Key Insights

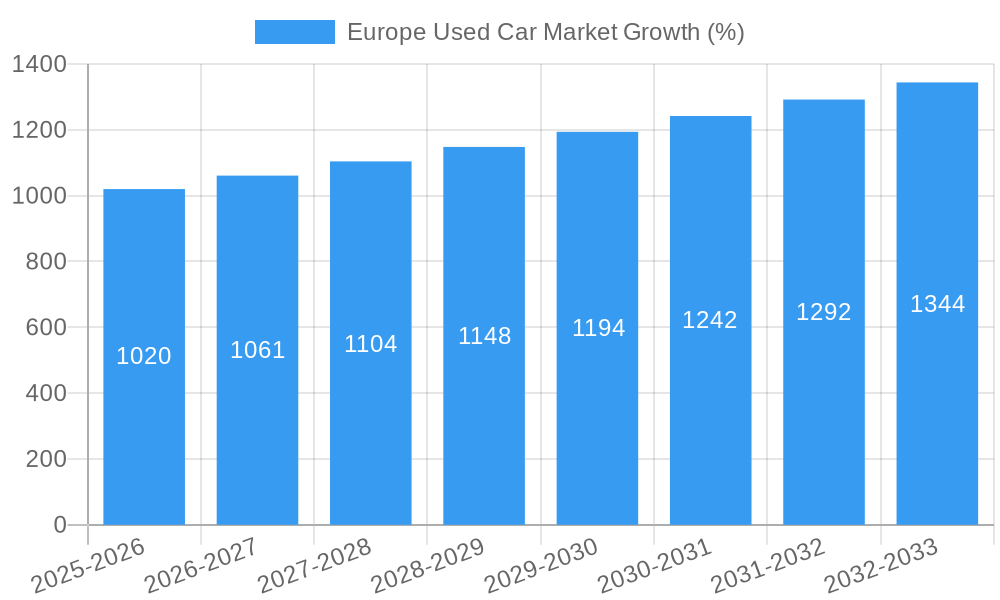

The European used car market, valued at approximately €XX million in 2025, is projected to experience robust growth, driven by several key factors. The increasing preference for more affordable transportation options amidst rising new car prices and economic uncertainty is a major contributor. Furthermore, the expanding online used car marketplaces and improved vehicle condition assessment technologies are enhancing consumer confidence and transparency, fueling market expansion. Segment-wise, the SUV segment is expected to dominate due to its growing popularity across various demographics, while the electric used car segment will show significant albeit slower growth, driven by increasing EV adoption rates and falling prices of pre-owned electric vehicles. Organized vendors are likely to capture a larger market share compared to unorganized players due to their better inventory management, customer service, and financing options. Geographical variations are expected, with Germany, the UK, and France remaining the largest markets due to their larger populations and robust automotive industries. However, growth in countries like Spain and Italy is expected to be more significant, fueled by increased economic activity and evolving consumer preferences. Restrictive regulations on emissions and potential economic downturns remain potential constraints on market growth. The forecast period (2025-2033) anticipates a consistent, if moderate, growth trajectory, largely influenced by the interplay of these driving and restraining forces. The CAGR of 4.12% suggests a steady expansion, albeit potentially subject to year-on-year fluctuations based on macroeconomic conditions and technological advancements within the automotive sector.

Looking ahead, the used car market in Europe will likely see continued consolidation among organized vendors, with larger players acquiring smaller dealerships to enhance their market reach and service offerings. Technological advancements, including AI-powered valuation tools and virtual inspections, will further refine the customer experience and streamline transactions. The increasing adoption of subscription models for used cars also presents a promising avenue for future growth. However, the market's sustainability depends on addressing concerns around vehicle reliability, addressing concerns about the environmental impact of used car emissions, and adapting to evolving consumer demands for features and technologies. Successful players will need to leverage data analytics to understand consumer preferences, optimize pricing strategies, and enhance inventory management across various segments and geographic locations. The integration of innovative financing options and extended warranties will also play a crucial role in boosting consumer confidence and driving sales.

Europe Used Car Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the Europe used car market, encompassing market size, trends, leading players, and future growth prospects. With a focus on the period 2019-2033, including a base year of 2025 and a forecast period of 2025-2033, this report is an essential resource for stakeholders seeking to understand and capitalize on opportunities within this dynamic sector. The report covers key segments including Vehicle Type (Hatchback, Sedan, SUV, MPV), Vendor Type (Organized, Unorganized), and Fuel Type (Gasoline, Diesel, Electric, Other). Geographic coverage includes Germany, the United Kingdom, France, Italy, Spain, Russia, and the Rest of Europe. The total market value is estimated at xx Million in 2025, with a projected growth to xx Million by 2033.

Europe Used Car Market Composition & Trends

This section delves into the competitive landscape of the European used car market, examining market concentration, innovation drivers, regulatory frameworks, substitute products, end-user profiles, and mergers and acquisitions (M&A) activity. The market is characterized by a mix of large multinational corporations and smaller, independent dealers. Market share is currently dominated by a few key players, but the market is relatively fragmented with a high number of smaller independent businesses.

- Market Concentration: The top 5 players account for approximately xx% of the market share in 2025, with the remaining xx% distributed amongst numerous smaller players.

- Innovation Catalysts: Technological advancements such as online marketplaces and data-driven pricing models are driving innovation, improving transparency and efficiency.

- Regulatory Landscape: Emissions regulations and safety standards influence the market dynamics, favoring the adoption of newer, more fuel-efficient vehicles.

- Substitute Products: Public transportation and ride-sharing services pose some competitive pressures, particularly in urban areas.

- End-User Profiles: The market caters to a diverse customer base, ranging from private individuals to businesses.

- M&A Activities: The used car market has seen significant M&A activity in recent years, with deals valued at an estimated xx Million in 2024. This consolidation trend is expected to continue.

Europe Used Car Market Industry Evolution

The European used car market has witnessed significant evolution driven by technological advancements, shifting consumer preferences, and evolving regulatory frameworks. The market has experienced growth despite economic fluctuations, and the ongoing shift towards digital platforms has transformed how consumers access and purchase used vehicles. The historical period (2019-2024) showed an average annual growth rate (AAGR) of xx%, while the forecast period (2025-2033) projects a AAGR of xx%. This growth is fueled by factors such as rising disposable incomes, increasing urbanization, and the expansion of online marketplaces. Further, the growing adoption of electric vehicles is expected to reshape the market in the coming years. Technological developments, including online car valuation tools and transparent online auctions, increase buyer confidence and streamlined transaction processes.

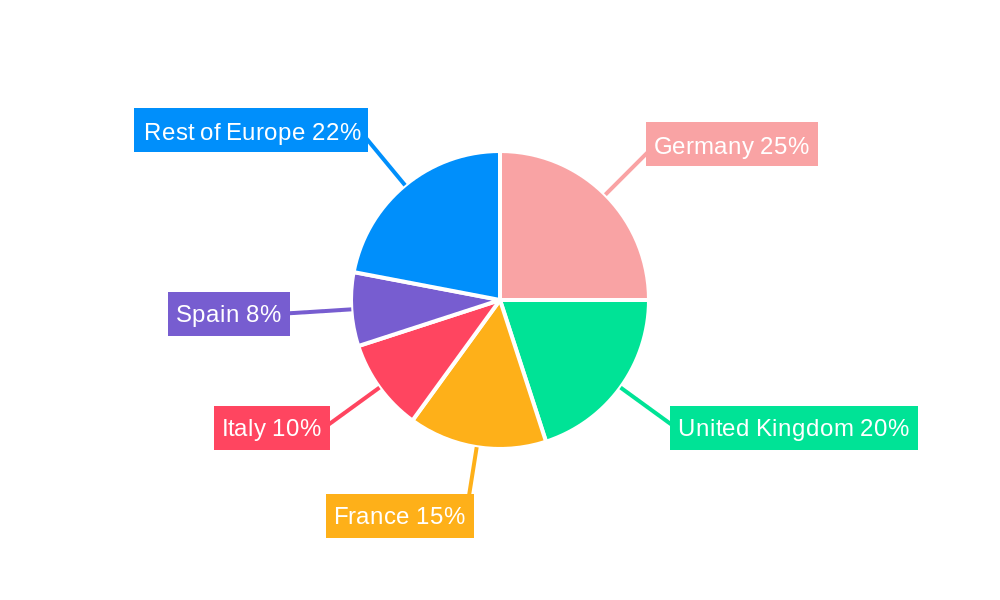

Leading Regions, Countries, or Segments in Europe Used Car Market

Germany, the United Kingdom, and France represent the largest national markets within Europe, largely due to their larger populations and developed automotive industries. The organized vendor segment holds a larger market share compared to the unorganized sector due to factors such as customer trust and more efficient inventory management systems. The SUV segment demonstrates significant growth, propelled by consumer preferences for spaciousness and versatility.

- Key Drivers for Germany: Strong domestic automotive manufacturing, robust consumer demand, and a well-established used car infrastructure.

- Key Drivers for the UK: Large population, high vehicle ownership rates, and a developed online car retail market.

- Key Drivers for Organized Vendors: Higher customer trust, better inventory management, and better after-sales service.

- Key Drivers for SUVs: Growing popularity among families, rising disposable income, and improvements in fuel efficiency.

Europe Used Car Market Product Innovations

Recent innovations in the used car market include the introduction of online marketplaces that facilitate transparent and efficient transactions. These platforms often incorporate data-driven pricing algorithms, detailed vehicle history reports, and virtual inspections. This enhances the buyer's experience by increasing vehicle transparency, which leads to increased buyer confidence and reduces the risk involved in purchasing used vehicles. Furthermore, developments in car financing options and extended warranties are increasing the accessibility and affordability of used cars for a broader range of consumers.

Propelling Factors for Europe Used Car Market Growth

Several factors contribute to the growth of the European used car market. Firstly, economic factors such as fluctuating new car prices and consumer preference for more affordable transportation options stimulate demand for used vehicles. Secondly, technological advancements, particularly the rise of online marketplaces, have improved market efficiency and transparency. Finally, supportive regulatory policies which aim to ensure fair trade practices and environmental standards, play a vital role in shaping market growth.

Obstacles in the Europe Used Car Market

Challenges facing the European used car market include supply chain disruptions, which have increased vehicle prices and limited availability. Regulatory compliance, particularly concerning emissions standards and data protection, poses another hurdle for businesses. Lastly, intense competition, both from established players and new entrants, keeps profit margins under pressure. These factors are projected to impact the market's growth rate by approximately xx% over the next 5 years.

Future Opportunities in Europe Used Car Market

Future opportunities include the expansion of online marketplaces into underserved markets, the development of new financing and insurance products, and the growth of the used electric vehicle market. Further, data analytics and AI-powered services can offer more personalized customer experiences and improve market efficiency. The increasing adoption of subscription-based models will also influence market growth in the coming years.

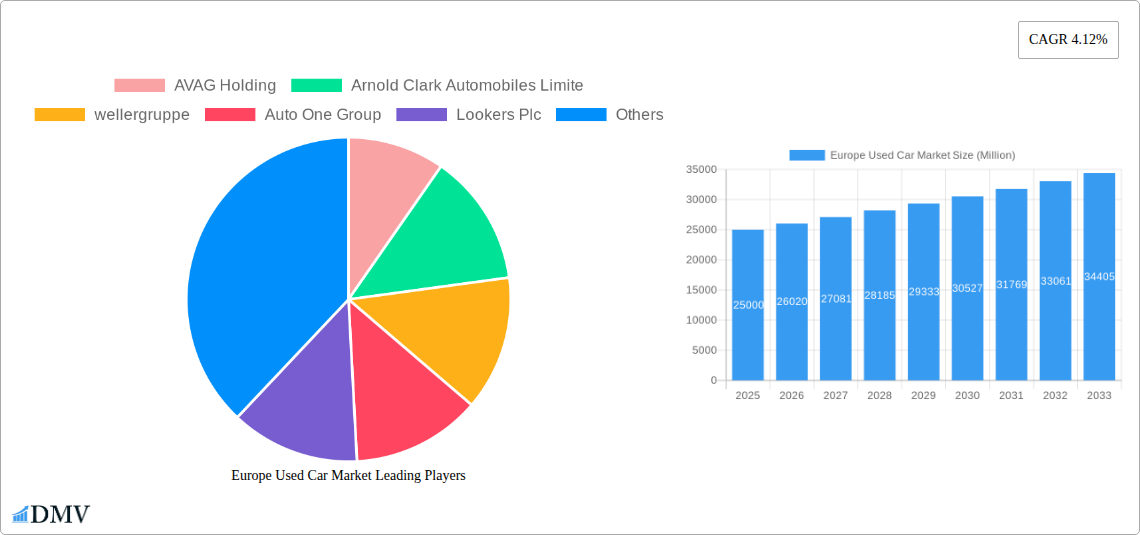

Major Players in the Europe Used Car Market Ecosystem

- AVAG Holding

- Arnold Clark Automobiles Limited

- wellergruppe

- Auto One Group

- Lookers Plc

- Auto Empire Trading GmbH

- Fahrzeug -werke LUEG AG

- Pendragon Plc

- Autorola Group Holding

- Emil Frey AG

- Penske Automotive Group

- Gottfried-schultz

Key Developments in Europe Used Car Market Industry

- March 2022: Toyota Motors Europe (TME) partnered with INDICATA Europe to provide used car pricing data across 13 European countries. This improved data transparency and pricing accuracy across the used car market.

- March 2022: Inchcape's withdrawal from the Russian market due to the Ukraine conflict highlights geopolitical risks affecting the automotive sector. This resulted in a reduction in overall market supply within Russia.

- March 2022: TrueCar Inc.'s launch of TrueCar+ indicates the increasing importance of online platforms in the used car market, enhancing convenience and choice for customers.

Strategic Europe Used Car Market Forecast

The European used car market is poised for continued growth, driven by a confluence of factors. Rising demand, fueled by increasing affordability and technological advancements, will shape the market over the forecast period. Further development of online platforms and innovative financing models will enhance the consumer experience and create new opportunities for market players. Sustained growth is anticipated, with market size expected to reach xx Million by 2033, reflecting a significant expansion from the 2025 baseline.

Europe Used Car Market Segmentation

-

1. Vehicle Type

- 1.1. Hatchback

- 1.2. Sedan

- 1.3. Sports Utility Vehicle

- 1.4. Multi-purpose Vehicle

-

2. Vendor Type

- 2.1. Organized

- 2.2. Unorganized

-

3. Fuel Type

- 3.1. Gasoline

- 3.2. Diesel

- 3.3. Electric

- 3.4. Other Fuel Types (LPG, CNG, etc.)

Europe Used Car Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Used Car Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.12% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Sales of Forklift; Others

- 3.3. Market Restrains

- 3.3.1. Supply Chain Disruption; Others

- 3.4. Market Trends

- 3.4.1. Online Infrastructure witnessing major growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Used Car Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Hatchback

- 5.1.2. Sedan

- 5.1.3. Sports Utility Vehicle

- 5.1.4. Multi-purpose Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Vendor Type

- 5.2.1. Organized

- 5.2.2. Unorganized

- 5.3. Market Analysis, Insights and Forecast - by Fuel Type

- 5.3.1. Gasoline

- 5.3.2. Diesel

- 5.3.3. Electric

- 5.3.4. Other Fuel Types (LPG, CNG, etc.)

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Germany Europe Used Car Market Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Used Car Market Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Used Car Market Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Used Car Market Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Used Car Market Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Used Car Market Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Used Car Market Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 AVAG Holding

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Arnold Clark Automobiles Limite

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 wellergruppe

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Auto One Group

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Lookers Plc

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Auto Empire Trading GmbH

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Fahrzeug -werke LUEG AG

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Pendragon Plc

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Autorola Group Holding

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Emil Frey AG

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Penske Automotive Group

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Gottfried-schultz

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.1 AVAG Holding

List of Figures

- Figure 1: Europe Used Car Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Used Car Market Share (%) by Company 2024

List of Tables

- Table 1: Europe Used Car Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Used Car Market Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 3: Europe Used Car Market Revenue Million Forecast, by Vendor Type 2019 & 2032

- Table 4: Europe Used Car Market Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 5: Europe Used Car Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe Used Car Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Europe Used Car Market Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 15: Europe Used Car Market Revenue Million Forecast, by Vendor Type 2019 & 2032

- Table 16: Europe Used Car Market Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 17: Europe Used Car Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: United Kingdom Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Germany Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: France Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Italy Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Spain Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Netherlands Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Belgium Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Sweden Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Norway Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Poland Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Denmark Europe Used Car Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Used Car Market?

The projected CAGR is approximately 4.12%.

2. Which companies are prominent players in the Europe Used Car Market?

Key companies in the market include AVAG Holding, Arnold Clark Automobiles Limite, wellergruppe, Auto One Group, Lookers Plc, Auto Empire Trading GmbH, Fahrzeug -werke LUEG AG, Pendragon Plc, Autorola Group Holding, Emil Frey AG, Penske Automotive Group, Gottfried-schultz.

3. What are the main segments of the Europe Used Car Market?

The market segments include Vehicle Type, Vendor Type, Fuel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Sales of Forklift; Others.

6. What are the notable trends driving market growth?

Online Infrastructure witnessing major growth.

7. Are there any restraints impacting market growth?

Supply Chain Disruption; Others.

8. Can you provide examples of recent developments in the market?

March 2022: Toyota Motors Europe (TME) announced a major new contract with INDICATA Europe to roll out its used car pricing data to 13 countries over the next two months. INDICATA developed a bespoke reporting suite for TME that tracks all the online used Toyota and Lexus adverts from its dealer networks across Europe and presented it into an easy-to-read dashboard for each country.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Used Car Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Used Car Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Used Car Market?

To stay informed about further developments, trends, and reports in the Europe Used Car Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence