Key Insights

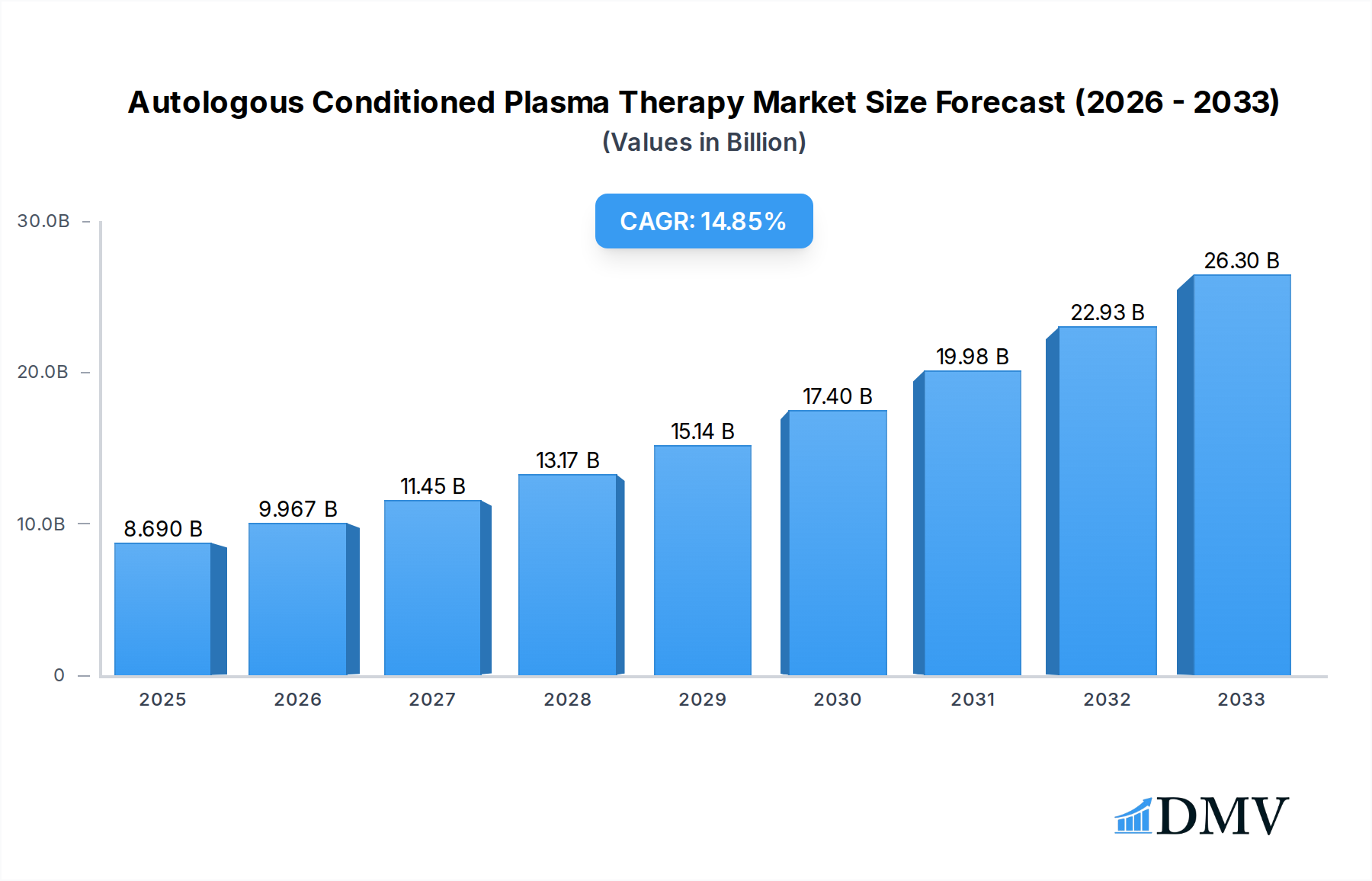

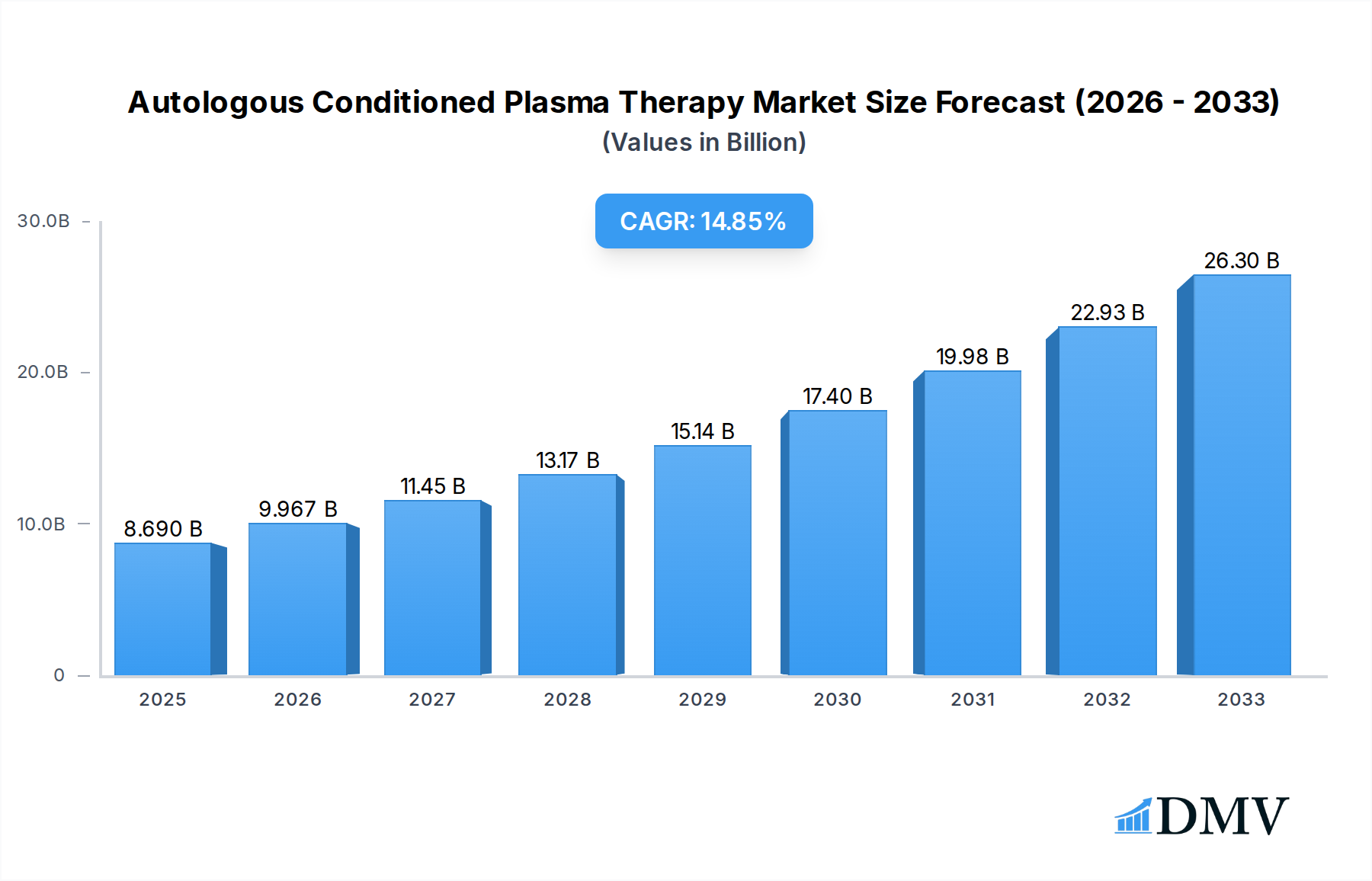

The Autologous Conditioned Plasma (ACP) Therapy market is poised for significant expansion, with a projected market size of $8.69 billion in 2025. This growth is driven by an impressive Compound Annual Growth Rate (CAGR) of 14.72% over the forecast period. The increasing prevalence of orthopedic conditions, sports injuries, and degenerative diseases globally is a primary catalyst for this upward trajectory. Advances in ACP preparation technologies, leading to enhanced therapeutic efficacy and patient outcomes, are further fueling market adoption. Specialized clinics and ambulatory surgical centers are emerging as key growth areas, alongside traditional hospital settings, as ACP therapy demonstrates its versatility across a spectrum of medical applications, including wound healing, osteoarthritis management, and post-operative recovery. The market's robust growth is also supported by rising healthcare expenditure and a growing patient preference for minimally invasive and regenerative treatment options.

Autologous Conditioned Plasma Therapy Market Size (In Billion)

The market segmentation reveals a dynamic landscape, with Pure Platelet-Rich Plasma (P-PRP) and Pure Platelet-Rich Fibrin (P-PRF) holding substantial shares due to their widespread clinical application and proven benefits. While the rising demand for advanced regenerative medicine solutions and the expanding application areas are major drivers, certain factors, such as the initial cost of equipment and the need for specialized training for healthcare professionals, could present moderate restraints. However, the long-term benefits of ACP therapy, including reduced recovery times and improved quality of life for patients, are expected to outweigh these challenges. Leading companies like Zimmer Biomet Inc., Terumo Corporation, and Arthrex, Inc. are actively investing in research and development, further propelling innovation and market penetration across key regions like North America and Europe, with the Asia Pacific region showing promising future growth potential.

Autologous Conditioned Plasma Therapy Company Market Share

Autologous Conditioned Plasma Therapy Market Composition & Trends

The autologous conditioned plasma (ACP) therapy market is characterized by dynamic growth driven by increasing adoption in orthopedic and regenerative medicine. Market concentration is moderate, with key players investing heavily in research and development to refine ACP extraction and application techniques. Innovation catalysts include advancements in PRP and PRF preparation systems, leading to improved efficacy and patient outcomes. The regulatory landscape is evolving, with a growing emphasis on standardized protocols and clinical validation for ACP therapies. Substitute products, such as allogeneic stem cell therapies and synthetic growth factors, present a competitive challenge, though ACP's inherent safety and autologous nature remain significant advantages. End-user profiles are expanding beyond traditional orthopedic surgeons to include sports medicine specialists, dermatologists, and even dentists, driven by the diverse therapeutic applications of ACP. Mergers and acquisitions (M&A) activity is projected to intensify, with estimated deal values reaching upwards of one billion dollars, as larger medical device companies seek to consolidate their positions and acquire innovative ACP technologies. Market share distribution is a key focus for stakeholders, with current estimations placing the leading companies at approximately 30% combined market share, projected to grow to 45% by the end of the forecast period.

Autologous Conditioned Plasma Therapy Industry Evolution

The autologous conditioned plasma (ACP) therapy industry is on an upward trajectory, exhibiting robust growth rates driven by a confluence of factors including increasing awareness of regenerative medicine's potential, a rising incidence of chronic and degenerative diseases, and significant technological advancements in ACP preparation and delivery. The historical period, from 2019 to 2024, witnessed a foundational growth phase, with an estimated market valuation of 2.5 billion dollars in 2019, escalating to 6.8 billion dollars by the end of 2024, representing a compound annual growth rate (CAGR) of approximately 21%. This evolution is intricately linked to a paradigm shift in healthcare towards less invasive and more natural treatment modalities.

Technological advancements have been pivotal in shaping the industry. Early iterations of ACP involved relatively basic centrifuges, but the market has since seen the introduction of sophisticated, automated devices that ensure precise and reproducible preparation of platelet-rich plasma (PRP) and platelet-rich fibrin (PRF) formulations. These advancements have not only enhanced the concentration of growth factors and healing mediators but have also improved the ease of use for healthcare practitioners. The development of different ACP types, such as Pure Platelet-Rich Plasma (P-PRP), Leukocyte- and Platelet-Rich Plasma (LPRP), Pure Platelet-Rich Fibrin (P-PRF), and Leukocyte- and Platelet-Rich Fibrin (L-PRF), caters to a wider spectrum of clinical needs, allowing for tailored therapeutic approaches. For instance, the introduction of L-PRF, with its fibrin matrix structure, offers enhanced scaffolding properties for tissue regeneration, contributing to its increasing adoption in complex wound healing and surgical repair.

Shifting consumer demands have also played a crucial role. Patients are increasingly seeking regenerative treatments that offer faster recovery times, reduced pain, and minimal side effects compared to traditional surgical interventions or pharmaceutical drugs. The appeal of using one's own blood components for healing resonates strongly with this patient demographic. This demand has spurred greater investment in clinical research to validate the efficacy of ACP across various applications, from osteoarthritis and tendinopathies to wound care and post-surgical recovery. The estimated investment in R&D for ACP therapies has more than doubled from 300 million dollars in 2019 to 750 million dollars in 2024.

The base year, 2025, sees the global ACP therapy market valued at an estimated 8.2 billion dollars, with a projected CAGR of 19% during the forecast period of 2025–2033. This sustained growth is underpinned by the expanding clinical evidence base, growing physician acceptance, and an increasing number of specialized clinics dedicated to regenerative medicine. The market is expected to reach a monumental valuation of 34.5 billion dollars by 2033, reflecting the profound impact of ACP therapies on modern healthcare. The adoption metrics for ACP therapies in orthopedic applications have surged from 15% in 2019 to an estimated 40% by 2024, with projections indicating further escalation.

Leading Regions, Countries, or Segments in Autologous Conditioned Plasma Therapy

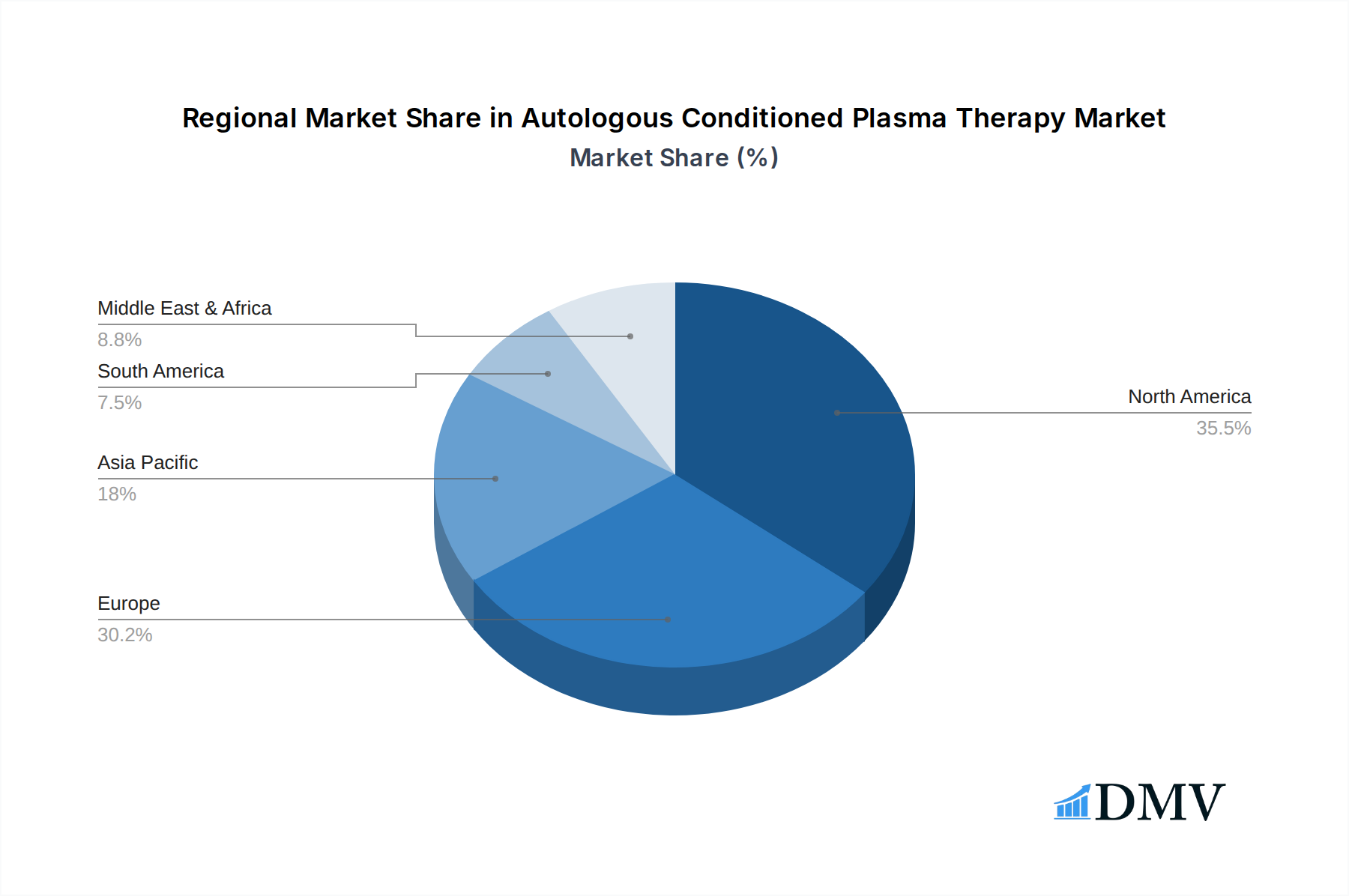

The global autologous conditioned plasma (ACP) therapy market is experiencing significant expansion across various regions and segments, with North America currently leading in terms of market share and adoption. This dominance is attributed to several key drivers, including a well-established healthcare infrastructure, substantial investment in research and development, favorable reimbursement policies for regenerative medicine, and a high prevalence of orthopedic conditions.

Within the application segments, Orthopedic & Trauma Centers represent the most dominant segment, accounting for an estimated 45% of the total market share in 2024. This leadership is fueled by the widespread use of ACP therapies in treating musculoskeletal injuries such as osteoarthritis, tendinopathies, ligament tears, and sports-related trauma. The ability of ACP to stimulate tissue repair, reduce inflammation, and alleviate pain without the risks associated with synthetic materials or invasive surgery makes it a preferred choice for orthopedic surgeons. Investment trends in this segment are robust, with an estimated 1.2 billion dollars invested in research and clinical trials related to orthopedic applications from 2019 to 2024.

The Hospitals segment is another significant contributor, holding approximately 30% of the market share. Hospitals are increasingly integrating ACP therapies into their surgical and post-operative care protocols, particularly in specialized departments like orthopedics, sports medicine, and regenerative surgery. The growing acceptance of ACP as a standard of care in these settings, coupled with the availability of advanced ACP preparation systems, is driving its adoption. Regulatory support in major economies has been instrumental in facilitating this integration, with clear guidelines emerging for the safe and effective use of ACP.

Specialized Clinics focusing on sports medicine, regenerative medicine, and pain management are also witnessing substantial growth, representing around 15% of the market share. These clinics often serve as early adopters of innovative ACP technologies and cater to a patient population actively seeking advanced treatment options. The personalized approach offered by these clinics, combined with their focus on patient outcomes, further bolsters the demand for ACP.

The Ambulatory Surgical Centers segment, while smaller at approximately 5%, is experiencing rapid growth as ACP procedures become more streamlined and suitable for outpatient settings. This trend is driven by the desire for cost-effective and convenient treatment options.

Research Institutes play a crucial role in advancing the understanding and application of ACP, contributing to market growth through ongoing research and development, although their direct market share is smaller.

Considering the types of ACP therapies, Pure Platelet-Rich Plasma (P-PRP) and Leukocyte- and Platelet-Rich Plasma (LPRP) collectively dominate the market, accounting for approximately 70% of the total share. P-PRP is widely used for its potent growth factor content, while LPRP's added leukocytes offer immunomodulatory and anti-infective properties, making it suitable for specific applications like infected wounds or bone regeneration. Pure Platelet-Rich Fibrin (P-PRF) and Leukocyte- and Platelet-Rich Fibrin (L-PRF) are gaining traction, especially in wound healing and bone grafting, due to their sustained release of growth factors and scaffold-forming capabilities, representing around 30% of the market share and exhibiting a higher growth rate.

The market in North America is estimated to be valued at 3.1 billion dollars in 2024, with a projected CAGR of 20% during the forecast period. Europe follows closely, with a market valuation of 2.5 billion dollars in 2024 and a projected CAGR of 18%. Asia Pacific is expected to be the fastest-growing region, driven by increasing healthcare expenditure and a rising awareness of regenerative therapies, with a projected CAGR of 22%.

Autologous Conditioned Plasma Therapy Product Innovations

Product innovation in autologous conditioned plasma (ACP) therapy is rapidly advancing, focusing on enhancing the efficacy, safety, and ease of use of ACP preparations. Key advancements include the development of next-generation centrifuges and collection systems that optimize platelet yield and concentration, leading to higher therapeutic potential. Innovations in PRF and PRP formulations are also emerging, with tailored compositions designed for specific applications such as enhanced bone regeneration or accelerated soft tissue healing. Furthermore, the integration of advanced imaging and diagnostic tools with ACP delivery systems is improving treatment precision and patient outcomes. These technological leaps are not only differentiating products but also expanding the clinical utility of ACP therapies, with unique selling propositions centered on superior growth factor activation and sustained release mechanisms.

Propelling Factors for Autologous Conditioned Plasma Therapy Growth

Several key factors are propelling the growth of the autologous conditioned plasma (ACP) therapy market. Technologically, advancements in ACP preparation devices and techniques have significantly improved the quality and consistency of platelet concentrates, leading to better clinical outcomes. Economically, the rising healthcare expenditure globally, coupled with an increasing demand for minimally invasive and regenerative treatments, is creating a favorable market environment. Regulatory bodies are also increasingly recognizing the therapeutic potential of ACP, with evolving frameworks that support clinical research and product approvals, albeit with a focus on robust data. Furthermore, the growing body of clinical evidence demonstrating the efficacy of ACP in orthopedic, sports medicine, and wound care applications is a significant driver, boosting physician confidence and patient acceptance. The projected market value of 34.5 billion dollars by 2033 underscores this robust growth trajectory.

Obstacles in the Autologous Conditioned Plasma Therapy Market

Despite its promising growth, the autologous conditioned plasma (ACP) therapy market faces several obstacles. Regulatory challenges persist, with variations in approval pathways and standardization requirements across different regions, potentially slowing down market penetration. The lack of universally standardized protocols for ACP preparation and application can lead to inconsistent outcomes, impacting physician confidence and broader adoption. Supply chain disruptions, particularly for specialized consumables and equipment, can also hinder consistent product availability. Competitive pressures from alternative regenerative therapies, such as stem cell therapies and advanced biomaterials, require ACP to continuously demonstrate its superior cost-effectiveness and efficacy. The estimated impact of these regulatory hurdles could delay market penetration by up to 15% in certain regions.

Future Opportunities in Autologous Conditioned Plasma Therapy

Emerging opportunities in the autologous conditioned plasma (ACP) therapy market are abundant. The expansion of ACP into new clinical applications, such as aesthetic medicine, ophthalmic treatments, and even urological conditions, presents significant growth potential. Technological advancements in personalized ACP formulations, tailored to individual patient needs and specific pathologies, are poised to drive further innovation. The growing trend towards at-home regenerative care, supported by advancements in remote monitoring and simplified ACP delivery systems, could also unlock new market segments. Furthermore, the increasing focus on preventative medicine and early intervention for degenerative diseases will likely boost the demand for ACP as a proactive therapeutic option. The projected growth in these new avenues suggests a potential market expansion of 5 billion dollars by 2030.

Major Players in the Autologous Conditioned Plasma Therapy Ecosystem

- Zimmer Biomet Inc.

- Terumo Corporation

- AdiStem Ltd.

- Arthrex, Inc.

- Stryker Corporation

- Cesca Therapeutics, Inc.

- Biotechnology Institute BTI

- Dr. PRP America LLC

- EmCyte Corporation

- Vivostat A/S

- Regen Lab SA

- Royal Biologics

- Exactech, Inc.

- Plateltex S.R.O.

Key Developments in Autologous Conditioned Plasma Therapy Industry

- 2023 Q4: Launch of next-generation PRP preparation systems with enhanced platelet yield and purity, improving treatment efficacy.

- 2024 Q1: Significant increase in clinical trials investigating ACP for osteoarthritis and chronic wound healing, demonstrating positive outcomes.

- 2024 Q2: Major orthopedic device manufacturers announce strategic partnerships to integrate ACP technologies into their surgical platforms.

- 2024 Q3: Regulatory bodies in key European markets release updated guidelines for the clinical use of platelet-rich fibrin (PRF) therapies.

- 2024 Q4: Emergence of advanced ACP delivery devices with integrated imaging capabilities for more precise application in complex musculoskeletal injuries.

- 2025 Q1: First significant acquisition of a specialized ACP technology developer by a global medical device company, signaling industry consolidation.

- 2025 Q2: Introduction of novel L-PRF formulations with enhanced fibrin scaffold properties for improved bone regeneration applications.

- 2025 Q3: Growing adoption of ACP therapies in sports medicine clinics in North America, driven by faster athlete recovery rates.

- 2025 Q4: Increased investment in R&D for combined ACP and exosome therapies, exploring synergistic regenerative effects.

- 2026 Q1: Expansion of ACP therapy applications into the field of aesthetic medicine for skin rejuvenation and hair restoration.

Strategic Autologous Conditioned Plasma Therapy Market Forecast

The strategic forecast for the autologous conditioned plasma (ACP) therapy market is exceptionally promising, projecting a substantial CAGR of 19% from 2025 to 2033, culminating in a market valuation of 34.5 billion dollars. This robust growth is underpinned by the continuous innovation in ACP preparation and delivery technologies, coupled with an expanding body of compelling clinical evidence demonstrating its efficacy across a widening array of medical applications. The increasing patient and physician preference for minimally invasive, regenerative solutions, alongside supportive regulatory environments and rising global healthcare investments, will continue to fuel market expansion. Future opportunities lie in the exploration of novel ACP formulations, synergistic combination therapies, and penetration into underserved clinical areas and emerging economies. The market's trajectory indicates a significant shift towards regenerative medicine, with ACP therapies poised to play a central role in the future of healthcare.

Autologous Conditioned Plasma Therapy Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Specialized Clinics

- 1.3. Ambulatory Surgical Centers

- 1.4. Orthopedic & Trauma Centers

- 1.5. Research Institutes

-

2. Types

- 2.1. Pure Platelet-Rich Plasma (P-PRP)

- 2.2. Leukocyte- and Platelet-Rich Plasma (LPRP)

- 2.3. Pure Platelet-Rich Fibrin (P-PRF)

- 2.4. Leukocyte- and Platelet-Rich Fibrin (L-PRF)

Autologous Conditioned Plasma Therapy Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Autologous Conditioned Plasma Therapy Regional Market Share

Geographic Coverage of Autologous Conditioned Plasma Therapy

Autologous Conditioned Plasma Therapy REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.72% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Specialized Clinics

- 5.1.3. Ambulatory Surgical Centers

- 5.1.4. Orthopedic & Trauma Centers

- 5.1.5. Research Institutes

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Pure Platelet-Rich Plasma (P-PRP)

- 5.2.2. Leukocyte- and Platelet-Rich Plasma (LPRP)

- 5.2.3. Pure Platelet-Rich Fibrin (P-PRF)

- 5.2.4. Leukocyte- and Platelet-Rich Fibrin (L-PRF)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Autologous Conditioned Plasma Therapy Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Specialized Clinics

- 6.1.3. Ambulatory Surgical Centers

- 6.1.4. Orthopedic & Trauma Centers

- 6.1.5. Research Institutes

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Pure Platelet-Rich Plasma (P-PRP)

- 6.2.2. Leukocyte- and Platelet-Rich Plasma (LPRP)

- 6.2.3. Pure Platelet-Rich Fibrin (P-PRF)

- 6.2.4. Leukocyte- and Platelet-Rich Fibrin (L-PRF)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Autologous Conditioned Plasma Therapy Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Specialized Clinics

- 7.1.3. Ambulatory Surgical Centers

- 7.1.4. Orthopedic & Trauma Centers

- 7.1.5. Research Institutes

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Pure Platelet-Rich Plasma (P-PRP)

- 7.2.2. Leukocyte- and Platelet-Rich Plasma (LPRP)

- 7.2.3. Pure Platelet-Rich Fibrin (P-PRF)

- 7.2.4. Leukocyte- and Platelet-Rich Fibrin (L-PRF)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Autologous Conditioned Plasma Therapy Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Specialized Clinics

- 8.1.3. Ambulatory Surgical Centers

- 8.1.4. Orthopedic & Trauma Centers

- 8.1.5. Research Institutes

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Pure Platelet-Rich Plasma (P-PRP)

- 8.2.2. Leukocyte- and Platelet-Rich Plasma (LPRP)

- 8.2.3. Pure Platelet-Rich Fibrin (P-PRF)

- 8.2.4. Leukocyte- and Platelet-Rich Fibrin (L-PRF)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Autologous Conditioned Plasma Therapy Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Specialized Clinics

- 9.1.3. Ambulatory Surgical Centers

- 9.1.4. Orthopedic & Trauma Centers

- 9.1.5. Research Institutes

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Pure Platelet-Rich Plasma (P-PRP)

- 9.2.2. Leukocyte- and Platelet-Rich Plasma (LPRP)

- 9.2.3. Pure Platelet-Rich Fibrin (P-PRF)

- 9.2.4. Leukocyte- and Platelet-Rich Fibrin (L-PRF)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Autologous Conditioned Plasma Therapy Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Specialized Clinics

- 10.1.3. Ambulatory Surgical Centers

- 10.1.4. Orthopedic & Trauma Centers

- 10.1.5. Research Institutes

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Pure Platelet-Rich Plasma (P-PRP)

- 10.2.2. Leukocyte- and Platelet-Rich Plasma (LPRP)

- 10.2.3. Pure Platelet-Rich Fibrin (P-PRF)

- 10.2.4. Leukocyte- and Platelet-Rich Fibrin (L-PRF)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Autologous Conditioned Plasma Therapy Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Specialized Clinics

- 11.1.3. Ambulatory Surgical Centers

- 11.1.4. Orthopedic & Trauma Centers

- 11.1.5. Research Institutes

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Pure Platelet-Rich Plasma (P-PRP)

- 11.2.2. Leukocyte- and Platelet-Rich Plasma (LPRP)

- 11.2.3. Pure Platelet-Rich Fibrin (P-PRF)

- 11.2.4. Leukocyte- and Platelet-Rich Fibrin (L-PRF)

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Zimmer Biomet Inc.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Terumo Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 AdiStem Ltd.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Arthrex

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Inc.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Stryker Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Cesca Therapeutics

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Biotechnology Institute BTI

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Dr. PRP America LLC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 EmCyte Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Vivostat A/S

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Regen Lab SA

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Royal Biologics

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Exactech

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Inc.

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Plateltex S.R.O.

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 Zimmer Biomet Inc.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Autologous Conditioned Plasma Therapy Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Autologous Conditioned Plasma Therapy Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Autologous Conditioned Plasma Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Autologous Conditioned Plasma Therapy Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Autologous Conditioned Plasma Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Autologous Conditioned Plasma Therapy Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Autologous Conditioned Plasma Therapy Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Autologous Conditioned Plasma Therapy Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Autologous Conditioned Plasma Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Autologous Conditioned Plasma Therapy Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Autologous Conditioned Plasma Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Autologous Conditioned Plasma Therapy Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Autologous Conditioned Plasma Therapy Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Autologous Conditioned Plasma Therapy Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Autologous Conditioned Plasma Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Autologous Conditioned Plasma Therapy Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Autologous Conditioned Plasma Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Autologous Conditioned Plasma Therapy Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Autologous Conditioned Plasma Therapy Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Autologous Conditioned Plasma Therapy Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Autologous Conditioned Plasma Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Autologous Conditioned Plasma Therapy Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Autologous Conditioned Plasma Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Autologous Conditioned Plasma Therapy Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Autologous Conditioned Plasma Therapy Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Autologous Conditioned Plasma Therapy Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Autologous Conditioned Plasma Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Autologous Conditioned Plasma Therapy Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Autologous Conditioned Plasma Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Autologous Conditioned Plasma Therapy Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Autologous Conditioned Plasma Therapy Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Autologous Conditioned Plasma Therapy Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Autologous Conditioned Plasma Therapy Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autologous Conditioned Plasma Therapy?

The projected CAGR is approximately 14.72%.

2. Which companies are prominent players in the Autologous Conditioned Plasma Therapy?

Key companies in the market include Zimmer Biomet Inc., Terumo Corporation, AdiStem Ltd., Arthrex, Inc., Stryker Corporation, Cesca Therapeutics, Inc., Biotechnology Institute BTI, Dr. PRP America LLC, EmCyte Corporation, Vivostat A/S, Regen Lab SA, Royal Biologics, Exactech, Inc., Plateltex S.R.O..

3. What are the main segments of the Autologous Conditioned Plasma Therapy?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.69 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Autologous Conditioned Plasma Therapy," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Autologous Conditioned Plasma Therapy report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Autologous Conditioned Plasma Therapy?

To stay informed about further developments, trends, and reports in the Autologous Conditioned Plasma Therapy, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence