Key Insights

The global Commodity Chemicals market is poised for significant expansion, projected to reach a substantial market size in 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) over the forecast period, indicating sustained demand and increasing value within the sector. The broad applications of commodity chemicals across diverse industries, from healthcare and biotechnology to advanced scientific research and education, serve as primary growth drivers. Hospitals rely on these chemicals for sterilization and diagnostics, biotechnology firms for R&D and manufacturing, and academic institutions for fundamental research and training. The "Others" segment, encompassing a wide array of industrial applications, further contributes to this expansive demand. The market's dynamism is also reflected in its segmentation by type, with Organics, Inorganics, Plastics Resins, Synthetic Rubbers, and Fibers representing core product categories experiencing consistent uptake.

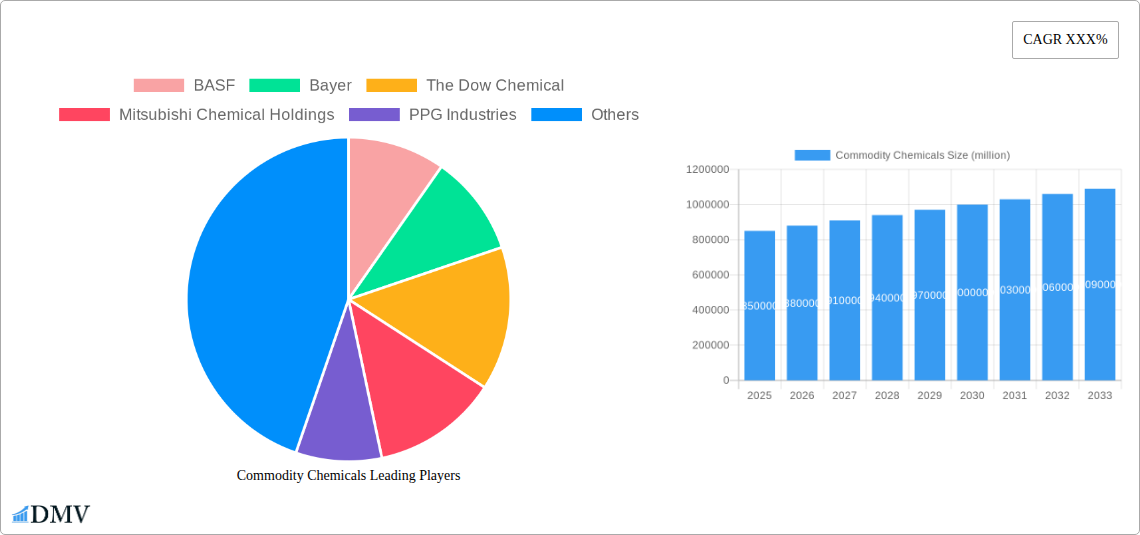

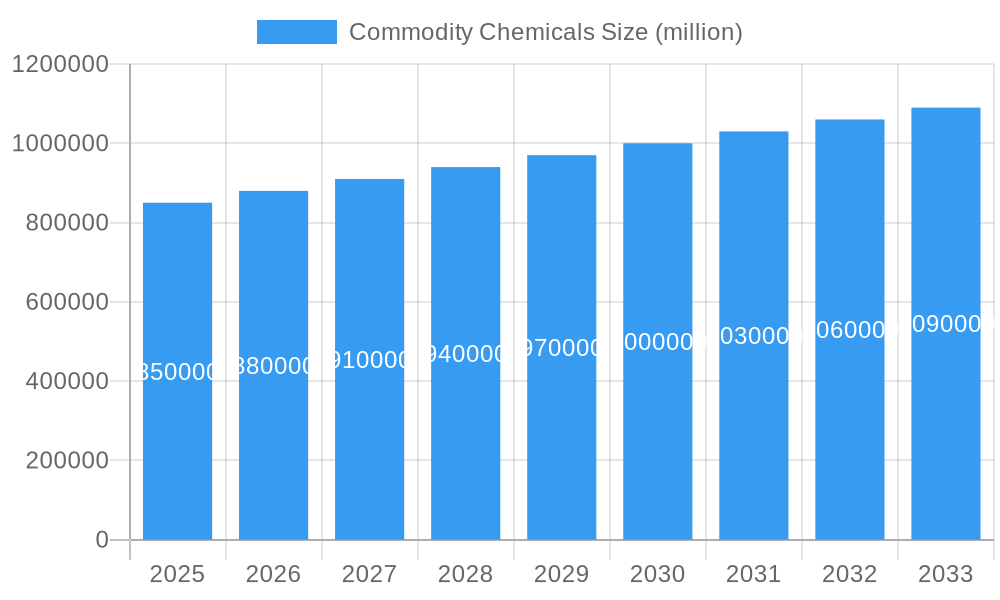

Commodity Chemicals Market Size (In Billion)

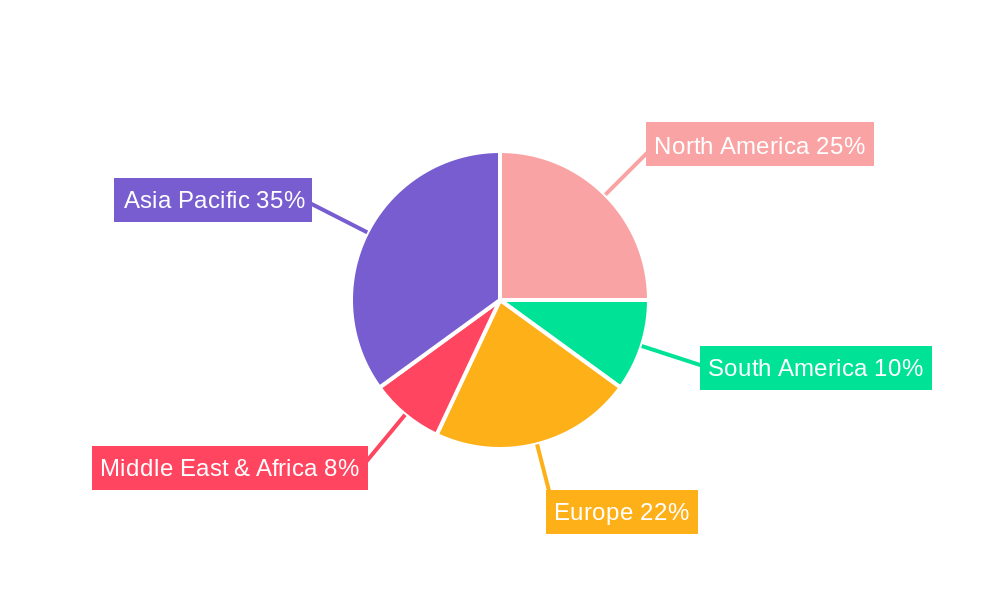

Further fueling market expansion are key trends such as the increasing emphasis on sustainable chemical production, the development of bio-based alternatives, and the growing demand for high-performance materials in sectors like automotive and construction. The rising middle class in developing economies, particularly in the Asia Pacific region, is a significant contributor to this growth, boosting consumption across various end-use industries. However, the market is not without its challenges. Fluctuations in raw material prices, stringent environmental regulations, and intense competition among major players like BASF, Bayer, The Dow Chemical, and Mitsubishi Chemical Holdings, among others, can act as restraints. Geographically, the Asia Pacific region is expected to lead in market share due to its rapid industrialization and large consumer base, followed by North America and Europe, which are characterized by mature markets and advanced technological adoption.

Commodity Chemicals Company Market Share

Here's an SEO-optimized, insightful report description for the Commodity Chemicals market, designed for immediate use without modification.

Commodity Chemicals Market Composition & Trends

The global commodity chemicals market, a foundational pillar of modern industry, exhibits a dynamic and evolving landscape. Market concentration remains significant, with major players like BASF, The Dow Chemical, and LyondellBasell Industries holding substantial shares. Innovation catalysts are increasingly driven by sustainability initiatives, the demand for higher-performance materials, and advancements in catalysis and process optimization. The regulatory environment is a critical factor, with evolving policies on environmental impact, safety standards, and chemical registration influencing production and market access. Substitute products, particularly in the plastics and petrochemicals segments, are emerging from bio-based and recycled feedstocks, posing a long-term challenge. End-user profiles are diversifying, with significant demand emanating from burgeoning sectors like healthcare, electronics, and renewable energy, alongside traditional industries. Mergers and acquisitions (M&A) activity continues to shape the market, with recent deals indicating a trend towards consolidation and strategic portfolio adjustments. For instance, the M&A deal value in the last three years reached approximately XXX million, reflecting a strong appetite for inorganic growth and synergistic integration. The market share distribution is currently characterized by a few dominant entities controlling over 50% of the total market valuation, underscoring the competitive intensity and the strategic importance of scale.

Commodity Chemicals Industry Evolution

The commodity chemicals industry has undergone a profound transformation over the historical period of 2019–2024, characterized by remarkable market growth trajectories, rapid technological advancements, and a discernible shift in consumer demands. During this period, the global market experienced an average annual growth rate of approximately 4.5%, a testament to its essential role across a vast array of downstream industries. Technological advancements have been pivotal, with significant investments in process intensification, digitalization of manufacturing, and the development of more efficient and environmentally friendly production methods. The adoption of advanced catalytic processes, for example, has led to a reduction in energy consumption by up to 15% in key petrochemical operations, thereby improving profitability and sustainability. Furthermore, the rise of the circular economy has spurred innovation in chemical recycling technologies, enabling the recovery and reuse of valuable materials from waste streams, a trend expected to accelerate in the coming forecast period. Shifting consumer demands, particularly a heightened awareness of environmental sustainability and product safety, have also reshaped the industry. This has led to an increased demand for bio-based chemicals, biodegradable plastics, and products with lower carbon footprints. The industry's response has been to invest heavily in research and development of green chemistry solutions and sustainable sourcing strategies. For example, the demand for bio-plastics saw a compound annual growth rate (CAGR) of over 10% from 2019 to 2024. The base year of 2025 marks a critical juncture, with the industry poised for continued expansion, driven by these interwoven factors of technological prowess, evolving consumer preferences, and the imperative for sustainable practices. The estimated market valuation in 2025 is projected to reach over XXX million.

Leading Regions, Countries, or Segments in Commodity Chemicals

The Asia-Pacific region stands as the undisputed leader in the global commodity chemicals market, demonstrating unparalleled dominance across multiple product types and applications. Within this expansive region, China has emerged as a powerhouse, driven by a confluence of factors including robust industrialization, massive domestic demand, and substantial government support for the chemical sector. The country’s extensive manufacturing capabilities and its position as a global supply chain hub contribute significantly to its leading role.

Key Drivers of Dominance in Asia-Pacific:

- Massive Industrial Base: The presence of a vast and growing manufacturing sector across industries such as automotive, electronics, construction, and textiles creates a colossal demand for commodity chemicals like plastics, petrochemicals, and inorganics.

- Government Support and Investment: Favorable government policies, including subsidies, tax incentives, and strategic investments in infrastructure and R&D, have fueled rapid capacity expansion and technological upgrades in the Chinese chemical industry.

- Growing Middle Class and Consumer Demand: A rapidly expanding middle class in countries like China and India fuels demand for a wide range of consumer goods, directly translating into increased consumption of commodity chemicals for their production.

- Cost-Effectiveness and Economies of Scale: Large-scale production facilities in the region enable cost efficiencies and economies of scale, making its products highly competitive in the global market.

Dominant Segments:

- Petrochemicals: This segment is particularly strong in Asia-Pacific, with significant production capacities for ethylene, propylene, benzene, and their derivatives, which are crucial building blocks for numerous downstream products. The demand for petrochemicals is intrinsically linked to the region's booming manufacturing and construction sectors.

- Plastics Resins: The region is a leading producer and consumer of various plastic resins, including polyethylene (PE), polypropylene (PP), and polyvinyl chloride (PVC), essential for packaging, automotive parts, construction materials, and consumer electronics.

- Organics: The production and consumption of a wide array of organic chemicals, serving as intermediates for pharmaceuticals, agrochemicals, and specialty chemicals, are also heavily concentrated in Asia-Pacific.

While segments like Organics and Petrochemicals are paramount, the region also shows significant growth in Inorganics to support industrial development and a rising demand for Synthetic Rubbers and Fibers driven by the automotive and textile industries, respectively. The application segments of Others (encompassing textiles, automotive, electronics, construction, and agriculture) are the primary beneficiaries of this chemical production, far outpacing the demand from Hospitals, Biotechnology Companies, and Scientific Research Institutions and Universities in terms of volume. The sheer scale of industrial output and consumer market penetration solidifies Asia-Pacific's, and particularly China's, enduring leadership in the global commodity chemicals arena, with a projected market share of over 55% by 2033.

Commodity Chemicals Product Innovations

Product innovations in commodity chemicals are increasingly focused on sustainability and enhanced performance. Breakthroughs in catalysis are enabling the production of essential chemicals with significantly reduced energy consumption and waste generation, exemplified by new enzyme-based processes for organic synthesis. In the realm of plastics, advancements are leading to the development of bio-based and biodegradable resins with comparable or superior mechanical properties to their fossil fuel-derived counterparts. For instance, new grades of polyethylene derived from renewable feedstocks now offer enhanced barrier properties for food packaging. Similarly, the development of flame-retardant additives for synthetic rubbers that are free from halogenated compounds addresses critical environmental and health concerns. These innovations are not only meeting stringent regulatory requirements but also catering to a growing demand for eco-friendly and high-performance materials across diverse applications. The unique selling proposition lies in achieving superior functionality while minimizing environmental impact, thereby creating new market opportunities.

Propelling Factors for Commodity Chemicals Growth

The commodity chemicals market is propelled by a confluence of robust economic growth, technological advancements, and supportive regulatory frameworks. Economic expansion, particularly in emerging economies, fuels industrialization and increases demand for basic chemicals across sectors like construction, automotive, and consumer goods. Technological innovations, such as advanced catalysis and process optimization, enhance production efficiency, reduce costs, and enable the development of more sustainable chemical pathways. Government initiatives promoting industrial development and investing in chemical infrastructure further bolster growth. For example, recent policies in several Asian countries aimed at boosting domestic chemical production are expected to add over XXX million in market value by 2028. The ongoing drive for sustainability is also a significant catalyst, pushing for the development and adoption of greener chemical alternatives and recycling technologies.

Obstacles in the Commodity Chemicals Market

Despite strong growth potential, the commodity chemicals market faces several significant obstacles. Stringent environmental regulations and increasing compliance costs present a substantial barrier, requiring significant investment in pollution control and sustainable practices. Supply chain disruptions, exacerbated by geopolitical events and logistical challenges, can lead to price volatility and impact production continuity, as evidenced by price spikes of over 20% in certain petrochemicals during recent global events. Intense global competition and overcapacity in certain segments can depress profit margins, making it difficult for smaller players to compete. Furthermore, the high capital intensity of establishing and operating commodity chemical plants necessitates substantial upfront investment, posing a challenge for new market entrants. The transition to a circular economy, while an opportunity, also requires significant investment in new infrastructure and technologies.

Future Opportunities in Commodity Chemicals

The future of the commodity chemicals market is ripe with emerging opportunities, primarily driven by the global transition towards a sustainable economy and the accelerating demand for specialized materials. The development and widespread adoption of bio-based and recycled feedstocks for chemical production represent a monumental opportunity, aligning with circular economy principles and reducing reliance on fossil fuels. Growth in advanced materials for renewable energy technologies, such as solar panels and battery components, will create new demand streams. Furthermore, the digitalization of chemical manufacturing, including the implementation of AI and IoT for process optimization and predictive maintenance, offers significant opportunities for efficiency gains and cost reductions. Emerging markets in Africa and Southeast Asia, with their burgeoning industrial bases and growing populations, present untapped potential for market expansion. The estimated market size for green commodity chemicals is projected to reach XXX million by 2033.

Major Players in the Commodity Chemicals Ecosystem

- BASF

- Bayer

- The Dow Chemical

- Mitsubishi Chemical Holdings

- PPG Industries

- Linde

- Akzo Nobel

- LyondellBasell Industries

- Asahi Kasei

- Sumitomo Chemicals

- Evonik Industries

- INEOS

- Chem

Key Developments in Commodity Chemicals Industry

- March 2023: BASF announces a strategic investment of XXX million to expand its bio-based chemical production capacity, emphasizing a commitment to sustainability.

- November 2022: The Dow Chemical and LyondellBasell Industries form a joint venture to develop and commercialize advanced chemical recycling technologies, aiming to address plastic waste.

- June 2022: Linde secures a long-term contract to supply hydrogen to a major petrochemical complex, highlighting the growing importance of green hydrogen in industrial processes.

- January 2022: Mitsubishi Chemical Holdings launches a new line of biodegradable plastics derived from renewable resources, targeting the packaging and consumer goods sectors.

- September 2021: PPG Industries acquires a specialty coatings company to enhance its portfolio in high-performance materials, indicating a trend towards value-added products.

- April 2021: In response to increasing regulatory scrutiny, Akzo Nobel announces a comprehensive plan to phase out certain hazardous chemicals from its product lines.

- December 2020: Sumitomo Chemicals reports successful pilot testing of a novel catalytic process that significantly reduces energy consumption in ammonia production by over 20%.

- August 2020: Evonik Industries invests XXX million in a new R&D center focused on developing advanced materials for electric vehicles, anticipating future market demands.

- July 2019: INEOS announces a major expansion of its ethylene cracker in Europe, aiming to meet growing demand for polyolefins.

Strategic Commodity Chemicals Market Forecast

The strategic forecast for the commodity chemicals market projects continued robust growth, driven by a persistent global demand for essential materials and an accelerating shift towards sustainability. The forecast period of 2025–2033 is expected to witness an average annual growth rate of approximately 5.2%, reaching an estimated market valuation of over XXX million by the end of the forecast period. This expansion will be underpinned by increasing investments in green chemistry, bio-based feedstocks, and advanced recycling technologies, all aimed at reducing the industry's environmental footprint. The demand from burgeoning end-user industries such as electric vehicles, renewable energy infrastructure, and advanced healthcare will also be a significant growth catalyst. Strategic focus on innovation, operational efficiency, and market diversification will be crucial for players to capitalize on these opportunities and navigate evolving regulatory landscapes, ensuring long-term profitability and market leadership in this dynamic sector.

Commodity Chemicals Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Biotechnology Companies

- 1.3. Scientific Research Institutions And Universities

- 1.4. Others

-

2. Type

- 2.1. Organics

- 2.2. Inorganics

- 2.3. Plastics Resins

- 2.4. Synthetic Rubbers

- 2.5. Fibers

- 2.6. Films

- 2.7. Explosives

- 2.8. Petrochemicals

Commodity Chemicals Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Commodity Chemicals Regional Market Share

Geographic Coverage of Commodity Chemicals

Commodity Chemicals REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Biotechnology Companies

- 5.1.3. Scientific Research Institutions And Universities

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Organics

- 5.2.2. Inorganics

- 5.2.3. Plastics Resins

- 5.2.4. Synthetic Rubbers

- 5.2.5. Fibers

- 5.2.6. Films

- 5.2.7. Explosives

- 5.2.8. Petrochemicals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Commodity Chemicals Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Biotechnology Companies

- 6.1.3. Scientific Research Institutions And Universities

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Organics

- 6.2.2. Inorganics

- 6.2.3. Plastics Resins

- 6.2.4. Synthetic Rubbers

- 6.2.5. Fibers

- 6.2.6. Films

- 6.2.7. Explosives

- 6.2.8. Petrochemicals

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Commodity Chemicals Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Biotechnology Companies

- 7.1.3. Scientific Research Institutions And Universities

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Organics

- 7.2.2. Inorganics

- 7.2.3. Plastics Resins

- 7.2.4. Synthetic Rubbers

- 7.2.5. Fibers

- 7.2.6. Films

- 7.2.7. Explosives

- 7.2.8. Petrochemicals

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Commodity Chemicals Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Biotechnology Companies

- 8.1.3. Scientific Research Institutions And Universities

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Organics

- 8.2.2. Inorganics

- 8.2.3. Plastics Resins

- 8.2.4. Synthetic Rubbers

- 8.2.5. Fibers

- 8.2.6. Films

- 8.2.7. Explosives

- 8.2.8. Petrochemicals

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Commodity Chemicals Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Biotechnology Companies

- 9.1.3. Scientific Research Institutions And Universities

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Organics

- 9.2.2. Inorganics

- 9.2.3. Plastics Resins

- 9.2.4. Synthetic Rubbers

- 9.2.5. Fibers

- 9.2.6. Films

- 9.2.7. Explosives

- 9.2.8. Petrochemicals

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Commodity Chemicals Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Biotechnology Companies

- 10.1.3. Scientific Research Institutions And Universities

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Organics

- 10.2.2. Inorganics

- 10.2.3. Plastics Resins

- 10.2.4. Synthetic Rubbers

- 10.2.5. Fibers

- 10.2.6. Films

- 10.2.7. Explosives

- 10.2.8. Petrochemicals

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Commodity Chemicals Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Biotechnology Companies

- 11.1.3. Scientific Research Institutions And Universities

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Organics

- 11.2.2. Inorganics

- 11.2.3. Plastics Resins

- 11.2.4. Synthetic Rubbers

- 11.2.5. Fibers

- 11.2.6. Films

- 11.2.7. Explosives

- 11.2.8. Petrochemicals

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BASF

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Bayer

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 The Dow Chemical

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Mitsubishi Chemical Holdings

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 PPG Industries

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Linde

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Akzo Nobel

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 LyondellBasell Industries

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Asahi Kasei

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sumitomo Chemicals

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Evonik Industries

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 INEOS

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Chem

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 BASF

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Commodity Chemicals Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Commodity Chemicals Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Commodity Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Commodity Chemicals Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Commodity Chemicals Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Commodity Chemicals Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Commodity Chemicals Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Commodity Chemicals Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Commodity Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Commodity Chemicals Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Commodity Chemicals Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Commodity Chemicals Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Commodity Chemicals Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Commodity Chemicals Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Commodity Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Commodity Chemicals Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Commodity Chemicals Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Commodity Chemicals Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Commodity Chemicals Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Commodity Chemicals Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Commodity Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Commodity Chemicals Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Commodity Chemicals Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Commodity Chemicals Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Commodity Chemicals Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Commodity Chemicals Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Commodity Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Commodity Chemicals Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Commodity Chemicals Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Commodity Chemicals Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Commodity Chemicals Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Commodity Chemicals Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Commodity Chemicals Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Commodity Chemicals Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Commodity Chemicals Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Commodity Chemicals Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Commodity Chemicals Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Commodity Chemicals Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Commodity Chemicals Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Commodity Chemicals Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Commodity Chemicals Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Commodity Chemicals Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Commodity Chemicals Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Commodity Chemicals Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Commodity Chemicals Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Commodity Chemicals Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Commodity Chemicals Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Commodity Chemicals Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Commodity Chemicals Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Commodity Chemicals Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Commodity Chemicals?

The projected CAGR is approximately 2.3%.

2. Which companies are prominent players in the Commodity Chemicals?

Key companies in the market include BASF, Bayer, The Dow Chemical, Mitsubishi Chemical Holdings, PPG Industries, Linde, Akzo Nobel, LyondellBasell Industries, Asahi Kasei, Sumitomo Chemicals, Evonik Industries, INEOS, Chem.

3. What are the main segments of the Commodity Chemicals?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Commodity Chemicals," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Commodity Chemicals report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Commodity Chemicals?

To stay informed about further developments, trends, and reports in the Commodity Chemicals, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence