Key Insights

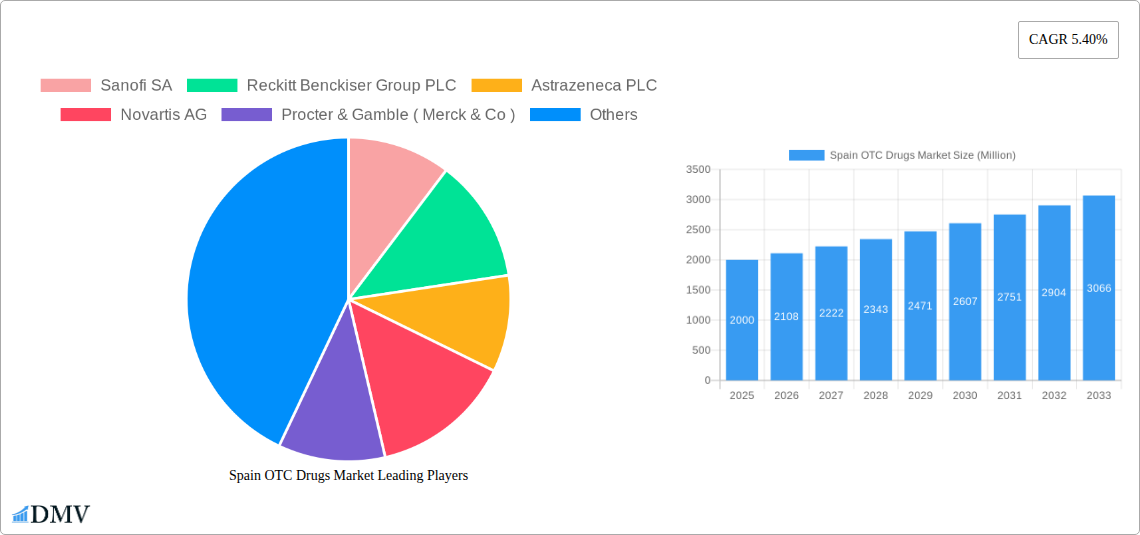

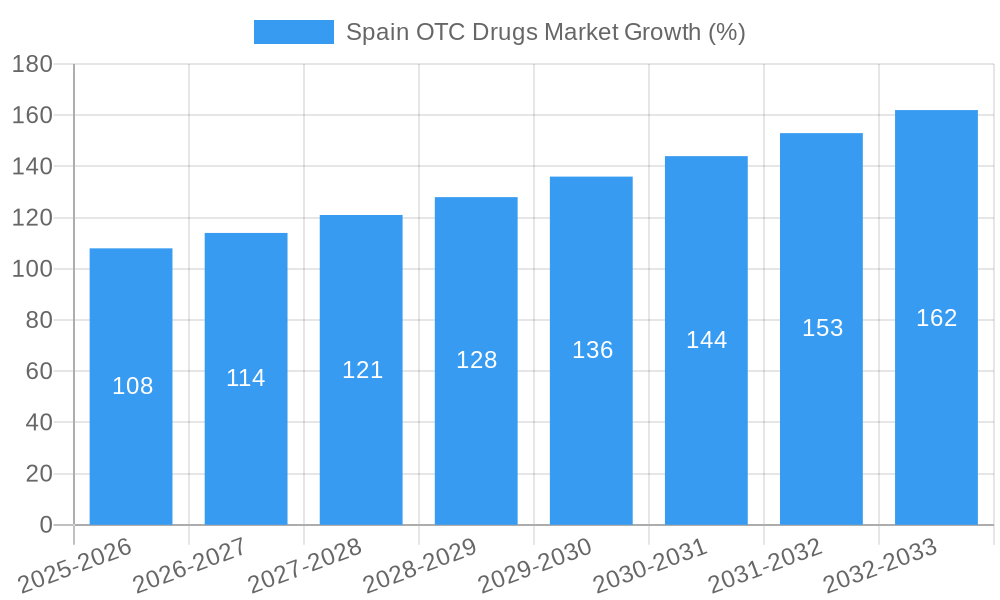

The Spain OTC Drugs Market, valued at approximately €[Estimate based on market size XX and currency conversion, for example: 2 Billion] in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 5.40% from 2025 to 2033. This growth is fueled by several key drivers. The increasing prevalence of chronic conditions like allergies, gastrointestinal issues, and pain, coupled with rising healthcare costs and increased self-medication practices, are significantly boosting demand for readily available over-the-counter (OTC) medications. Furthermore, the growing popularity of online pharmacies, providing convenient access to a wider range of products, contributes to market expansion. The market is segmented by product type (Cough, Cold & Flu; Analgesics; Dermatology; Gastrointestinal; Vitamins, Minerals & Supplements; Weight-loss/Dietary; Ophthalmic; Sleeping Aids; Other) and distribution channels (Retail Pharmacies, Online Pharmacies, Other). While the retail pharmacy segment currently dominates, the online channel is experiencing rapid growth, driven by factors such as ease of access and competitive pricing.

However, the market faces certain restraints. Stringent regulatory frameworks surrounding OTC drug approvals and marketing, along with concerns regarding potential misuse and adverse effects of self-medication, pose challenges. Furthermore, the increasing popularity of alternative and complementary medicine might partially restrict the growth of the conventional OTC drug market. Nevertheless, the robust growth in the aging population in Spain, necessitating a greater need for pain relief and other OTC medications, is poised to counteract these limitations. Key players like Sanofi, Reckitt Benckiser, AstraZeneca, and others are focusing on innovation, product diversification, and strategic partnerships to maintain a strong foothold in this competitive market. The forecast period of 2025-2033 anticipates continued growth, propelled by factors including increased health awareness, improved product accessibility, and strategic marketing initiatives by major players.

Spain OTC Drugs Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the Spain OTC drugs market, encompassing market size, growth trends, leading players, and future opportunities. The study period covers 2019-2033, with 2025 as the base and estimated year, and a forecast period of 2025-2033. The historical period analyzed is 2019-2024. This report is crucial for stakeholders seeking to understand the dynamics of this lucrative market and make informed strategic decisions. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033.

Spain OTC Drugs Market Composition & Trends

This section delves into the competitive landscape of the Spain OTC drugs market, analyzing market concentration, innovation drivers, regulatory frameworks, substitute products, and end-user demographics. We examine the impact of mergers and acquisitions (M&A) activities, providing insights into deal values and market share distribution among key players. The report highlights the roles of companies like Sanofi SA, Reckitt Benckiser Group PLC, AstraZeneca PLC, Novartis AG, Procter & Gamble (Merck & Co), Leo Pharma AS, Bristol-Myers Squibb, Johnson & Johnson, Cardinal Health, Takeda Pharmaceutical Company Ltd, Bayer, GlaxoSmithKline PLC, and Pfizer Inc.

- Market Concentration: The market exhibits a [Describe concentration level, e.g., moderately concentrated] structure, with the top 5 players holding approximately [xx]% market share in 2025.

- Innovation Catalysts: Focus on R&D investments in targeted therapies and personalized medicine fuels innovation.

- Regulatory Landscape: Analysis of the Spanish Agency of Medicines and Medical Devices (AEMPS) regulations and their impact on market access and product approvals.

- Substitute Products: Evaluation of the availability and impact of herbal remedies and homeopathic alternatives.

- End-User Profiles: Segmentation of consumers based on age, health conditions, and purchasing behavior.

- M&A Activities: Detailed analysis of significant M&A deals in the historical period, including deal values and their impact on market dynamics (e.g., xx Million deal between Company A and Company B in 2022).

Spain OTC Drugs Market Industry Evolution

This section meticulously traces the evolution of the Spain OTC drugs market, analyzing growth trajectories, technological advancements, and changing consumer preferences from 2019 to 2033. The report meticulously quantifies growth rates, adoption metrics for innovative products, and the impact of external factors shaping market expansion. We examine trends in digital marketing, e-commerce penetration and its impact on sales distribution, and evolving consumer health awareness. The rise of personalized medicine and the impact of telehealth on market growth are key focus areas.

Leading Regions, Countries, or Segments in Spain OTC Drugs Market

This section identifies the dominant regions, countries, and product segments within the Spain OTC drugs market. It provides a granular breakdown of performance across key categories, pinpointing the drivers behind their market leadership.

Leading Product Segments:

- Analgesics: High demand driven by an aging population and prevalence of musculoskeletal disorders.

- Cough, Cold, and Flu Products: Seasonal demand fluctuations analyzed.

- Dermatology Products: Growing market influenced by increasing awareness of skincare. Key Drivers: Rising disposable income and increased focus on aesthetics.

- Gastrointestinal Products: Strong demand due to lifestyle factors and digestive health concerns. Key Drivers: Increased prevalence of digestive issues and rising consumer awareness of gut health.

- Vitamin, Mineral, and Supplement (VMS) Products: Driven by a wellness trend and increased focus on preventative health. Key Drivers: Growing popularity of functional foods and supplements.

- Other Product Types: Analysis of minor yet relevant segment contributions.

Leading Distribution Channels:

- Retail Pharmacies: Still the dominant channel, benefiting from accessibility and expert advice. Key Drivers: Trust and convenience associated with brick-and-mortar pharmacies.

- Online Pharmacies: Rapid growth driven by convenience and competitive pricing. Key Drivers: Increased internet penetration and convenience of online shopping.

- Other Distribution Channels: Analysis of supermarkets, hypermarkets and other channels.

Spain OTC Drugs Market Product Innovations

This section showcases recent product innovations, highlighting their applications and performance metrics. We analyze unique selling propositions (USPs), technological advancements impacting product efficacy, safety, and patient compliance. Examples of novel formulations, delivery systems, and active ingredients will be detailed, alongside market feedback and early adoption data.

Propelling Factors for Spain OTC Drugs Market Growth

Several key factors contribute to the growth of the Spain OTC drugs market. These include a rising elderly population increasing demand for chronic disease management medications; increased consumer awareness of self-care and preventative health; growing adoption of e-commerce for pharmaceutical purchases; and supportive government policies promoting access to affordable healthcare. Technological advancements in drug formulation and delivery systems also contribute to market expansion.

Obstacles in the Spain OTC Drugs Market

The Spain OTC drugs market faces challenges including stringent regulatory hurdles for new product approvals; the potential for supply chain disruptions impacting availability and pricing; and intense competition from both established players and new entrants. Pricing pressures and fluctuations in raw material costs also add complexities to market operations.

Future Opportunities in Spain OTC Drugs Market

Emerging opportunities in the Spain OTC drugs market include growth in personalized medicine; the development of innovative drug delivery systems (e.g., transdermal patches); increased demand for nutraceuticals; and the expansion of telehealth services. These trends promise increased market reach and potential.

Major Players in the Spain OTC Drugs Market Ecosystem

- Sanofi SA

- Reckitt Benckiser Group PLC

- AstraZeneca PLC

- Novartis AG

- Procter & Gamble (Merck & Co)

- Leo Pharma AS

- Bristol-Myers Squibb

- Johnson & Johnson

- Cardinal Health

- Takeda Pharmaceutical Company Ltd

- Bayer

- GlaxoSmithKline PLC

- Pfizer Inc

Key Developments in Spain OTC Drugs Market Industry

- [Month, Year]: Launch of new analgesic formulation by [Company Name].

- [Month, Year]: Acquisition of [Company A] by [Company B] for xx Million.

- [Month, Year]: Approval of new dermatology product by AEMPS.

- [Month, Year]: Introduction of a new online pharmacy platform by [Company Name].

- [Month, Year]: New marketing campaign launched by [Company Name].

Strategic Spain OTC Drugs Market Forecast

The Spain OTC drugs market is poised for robust growth driven by an aging population, increased consumer awareness, and technological advancements. The expansion of e-commerce, coupled with the growing adoption of personalized medicine, presents significant opportunities for market players. Continued investment in R&D and innovative product launches will be pivotal in shaping the future trajectory of this dynamic market. The increasing demand for convenience and accessibility of healthcare are likely to fuel growth in the online pharmacy segment and drive market expansion in the coming years.

Spain OTC Drugs Market Segmentation

-

1. Product

- 1.1. Cough, Cold, and Flu Products

- 1.2. Analgesics

- 1.3. Dermatology Products

- 1.4. Gastrointestinal Products

- 1.5. Vitamin, Mineral, and Supplement (VMS) Products

- 1.6. Weight-loss/Dietary Products

- 1.7. Ophthalmic Products

- 1.8. Sleeping Aids

- 1.9. Other Product Types

-

2. Distribution Channel

- 2.1. Retail Pharmacies

- 2.2. Online Pharmacies

- 2.3. Other Distribution Channels

Spain OTC Drugs Market Segmentation By Geography

- 1. Spain

Spain OTC Drugs Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.40% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Inclination of Pharmaceutical Companies to Switch From Rx to OTC Drugs; Increasing Self Medication Among the General Population; High Penetration in Emerging Markets

- 3.3. Market Restrains

- 3.3.1. Incorrect Self Diagnosis; Probability of Substance Abuse

- 3.4. Market Trends

- 3.4.1 The Cough

- 3.4.2 Cold

- 3.4.3 and Flu Products Segment is Expected to Dominate the Market over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Spain OTC Drugs Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Cough, Cold, and Flu Products

- 5.1.2. Analgesics

- 5.1.3. Dermatology Products

- 5.1.4. Gastrointestinal Products

- 5.1.5. Vitamin, Mineral, and Supplement (VMS) Products

- 5.1.6. Weight-loss/Dietary Products

- 5.1.7. Ophthalmic Products

- 5.1.8. Sleeping Aids

- 5.1.9. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Retail Pharmacies

- 5.2.2. Online Pharmacies

- 5.2.3. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Sanofi SA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Reckitt Benckiser Group PLC

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Astrazeneca PLC

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Novartis AG

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Procter & Gamble ( Merck & Co )

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Leo Pharma AS

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Bristol-Myers Squibb

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Johnson and Johnson

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Cardinal Health

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Takeda Pharamaceutical Company Ltd

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Bayer

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 GlaxoSmithKline PLC

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Pfizer Inc

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.1 Sanofi SA

List of Figures

- Figure 1: Spain OTC Drugs Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Spain OTC Drugs Market Share (%) by Company 2024

List of Tables

- Table 1: Spain OTC Drugs Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Spain OTC Drugs Market Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Spain OTC Drugs Market Revenue Million Forecast, by Product 2019 & 2032

- Table 4: Spain OTC Drugs Market Volume K Unit Forecast, by Product 2019 & 2032

- Table 5: Spain OTC Drugs Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 6: Spain OTC Drugs Market Volume K Unit Forecast, by Distribution Channel 2019 & 2032

- Table 7: Spain OTC Drugs Market Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Spain OTC Drugs Market Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: Spain OTC Drugs Market Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Spain OTC Drugs Market Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: Spain OTC Drugs Market Revenue Million Forecast, by Product 2019 & 2032

- Table 12: Spain OTC Drugs Market Volume K Unit Forecast, by Product 2019 & 2032

- Table 13: Spain OTC Drugs Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 14: Spain OTC Drugs Market Volume K Unit Forecast, by Distribution Channel 2019 & 2032

- Table 15: Spain OTC Drugs Market Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Spain OTC Drugs Market Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain OTC Drugs Market?

The projected CAGR is approximately 5.40%.

2. Which companies are prominent players in the Spain OTC Drugs Market?

Key companies in the market include Sanofi SA, Reckitt Benckiser Group PLC, Astrazeneca PLC, Novartis AG, Procter & Gamble ( Merck & Co ), Leo Pharma AS, Bristol-Myers Squibb, Johnson and Johnson, Cardinal Health, Takeda Pharamaceutical Company Ltd, Bayer, GlaxoSmithKline PLC, Pfizer Inc.

3. What are the main segments of the Spain OTC Drugs Market?

The market segments include Product, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Inclination of Pharmaceutical Companies to Switch From Rx to OTC Drugs; Increasing Self Medication Among the General Population; High Penetration in Emerging Markets.

6. What are the notable trends driving market growth?

The Cough. Cold. and Flu Products Segment is Expected to Dominate the Market over the Forecast Period.

7. Are there any restraints impacting market growth?

Incorrect Self Diagnosis; Probability of Substance Abuse.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain OTC Drugs Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain OTC Drugs Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain OTC Drugs Market?

To stay informed about further developments, trends, and reports in the Spain OTC Drugs Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence