotech

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 BlueRock Therapeutics

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Century Therapeutics

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Fate Therapeutics

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Cellino

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Xellsmart

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Shanghai UniXell Biotechnology

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ipsc Derived Cell Drugs Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Ipsc Derived Cell Drugs Revenue (million), by Application 2025 & 2033

- Figure 3: North America Ipsc Derived Cell Drugs Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Ipsc Derived Cell Drugs Revenue (million), by Type 2025 & 2033

- Figure 5: North America Ipsc Derived Cell Drugs Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Ipsc Derived Cell Drugs Revenue (million), by Country 2025 & 2033

- Figure 7: North America Ipsc Derived Cell Drugs Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ipsc Derived Cell Drugs Revenue (million), by Application 2025 & 2033

- Figure 9: South America Ipsc Derived Cell Drugs Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Ipsc Derived Cell Drugs Revenue (million), by Type 2025 & 2033

- Figure 11: South America Ipsc Derived Cell Drugs Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Ipsc Derived Cell Drugs Revenue (million), by Country 2025 & 2033

- Figure 13: South America Ipsc Derived Cell Drugs Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ipsc Derived Cell Drugs Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Ipsc Derived Cell Drugs Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ipsc Derived Cell Drugs Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Ipsc Derived Cell Drugs Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Ipsc Derived Cell Drugs Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Ipsc Derived Cell Drugs Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ipsc Derived Cell Drugs Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Ipsc Derived Cell Drugs Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Ipsc Derived Cell Drugs Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Ipsc Derived Cell Drugs Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Ipsc Derived Cell Drugs Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ipsc Derived Cell Drugs Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ipsc Derived Cell Drugs Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Ipsc Derived Cell Drugs Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Ipsc Derived Cell Drugs Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Ipsc Derived Cell Drugs Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Ipsc Derived Cell Drugs Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Ipsc Derived Cell Drugs Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Ipsc Derived Cell Drugs Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ipsc Derived Cell Drugs Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ipsc Derived Cell Drugs?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the Ipsc Derived Cell Drugs?

Key companies in the market include Shanghai UniXell Biotechnology, HELP Therapeutics, Hopstem Biotechnology, Nuwacell, Allele Biotech, BlueRock Therapeutics, Century Therapeutics, Fate Therapeutics, Cellino, Xellsmart.

3. What are the main segments of the Ipsc Derived Cell Drugs?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 309 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ipsc Derived Cell Drugs," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ipsc Derived Cell Drugs report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ipsc Derived Cell Drugs?

To stay informed about further developments, trends, and reports in the Ipsc Derived Cell Drugs, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence