Key Insights

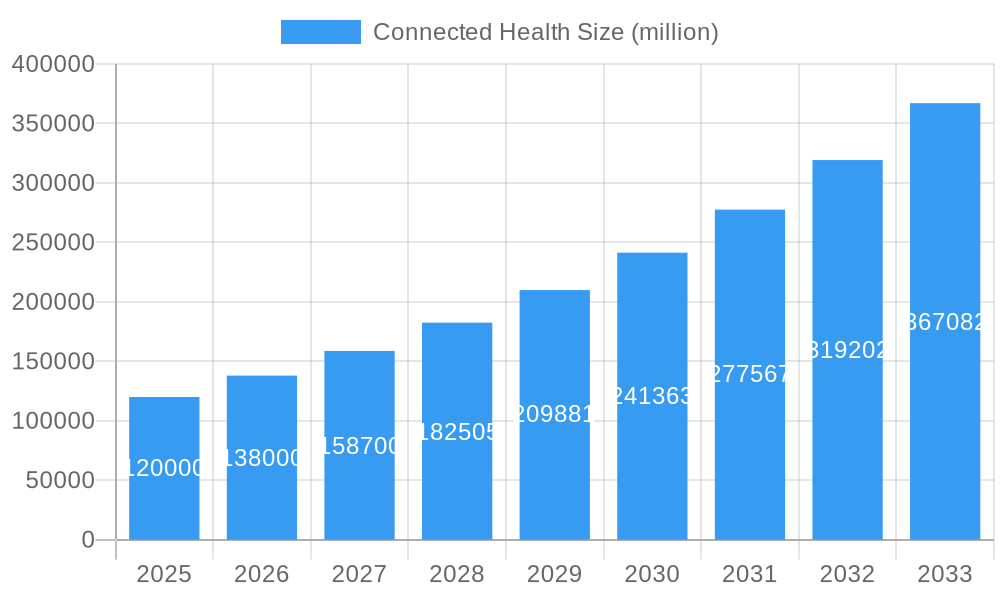

The global Connected Health market is projected for significant expansion, driven by the increasing adoption of remote patient monitoring and the rising prevalence of chronic diseases. With an estimated market size of 61.76 billion in the base year of 2025, the sector is anticipated to witness a Compound Annual Growth Rate (CAGR) of approximately 27.6% throughout the forecast period. This growth is fundamentally fueled by the escalating demand for personalized and proactive healthcare solutions, advancements in IoT and AI technologies, and a greater emphasis on preventive care and wellness. The aging global population and the subsequent rise in age-related health conditions further underscore the need for accessible and efficient healthcare delivery, a role that connected health solutions are ideally positioned to fulfill. Government initiatives promoting digital health infrastructure and increasing investments in healthcare technology are also significant accelerators. The market's trajectory points towards a future where healthcare is more integrated, data-driven, and patient-centric, transforming traditional care models.

Connected Health Market Size (In Billion)

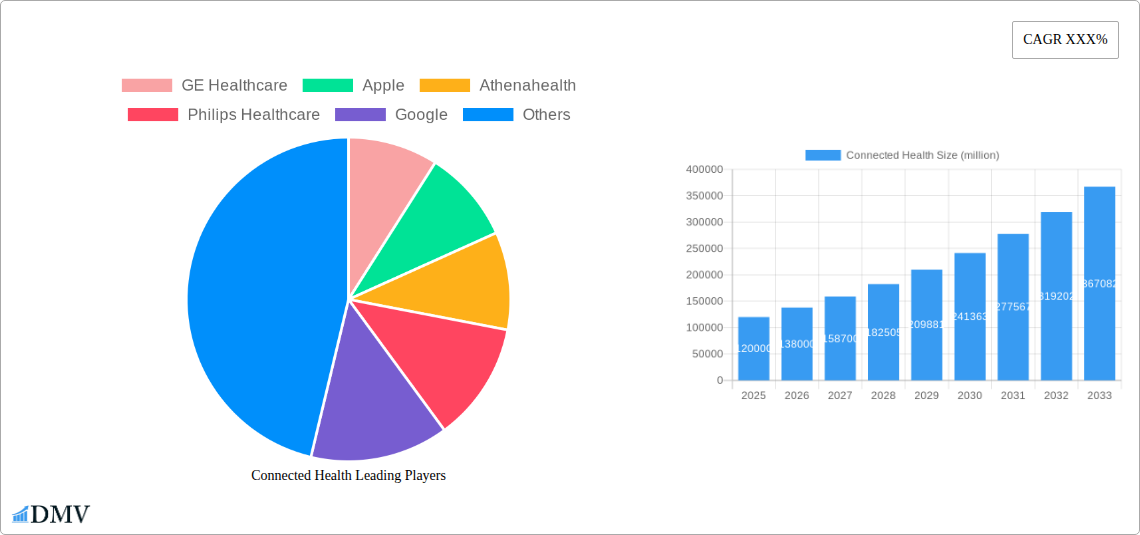

The Connected Health market is segmented by application into Hospitals and Individual Customers. Hospitals currently represent a larger share due to their comprehensive integration of these technologies for patient management and care coordination. However, the Individual Customer segment is poised for rapid growth, propelled by the proliferation of wearable devices, mobile health applications, and home-based monitoring solutions. By type, Monitoring Devices and Diagnostic and Treatment Devices form the key segments, with monitoring devices leading adoption. Key players such as GE Healthcare, Philips Healthcare, Apple, and Google are heavily investing in research and development, introducing innovative solutions that enhance patient outcomes and operational efficiency. Emerging markets, particularly in the Asia Pacific region, show significant potential due to increasing healthcare expenditure and growing digital infrastructure. However, challenges such as data security concerns, regulatory hurdles, and the need for interoperability across different platforms require strategic attention to fully realize the market's potential.

Connected Health Company Market Share

Connected Health Market: A Comprehensive Analysis (2019–2033)

This in-depth report provides a detailed analysis of the burgeoning Connected Health market, encompassing its current landscape, historical performance, and future projections from 2019 to 2033. Examining key segments, technological innovations, and the competitive dynamics driven by industry giants like GE Healthcare, Apple, Philips Healthcare, Google, and Microsoft, this report offers invaluable insights for stakeholders seeking to navigate this rapidly evolving sector. With a base year of 2025 and a forecast period extending to 2033, this analysis is crucial for understanding the transformative impact of digital health on healthcare delivery and patient outcomes.

Connected Health Market Composition & Trends

The Connected Health market is characterized by a dynamic interplay of innovation, strategic partnerships, and evolving regulatory frameworks. Market concentration, while influenced by a few dominant players such as GE Healthcare, Apple, and Philips Healthcare, also features a growing ecosystem of specialized firms and startups. Innovation catalysts, including advancements in AI, IoT, and wearable technology, are continuously reshaping product offerings and service delivery models. Regulatory landscapes, particularly in regions like North America and Europe, are adapting to accommodate the influx of digital health solutions, fostering both growth and compliance challenges. The presence of substitute products, ranging from traditional medical devices to nascent telehealth platforms, necessitates a clear differentiation strategy. End-user profiles are diversifying, encompassing not only hospitals and healthcare providers but also individual consumers actively seeking personalized health management tools. Mergers and acquisitions (M&A) activities remain a significant trend, with deal values often in the million range, as larger entities seek to consolidate market share and acquire cutting-edge technologies. For instance, recent M&A activities have seen companies like Athenahealth and Allscripts exploring strategic consolidations to enhance their integrated healthcare IT offerings. Market share distribution is influenced by product adoption rates and strategic alliances, with key companies vying for dominance in areas like remote patient monitoring and chronic disease management.

- Market Share Distribution: Influenced by adoption rates of wearable health trackers and remote monitoring systems.

- M&A Deal Values: Ranging from tens of million to hundreds of million, driven by the acquisition of innovative AI-driven diagnostic platforms and data analytics capabilities.

- Innovation Catalysts: Rise of AI-powered diagnostics, IoT-enabled patient monitoring, and personalized wellness apps.

- Regulatory Landscapes: Increasing focus on data privacy (e.g., GDPR, HIPAA) and interoperability standards for seamless data exchange between devices and Electronic Health Records (EHRs).

- Substitute Products: Competition from traditional medical devices, standalone health apps, and emerging AI-driven health assessment tools.

- End-User Profiles: Hospitals, clinics, individual customers, pharmaceutical companies (e.g., F. Hoffmann-La Roche), and employers focusing on corporate wellness.

- M&A Activities: Strategic acquisitions to enhance product portfolios and market reach.

Connected Health Industry Evolution

The Connected Health industry has undergone a profound transformation, evolving from nascent remote monitoring solutions to a comprehensive digital health ecosystem. The study period, 2019–2024, witnessed significant foundational growth, fueled by increased awareness of proactive health management and the growing prevalence of chronic diseases. The base year of 2025 marks a pivotal point, with accelerated adoption rates driven by technological maturity and greater consumer acceptance. The forecast period, 2025–2033, is poised for exponential expansion, projecting a Compound Annual Growth Rate (CAGR) of approximately xx%. This growth is underpinned by several key factors:

- Technological Advancements: The integration of Artificial Intelligence (AI) and Machine Learning (ML) into diagnostic and treatment devices is revolutionizing precision medicine and early disease detection. Companies like Google and Microsoft are heavily investing in AI-driven health analytics platforms, processing vast datasets to provide actionable insights for both clinicians and patients. The proliferation of Internet of Things (IoT) devices, from smart wearables by Apple and OMRON to sophisticated hospital monitoring systems by GE Healthcare and Philips Healthcare, enables continuous, real-time data collection. Qualcomm's advancements in connectivity solutions are crucial for seamless data transfer across these devices.

- Shifting Consumer Demands: There is a discernible shift in consumer behavior towards greater personal health responsibility. Individuals are increasingly seeking convenient, accessible, and personalized health management solutions. The rise of direct-to-consumer (DTC) connected health devices, such as those offered by Abbott for glucose monitoring or HP for health tracking, caters to this demand. The convenience of telehealth services, facilitated by platforms like Athenahealth and Allscripts, further empowers individuals to manage their health from the comfort of their homes. Evolent Health is also playing a role in shaping consumer engagement through value-based care models.

- Market Growth Trajectories: The market for connected health devices is projected to reach several hundred million by the end of the forecast period. Growth in the diagnostic and treatment devices segment, driven by innovations from Medtronic and Johnson & Johnson, is expected to outpace that of monitoring devices, although the latter will remain a substantial market. The hospital segment will continue to be a major adopter due to the need for improved patient care efficiency and reduced readmission rates. However, the individual customer segment is anticipated to grow at a faster pace, propelled by increased health consciousness and the availability of affordable consumer-grade devices. Skyscape's contributions in developing robust mobile health solutions for healthcare professionals are also impacting the industry's growth trajectory. Zebra Technologies' role in asset tracking and workflow optimization within healthcare settings is another critical element of this evolving landscape.

The industry's evolution is marked by a move from fragmented solutions to integrated platforms, emphasizing interoperability and data-driven decision-making. The influence of major players like Epic Systems in EHR integration and Huawei in providing underlying connectivity infrastructure further solidifies the industry's robust growth path.

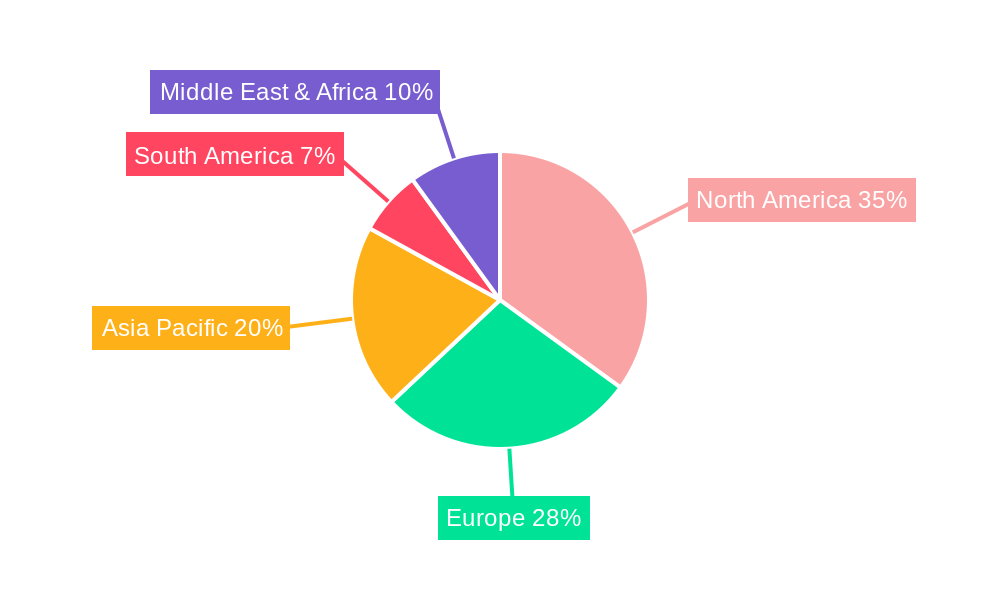

Leading Regions, Countries, or Segments in Connected Health

The Hospitals segment, particularly within North America (specifically the United States), stands as the dominant force in the Connected Health market. This leadership is driven by a confluence of robust healthcare infrastructure, significant investment in advanced medical technologies, and a proactive regulatory environment that encourages innovation and adoption. The sheer scale of the US healthcare system, coupled with a high prevalence of chronic diseases, creates a substantial demand for connected health solutions.

- Key Drivers for Hospital Dominance in North America:

- High Healthcare Spending: The US consistently leads in per capita healthcare expenditure, enabling hospitals to invest in cutting-edge connected health technologies to improve patient outcomes and operational efficiency. Investments in remote patient monitoring systems and AI-powered diagnostic tools are particularly strong.

- Regulatory Support and Incentives: Government initiatives and reimbursement policies, such as those supporting telehealth and remote patient monitoring for Medicare beneficiaries, have significantly boosted adoption. The push for interoperability standards also encourages the integration of diverse connected health devices into existing hospital workflows.

- Technological Adoption: Hospitals are early adopters of advanced technologies. Companies like GE Healthcare, Philips Healthcare, and Medtronic are at the forefront of providing sophisticated connected devices and platforms tailored for clinical settings. The demand for integrated systems that can streamline patient care, reduce hospital readmissions, and enhance data analytics is immense.

- Focus on Value-Based Care: The shift towards value-based care models incentivizes hospitals to invest in solutions that improve patient health outcomes and reduce overall healthcare costs. Connected health technologies play a pivotal role in enabling continuous patient monitoring and proactive intervention, aligning perfectly with these value-based objectives. Epic Systems, a major EHR vendor, plays a crucial role in facilitating the integration of these technologies within hospital IT infrastructures.

- Strong Presence of Major Players: The presence of major connected health players like GE Healthcare, Apple, Athenahealth, Philips Healthcare, Google, Abbott, Allscripts, HP, Johnson & Johnson, Microsoft, Medtronic, and Epic Systems in the North American market ensures a constant flow of innovative products and services, further solidifying its leadership position.

While Individual Customers represent a rapidly growing segment, driven by increased health consciousness and the accessibility of wearable devices and mobile health apps, hospitals currently represent the largest revenue-generating and most influential segment due to the scale of their procurements and their central role in healthcare delivery. The Diagnostic and Treatment Devices type is also seeing robust growth, propelled by advancements in areas like AI-assisted surgery and personalized therapeutic devices, further cementing the dominance of the hospital segment and North America's leadership.

Connected Health Product Innovations

The Connected Health landscape is continuously reshaped by groundbreaking product innovations that enhance patient care and operational efficiency. Abbott's FreeStyle Libre series, for instance, has revolutionized continuous glucose monitoring for individuals with diabetes, offering a user-friendly, connected experience. Apple's Watch series continues to push boundaries in consumer health tracking, incorporating advanced sensors for ECG, blood oxygen, and fall detection. GE Healthcare and Philips Healthcare are leading the charge in developing connected diagnostic imaging equipment and sophisticated remote patient monitoring systems for critical care units, enabling real-time data analysis and proactive intervention. Medtronic's advancements in connected pacemakers and insulin pumps offer greater patient autonomy and remote physician oversight. OMRON's connected blood pressure monitors and scales empower individuals to track vital health metrics with ease. These innovations are characterized by their enhanced accuracy, seamless connectivity, user-centric design, and the integration of AI for predictive analytics, offering unique selling propositions that drive market adoption and redefine the standard of care.

Propelling Factors for Connected Health Growth

The growth of the Connected Health market is propelled by a potent combination of technological advancements, favorable economic conditions, and supportive regulatory frameworks.

- Technological Advancements: The rapid evolution of AI, IoT, 5G connectivity, and advanced sensor technology fuels the development of more sophisticated and accessible connected health devices.

- Growing Health Consciousness: An increasing global awareness of preventive healthcare and wellness drives consumer demand for personal health monitoring tools and digital health solutions.

- Rising Chronic Disease Burden: The escalating prevalence of chronic conditions necessitates continuous monitoring and proactive management, for which connected health technologies are ideally suited.

- Government Initiatives and Reimbursement: Supportive government policies, funding for digital health research, and reimbursement for telehealth and remote patient monitoring services create a conducive market environment.

- Investment and Funding: Significant investment from venture capitalists and strategic partnerships among industry players like Google, Microsoft, and Apple inject capital into innovation and market expansion.

Obstacles in the Connected Health Market

Despite its promising trajectory, the Connected Health market faces several significant obstacles.

- Regulatory Hurdles and Data Privacy Concerns: Navigating diverse and evolving regulatory landscapes across different geographies presents a considerable challenge. Strict data privacy regulations, such as HIPAA and GDPR, necessitate robust security measures, which can increase development and operational costs.

- Interoperability Challenges: Achieving seamless data exchange between disparate devices and healthcare systems remains a persistent issue. Lack of standardization can hinder the integration of solutions from various vendors, limiting the full potential of connected health ecosystems.

- High Initial Investment Costs: The development and implementation of advanced connected health infrastructure, particularly for healthcare institutions, can involve substantial upfront capital expenditure.

- Cybersecurity Threats: The increasing reliance on digital data makes connected health systems vulnerable to cyberattacks, which can compromise patient data integrity and pose risks to patient safety. The potential impact of a major data breach could run into hundreds of million in fines and reputational damage.

- Digital Divide and Accessibility: Unequal access to reliable internet connectivity and digital literacy can limit the adoption of connected health solutions in certain demographics and underserved regions.

Future Opportunities in Connected Health

The future of Connected Health is replete with promising opportunities, driven by emerging trends and unmet needs.

- Personalized and Predictive Healthcare: Advancements in AI and data analytics will unlock hyper-personalized treatment plans and predictive diagnostics, moving healthcare from reactive to proactive.

- Expansion in Remote and Home-Based Care: The growing demand for aging-in-place solutions and the convenience of remote care will fuel the market for advanced home monitoring systems and telehealth platforms.

- Integration with Wearable Technology: Deeper integration of medical-grade sensors into consumer wearables will enable more comprehensive health tracking and early disease detection.

- Emerging Markets: Untapped potential exists in developing economies where the adoption of mobile technology is high, offering an opportunity to leapfrog traditional healthcare infrastructure with connected solutions.

- Digital Therapeutics: The development and adoption of regulated digital therapeutics will offer new avenues for treating various conditions through software-based interventions.

Major Players in the Connected Health Ecosystem

- GE Healthcare

- Apple

- Athenahealth

- Philips Healthcare

- Abbott

- Allscripts

- F. Hoffmann-La Roche

- HP

- Johnson & Johnson

- Microsoft

- OMRON

- Huawei

- Evolent Health

- Epic Systems

- Medtronic

- Zebra Technologies

- Qualcomm

- Skyscape

Key Developments in Connected Health Industry

- 2019: Launch of Apple's ECG app and irregular rhythm notification feature, enhancing cardiac monitoring capabilities.

- 2020: Increased adoption of telehealth platforms like those from Athenahealth and Allscripts due to the COVID-19 pandemic, accelerating remote patient consultations.

- 2021: GE Healthcare and Philips Healthcare announce significant investments in AI-powered diagnostic imaging solutions for improved accuracy and efficiency.

- 2022: Abbott's FreeStyle Libre 3 receives FDA clearance, offering a smaller and more accurate continuous glucose monitoring system.

- 2023: Google's Verily and Qualcomm collaborate on next-generation wearable health sensors for advanced physiological monitoring.

- 2024: Medtronic expands its portfolio of connected insulin pumps and pacemakers, emphasizing remote data management for chronic disease patients.

- 2025 (Estimated): Increased integration of predictive analytics by companies like Microsoft and Google in healthcare platforms to identify at-risk patients proactively.

- 2026 (Forecast): Huawei to further enhance connectivity solutions for medical IoT devices, ensuring seamless data flow in healthcare settings.

- 2028 (Forecast): Johnson & Johnson to leverage connected devices for enhanced rehabilitation and post-operative care solutions.

- 2030 (Forecast): F. Hoffmann-La Roche to explore more advanced AI-driven drug discovery and personalized treatment pathways utilizing connected health data.

- 2033 (Forecast): Widespread adoption of fully integrated digital health ecosystems powered by advanced AI and IoT across healthcare institutions and individual homes.

Strategic Connected Health Market Forecast

The strategic forecast for the Connected Health market remains exceptionally strong, driven by an unyielding demand for efficient, personalized, and accessible healthcare solutions. The increasing integration of AI and IoT technologies will foster a new era of predictive and preventive medicine, significantly reducing the burden of chronic diseases and improving patient outcomes. Future growth catalysts include the expanding use of digital therapeutics, the continued innovation in wearable health technology, and the untapped potential in emerging markets. As regulatory frameworks mature and interoperability challenges are addressed, the market is poised for sustained expansion, with significant opportunities for stakeholders to innovate and capitalize on the transformation of global healthcare delivery. The market is projected to reach several hundred million by 2033, reflecting robust CAGR.

Connected Health Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Individual Customers

- 1.3. Others

-

2. Type

- 2.1. Monitoring Devices

- 2.2. Diagnostic and Treatment Devices

Connected Health Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Connected Health Regional Market Share

Geographic Coverage of Connected Health

Connected Health REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 27.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Individual Customers

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Monitoring Devices

- 5.2.2. Diagnostic and Treatment Devices

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Connected Health Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Individual Customers

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Monitoring Devices

- 6.2.2. Diagnostic and Treatment Devices

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Connected Health Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Individual Customers

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Monitoring Devices

- 7.2.2. Diagnostic and Treatment Devices

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Connected Health Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Individual Customers

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Monitoring Devices

- 8.2.2. Diagnostic and Treatment Devices

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Connected Health Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Individual Customers

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Monitoring Devices

- 9.2.2. Diagnostic and Treatment Devices

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Connected Health Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Individual Customers

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Monitoring Devices

- 10.2.2. Diagnostic and Treatment Devices

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Connected Health Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Individual Customers

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Monitoring Devices

- 11.2.2. Diagnostic and Treatment Devices

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 GE Healthcare

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Apple

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Athenahealth

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Philips Healthcare

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Google

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Abbott

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Allscripts

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 F. Hoffmann-La Roche

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 HP

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Johnson & Johnson

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Microsoft

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 OMRON

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Huawei

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Evolent Health

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Epic Systems

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Medtronic

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Zebra Technologies

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Qualcomm

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Skyscape

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.1 GE Healthcare

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Connected Health Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Connected Health Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Connected Health Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Connected Health Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Connected Health Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Connected Health Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Connected Health Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Connected Health Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Connected Health Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Connected Health Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Connected Health Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Connected Health Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Connected Health Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Connected Health Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Connected Health Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Connected Health Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Connected Health Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Connected Health Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Connected Health Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Connected Health Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Connected Health Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Connected Health Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Connected Health Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Connected Health Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Connected Health Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Connected Health Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Connected Health Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Connected Health Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Connected Health Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Connected Health Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Connected Health Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Connected Health Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Connected Health Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Connected Health Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Connected Health Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Connected Health Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Connected Health Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Connected Health Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Connected Health Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Connected Health Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Connected Health Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Connected Health Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Connected Health Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Connected Health Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Connected Health Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Connected Health Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Connected Health Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Connected Health Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Connected Health Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Connected Health Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Connected Health?

The projected CAGR is approximately 27.6%.

2. Which companies are prominent players in the Connected Health?

Key companies in the market include GE Healthcare, Apple, Athenahealth, Philips Healthcare, Google, Abbott, Allscripts, F. Hoffmann-La Roche, HP, Johnson & Johnson, Microsoft, OMRON, Huawei, Evolent Health, Epic Systems, Medtronic, Zebra Technologies, Qualcomm, Skyscape.

3. What are the main segments of the Connected Health?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 61.76 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Connected Health," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Connected Health report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Connected Health?

To stay informed about further developments, trends, and reports in the Connected Health, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence