Key Insights

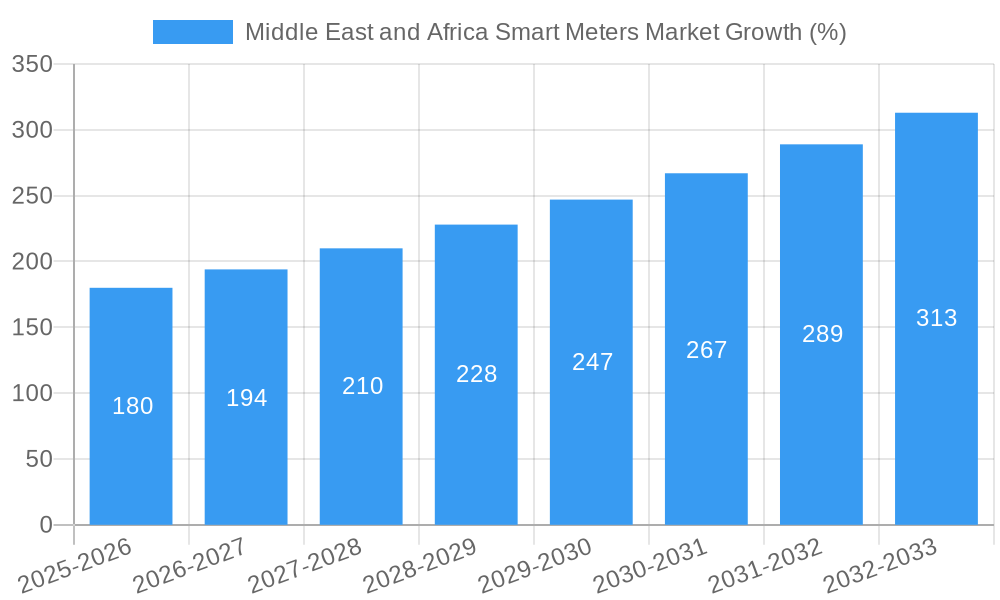

The Middle East and Africa Smart Meters Market is experiencing robust growth, driven by increasing urbanization, rising electricity demand, and government initiatives promoting energy efficiency and smart grid infrastructure. A CAGR of 7.20% from 2019-2033 suggests a significant expansion, with the market projected to reach substantial value by 2033. While precise figures for the Middle East and Africa are unavailable in the provided data, we can infer substantial growth based on the overall market trends and the high adoption rate of smart meters in developing economies. Key factors fueling this growth include the need to reduce energy losses, improve billing accuracy, and enhance grid management. The residential segment is expected to dominate the market share, driven by increasing household electrification and consumer demand for advanced metering solutions. However, the commercial and industrial sectors also present significant opportunities, particularly as businesses seek to optimize energy consumption and reduce operational costs. Further growth will be driven by technological advancements like the incorporation of advanced communication protocols (e.g., NB-IoT, LoRaWAN) and the integration of smart meters with broader energy management systems. Challenges remain, such as the high initial investment costs associated with smart meter deployments, especially in less developed regions, and the need for robust infrastructure to support data communication. However, the long-term benefits of smart meters in terms of energy efficiency, cost savings, and improved grid management are expected to outweigh these challenges, ensuring sustained market expansion.

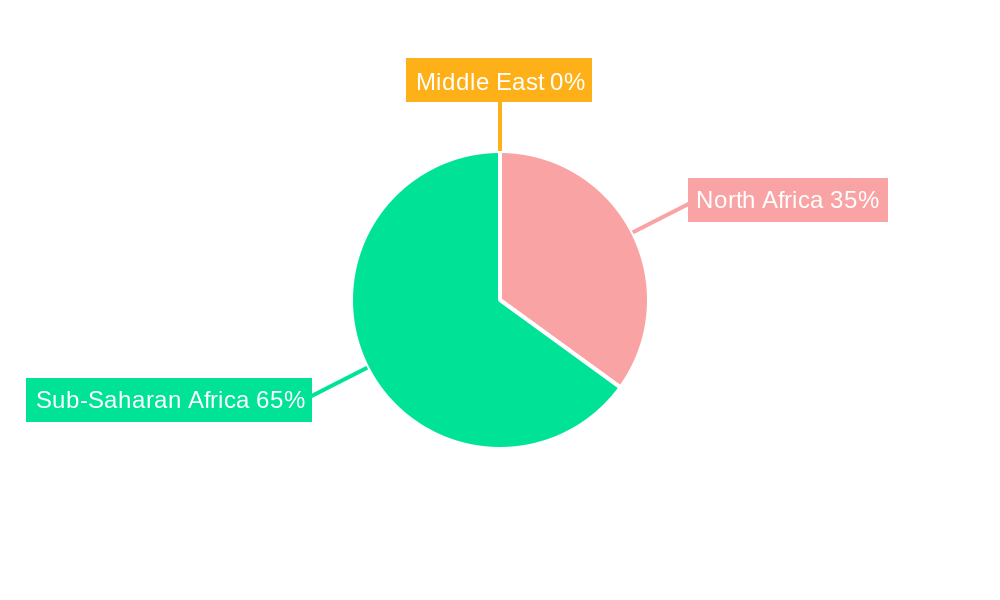

The adoption of smart gas and water meters is also anticipated to increase significantly during the forecast period. This is particularly relevant for water-stressed regions in Africa, where smart water metering can help in efficient resource management and reduce water loss. South Africa, with its relatively developed infrastructure, is expected to lead the regional market. However, significant growth potential exists in other African countries as government initiatives and investments in infrastructure development accelerate. The competitive landscape is characterized by both established international players and local companies, creating a dynamic market with potential for both consolidation and diversification. The continuous innovation in smart meter technology, combined with favorable government policies, suggests that the Middle East and Africa Smart Meters market is poised for considerable expansion in the coming years.

Middle East and Africa Smart Meters Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the Middle East and Africa Smart Meters Market, offering valuable insights for stakeholders across the value chain. Covering the period 2019-2033, with a focus on 2025, this comprehensive study unveils market trends, growth drivers, challenges, and future opportunities within this dynamic sector. The report meticulously examines various segments, including smart electricity, gas, and water meters, across residential, commercial, and industrial end-user categories, providing a granular understanding of market dynamics across the region. The market is projected to reach xx Million by 2033.

Middle East and Africa Smart Meters Market Composition & Trends

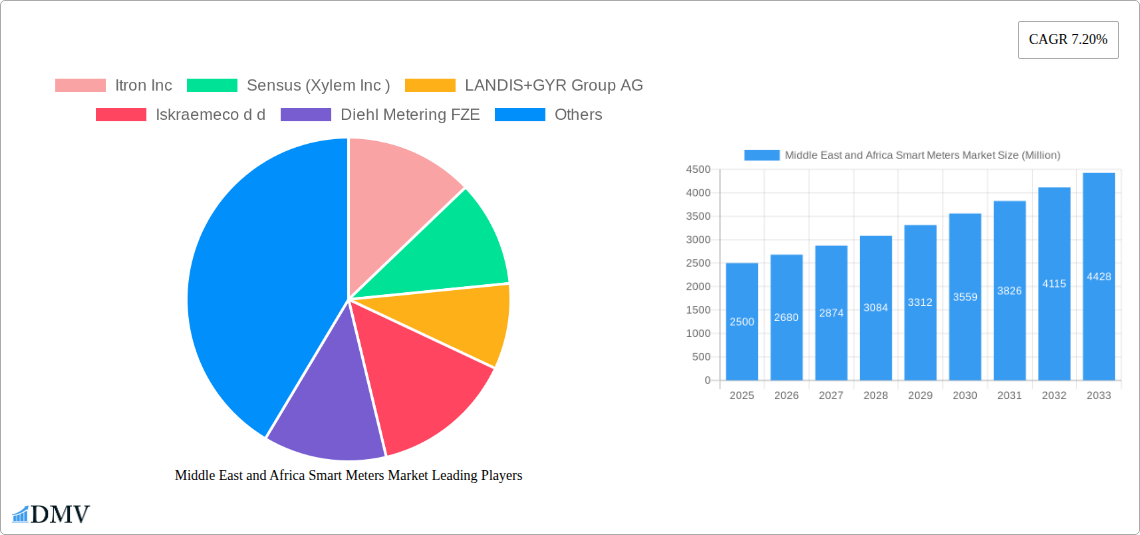

This section delves into the competitive landscape of the Middle East and Africa smart meters market, analyzing market concentration, innovation drivers, regulatory frameworks, substitute products, end-user profiles, and mergers and acquisitions (M&A) activity. We examine the market share distribution amongst key players, highlighting the strategies employed by leading companies. The report also assesses the impact of evolving regulatory landscapes on market growth and the role of technological advancements in shaping market dynamics. The estimated market size in 2025 is xx Million.

- Market Concentration: The market exhibits a moderately concentrated structure, with key players holding significant market shares. Analysis of market share data reveals that Itron Inc and Landis+Gyr Group AG account for approximately xx% of the total market share in 2025.

- Innovation Catalysts: Government initiatives promoting smart grid infrastructure are significant innovation drivers, alongside the rising demand for enhanced energy efficiency and improved water resource management.

- Regulatory Landscape: Varying regulatory policies across different countries impact market growth; some nations have implemented supportive policies to encourage adoption of smart meters, while others are still in the initial stages of development.

- Substitute Products: While smart meters offer superior functionality, traditional metering systems remain a potential substitute in some areas, particularly where cost constraints exist.

- End-User Profiles: The report provides detailed profiles of residential, commercial, and industrial end-users, assessing their specific needs and adoption rates for different types of smart meters.

- M&A Activity: The report analyzes recent M&A deals in the smart meters industry, examining their impact on market consolidation and competitive dynamics. The total value of M&A transactions in the period 2019-2024 is estimated at xx Million.

Middle East and Africa Smart Meters Market Industry Evolution

This section analyzes the historical and projected growth trajectories of the Middle East and Africa smart meters market. We examine the impact of technological advancements, such as advanced communication technologies (e.g., NB-IoT, LoRaWAN), and evolving consumer demands on market evolution. The analysis also considers factors such as increasing urbanization, rising energy consumption, and growing awareness of water conservation, all of which drive adoption rates. The market witnessed a Compound Annual Growth Rate (CAGR) of xx% during 2019-2024 and is projected to grow at a CAGR of xx% from 2025 to 2033. Key aspects of this evolution include:

The adoption of advanced metering infrastructure (AMI) across various countries.

The gradual shift from traditional meters to smart meters driven by government initiatives and economic incentives.

The increasing integration of smart meters with smart grid initiatives and renewable energy sources.

Technological innovations leading to more cost-effective and feature-rich smart meters.

Leading Regions, Countries, or Segments in Middle East and Africa Smart Meters Market

This section identifies the leading regions, countries, and segments within the Middle East and Africa smart meters market. Analysis focuses on factors driving market dominance within each segment:

Dominant Region: The United Arab Emirates (UAE) and Saudi Arabia emerge as leading countries in the Middle East segment, driven by substantial investments in smart city infrastructure and a commitment to improving energy efficiency. South Africa takes a similar position in the African segment.

Key Drivers for UAE & Saudi Arabia:

- Substantial investments in smart city infrastructure projects.

- Government support and regulatory frameworks promoting smart meter adoption.

- Focus on enhancing energy efficiency and reducing energy losses.

- High levels of technological advancement and infrastructure readiness.

Key Drivers for South Africa:

- Increasing demand for reliable and efficient water and electricity services.

- Government initiatives to modernize aging infrastructure.

- Focus on improving energy efficiency and reducing water losses.

Dominant Segment (By End-User): The residential segment holds the largest market share, driven by rising urbanization and increasing household penetration of electricity and water connections.

Dominant Segment (By Type): Smart electricity meters are currently the dominant segment, accounting for the majority of market share; however, growth in smart gas and water meters is projected to be significant.

Regional Variations: The adoption rate of smart meters varies significantly across different regions, influenced by factors such as economic development, government policies, and infrastructure readiness.

Middle East and Africa Smart Meters Market Product Innovations

Recent innovations focus on enhanced data analytics capabilities, advanced communication protocols, and improved security features. New smart meters boast improved energy efficiency, remote monitoring, and predictive maintenance capabilities, enabling utilities to enhance operational efficiency and customer service. These innovations contribute significantly to the overall value proposition by enabling more precise billing, early detection of faults, and improved load management.

Propelling Factors for Middle East and Africa Smart Meters Market Growth

Several factors drive the growth of the Middle East and Africa smart meters market. These include:

- Government initiatives: Government policies and regulatory frameworks promoting smart grid development, energy efficiency, and water conservation are key drivers. The substantial investments made by the UAE, Saudi Arabia and others, along with their ambitious smart city initiatives, significantly influence the overall market growth.

- Technological advancements: Continuous innovation in communication technologies (e.g., NB-IoT, LoRaWAN) improves the efficiency and cost-effectiveness of smart meters, enhancing their attractiveness to utilities and end-users.

- Economic factors: Rising energy consumption and demand for reliable utility services, coupled with the need to manage resources efficiently, are leading to increased investment in smart metering infrastructure.

Obstacles in the Middle East and Africa Smart Meters Market

Despite significant growth potential, challenges remain within the Middle East and Africa smart meters market. These include:

- High initial investment costs: The significant upfront costs associated with deploying smart meters can hinder adoption, particularly in regions with limited financial resources.

- Regulatory complexities: Varying regulatory landscapes across different countries can create uncertainties and complexities for market players.

- Cybersecurity concerns: The increased reliance on interconnected smart meters raises concerns about data security and the potential for cyberattacks.

- Infrastructure limitations: In some areas, limited or outdated communication infrastructure can restrict the deployment and effectiveness of advanced smart metering systems.

Future Opportunities in Middle East and Africa Smart Meters Market

The Middle East and Africa smart meters market presents several promising future opportunities. These include:

- Expansion into underserved markets: Many countries in the region still lack extensive smart metering infrastructure, providing significant growth potential.

- Integration with renewable energy sources: Smart meters are increasingly integrated with renewable energy systems, enabling efficient management of distributed energy resources.

- Advancements in data analytics: Leveraging data generated by smart meters to improve grid management, enhance customer engagement, and optimize energy consumption offers significant opportunities.

Major Players in the Middle East and Africa Smart Meters Market Ecosystem

- Itron Inc

- Sensus (Xylem Inc)

- LANDIS+GYR Group AG

- Iskraemeco d.d.

- Diehl Metering FZE

- Kamstrup AS

- Hexing Electric Co Ltd

- Electromed (Termikel Group)

- Sagemcom SAS

- Holley Technology

Key Developments in Middle East and Africa Smart Meters Market Industry

- June 2022: The National Iranian Gas Company (NIGC) announced plans to install 26 Million smart gas meters across Iran over four years, significantly boosting the gas meter segment.

- May 2022: Dubai Electricity & Water Authority (DEWA)'s USD 1.9 Billion investment in its Smart Grid Strategy (2021-2035) demonstrates a strong commitment to expanding smart meter deployment. This builds upon previous efforts (2015-2020) replacing millions of existing meters.

- April 2022: DEWA's launch of a smart tool for assessing water and electricity consumption in Dubai homes further enhances customer engagement and promotes efficient resource management.

Strategic Middle East and Africa Smart Meters Market Forecast

The Middle East and Africa smart meters market is poised for significant growth over the forecast period (2025-2033). Government support, technological advancements, and increasing demand for efficient resource management will continue to drive adoption. The focus on smart city initiatives and renewable energy integration presents lucrative opportunities for market players. The market's future trajectory will be significantly impacted by the successful execution of large-scale smart grid projects, along with the continued adoption of smart meters across residential, commercial, and industrial sectors.

Middle East and Africa Smart Meters Market Segmentation

-

1. End User

- 1.1. Residential

- 1.2. Commercial

- 1.3. Industrial

Middle East and Africa Smart Meters Market Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle East and Africa Smart Meters Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.20% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Need For Improvement in Energy Efficiency and Smart City Investments; Supportive Government Initiatives and Regulations

- 3.3. Market Restrains

- 3.3.1. High Costs and Integration Difficulties with Smart Meters; Lack of Capital Investment for Infrastructure Installation

- 3.4. Market Trends

- 3.4.1. Commercial Sector to Hold Significant Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Middle East and Africa Smart Meters Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by End User

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.1.3. Industrial

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by End User

- 6. South Africa Middle East and Africa Smart Meters Market Analysis, Insights and Forecast, 2019-2031

- 7. Sudan Middle East and Africa Smart Meters Market Analysis, Insights and Forecast, 2019-2031

- 8. Uganda Middle East and Africa Smart Meters Market Analysis, Insights and Forecast, 2019-2031

- 9. Tanzania Middle East and Africa Smart Meters Market Analysis, Insights and Forecast, 2019-2031

- 10. Kenya Middle East and Africa Smart Meters Market Analysis, Insights and Forecast, 2019-2031

- 11. Rest of Africa Middle East and Africa Smart Meters Market Analysis, Insights and Forecast, 2019-2031

- 12. Competitive Analysis

- 12.1. Market Share Analysis 2024

- 12.2. Company Profiles

- 12.2.1 Itron Inc

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Sensus (Xylem Inc )

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 LANDIS+GYR Group AG

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Iskraemeco d d

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Diehl Metering FZE

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Kamstrup AS

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 Hexing Electric Co Ltd

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Electromed (Termikel Group)

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Sagemcom SAS*List Not Exhaustive

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Holley Technology

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.1 Itron Inc

List of Figures

- Figure 1: Middle East and Africa Smart Meters Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Middle East and Africa Smart Meters Market Share (%) by Company 2024

List of Tables

- Table 1: Middle East and Africa Smart Meters Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Middle East and Africa Smart Meters Market Revenue Million Forecast, by End User 2019 & 2032

- Table 3: Middle East and Africa Smart Meters Market Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Middle East and Africa Smart Meters Market Revenue Million Forecast, by Country 2019 & 2032

- Table 5: South Africa Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Sudan Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Uganda Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Tanzania Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Kenya Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of Africa Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Middle East and Africa Smart Meters Market Revenue Million Forecast, by End User 2019 & 2032

- Table 12: Middle East and Africa Smart Meters Market Revenue Million Forecast, by Country 2019 & 2032

- Table 13: Saudi Arabia Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: United Arab Emirates Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Israel Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Qatar Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Kuwait Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Oman Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Bahrain Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Jordan Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Lebanon Middle East and Africa Smart Meters Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East and Africa Smart Meters Market?

The projected CAGR is approximately 7.20%.

2. Which companies are prominent players in the Middle East and Africa Smart Meters Market?

Key companies in the market include Itron Inc, Sensus (Xylem Inc ), LANDIS+GYR Group AG, Iskraemeco d d, Diehl Metering FZE, Kamstrup AS, Hexing Electric Co Ltd, Electromed (Termikel Group), Sagemcom SAS*List Not Exhaustive, Holley Technology.

3. What are the main segments of the Middle East and Africa Smart Meters Market?

The market segments include End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Need For Improvement in Energy Efficiency and Smart City Investments; Supportive Government Initiatives and Regulations.

6. What are the notable trends driving market growth?

Commercial Sector to Hold Significant Share.

7. Are there any restraints impacting market growth?

High Costs and Integration Difficulties with Smart Meters; Lack of Capital Investment for Infrastructure Installation.

8. Can you provide examples of recent developments in the market?

June 2022: The National Iranian Gas Company (NIGC) intends to install 26 million smart gas meters across Iran over the next four years.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East and Africa Smart Meters Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East and Africa Smart Meters Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East and Africa Smart Meters Market?

To stay informed about further developments, trends, and reports in the Middle East and Africa Smart Meters Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence