Key Insights

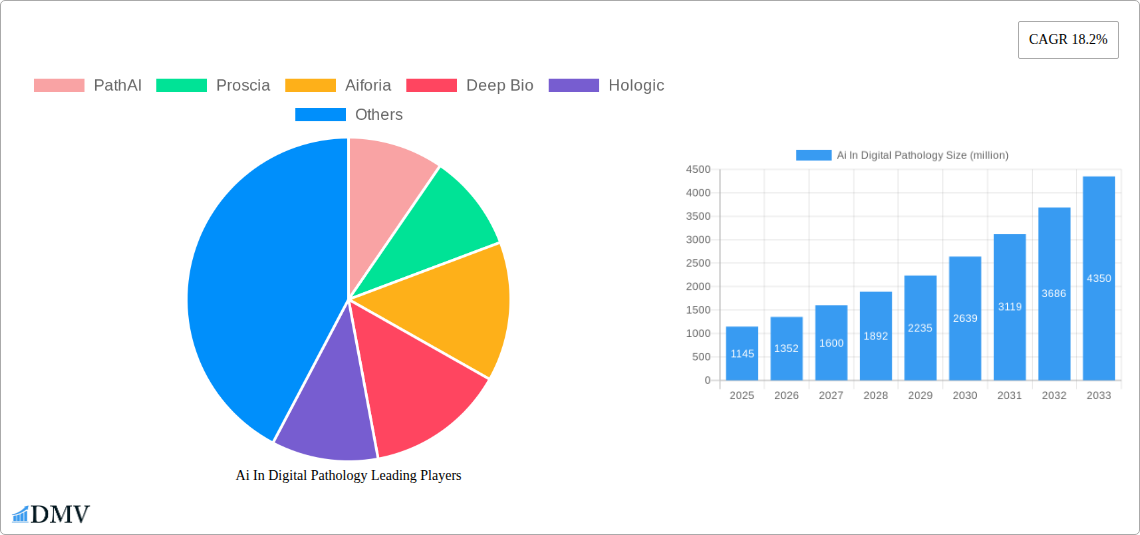

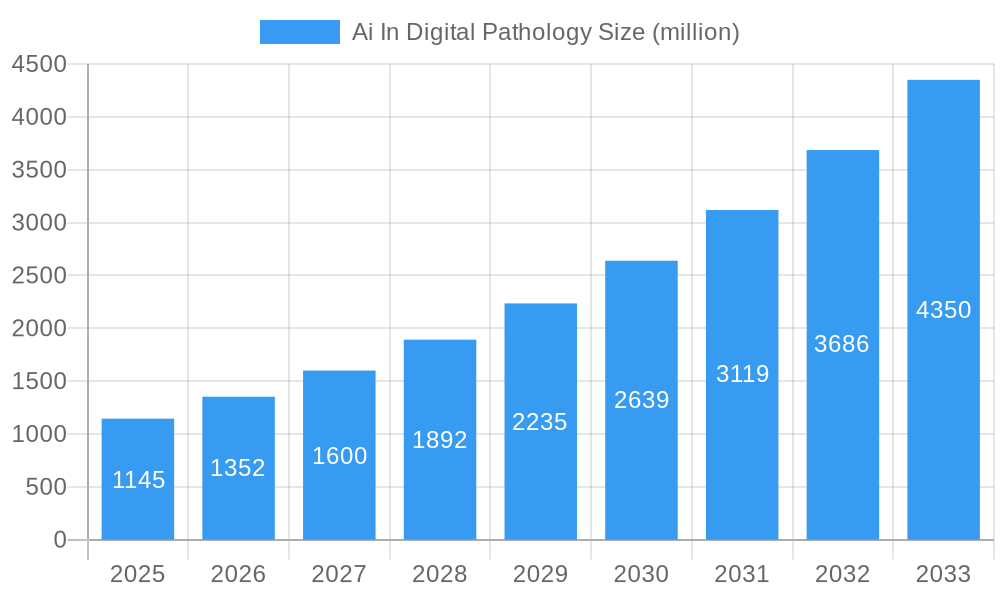

The AI in Digital Pathology market is poised for substantial expansion, with a current market size of approximately $1145 million in 2025, projected to grow at a robust Compound Annual Growth Rate (CAGR) of 18.2% through 2033. This impressive growth trajectory is fueled by several key drivers, including the increasing adoption of digital pathology solutions across healthcare institutions, the growing demand for faster and more accurate disease diagnosis, and the escalating volume of pathology slides requiring analysis. The ability of AI to enhance diagnostic accuracy, streamline workflows, and reduce turnaround times is becoming indispensable for hospitals, diagnostic centers, and research institutes alike. Furthermore, advancements in machine learning algorithms and computing power are enabling more sophisticated applications, such as predictive modeling for patient outcomes and advanced image analysis for subtle pattern recognition that might be missed by the human eye. The market is segmented across various applications, with diagnostic support and image analysis and detection being prominent. The increasing emphasis on precision medicine and personalized treatment plans further underscores the critical role of AI in interpreting complex pathological data for better therapeutic decision-making.

Ai In Digital Pathology Market Size (In Billion)

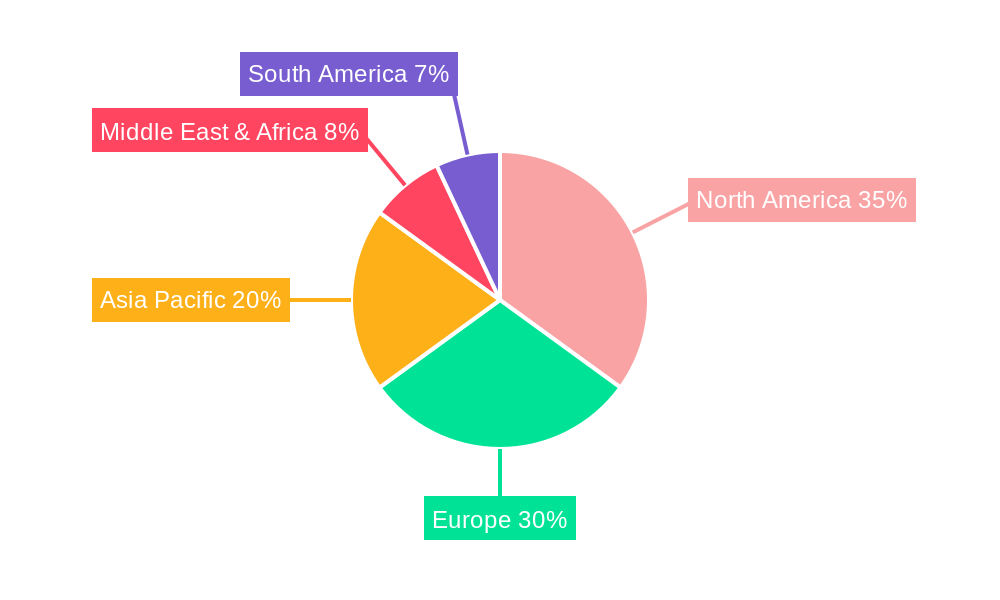

The market's dynamic landscape is characterized by significant technological innovation and strategic collaborations among leading companies like PathAI, Proscia, and Aiforia, who are at the forefront of developing advanced AI-powered solutions. While the market is driven by the inherent benefits of AI in improving healthcare outcomes, certain restraints may influence its pace. These could include the initial investment costs for implementing digital pathology infrastructure, regulatory hurdles in approving AI-based diagnostic tools, and the need for extensive training to integrate these new technologies into existing clinical workflows. However, the overwhelming potential of AI to revolutionize pathology, from early cancer detection to personalized treatment strategies, is expected to mitigate these challenges. Geographically, North America and Europe are expected to lead the market due to their advanced healthcare infrastructure and early adoption of cutting-edge technologies. The Asia Pacific region, driven by a large patient population and increasing healthcare investments, is also anticipated to witness significant growth in the coming years, further solidifying the global reach and impact of AI in digital pathology.

Ai In Digital Pathology Company Market Share

AI in Digital Pathology: A Comprehensive Market Analysis and Future Outlook

This in-depth report provides a comprehensive analysis of the AI in Digital Pathology market, projecting a robust growth trajectory from its base year of 2025 through 2033. Covering the historical period of 2019-2024 and offering insights into the estimated 2025 market landscape, this research delves into critical aspects of market composition, industry evolution, regional dominance, product innovations, growth drivers, obstacles, future opportunities, and the key players shaping this transformative sector. Stakeholders seeking to understand the strategic landscape, investment potential, and technological advancements within AI-powered digital pathology will find this report indispensable.

AI In Digital Pathology Market Composition & Trends

The AI in Digital Pathology market is characterized by a dynamic interplay of innovation and strategic consolidation. Market concentration is gradually increasing as key players solidify their positions through substantial investments in research and development and strategic partnerships. Innovation catalysts are primarily driven by advancements in deep learning algorithms, improved image acquisition hardware, and the growing need for efficient and accurate diagnostic tools in healthcare. The regulatory landscape, while evolving, is a significant factor influencing market entry and product validation, with a focus on patient safety and data integrity. Substitute products, such as traditional histopathology methods, are gradually being augmented or replaced by AI-driven solutions due to their superior speed and accuracy. End-user profiles span a wide spectrum, from large hospital systems and specialized diagnostic centers to academic research institutes, all seeking to leverage AI for enhanced diagnostic capabilities. Mergers and acquisitions (M&A) activities are on the rise, with deal values expected to reach several hundred million dollars as companies seek to expand their technological portfolios and market reach. For instance, recent M&A activities have seen valuations in the range of \$200 million to \$400 million, underscoring the significant investment flowing into this sector. The market share distribution is anticipated to see a significant shift towards AI-integrated solutions, with early adopters capturing substantial portions of the market.

- Market Share Distribution: Projected shift towards AI-integrated solutions, with early adopters capturing up to 30% of the market share by 2030.

- M&A Deal Values: Estimated to reach an aggregate of \$1,500 million over the forecast period, driven by strategic acquisitions for technology and market access.

- Innovation Catalysts: Breakthroughs in deep learning architectures, cloud-based AI platforms, and integration with laboratory information systems (LIS).

- Regulatory Landscape: Increasing focus on FDA approvals and CE marking for AI-based diagnostic software, with estimated approval timelines reducing by 15% for validated solutions.

- End-User Adoption Rates: Expected to grow from 10% in 2024 to over 40% by 2030 across major healthcare institutions.

AI In Digital Pathology Industry Evolution

The AI in Digital Pathology industry has witnessed a remarkable evolutionary trajectory, driven by an insatiable demand for more accurate, efficient, and cost-effective diagnostic methodologies. From its nascent stages, the market has rapidly advanced, propelled by breakthroughs in artificial intelligence, particularly in machine learning and deep learning, which have enabled sophisticated image analysis capabilities. The historical period from 2019 to 2024 laid the groundwork for widespread adoption, marked by initial pilot programs and the development of foundational AI algorithms. As we move into the base year of 2025 and the subsequent forecast period through 2033, the industry is poised for exponential growth. Market growth trajectories are steep, with a projected Compound Annual Growth Rate (CAGR) of approximately 28% between 2025 and 2033. This robust expansion is fueled by increasing investments in healthcare IT infrastructure and a growing recognition of the potential of AI to revolutionize pathology workflows. Technological advancements have been the cornerstone of this evolution, with the development of sophisticated convolutional neural networks (CNNs) capable of identifying subtle pathological features that might be missed by the human eye. Furthermore, advancements in whole-slide imaging (WSI) scanners have provided the high-resolution digital images necessary for effective AI analysis. Shifting consumer demands, primarily from healthcare providers, are gravitating towards solutions that can enhance diagnostic accuracy, reduce turnaround times, and alleviate the burden on pathologists. The adoption of AI in digital pathology is not merely an incremental improvement; it represents a paradigm shift, moving from qualitative assessment to quantitative, data-driven diagnostics. Early adoption metrics indicate a significant upward trend, with an estimated 15% of pathology labs in developed nations utilizing some form of AI-assisted analysis by 2025, projected to rise to over 50% by 2033. The integration of AI into diagnostic support systems, predictive modeling for disease progression, and automated pattern recognition is transforming the practice of pathology, offering tangible benefits in terms of patient outcomes and healthcare economics. The market is also witnessing a growing emphasis on multi-modal AI approaches, combining image data with genomic and clinical information for more holistic patient assessments. The initial investment in AI platforms and digital pathology infrastructure, though substantial, is increasingly being offset by long-term cost savings through improved efficiency and reduced diagnostic errors, estimated to contribute to savings of up to 10% in operational costs for adopting institutions.

Leading Regions, Countries, or Segments in Ai In Digital Pathology

North America currently stands as the dominant region in the AI in Digital Pathology market, driven by a confluence of factors including significant healthcare expenditure, a proactive regulatory environment, and a strong presence of leading technology and research institutions. Within North America, the United States spearheads this growth, fueled by substantial government and private sector investments in AI research and healthcare innovation. The Application segment of Hospitals is experiencing the most pronounced dominance, accounting for an estimated 45% of the market share. Hospitals are increasingly adopting digital pathology solutions to streamline workflows, improve diagnostic accuracy, and manage the growing volume of pathology specimens. This is closely followed by Diagnostic Centers, which are leveraging AI to enhance their service offerings and compete in an evolving healthcare landscape, representing approximately 30% of the market.

The Type segment of Diagnosis Support is the primary driver of AI adoption, comprising an estimated 50% of the market. AI algorithms excel at assisting pathologists in identifying cancerous cells, grading tumors, and detecting subtle anomalies, thereby improving diagnostic confidence and speed. Image Analysis and Detection represents another significant segment, accounting for 30%, as AI's capability to automate the identification and quantification of specific features within digital slides is invaluable. The segment of Predictive Modeling is steadily gaining traction, projected to grow at a CAGR of 35% over the forecast period, as AI models are developed to predict patient response to treatments and disease prognosis.

- Key Drivers in North America:

- Investment Trends: Over \$1,000 million in venture capital funding and R&D investment poured into AI in digital pathology companies in North America over the historical period.

- Regulatory Support: Favorable regulatory pathways, such as FDA clearance for AI-powered medical devices, are accelerating market penetration.

- Technological Infrastructure: Widespread availability of high-speed internet and robust IT infrastructure facilitates the adoption of cloud-based AI solutions.

- Pathologist Shortage: The increasing demand for pathology services coupled with a projected shortage of pathologists is driving the need for AI-driven efficiency.

- Dominance Factors in Hospitals Application:

- Improved Diagnostic Accuracy: AI systems can detect subtle pathological findings with high sensitivity, leading to earlier and more precise diagnoses.

- Workflow Efficiency: Automation of repetitive tasks such as cell counting and feature quantification significantly reduces turnaround times.

- Enhanced Collaboration: Digital pathology platforms enable seamless sharing of cases among pathologists, facilitating multidisciplinary team discussions.

- Reduced Error Rates: AI acts as a second reader, minimizing the risk of human error and improving overall patient safety, with studies indicating up to a 10% reduction in misdiagnosis rates.

- Growth in Diagnosis Support and Predictive Modeling:

- Diagnosis Support: AI algorithms are trained on vast datasets of annotated slides, enabling them to provide consistent and reliable diagnostic recommendations, with an accuracy rate of over 95% for certain cancer detection tasks.

- Predictive Modeling: The integration of AI with clinical and genomic data allows for the prediction of treatment efficacy and patient outcomes, offering personalized medicine approaches. Early predictive models have shown a 20% improvement in identifying patients likely to respond to specific therapies.

AI In Digital Pathology Product Innovations

AI in Digital Pathology is witnessing rapid product innovation, with companies developing sophisticated algorithms for a wide array of applications. Innovations include AI-powered tools for cancer detection and grading, infectious disease identification, and prediction of treatment response. For instance, advanced AI models are now capable of identifying microscopic metastases in lymph nodes with an accuracy exceeding 98%, significantly reducing the manual review time for pathologists. These solutions offer unique selling propositions such as real-time analysis, integration with existing laboratory information systems, and enhanced diagnostic confidence. Technological advancements are focused on improving the explainability of AI models and ensuring their robustness across diverse datasets, addressing critical needs in clinical practice.

Propelling Factors for AI In Digital Pathology Growth

The AI in Digital Pathology market is propelled by a confluence of transformative factors. Firstly, the escalating demand for accurate and efficient disease diagnosis is a primary catalyst, with AI offering a solution to overcome the limitations of manual interpretation and a growing shortage of skilled pathologists. Secondly, significant technological advancements in deep learning and computational power have made sophisticated AI algorithms feasible for complex image analysis tasks. Thirdly, increasing healthcare expenditure globally, coupled with a growing emphasis on personalized medicine, is driving the adoption of advanced diagnostic technologies. Finally, supportive regulatory frameworks in key markets, such as the FDA's evolving stance on AI in medical devices, are paving the way for broader market penetration and commercialization. These drivers are collectively creating an environment ripe for rapid growth and innovation.

- Technological Advancements: Continuous improvements in AI algorithms (e.g., transformer models) and computational hardware.

- Increasing Healthcare Expenditure: Global healthcare spending expected to exceed \$10 trillion by 2028, with a significant portion allocated to advanced diagnostics.

- Need for Efficiency and Accuracy: AI promises to reduce diagnostic turnaround times by up to 50% and improve accuracy rates in identifying subtle pathologies.

- Supportive Regulatory Frameworks: Streamlined approval processes for AI-based medical devices in major economies.

Obstacles in the AI In Digital Pathology Market

Despite its immense potential, the AI in Digital Pathology market faces several significant obstacles. Regulatory hurdles remain a challenge, with the complex and evolving approval processes for AI-powered medical devices in different regions causing delays in market entry. The high initial cost of implementing digital pathology infrastructure and AI software can be prohibitive for smaller institutions, leading to adoption barriers. Data privacy and security concerns are paramount, requiring robust protocols to protect sensitive patient information. Furthermore, the need for extensive validation and integration of AI models with existing clinical workflows can be technically challenging. Finally, the widespread adoption of AI also necessitates comprehensive training and upskilling of pathologists and laboratory staff to ensure effective utilization and trust in AI-driven diagnostics, which represents an estimated \$500 million annual training expenditure requirement across the industry.

- Regulatory Hurdles: Extended validation periods and evolving approval standards for AI medical devices.

- High Initial Investment Costs: Significant upfront capital required for digital scanners, servers, and AI software licenses.

- Data Privacy and Security Concerns: Stringent compliance requirements for handling sensitive patient data, with potential data breaches leading to multi-million dollar fines.

- Integration Challenges: Difficulty in seamlessly integrating AI solutions with existing Laboratory Information Systems (LIS) and Hospital Information Systems (HIS).

- Need for Workforce Training: Requirement for substantial investment in training programs to equip professionals with AI interpretation skills, estimated at \$50 million annually for large healthcare networks.

Future Opportunities in AI In Digital Pathology

The future of AI in Digital Pathology is brimming with opportunities. The expansion into emerging markets in Asia-Pacific and Latin America presents a significant growth avenue as these regions invest in modernizing their healthcare infrastructure. Further development of AI for multi-modal diagnostics, integrating imaging data with genomics, proteomics, and clinical information, will unlock deeper insights into disease mechanisms and treatment responses. The application of AI in drug discovery and development, by analyzing vast pathological datasets to identify biomarkers and predict drug efficacy, represents another lucrative area. Furthermore, the growing demand for remote pathology services and tele-pathology solutions will be augmented by AI, enabling expert consultations and diagnostics across geographical barriers. The development of federated learning approaches will allow for collaborative model training without centralizing sensitive data, addressing privacy concerns.

- Emerging Market Expansion: Untapped potential in regions with growing healthcare investments and increasing adoption of digital technologies.

- Multi-modal Diagnostics: Integration of AI with other omics data for comprehensive patient profiling and personalized treatment strategies.

- AI in Drug Discovery: Leveraging AI for biomarker identification and prediction of drug efficacy, accelerating pharmaceutical R&D.

- Tele-pathology and Remote Diagnostics: Enhancing remote consultations and access to expert pathology services globally.

Major Players in the Ai In Digital Pathology Ecosystem

- PathAI

- Proscia

- Aiforia

- Deep Bio

- Hologic

- Dipath

- iDeepwise

- LBP

- F.Q pathtech

- CellaVision

- AIRA Matrix

- Syntropy

- Indica Labs

- DoMore Diagnostics

- Mindpeak

- Evidium

Key Developments in Ai In Digital Pathology Industry

- 2023/05: Proscia announces a significant partnership to integrate its AI-powered pathology platform with a leading hospital network, enhancing cancer diagnosis.

- 2023/08: Aiforia receives regulatory approval for its AI solution in Europe, expanding its market reach for automated image analysis.

- 2023/11: PathAI secures a substantial Series C funding round of \$250 million to accelerate its AI development and global expansion.

- 2024/01: Deep Bio launches a new AI algorithm for early detection of Alzheimer's disease from brain tissue samples.

- 2024/03: Hologic acquires a digital pathology company to bolster its AI capabilities in women's health diagnostics.

- 2024/06: Indica Labs receives FDA clearance for its AI-powered quantitative analysis software for breast cancer biomarker assessment.

- 2024/09: CellaVision introduces an updated AI-assisted cell counting solution with enhanced accuracy and speed.

- 2025/02: Mindpeak announces a collaboration with a major pharmaceutical company for AI-driven drug discovery in oncology.

- 2025/05: DoMore Diagnostics secures \$50 million in Series B funding to scale its AI platform for diagnostic support.

- 2025/08: Evidium receives CE marking for its AI-based system for prostate cancer grading.

Strategic Ai In Digital Pathology Market Forecast

The strategic forecast for the AI in Digital Pathology market is overwhelmingly positive, driven by robust growth catalysts and emerging opportunities. The increasing adoption of AI for diagnosis support, predictive modeling, and pattern recognition will continue to be the primary growth engines. Key developments such as advancements in AI algorithms, expanding regulatory approvals, and strategic partnerships will further accelerate market penetration. The substantial investment flowing into this sector, coupled with the demonstrable benefits in terms of improved diagnostic accuracy and workflow efficiency, positions AI in Digital Pathology as a cornerstone of future healthcare. The market is projected to witness sustained high growth, with significant potential for innovation and value creation, ultimately transforming patient care and outcomes worldwide.

Ai In Digital Pathology Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Diagnostic Centers

- 1.3. Laboratories & Research Institutes

-

2. Type

- 2.1. Diagnosis Support

- 2.2. Predictive Modeling

- 2.3. Pattern Recognition

- 2.4. Image Analysis and Detection

- 2.5. Other

Ai In Digital Pathology Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ai In Digital Pathology Regional Market Share

Geographic Coverage of Ai In Digital Pathology

Ai In Digital Pathology REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Diagnostic Centers

- 5.1.3. Laboratories & Research Institutes

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Diagnosis Support

- 5.2.2. Predictive Modeling

- 5.2.3. Pattern Recognition

- 5.2.4. Image Analysis and Detection

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Ai In Digital Pathology Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Diagnostic Centers

- 6.1.3. Laboratories & Research Institutes

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Diagnosis Support

- 6.2.2. Predictive Modeling

- 6.2.3. Pattern Recognition

- 6.2.4. Image Analysis and Detection

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Ai In Digital Pathology Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Diagnostic Centers

- 7.1.3. Laboratories & Research Institutes

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Diagnosis Support

- 7.2.2. Predictive Modeling

- 7.2.3. Pattern Recognition

- 7.2.4. Image Analysis and Detection

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Ai In Digital Pathology Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Diagnostic Centers

- 8.1.3. Laboratories & Research Institutes

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Diagnosis Support

- 8.2.2. Predictive Modeling

- 8.2.3. Pattern Recognition

- 8.2.4. Image Analysis and Detection

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Ai In Digital Pathology Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Diagnostic Centers

- 9.1.3. Laboratories & Research Institutes

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Diagnosis Support

- 9.2.2. Predictive Modeling

- 9.2.3. Pattern Recognition

- 9.2.4. Image Analysis and Detection

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Ai In Digital Pathology Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Diagnostic Centers

- 10.1.3. Laboratories & Research Institutes

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Diagnosis Support

- 10.2.2. Predictive Modeling

- 10.2.3. Pattern Recognition

- 10.2.4. Image Analysis and Detection

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Ai In Digital Pathology Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospital

- 11.1.2. Diagnostic Centers

- 11.1.3. Laboratories & Research Institutes

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Diagnosis Support

- 11.2.2. Predictive Modeling

- 11.2.3. Pattern Recognition

- 11.2.4. Image Analysis and Detection

- 11.2.5. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 PathAI

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Proscia

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Aiforia

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Deep Bio

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Hologic

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Dipath

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 iDeepwise

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 LBP

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 F.Q pathtech

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 CellaVision

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 AIRA Matrix

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Syntropy

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Indica Labs

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 DoMore Diagnostics

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Mindpeak

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Evidium

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 PathAI

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ai In Digital Pathology Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Ai In Digital Pathology Revenue (million), by Application 2025 & 2033

- Figure 3: North America Ai In Digital Pathology Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Ai In Digital Pathology Revenue (million), by Type 2025 & 2033

- Figure 5: North America Ai In Digital Pathology Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Ai In Digital Pathology Revenue (million), by Country 2025 & 2033

- Figure 7: North America Ai In Digital Pathology Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ai In Digital Pathology Revenue (million), by Application 2025 & 2033

- Figure 9: South America Ai In Digital Pathology Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Ai In Digital Pathology Revenue (million), by Type 2025 & 2033

- Figure 11: South America Ai In Digital Pathology Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Ai In Digital Pathology Revenue (million), by Country 2025 & 2033

- Figure 13: South America Ai In Digital Pathology Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ai In Digital Pathology Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Ai In Digital Pathology Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ai In Digital Pathology Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Ai In Digital Pathology Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Ai In Digital Pathology Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Ai In Digital Pathology Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ai In Digital Pathology Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Ai In Digital Pathology Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Ai In Digital Pathology Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Ai In Digital Pathology Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Ai In Digital Pathology Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ai In Digital Pathology Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ai In Digital Pathology Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Ai In Digital Pathology Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Ai In Digital Pathology Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Ai In Digital Pathology Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Ai In Digital Pathology Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Ai In Digital Pathology Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ai In Digital Pathology Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Ai In Digital Pathology Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Ai In Digital Pathology Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Ai In Digital Pathology Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Ai In Digital Pathology Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Ai In Digital Pathology Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Ai In Digital Pathology Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Ai In Digital Pathology Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Ai In Digital Pathology Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Ai In Digital Pathology Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Ai In Digital Pathology Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Ai In Digital Pathology Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Ai In Digital Pathology Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Ai In Digital Pathology Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Ai In Digital Pathology Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Ai In Digital Pathology Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Ai In Digital Pathology Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Ai In Digital Pathology Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ai In Digital Pathology Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ai In Digital Pathology?

The projected CAGR is approximately 18.2%.

2. Which companies are prominent players in the Ai In Digital Pathology?

Key companies in the market include PathAI, Proscia, Aiforia, Deep Bio, Hologic, Dipath, iDeepwise, LBP, F.Q pathtech, CellaVision, AIRA Matrix, Syntropy, Indica Labs, DoMore Diagnostics, Mindpeak, Evidium.

3. What are the main segments of the Ai In Digital Pathology?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1145 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ai In Digital Pathology," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ai In Digital Pathology report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ai In Digital Pathology?

To stay informed about further developments, trends, and reports in the Ai In Digital Pathology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence