Key Insights

The global automotive traction control system (TCS) market is experiencing robust growth, driven by increasing demand for enhanced vehicle safety and stability features. The market's expansion is fueled by stringent government regulations mandating advanced driver-assistance systems (ADAS) in new vehicles globally. This trend is particularly pronounced in developed regions like North America and Europe, where consumer awareness of safety technologies is high and purchasing power is strong. Technological advancements, such as the integration of TCS with other ADAS features like electronic stability control (ESC) and anti-lock braking systems (ABS), are further boosting market growth. Furthermore, the rising adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs) is creating new opportunities for TCS manufacturers, as these vehicles require sophisticated traction control systems to manage their unique power delivery characteristics. The competitive landscape is characterized by a mix of established automotive component suppliers and emerging technology companies, leading to continuous innovation and a focus on cost-effective solutions.

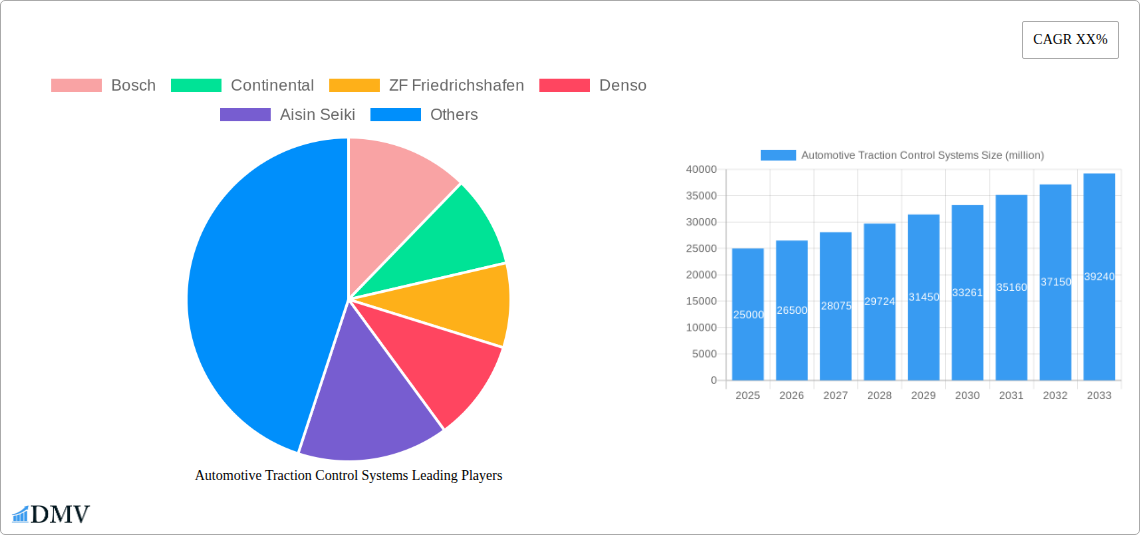

However, the market faces challenges. High initial investment costs associated with developing and implementing advanced TCS technologies can be a barrier to entry for smaller players. The fluctuating prices of raw materials, particularly precious metals used in sensor technologies, can impact profitability. Additionally, regional variations in infrastructure and consumer preferences can influence the market’s growth trajectory. Despite these restraints, the long-term outlook for the automotive TCS market remains positive, driven by ongoing technological innovation and the increasing integration of TCS into the broader ecosystem of advanced vehicle safety features. The market is expected to witness a sustained period of growth, fueled by ongoing advancements and the increasing demand for safer and more efficient vehicles. Leading players, such as Bosch, Continental, and ZF Friedrichshafen, are investing heavily in R&D to maintain their market leadership and capitalize on emerging trends.

Automotive Traction Control Systems Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the global Automotive Traction Control Systems market, projecting a market value exceeding $XX billion by 2033. The study covers the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033, offering invaluable insights for stakeholders across the automotive industry. The report meticulously examines market trends, technological advancements, leading players, and future opportunities, empowering informed decision-making and strategic planning.

Automotive Traction Control Systems Market Composition & Trends

This section delves into the competitive landscape of the automotive traction control systems market, analyzing market concentration, innovation drivers, regulatory influences, substitute technologies, and end-user trends. We examine the impact of mergers and acquisitions (M&A) activity, quantifying deal values in the millions of dollars. The report reveals market share distribution among key players, including Bosch, Continental, ZF Friedrichshafen, and others, identifying the dominant players and emerging competitors. For example, we analyze how the increasing demand for enhanced safety features in electric vehicles (EVs) and autonomous driving systems is driving innovation and influencing market dynamics. Regulatory changes concerning emissions and safety standards are also scrutinized, alongside the emergence of substitute technologies and the evolving end-user preferences. The analysis incorporates a detailed overview of M&A activity within the sector, including a quantitative analysis of deal values (in millions of dollars) and their impact on market consolidation and technological advancements. Specific examples of successful and failed mergers and acquisitions will illustrate the complexities of this dynamic market. The evolving landscape of the automotive industry, with its significant focus on electric and autonomous vehicles, presents both opportunities and challenges for traction control system manufacturers.

- Market Concentration: Analysis of market share distribution among top players (Bosch, Continental, ZF Friedrichshafen, etc.) indicating a moderately concentrated market with significant opportunities for smaller players.

- Innovation Catalysts: Discussion of factors driving innovation, such as stricter safety regulations, the rise of EVs and autonomous vehicles, and consumer demand for advanced driver-assistance systems (ADAS).

- Regulatory Landscape: Evaluation of the impact of global and regional regulations (e.g., emission standards, safety regulations) on market growth and technological advancements.

- Substitute Products: Analysis of potential substitute technologies and their competitive threat to traditional traction control systems.

- End-User Profiles: Segmentation of end-users based on vehicle type (passenger cars, commercial vehicles, etc.) and geographic region.

- M&A Activities: Detailed analysis of M&A activities in the sector, including deal values (in millions of USD), implications for market concentration, and resulting technological advancements. (e.g., Deal A: $XX million, Deal B: $YY million).

Automotive Traction Control Systems Industry Evolution

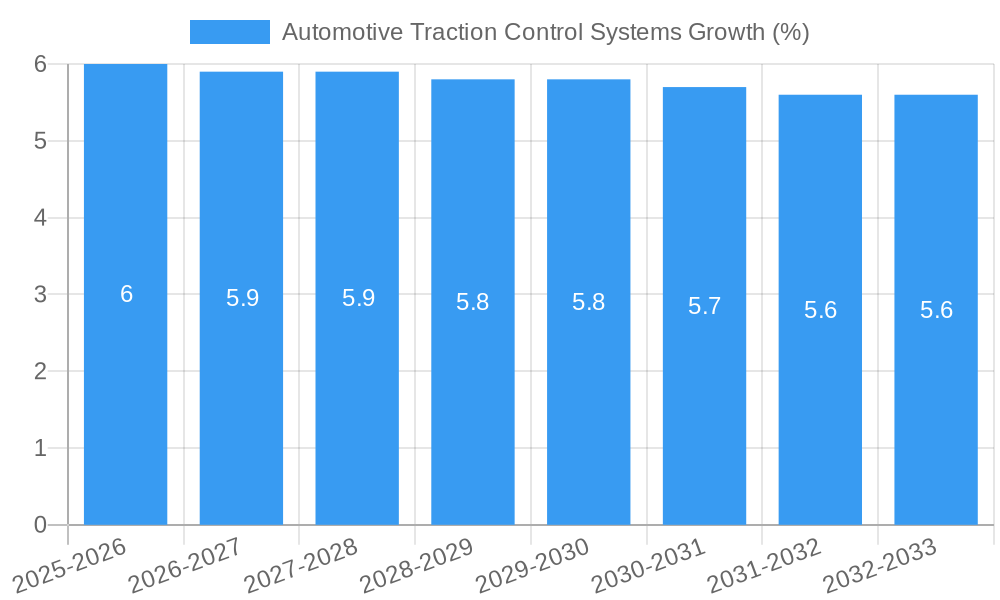

This section provides a comprehensive analysis of the historical and projected growth trajectories of the automotive traction control systems market. We examine technological advancements such as the integration of electronic stability control (ESC) and anti-lock braking systems (ABS), along with the shifting consumer preferences toward improved safety and fuel efficiency. Quantitative data on market growth rates (e.g., CAGR for 2019-2024 and 2025-2033) and adoption rates of advanced traction control technologies will be included. The impact of technological advancements, such as the shift towards electric and autonomous vehicles, on market growth will be thoroughly explored. We will also analyze how evolving consumer demands, such as the preference for enhanced safety and fuel efficiency, are shaping the market. The adoption rate of advanced traction control systems across different vehicle segments and geographical regions will be analyzed in detail. This section will present a narrative examining the interplay of these factors and their impact on the overall market. Specific examples of technological breakthroughs and their impact on market evolution will be provided.

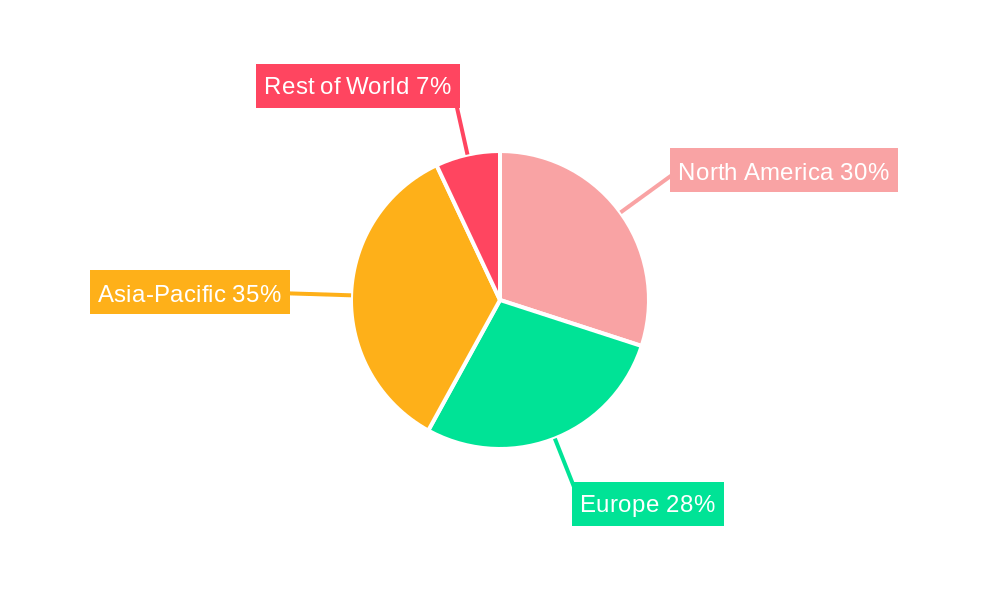

Leading Regions, Countries, or Segments in Automotive Traction Control Systems

This section identifies the dominant regions, countries, and segments within the automotive traction control systems market. We analyze the key factors driving this dominance, including investment trends, governmental support, and market maturity. The detailed analysis will employ a combination of paragraphs and bullet points for clarity and impact. The report will clearly highlight the leading region/country, detailing its contribution to the overall market share.

- Key Drivers in Dominant Region/Country:

- High automotive production volume.

- Significant government investments in automotive infrastructure.

- Favorable regulatory environment promoting safety and emission standards.

- Strong consumer demand for vehicles with advanced safety features.

- Presence of major automotive manufacturers and traction control system suppliers.

Automotive Traction Control Systems Product Innovations

This section highlights recent product innovations, applications, and performance metrics. We discuss unique selling propositions (USPs) of new products and technological advancements influencing the market. This section will showcase innovations like improved algorithms for better traction control, integration with other ADAS features, and the use of advanced sensor technologies to improve performance.

Propelling Factors for Automotive Traction Control Systems Growth

This section identifies key growth drivers, such as technological advancements, economic factors, and regulatory changes, providing specific examples and quantifiable data wherever possible. The increasing demand for safer and more fuel-efficient vehicles will be discussed, along with the rising adoption of ADAS. Growth in the global automotive industry and the rising demand for electric vehicles (EVs) will also be examined.

Obstacles in the Automotive Traction Control Systems Market

This section identifies and analyzes barriers to market growth, such as regulatory hurdles, supply chain disruptions, and intensifying competition. We will quantify the impact of these challenges, using relevant data wherever available. The impact of supply chain disruptions on raw material costs and production will be evaluated.

Future Opportunities in Automotive Traction Control Systems

This section highlights emerging opportunities in new markets, technologies, or consumer trends. The report will explore opportunities presented by the increasing adoption of autonomous vehicles, connected cars, and the ongoing shift towards EVs.

Major Players in the Automotive Traction Control Systems Ecosystem

- Bosch

- Continental

- ZF Friedrichshafen

- Denso

- Aisin Seiki

- Magna International

- JTEKT Corporation

- Mando Corporation

- GKN Automotive

- Schaeffler

- Hitachi Automotive Systems

- Eaton

- BorgWarner

- Haldex

- WABCO

- Dana Incorporated

- Knorr-Bremse

- Nidec Corporation

- Oerlikon Graziano

- Rheinmetall Automotive

- Ricardo

- TRW Automotive

- Valeo

- SKF

- Punch Powertrain

Key Developments in Automotive Traction Control Systems Industry

- [Year/Month]: Launch of a new traction control system with enhanced features by [Company Name].

- [Year/Month]: Acquisition of [Company A] by [Company B] resulting in increased market share.

- [Year/Month]: Introduction of new regulations impacting traction control system design and performance.

- [Year/Month]: Significant investment in R&D for advanced traction control technologies by [Company Name].

Strategic Automotive Traction Control Systems Market Forecast

This section summarizes the key growth catalysts and market potential for the automotive traction control systems market over the forecast period (2025-2033). We highlight the continuing growth in the global automotive industry, particularly in developing economies, and its impact on the demand for traction control systems. The ongoing integration of traction control systems with other ADAS technologies will also be discussed, alongside the increasing emphasis on safety and fuel efficiency in the automotive sector. The report provides a concise summary of the opportunities and challenges ahead, offering insights into the potential market size and growth trajectory for the coming years.

Automotive Traction Control Systems Segmentation

- 1. Application

- 2. Types

Automotive Traction Control Systems Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Automotive Traction Control Systems REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Automotive Traction Control Systems Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Bosch

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Continental

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 ZF Friedrichshafen

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Denso

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Aisin Seiki

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Magna International

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 JTEKT Corporation

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Mando Corporation

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 GKN Automotive

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Schaeffler

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Hitachi Automotive Systems

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Eaton

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 BorgWarner

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Haldex

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 WABCO

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 Dana Incorporated

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 Knorr-Bremse

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.18 Nidec Corporation

- 6.2.18.1. Overview

- 6.2.18.2. Products

- 6.2.18.3. SWOT Analysis

- 6.2.18.4. Recent Developments

- 6.2.18.5. Financials (Based on Availability)

- 6.2.19 Oerlikon Graziano

- 6.2.19.1. Overview

- 6.2.19.2. Products

- 6.2.19.3. SWOT Analysis

- 6.2.19.4. Recent Developments

- 6.2.19.5. Financials (Based on Availability)

- 6.2.20 Rheinmetall Automotive

- 6.2.20.1. Overview

- 6.2.20.2. Products

- 6.2.20.3. SWOT Analysis

- 6.2.20.4. Recent Developments

- 6.2.20.5. Financials (Based on Availability)

- 6.2.21 Ricardo

- 6.2.21.1. Overview

- 6.2.21.2. Products

- 6.2.21.3. SWOT Analysis

- 6.2.21.4. Recent Developments

- 6.2.21.5. Financials (Based on Availability)

- 6.2.22 TRW Automotive

- 6.2.22.1. Overview

- 6.2.22.2. Products

- 6.2.22.3. SWOT Analysis

- 6.2.22.4. Recent Developments

- 6.2.22.5. Financials (Based on Availability)

- 6.2.23 Valeo

- 6.2.23.1. Overview

- 6.2.23.2. Products

- 6.2.23.3. SWOT Analysis

- 6.2.23.4. Recent Developments

- 6.2.23.5. Financials (Based on Availability)

- 6.2.24 SKF

- 6.2.24.1. Overview

- 6.2.24.2. Products

- 6.2.24.3. SWOT Analysis

- 6.2.24.4. Recent Developments

- 6.2.24.5. Financials (Based on Availability)

- 6.2.25 Punch Powertrain

- 6.2.25.1. Overview

- 6.2.25.2. Products

- 6.2.25.3. SWOT Analysis

- 6.2.25.4. Recent Developments

- 6.2.25.5. Financials (Based on Availability)

- 6.2.1 Bosch

List of Figures

- Figure 1: Automotive Traction Control Systems Revenue Breakdown (million, %) by Product 2024 & 2032

- Figure 2: Automotive Traction Control Systems Share (%) by Company 2024

List of Tables

- Table 1: Automotive Traction Control Systems Revenue million Forecast, by Region 2019 & 2032

- Table 2: Automotive Traction Control Systems Revenue million Forecast, by Application 2019 & 2032

- Table 3: Automotive Traction Control Systems Revenue million Forecast, by Types 2019 & 2032

- Table 4: Automotive Traction Control Systems Revenue million Forecast, by Region 2019 & 2032

- Table 5: Automotive Traction Control Systems Revenue million Forecast, by Application 2019 & 2032

- Table 6: Automotive Traction Control Systems Revenue million Forecast, by Types 2019 & 2032

- Table 7: Automotive Traction Control Systems Revenue million Forecast, by Country 2019 & 2032

- Table 8: United Kingdom Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Germany Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: France Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Italy Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 12: Spain Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 13: Netherlands Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 14: Belgium Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Sweden Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Norway Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Poland Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Denmark Automotive Traction Control Systems Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Traction Control Systems?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Automotive Traction Control Systems?

Key companies in the market include Bosch, Continental, ZF Friedrichshafen, Denso, Aisin Seiki, Magna International, JTEKT Corporation, Mando Corporation, GKN Automotive, Schaeffler, Hitachi Automotive Systems, Eaton, BorgWarner, Haldex, WABCO, Dana Incorporated, Knorr-Bremse, Nidec Corporation, Oerlikon Graziano, Rheinmetall Automotive, Ricardo, TRW Automotive, Valeo, SKF, Punch Powertrain.

3. What are the main segments of the Automotive Traction Control Systems?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3900.00, USD 5850.00, and USD 7800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Traction Control Systems," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Traction Control Systems report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Traction Control Systems?

To stay informed about further developments, trends, and reports in the Automotive Traction Control Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence