Key Insights

The Deformity Spinal System market is projected to expand significantly, with an estimated market size of $9.19 billion in the base year 2025, and is expected to grow at a robust Compound Annual Growth Rate (CAGR) of 13.42% by 2033. This substantial growth is attributed to the rising incidence of spinal deformities, including scoliosis and kyphosis, across pediatric and adult demographics. Key drivers include an aging global population experiencing degenerative spinal conditions, alongside heightened awareness and enhanced diagnostic precision. Technological advancements in surgical methodologies, such as minimally invasive techniques and the development of sophisticated implantable devices (e.g., advanced rods, hooks, and pedicle screws), are bolstering market demand by improving patient outcomes and accelerating recovery periods. Moreover, the increasing adoption of personalized treatment strategies and the integration of navigation systems and robotics in spinal surgery are enhancing the efficacy and acceptance of deformity spinal systems.

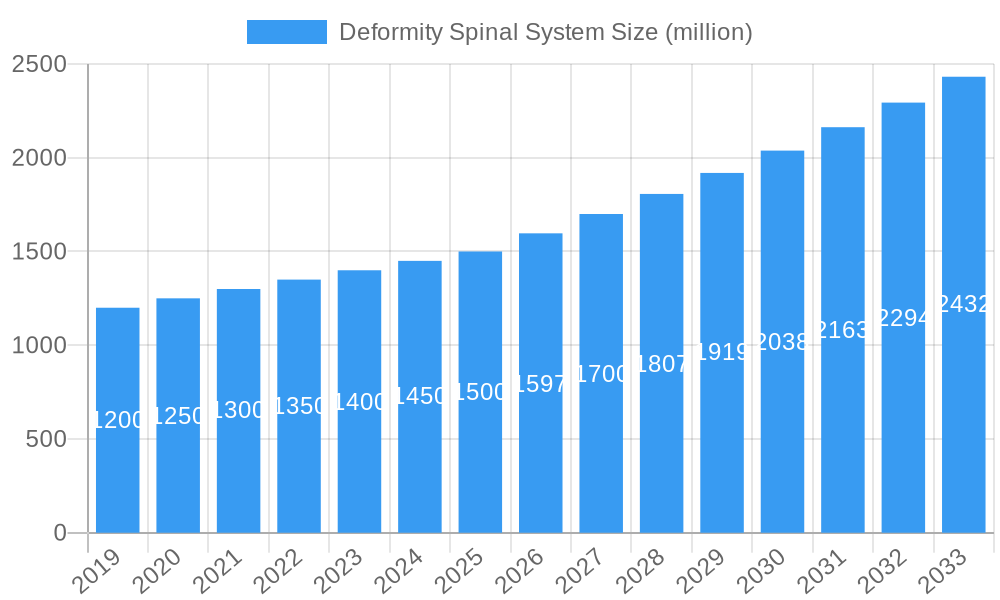

Deformity Spinal System Market Size (In Billion)

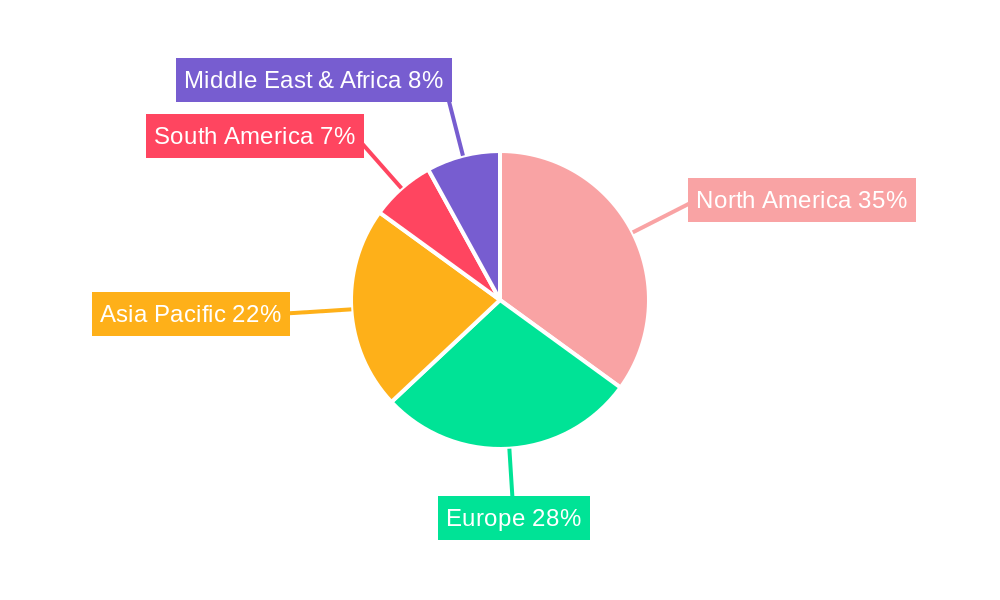

The market is segmented by application and product type, with hospitals and ambulatory surgical centers emerging as principal end-user segments, indicating a trend towards outpatient procedures where appropriate. Foundational product types include rods, hooks, and plates, while pedicle screws provide superior fixation and stability, essential for complex deformity corrections. Geographically, North America leads the market, propelled by a high prevalence of spinal deformities, advanced healthcare infrastructure, and considerable research and development investments from key industry players. However, the Asia Pacific region is anticipated to experience the most rapid growth, driven by escalating healthcare expenditure, a large and expanding patient population, and the increasing footprint of global medical device manufacturers. Potential market restraints, such as the high cost associated with advanced spinal surgeries and the risk of surgical complications, are being mitigated through ongoing innovation and a focused approach on optimized patient selection and surgical training.

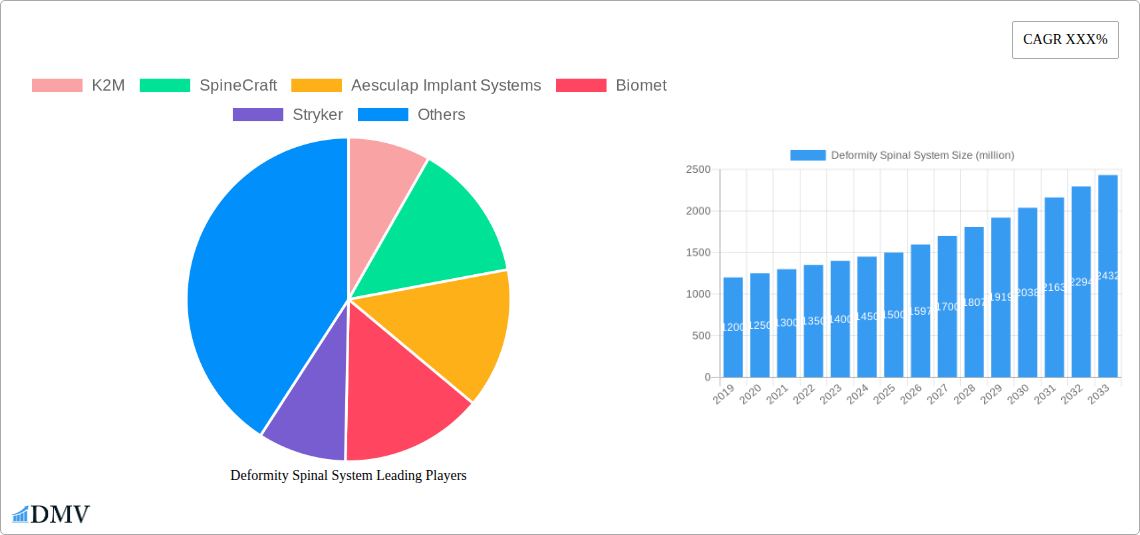

Deformity Spinal System Company Market Share

Deformity Spinal System Market Composition & Trends

The global Deformity Spinal System market is characterized by a moderate level of concentration, with key players like Stryker, NuVasive, and Aesculap Implant Systems holding significant market share. Innovation serves as a primary catalyst, driven by advancements in materials science and surgical techniques aimed at improving patient outcomes and reducing invasiveness. The regulatory landscape, overseen by bodies like the FDA and EMA, plays a crucial role in shaping product development and market access. While direct substitute products for spinal deformity correction are limited, alternative treatment modalities such as physical therapy and less invasive surgical approaches present indirect competition. End-users predominantly comprise hospitals and ambulatory surgical centers, with a growing presence of specialized orthopedic clinics. Mergers and acquisitions (M&A) are a recurring theme, with significant deal values of $1,500 million observed in recent years, indicating strategic consolidation and expansion efforts by major industry participants. For instance, the acquisition of a smaller player by a leading manufacturer in 2023, valued at $800 million, aimed to broaden the product portfolio and enhance market reach. Market share distribution sees leading companies commanding 20% to 25% of the global market. The continuous pursuit of minimally invasive solutions and patient-specific implants underscores the market's dynamic nature. The overall market value is projected to reach $15,000 million by 2033, reflecting sustained growth driven by increasing incidences of spinal deformities and technological advancements.

Deformity Spinal System Industry Evolution

The Deformity Spinal System industry has undergone a remarkable transformation, evolving from rudimentary fixation devices to sophisticated, patient-specific solutions. Over the historical period of 2019–2024, the market witnessed a steady growth trajectory, primarily fueled by an increasing global prevalence of spinal deformities such as scoliosis and kyphosis, particularly in aging populations and as a consequence of congenital conditions. During this period, the market size expanded from an estimated $8,000 million in 2019 to $9,500 million by 2024, representing a compound annual growth rate (CAGR) of approximately 3.5%. Technological advancements have been a pivotal force, with the advent of patient-specific implants, navigated surgery, and robotic-assisted procedures revolutionizing deformity correction. These innovations have led to improved surgical precision, reduced operative times, and enhanced patient recovery. For example, the adoption of intraoperative imaging and navigation systems has seen a substantial increase, now utilized in over 60% of complex spinal deformity surgeries.

The shift in consumer demand has been equally significant. Patients are increasingly seeking less invasive surgical options with shorter hospital stays and faster return to daily activities. This has spurred the development of smaller diameter rods, expandable cages, and low-profile fixation systems. Furthermore, the growing awareness among the general population and healthcare providers about the long-term implications of untreated spinal deformities has contributed to an uptick in surgical interventions. The base year of 2025 is projected to see the market size reach $10,000 million, with a projected CAGR of 6.2% during the forecast period of 2025–2033. This accelerated growth is anticipated due to further technological breakthroughs, including the integration of artificial intelligence in surgical planning and the development of bio-absorbable implants. The increasing investment in research and development by major players, with R&D expenditures averaging 15% of revenue, is a testament to the industry's commitment to innovation. Adoption metrics for advanced technologies, such as 3D-printed implants, are expected to climb from 20% in 2025 to over 50% by 2033.

Leading Regions, Countries, or Segments in Deformity Spinal System

North America currently stands as the dominant region in the Deformity Spinal System market, driven by a confluence of factors that foster innovation, robust healthcare infrastructure, and a high prevalence of spinal deformities. The United States, in particular, contributes significantly to this dominance, boasting advanced healthcare facilities, a high disposable income, and a receptive patient base for advanced surgical interventions. The application segment of Hospitals remains the largest revenue generator within this region, accounting for an estimated 70% of all deformity spinal system procedures. This is attributed to the complexity of deformity correction surgeries often requiring specialized equipment and multidisciplinary teams typically found in hospital settings.

Key drivers contributing to North America's leadership include:

- High Incidence of Spinal Deformities: A large aging population and a significant number of congenital cases contribute to a greater demand for deformity correction.

- Technological Adoption: Early and widespread adoption of advanced technologies like robotic-assisted surgery and patient-specific implants is prevalent.

- Reimbursement Policies: Favorable reimbursement policies for complex spinal surgeries encourage healthcare providers to invest in and offer these procedures.

- R&D Investment: Significant investment in research and development by leading medical device manufacturers, many of which are headquartered in North America, fuels product innovation.

Within the Type segment, Pedicle Screws continue to be the most widely utilized component, forming the backbone of spinal fixation systems. Their versatility and proven efficacy in providing spinal stability make them indispensable in deformity correction. However, the market is witnessing a growing demand for innovative solutions such as interbody cages and specialized rods designed for complex curvatures. Ambulatory Surgical Centers (ASCs) are emerging as a rapidly growing segment within the application category. While complex adolescent idiopathic scoliosis surgeries are still predominantly performed in hospitals, less complex adult degenerative deformity corrections are increasingly being shifted to ASCs, driven by cost-effectiveness and improved patient convenience. This shift is expected to contribute to a 5% annual growth rate in ASC procedures related to spinal deformities. The overall market size in North America is projected to reach $5,500 million by 2033, representing approximately 37% of the global market share. The region's continued emphasis on value-based care and patient outcomes further solidifies its leading position in the Deformity Spinal System landscape.

Deformity Spinal System Product Innovations

Product innovation in the Deformity Spinal System market is rapidly advancing, focusing on improving patient outcomes and streamlining surgical procedures. Key innovations include the development of 3D-printed titanium implants, offering superior biocompatibility and patient-specific customization for optimal bone integration. Expandable cages are gaining traction for their ability to provide adjustable spinal decompression and fusion in situ, minimizing the need for multiple cage sizes. Furthermore, advancements in biomaterials are leading to the creation of novel fusion enhancers and drug-eluting implants designed to accelerate bone healing and reduce infection rates. These technological leaps are driven by a commitment to creating less invasive, more effective, and safer solutions for complex spinal deformities.

Propelling Factors for Deformity Spinal System Growth

The growth of the Deformity Spinal System market is propelled by a synergistic interplay of several factors.

- Increasing Prevalence of Spinal Deformities: A growing global aging population, coupled with a rise in congenital and degenerative spinal conditions, is significantly boosting demand for corrective surgical interventions.

- Technological Advancements: Continuous innovation in implant design, navigation systems, and robotic-assisted surgery enhances surgical precision, reduces invasiveness, and improves patient outcomes, thereby driving adoption.

- Favorable Reimbursement Policies: In many developed nations, reimbursement structures adequately cover complex spinal surgeries, making these procedures more accessible to a wider patient population.

- Growing Awareness and Patient Demand: Increased public awareness about spinal health and the benefits of corrective surgery, alongside a growing patient preference for minimally invasive procedures, are key drivers.

- Investment in R&D: Significant investment by major players in research and development ensures a pipeline of innovative products and surgical techniques, further fueling market expansion.

Obstacles in the Deformity Spinal System Market

Despite robust growth, the Deformity Spinal System market faces several significant obstacles. High procedural costs associated with advanced implants and surgical technologies can be a substantial barrier to access, particularly in emerging economies. Stringent regulatory approval processes for novel spinal devices can lead to extended development timelines and increased R&D expenses, impacting market entry. Supply chain disruptions, as witnessed in recent global events, can lead to material shortages and increased manufacturing costs. Intense competition among established players and emerging entrants also exerts pressure on pricing and profit margins. Furthermore, the risk of surgical complications and the need for extensive rehabilitation can create apprehension among some patient populations. The potential for implant-related infections, although decreasing with advancements, remains a persistent concern.

Future Opportunities in Deformity Spinal System

The Deformity Spinal System market is ripe with future opportunities, primarily driven by emerging technologies and unmet patient needs. The burgeoning field of personalized medicine presents a significant opportunity for patient-specific implants, leveraging advanced imaging and 3D printing to create highly customized solutions. Growth in emerging economies, with their expanding healthcare infrastructure and increasing disposable incomes, offers a vast untapped market potential. The development of bio-integrated and regenerative medicine approaches, such as stem cell therapies and biodegradable scaffolds, holds promise for enhancing fusion rates and reducing the need for revision surgeries. Furthermore, the increasing demand for minimally invasive techniques will continue to drive innovation in endoscopic and robotic surgical platforms, creating new avenues for growth. The integration of AI in surgical planning and outcome prediction also represents a substantial opportunity for improving efficiency and patient care.

Major Players in the Deformity Spinal System Ecosystem

- K2M

- SpineCraft

- Aesculap Implant Systems

- Biomet

- Stryker

- Z-Medical

- NuVasive

Key Developments in Deformity Spinal System Industry

- 2023 August: Stryker launches a new generation of expandable cages designed for enhanced intraoperative adjustability and improved patient comfort.

- 2023 May: NuVasive announces expanded clinical trial data for its minimally invasive deformity correction system, demonstrating reduced blood loss and shorter hospital stays.

- 2022 December: Aesculap Implant Systems receives FDA approval for its novel posterior spinal instrumentation system, offering greater flexibility and biomechanical stability.

- 2022 June: Biomet announces a strategic partnership to advance the development of 3D-printed titanium implants for complex spinal deformities.

- 2021 September: K2M introduces a comprehensive suite of patient-specific rod and screw solutions for adolescent idiopathic scoliosis correction.

Strategic Deformity Spinal System Market Forecast

The Deformity Spinal System market is poised for robust growth, projected to reach $15,000 million by 2033, with an estimated CAGR of 6.2% from 2025 to 2033. This forecast is underpinned by continuous technological innovation, such as the increasing adoption of AI-driven surgical planning and 3D-printed implants, which enhance precision and patient-specific solutions. The rising global incidence of spinal deformities, particularly among the aging population, alongside a growing emphasis on minimally invasive procedures, will further fuel market expansion. Strategic investments in research and development by leading companies and favorable reimbursement policies in key regions will continue to propel the market forward, creating significant opportunities for stakeholders seeking to capitalize on the evolving landscape of spinal deformity correction.

Deformity Spinal System Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Ambulatory Surgical Centers

- 1.3. Others

-

2. Type

- 2.1. Rods

- 2.2. Hooks

- 2.3. Plates

- 2.4. Cages

- 2.5. Pedicle Screws

Deformity Spinal System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Deformity Spinal System Regional Market Share

Geographic Coverage of Deformity Spinal System

Deformity Spinal System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.42% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Ambulatory Surgical Centers

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Rods

- 5.2.2. Hooks

- 5.2.3. Plates

- 5.2.4. Cages

- 5.2.5. Pedicle Screws

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Deformity Spinal System Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Ambulatory Surgical Centers

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Rods

- 6.2.2. Hooks

- 6.2.3. Plates

- 6.2.4. Cages

- 6.2.5. Pedicle Screws

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Deformity Spinal System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Ambulatory Surgical Centers

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Rods

- 7.2.2. Hooks

- 7.2.3. Plates

- 7.2.4. Cages

- 7.2.5. Pedicle Screws

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Deformity Spinal System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Ambulatory Surgical Centers

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Rods

- 8.2.2. Hooks

- 8.2.3. Plates

- 8.2.4. Cages

- 8.2.5. Pedicle Screws

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Deformity Spinal System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Ambulatory Surgical Centers

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Rods

- 9.2.2. Hooks

- 9.2.3. Plates

- 9.2.4. Cages

- 9.2.5. Pedicle Screws

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Deformity Spinal System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Ambulatory Surgical Centers

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Rods

- 10.2.2. Hooks

- 10.2.3. Plates

- 10.2.4. Cages

- 10.2.5. Pedicle Screws

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Deformity Spinal System Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Ambulatory Surgical Centers

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Rods

- 11.2.2. Hooks

- 11.2.3. Plates

- 11.2.4. Cages

- 11.2.5. Pedicle Screws

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 K2M

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 SpineCraft

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Aesculap Implant Systems

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Biomet

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Stryker

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Z-Medical

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 NuVasive

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 K2M

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Deformity Spinal System Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Deformity Spinal System Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Deformity Spinal System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Deformity Spinal System Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Deformity Spinal System Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Deformity Spinal System Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Deformity Spinal System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Deformity Spinal System Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Deformity Spinal System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Deformity Spinal System Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Deformity Spinal System Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Deformity Spinal System Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Deformity Spinal System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Deformity Spinal System Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Deformity Spinal System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Deformity Spinal System Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Deformity Spinal System Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Deformity Spinal System Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Deformity Spinal System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Deformity Spinal System Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Deformity Spinal System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Deformity Spinal System Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Deformity Spinal System Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Deformity Spinal System Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Deformity Spinal System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Deformity Spinal System Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Deformity Spinal System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Deformity Spinal System Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Deformity Spinal System Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Deformity Spinal System Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Deformity Spinal System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Deformity Spinal System Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Deformity Spinal System Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Deformity Spinal System Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Deformity Spinal System Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Deformity Spinal System Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Deformity Spinal System Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Deformity Spinal System Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Deformity Spinal System Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Deformity Spinal System Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Deformity Spinal System Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Deformity Spinal System Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Deformity Spinal System Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Deformity Spinal System Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Deformity Spinal System Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Deformity Spinal System Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Deformity Spinal System Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Deformity Spinal System Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Deformity Spinal System Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Deformity Spinal System Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Deformity Spinal System?

The projected CAGR is approximately 13.42%.

2. Which companies are prominent players in the Deformity Spinal System?

Key companies in the market include K2M, SpineCraft, Aesculap Implant Systems, Biomet, Stryker, Z-Medical, NuVasive.

3. What are the main segments of the Deformity Spinal System?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.19 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Deformity Spinal System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Deformity Spinal System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Deformity Spinal System?

To stay informed about further developments, trends, and reports in the Deformity Spinal System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence