Key Insights

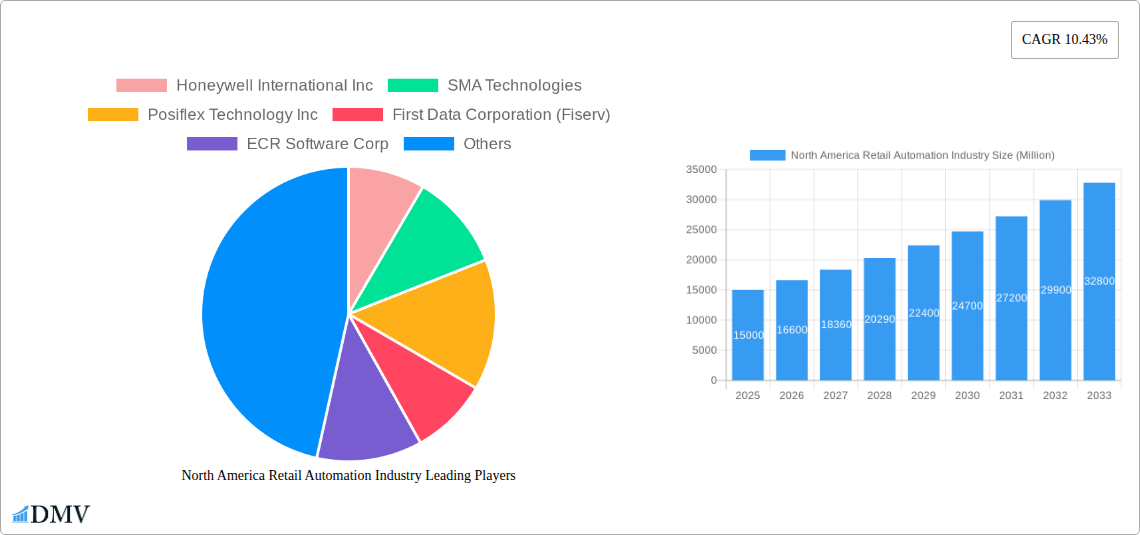

The North American retail automation market is experiencing robust growth, driven by the increasing need for efficiency, enhanced customer experience, and optimized supply chain management within the retail sector. A CAGR of 10.43% from 2019-2033 indicates a significant expansion, with the market valued at an estimated $XX million in 2025. This growth is fueled by several key factors. The proliferation of e-commerce and omnichannel strategies necessitates efficient inventory management, order fulfillment, and customer service solutions, all of which are addressed by retail automation technologies. Furthermore, labor shortages and rising labor costs are incentivizing retailers to adopt automation to maintain profitability and productivity. Specific segments demonstrating strong growth include grocery, driven by the increasing demand for speed and accuracy in order fulfillment and inventory tracking, and general merchandise, where automation assists in managing large and diverse product inventories. The adoption of advanced technologies like AI and machine learning is further accelerating market growth, enabling more sophisticated solutions for tasks such as demand forecasting, personalized shopping experiences, and fraud detection. Hardware solutions, such as point-of-sale (POS) systems, self-checkout kiosks, and automated storage and retrieval systems, are expected to maintain a significant share of the market. However, the high initial investment costs associated with implementing these solutions and the need for skilled workforce to manage and maintain the technology can act as potential restraints.

The competitive landscape is characterized by a mix of established players like Honeywell International Inc., NCR Corporation, and Zebra Technologies Corporation, and specialized solution providers. These companies are continuously innovating and expanding their product portfolios to cater to evolving customer needs. Growth is particularly strong in the United States and Canada, reflecting the high level of retail activity and adoption of advanced technologies in these regions. Future growth will likely be driven by increased investments in AI-powered solutions, integration of IoT devices, and the continued development of sophisticated supply chain management systems designed to streamline the retail process from end-to-end. The market's trajectory suggests significant opportunities for both established vendors and new entrants seeking to capitalize on the accelerating pace of digital transformation in the North American retail landscape. Considering the projected growth and the current market dynamics, a conservative estimate places the 2026 market value at approximately $XX million (assuming a 10.43% growth from a 2025 base of $XX million). Subsequent years can be projected using the same CAGR.

North America Retail Automation Industry: Market Report 2019-2033

This comprehensive report provides a detailed analysis of the North America retail automation industry, encompassing market size, growth drivers, challenges, and future opportunities from 2019 to 2033. The study period (2019-2024) and forecast period (2025-2033), with a base year of 2025 and estimated year of 2025, offer a complete understanding of this rapidly evolving sector. Key players like Honeywell International Inc, SMA Technologies, Posiflex Technology Inc, First Data Corporation (Fiserv), ECR Software Corp, NCR Corporation, Fujitsu Limited, Diebold Nixdorf Incorporated, Zebra Technologies Corporation, and Datalogic SpA are profiled, providing crucial insights into their strategies and market positions. The report segments the market by component (hardware, software), end-user (grocery, general merchandise, hospitality), and country (United States, Canada), delivering a granular view of industry dynamics. The market is expected to reach xx Million by 2033.

North America Retail Automation Industry Market Composition & Trends

This section evaluates the competitive landscape, innovative drivers, regulatory environment, substitute products, end-user profiles, and merger & acquisition (M&A) activities within the North America retail automation market. The market exhibits a moderately concentrated structure, with the top five players holding an estimated xx% market share in 2025. Innovation is driven by advancements in artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT), leading to the development of more sophisticated automation solutions. Regulatory landscapes, such as data privacy regulations, significantly impact the adoption of automation technologies. Substitute products, including manual processes, present competitive pressures. M&A activity has been significant, with deal values exceeding xx Million in the past five years, reflecting industry consolidation.

- Market Share Distribution (2025): Top 5 players - xx%; Others - xx%

- M&A Deal Value (2019-2024): Over xx Million

- Key End-Users: Grocery, General Merchandise, Hospitality

- Innovation Catalysts: AI, ML, IoT

North America Retail Automation Industry Industry Evolution

The North American retail automation industry has experienced substantial growth throughout the historical period (2019-2024), driven by increasing consumer demand for enhanced shopping experiences, operational efficiency improvements, and the need to optimize supply chains. Technological advancements, particularly in areas like AI-powered inventory management and robotics, are significantly contributing to this growth. The market has shown a Compound Annual Growth Rate (CAGR) of xx% during 2019-2024 and is projected to maintain a CAGR of xx% during the forecast period (2025-2033). This growth is further propelled by the increasing adoption of omnichannel strategies and the growing need for real-time data analytics in retail operations. The shift towards e-commerce and the demand for faster delivery times are also major catalysts for automation adoption. The integration of cloud-based solutions and the rise of edge computing are enhancing the capabilities of retail automation systems.

Leading Regions, Countries, or Segments in North America Retail Automation Industry

The United States dominates the North American retail automation market, driven by high technological adoption rates, robust investment in automation technologies, and a large retail sector. The grocery segment is a significant end-user, with supermarkets and hypermarkets leading automation adoption.

Key Drivers:

- United States: High technological adoption, significant retail sector, substantial investment in automation.

- Grocery Segment: Demand for improved inventory management, reduced labor costs, and enhanced customer experience.

- Hardware Component: Increased demand for point-of-sale (POS) systems, self-checkout kiosks, and automated storage and retrieval systems (AS/RS).

Dominance Factors:

The US market’s dominance stems from its mature retail landscape, robust technological infrastructure, and favorable regulatory environment encouraging innovation and investment. The grocery segment’s leading role is attributed to the high volume of transactions and the need for efficient inventory management in large-scale operations. Hardware leads the component segment due to the significant initial investments required for automation infrastructure.

North America Retail Automation Industry Product Innovations

Recent innovations include AI-powered inventory management systems that optimize stock levels and predict demand, robotic process automation (RPA) solutions automating repetitive tasks, and advanced POS systems integrating various payment methods and customer loyalty programs. These innovations enhance efficiency, improve accuracy, and offer personalized customer experiences, leading to increased ROI for retailers. Unique selling propositions focus on scalability, ease of integration with existing systems, and enhanced data analytics capabilities.

Propelling Factors for North America Retail Automation Industry Growth

Several factors drive the growth of the North America retail automation industry: the increasing need for enhanced operational efficiency, the desire for improved customer experiences through personalized services and faster checkout processes, and the growing adoption of omnichannel retail strategies. Government initiatives promoting technological advancement and automation also play a significant role. The rising labor costs and the need for increased productivity further fuel the adoption of automation solutions.

Obstacles in the North America Retail Automation Industry Market

High initial investment costs for automation systems pose a significant barrier for smaller retailers. Supply chain disruptions, particularly in the procurement of critical components, can impact the timely deployment of automation solutions. Intense competition among automation providers can also lead to price pressures. Furthermore, concerns about data security and the potential displacement of workers are important considerations.

Future Opportunities in North America Retail Automation Industry

The increasing adoption of cloud-based automation solutions, the integration of advanced analytics capabilities for improved decision-making, and the expansion into new market segments like quick-service restaurants offer significant opportunities. The development of more sophisticated robotics for tasks like warehouse management and delivery will also contribute to future growth. The increasing focus on sustainable and environmentally friendly automation solutions is an emerging trend.

Major Players in the North America Retail Automation Industry Ecosystem

- Honeywell International Inc

- SMA Technologies

- Posiflex Technology Inc

- First Data Corporation (Fiserv)

- ECR Software Corp

- NCR Corporation

- Fujitsu Limited

- Diebold Nixdorf Incorporated

- Zebra Technologies Corporation

- Datalogic SpA

Key Developments in North America Retail Automation Industry Industry

- April 2023: Walmart Inc. announces plans to automate two-thirds of its stores by the end of 2026, focusing on inventory management and supply chain optimization.

- February 2023: United Natural Foods Inc. (UNFI) partners with ECRS to integrate its Professional Services suite with ECRS' CATAPULT POS system, enhancing functionalities for retailers.

Strategic North America Retail Automation Industry Market Forecast

The North America retail automation market is poised for continued growth, driven by technological advancements, evolving consumer preferences, and the ongoing need for operational efficiencies. The increasing adoption of AI, ML, and IoT technologies will lead to the development of more sophisticated and integrated automation solutions. The focus on personalized customer experiences and seamless omnichannel integration will drive further investment in automation. The market’s expansion into new segments and geographic areas will create substantial opportunities for growth in the coming years.

North America Retail Automation Industry Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

-

2. End-User

- 2.1. Grocery

- 2.2. General

- 2.3. Hospital

North America Retail Automation Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Retail Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.43% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Faster Services; Growth Among Retail Industry and E-commerce; Increasing Retail Automation in Grocery Stores

- 3.3. Market Restrains

- 3.3.1. Slow Adoption of Automated Machine Learning Tools

- 3.4. Market Trends

- 3.4.1. Grocery Segment is expected grow at a higher pace.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Grocery

- 5.2.2. General

- 5.2.3. Hospital

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. United States North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Honeywell International Inc

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 SMA Technologies

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Posiflex Technology Inc

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 First Data Corporation (Fiserv)

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 ECR Software Corp

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 NCR Corporation

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Fujitsu Limited

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Diebold Nixdorf Incorporated

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Zebra Technologies Corporation

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Datalogic SpA

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Honeywell International Inc

List of Figures

- Figure 1: North America Retail Automation Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Retail Automation Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Retail Automation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Retail Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 3: North America Retail Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 4: North America Retail Automation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: North America Retail Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: North America Retail Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 11: North America Retail Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 12: North America Retail Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 13: United States North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Mexico North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Retail Automation Industry?

The projected CAGR is approximately 10.43%.

2. Which companies are prominent players in the North America Retail Automation Industry?

Key companies in the market include Honeywell International Inc, SMA Technologies, Posiflex Technology Inc, First Data Corporation (Fiserv), ECR Software Corp, NCR Corporation, Fujitsu Limited, Diebold Nixdorf Incorporated, Zebra Technologies Corporation, Datalogic SpA.

3. What are the main segments of the North America Retail Automation Industry?

The market segments include Component, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Faster Services; Growth Among Retail Industry and E-commerce; Increasing Retail Automation in Grocery Stores.

6. What are the notable trends driving market growth?

Grocery Segment is expected grow at a higher pace..

7. Are there any restraints impacting market growth?

Slow Adoption of Automated Machine Learning Tools.

8. Can you provide examples of recent developments in the market?

In April 2023, Walmart Inc. plans to automate two-thirds of its stores by the end of 2026 to improve inventory accuracy and flow, reduce costs, and enhance the overall shopping experience. The move is part of the organization’s strategy to reengineer its supply chain and make a more intelligent and connected omnichannel network to meet customers’ needs better. This involves a more significant use of data, intelligent software, and automation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Retail Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Retail Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Retail Automation Industry?

To stay informed about further developments, trends, and reports in the North America Retail Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence