Key Insights

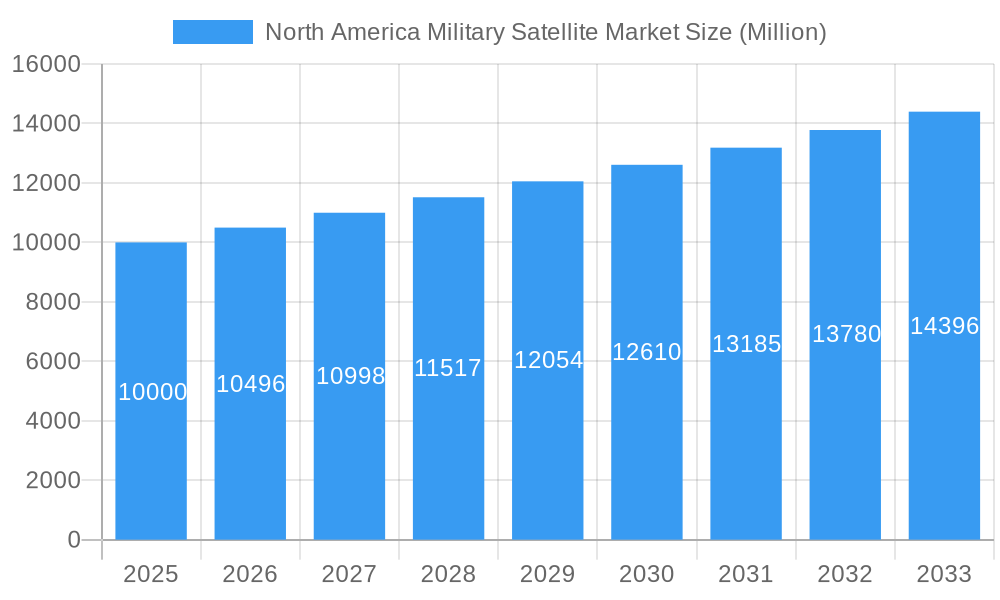

The North American military satellite market is experiencing robust growth, driven by increasing defense budgets, advancements in satellite technology, and the rising demand for enhanced surveillance, communication, and navigation capabilities. The market, valued at approximately $XX million in 2025 (assuming a logical extrapolation based on the provided CAGR and market size data), is projected to maintain a healthy Compound Annual Growth Rate (CAGR) of 4.96% through 2033. This growth is fueled by several key factors. Firstly, the modernization of existing military satellite constellations and the development of new space-based systems are significant contributors. Secondly, the increasing focus on space-based intelligence, surveillance, and reconnaissance (ISR) capabilities is driving demand for advanced satellites with improved resolution and data processing capabilities. Finally, the strategic importance of secure military communication networks relies heavily on resilient and advanced satellite technologies, further propelling market expansion. Within the North American region, the United States is the dominant market, accounting for the lion's share of revenue due to substantial investments in its national security infrastructure and ongoing technological advancements.

North America Military Satellite Market Market Size (In Billion)

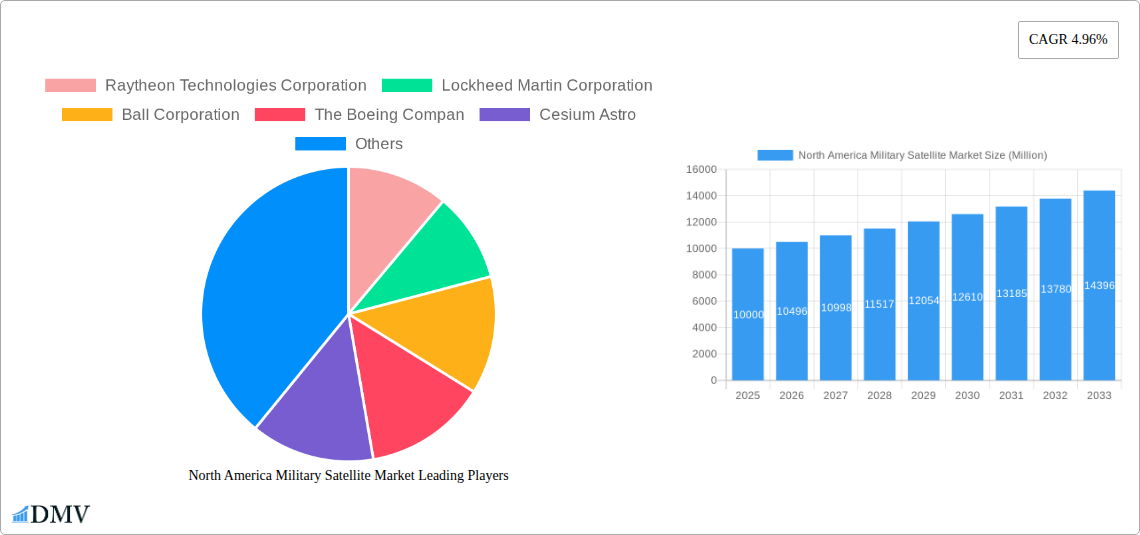

Segmentation analysis reveals significant market potential across various satellite types. Larger satellites (500-1000kg and above 1000kg) are likely to dominate the market due to their greater payload capacity and sophisticated capabilities. Geosynchronous Earth Orbit (GEO) satellites are anticipated to hold a significant market share due to their ability to provide continuous coverage over specific regions, crucial for military applications. The demand for advanced satellite subsystems, such as propulsion hardware, satellite buses, and solar arrays, is expected to increase proportionally to overall market growth. Key players like Raytheon Technologies Corporation, Lockheed Martin Corporation, and Boeing are strategically investing in research and development to maintain their leadership positions and meet the growing demand for next-generation military satellite technology. The competitive landscape is characterized by strong industry consolidation and collaboration, often involving partnerships between prime contractors and specialized subsystem providers.

North America Military Satellite Market Company Market Share

North America Military Satellite Market: A Comprehensive Report (2019-2033)

This insightful report provides a comprehensive analysis of the North America military satellite market, offering invaluable data and forecasts for stakeholders from 2019 to 2033. We delve into market trends, technological advancements, key players, and future growth projections, equipping you with the knowledge needed to navigate this dynamic sector. The report covers a detailed study period from 2019-2024 (historical period), with a base year of 2025 and a forecast period extending to 2033. The total market size is estimated at xx Million in 2025, and is projected to reach xx Million by 2033.

North America Military Satellite Market Composition & Trends

This section examines the North American military satellite market's competitive landscape, identifying key trends shaping its evolution. We analyze market concentration, revealing the market share distribution among leading players like Raytheon Technologies Corporation, Lockheed Martin Corporation, Ball Corporation, The Boeing Company, Cesium Astro, and Northrop Grumman Corporation. The report also assesses the impact of innovation catalysts, including advancements in satellite technology and miniaturization, alongside the regulatory landscape and its influence on market growth. Furthermore, we explore the role of substitute products and the impact of mergers and acquisitions (M&A) activities on market consolidation. M&A deal values for the period are estimated at xx Million, indicating significant market activity.

- Market Concentration: High, with a few major players dominating the market. Detailed market share breakdown is provided within the full report.

- Innovation Catalysts: Miniaturization, improved propulsion systems, and advanced sensors are driving innovation.

- Regulatory Landscape: Government regulations and funding significantly influence market growth.

- Substitute Products: Limited substitutes exist, given the specialized nature of military satellite applications.

- End-User Profiles: Primarily the US Department of Defense (DoD) and other government agencies.

- M&A Activities: Significant M&A activity observed, driven by consolidation and technology acquisition.

North America Military Satellite Market Industry Evolution

This section traces the North America military satellite market's evolution, examining growth trajectories, technological advancements, and shifting demands. We analyze historical growth rates, adoption metrics of various satellite technologies, and projected future growth. The market's expansion is fueled by increasing defense budgets, the need for enhanced surveillance and communication capabilities, and the proliferation of smallsat constellations for diverse military applications. Technological advancements, including the development of more resilient and cost-effective satellites, are further accelerating market growth. Specific data points on growth rates and technology adoption are provided within the detailed report.

Leading Regions, Countries, or Segments in North America Military Satellite Market

This segment pinpoints the leading regions, countries, and segments within the North American military satellite market. The analysis considers various market segmentations, including:

Satellite Mass:

- Below 10 Kg: Growth is driven by the increasing adoption of CubeSats and other small satellites.

- 10-100 kg: This segment represents a significant portion of the market, with continued strong demand.

- 100-500 kg: A crucial segment for medium-sized military satellites.

- 500-1000 kg: This segment caters to heavier payloads requiring more robust capabilities.

- Above 1000 kg: This segment comprises large, high-capacity satellites.

Orbit Class:

- LEO (Low Earth Orbit): Experiencing rapid growth due to increased smallsat deployments.

- MEO (Medium Earth Orbit): A stable segment with consistent demand.

- GEO (Geostationary Orbit): A crucial segment for communication and surveillance applications.

Satellite Subsystem:

- Satellite Bus & Subsystems: A consistently high-demand segment.

- Propulsion Hardware and Propellant: Essential for satellite maneuvering and station-keeping.

- Solar Array & Power Hardware: Critical for providing sustainable power to satellites.

- Structures, Harness & Mechanisms: Crucial for satellite structural integrity and functionality.

Application:

- Communication: A consistently significant segment.

- Earth Observation: Growing rapidly due to enhanced surveillance needs.

- Navigation: A crucial segment for military operations.

- Space Observation: A growing area for tracking space objects and threats.

- Others: This segment encompasses various other specialized military applications.

The dominant segment, based on our analysis, is the LEO orbit class for smallsat constellations (below 100 kg), driven by significant investments in this technology for enhanced situational awareness and communication capabilities. Detailed analysis of each segment's drivers and growth factors is provided in the report.

North America Military Satellite Market Product Innovations

Recent innovations focus on miniaturization, enhanced payload capabilities, increased resilience to space-based threats, and improved cost-effectiveness. These advancements allow for more versatile and efficient military satellite deployments, impacting mission effectiveness and overall operational cost. The emergence of smallsat constellations and the development of advanced sensors for improved intelligence, surveillance, and reconnaissance (ISR) are key examples of these innovations.

Propelling Factors for North America Military Satellite Market Growth

The North American military satellite market's growth is primarily driven by increasing defense budgets, the need for improved global surveillance, enhanced communication capabilities crucial for military operations, and the rise of space-based threats. Technological advancements enabling miniaturization, improved efficiency, and cost-reduction further fuel this growth. Government support and regulatory frameworks encouraging the development and deployment of military satellites also play a significant role.

Obstacles in the North America Military Satellite Market

The market faces challenges, including supply chain disruptions affecting component availability and escalating launch costs. Intense competition among major players also presents an obstacle, potentially leading to price wars and impacting profitability. Furthermore, stringent regulatory environments and the complexities associated with space launch operations can constrain market growth. These factors are quantified in the detailed report.

Future Opportunities in North America Military Satellite Market

Emerging opportunities lie in the development of advanced space-based ISR capabilities, including hypersonic missile detection and tracking, and the integration of AI and machine learning for enhanced satellite autonomy and data analysis. The expansion of smallsat constellations for both communication and observation applications and increasing reliance on space-based positioning, navigation, and timing (PNT) systems also present lucrative opportunities.

Major Players in the North America Military Satellite Market Ecosystem

Key Developments in North America Military Satellite Market Industry

- November 2023: Ball Aerospace secured a contract from the US Air Force to deliver the WSF-M weather satellite system for the DoD, showcasing the demand for advanced environmental monitoring capabilities.

- February 2023: Raytheon Technologies' subsidiary, Blue Canyon Technologies, contributed significantly to the Transporter-6 launch, highlighting the growing importance of smallsat technologies.

Strategic North America Military Satellite Market Forecast

The North American military satellite market exhibits robust growth potential, driven by sustained technological advancements, increasing defense spending, and heightened geopolitical uncertainty. Future growth hinges on continued investments in miniaturization, AI integration for improved data analytics, and the development of resilient space architectures to counter emerging threats. The market is poised for substantial expansion, with opportunities across various segments, particularly in LEO constellations and advanced sensor technologies.

North America Military Satellite Market Segmentation

-

1. Satellite Mass

- 1.1. 10-100kg

- 1.2. 100-500kg

- 1.3. 500-1000kg

- 1.4. Below 10 Kg

- 1.5. above 1000kg

-

2. Orbit Class

- 2.1. GEO

- 2.2. LEO

- 2.3. MEO

-

3. Satellite Subsystem

- 3.1. Propulsion Hardware and Propellant

- 3.2. Satellite Bus & Subsystems

- 3.3. Solar Array & Power Hardware

- 3.4. Structures, Harness & Mechanisms

-

4. Application

- 4.1. Communication

- 4.2. Earth Observation

- 4.3. Navigation

- 4.4. Space Observation

- 4.5. Others

North America Military Satellite Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

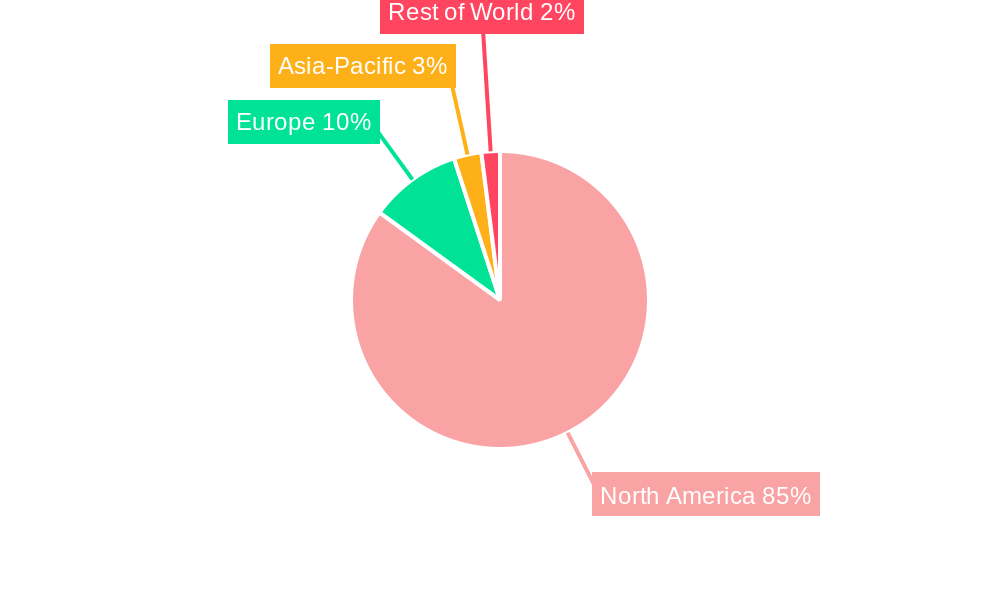

North America Military Satellite Market Regional Market Share

Geographic Coverage of North America Military Satellite Market

North America Military Satellite Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 5.1.1. 10-100kg

- 5.1.2. 100-500kg

- 5.1.3. 500-1000kg

- 5.1.4. Below 10 Kg

- 5.1.5. above 1000kg

- 5.2. Market Analysis, Insights and Forecast - by Orbit Class

- 5.2.1. GEO

- 5.2.2. LEO

- 5.2.3. MEO

- 5.3. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 5.3.1. Propulsion Hardware and Propellant

- 5.3.2. Satellite Bus & Subsystems

- 5.3.3. Solar Array & Power Hardware

- 5.3.4. Structures, Harness & Mechanisms

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. Communication

- 5.4.2. Earth Observation

- 5.4.3. Navigation

- 5.4.4. Space Observation

- 5.4.5. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 6. North America Military Satellite Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 6.1.1. 10-100kg

- 6.1.2. 100-500kg

- 6.1.3. 500-1000kg

- 6.1.4. Below 10 Kg

- 6.1.5. above 1000kg

- 6.2. Market Analysis, Insights and Forecast - by Orbit Class

- 6.2.1. GEO

- 6.2.2. LEO

- 6.2.3. MEO

- 6.3. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 6.3.1. Propulsion Hardware and Propellant

- 6.3.2. Satellite Bus & Subsystems

- 6.3.3. Solar Array & Power Hardware

- 6.3.4. Structures, Harness & Mechanisms

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. Communication

- 6.4.2. Earth Observation

- 6.4.3. Navigation

- 6.4.4. Space Observation

- 6.4.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Raytheon Technologies Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Lockheed Martin Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Ball Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 The Boeing Compan

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Cesium Astro

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Northrop Grumman Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.1 Raytheon Technologies Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Military Satellite Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Military Satellite Market Share (%) by Company 2025

List of Tables

- Table 1: North America Military Satellite Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 2: North America Military Satellite Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 3: North America Military Satellite Market Revenue billion Forecast, by Satellite Subsystem 2020 & 2033

- Table 4: North America Military Satellite Market Revenue billion Forecast, by Application 2020 & 2033

- Table 5: North America Military Satellite Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: North America Military Satellite Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 7: North America Military Satellite Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 8: North America Military Satellite Market Revenue billion Forecast, by Satellite Subsystem 2020 & 2033

- Table 9: North America Military Satellite Market Revenue billion Forecast, by Application 2020 & 2033

- Table 10: North America Military Satellite Market Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States North America Military Satellite Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada North America Military Satellite Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico North America Military Satellite Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Military Satellite Market?

The projected CAGR is approximately 6.8%.

2. Which companies are prominent players in the North America Military Satellite Market?

Key companies in the market include Raytheon Technologies Corporation, Lockheed Martin Corporation, Ball Corporation, The Boeing Compan, Cesium Astro, Northrop Grumman Corporation.

3. What are the main segments of the North America Military Satellite Market?

The market segments include Satellite Mass, Orbit Class, Satellite Subsystem, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

November 2023: Ball Aerospace was selected by the US Air Force's Space and Missile Systems Center (SMC) to deliver the next-generation operational environmental satellite system, Weather System Follow-on - Microwave (WSF-M), for the Department of Defense (DoD).February 2023: Blue Canyon Technologies LLC, a subsidiary of Raytheon Technologies, provided critical hardware components for several of the smallsat missions aboard the Transporter-6 launch, which pitched 114 small payloads into polar orbit.February 2023: Blue Canyon Technologies LLC, a subsidiary of Raytheon Technologies, provided critical hardware components for several of the SmallSat missions aboard the Transporter-6 launch that pitched 114 small payloads into polar orbit.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Military Satellite Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Military Satellite Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Military Satellite Market?

To stay informed about further developments, trends, and reports in the North America Military Satellite Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence