Key Insights

The Middle East and Africa (MEA) wine market, while smaller than established markets in Europe and North America, exhibits promising growth potential. Driven by increasing disposable incomes, particularly in emerging economies, and a growing appreciation for fine dining and sophisticated lifestyles, the demand for wine is steadily rising across the region. Tourism also plays a significant role, with international travelers introducing new tastes and preferences. The segment is diversified across distribution channels, with both on-trade (restaurants, hotels) and off-trade (retail stores, supermarkets) showing substantial growth. Still wine constitutes the largest segment by type, followed by sparkling and fortified wines. While cultural and religious factors in certain MEA countries present some restraints, the increasing availability of premium wine brands and the rise of online wine retailers are counteracting these limitations. The market is competitive, with both international and local players vying for market share. Key players like E&J Gallo Winery and Constellation Brands compete with regional producers, creating a dynamic market landscape. Future growth will likely be driven by targeted marketing efforts focusing on specific demographics and the diversification of product offerings to cater to local preferences. The rise of wine tourism and educational initiatives to promote wine culture will further accelerate the market's trajectory.

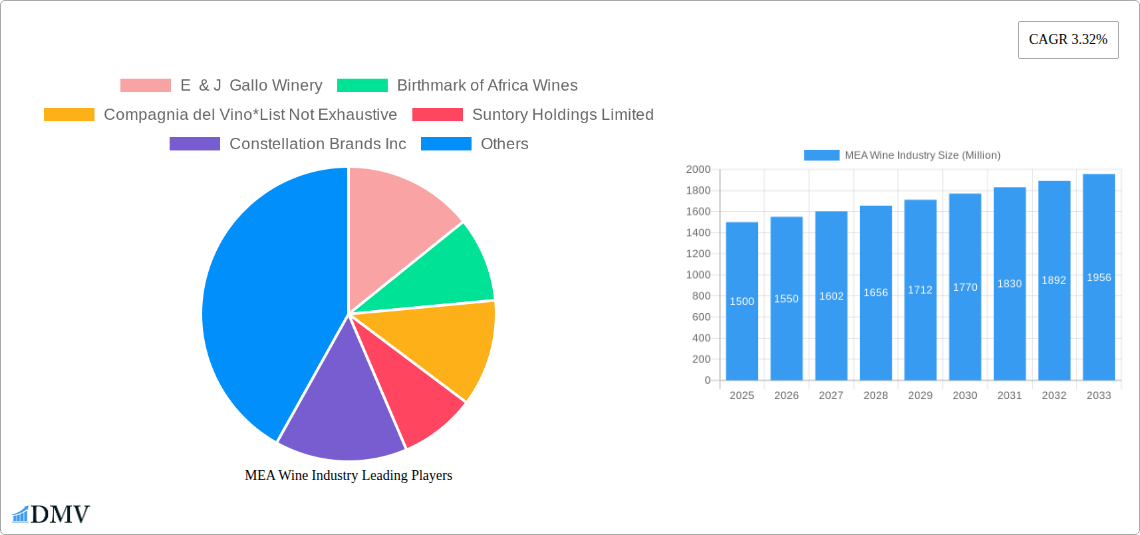

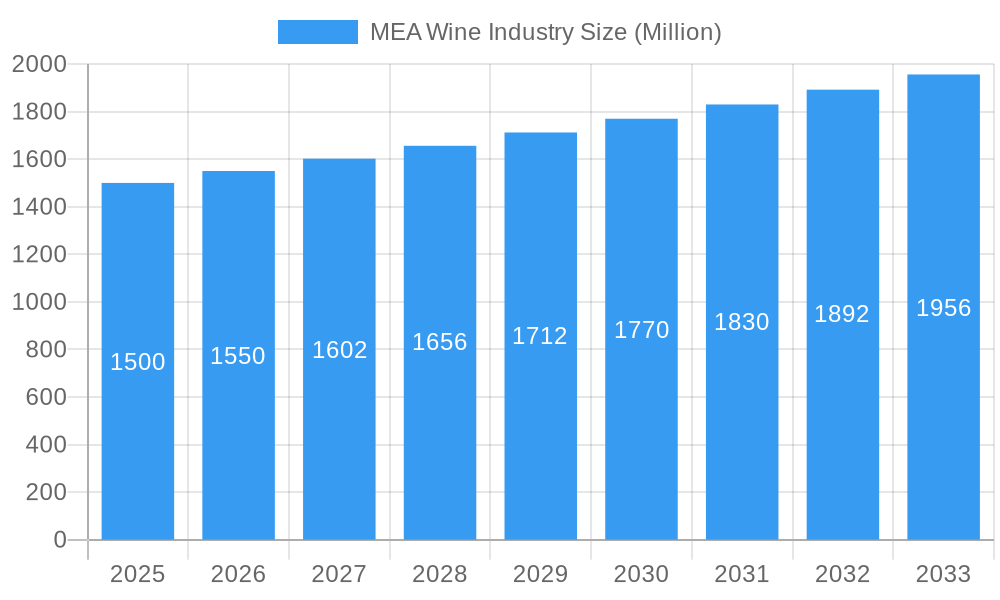

MEA Wine Industry Market Size (In Billion)

The projected Compound Annual Growth Rate (CAGR) of 3.32% suggests a steady and sustainable expansion of the MEA wine market over the forecast period (2025-2033). However, achieving this growth will require overcoming challenges including price sensitivity, import duties, and distribution infrastructure limitations in certain regions. A strategic focus on value-for-money products, efficient supply chains, and targeted marketing campaigns will be crucial for companies to succeed in this evolving market. Successful players will be those who effectively navigate the cultural nuances, regulatory landscape, and evolving consumer preferences within the diverse MEA region. The expansion of distribution networks, particularly in less penetrated markets, will unlock significant opportunities for growth. Investment in building brand awareness and educating consumers about wine varieties and consumption etiquette is critical for long-term success.

MEA Wine Industry Company Market Share

MEA Wine Industry: A Comprehensive Market Report (2019-2033)

This insightful report provides a detailed analysis of the Middle East and Africa (MEA) wine industry, offering a comprehensive overview of market trends, leading players, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and an estimated year of 2025, this report is an invaluable resource for stakeholders seeking to understand and capitalize on opportunities within this dynamic market. The forecast period covers 2025-2033, while the historical period analyzed is 2019-2024. The MEA wine market is projected to reach a value of xx Million by 2033, driven by factors such as rising disposable incomes and changing consumer preferences.

MEA Wine Industry Market Composition & Trends

This section delves into the competitive landscape of the MEA wine market, analyzing market concentration, innovation drivers, regulatory frameworks, substitute products, end-user profiles, and mergers & acquisitions (M&A) activity. The report examines the market share distribution amongst key players, including E & J Gallo Winery, Constellation Brands Inc, and Treasury Wine Estates, and analyzes the value of M&A deals within the region. The estimated market size in 2025 is xx Million.

- Market Concentration: A detailed analysis of market share held by top players, revealing the level of competition and potential for consolidation. xx% of the market is controlled by the top 5 players in 2025.

- Innovation Catalysts: Examination of factors driving innovation, such as evolving consumer tastes and technological advancements in winemaking and distribution.

- Regulatory Landscape: Assessment of the impact of regulations on market growth and investment, including import/export tariffs and alcohol licensing.

- Substitute Products: Analysis of competitive pressures from substitute beverages, such as beer, spirits, and non-alcoholic alternatives.

- End-User Profiles: Profiling of key consumer segments and their purchasing behaviors, including demographics and preferences.

- M&A Activity: Analysis of recent M&A transactions, their values (e.g., xx Million for a significant deal in 2024), and their impact on market dynamics.

MEA Wine Industry Industry Evolution

This section provides a comprehensive analysis of the MEA wine industry's evolution, exploring market growth trajectories, technological advancements, and the changing preferences of consumers. We examine data points such as growth rates and adoption metrics to provide a detailed understanding of the industry's transformation. The MEA wine market is expected to experience a CAGR of xx% during the forecast period (2025-2033).

The report traces the historical growth of the market, detailing the factors contributing to both periods of expansion and contraction. Key technological advancements, such as improved winemaking techniques and efficient distribution channels, are examined for their impact on market growth. The evolution of consumer preferences, particularly the increasing demand for premium wines and organic options, is also carefully analyzed. Specific examples of successful marketing campaigns and brand positioning strategies will be included. The shift towards e-commerce and online wine sales, along with the growth of specialized wine retailers, are discussed in detail, contributing to the overall understanding of the industry's dynamic evolution. Data on the growing popularity of specific wine types, such as sparkling and organic wines, are also provided.

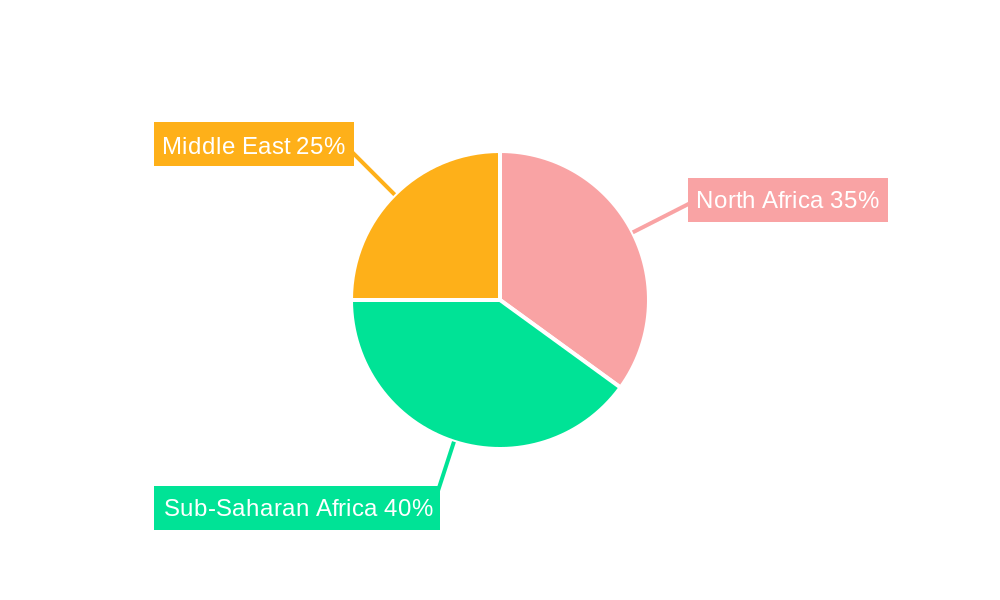

Leading Regions, Countries, or Segments in MEA Wine Industry

This section identifies the leading regions, countries, and segments within the MEA wine industry. It uses both bullet points for key drivers and paragraphs for in-depth analysis. The report will pinpoint the dominant distribution channel (on-trade vs. off-trade) and wine type (still, sparkling, dessert, fortified).

Dominant Segment: The report will identify the leading segment (e.g., still wine in South Africa, off-trade in UAE) with detailed justification.

Key Drivers for Dominance:

- Investment Trends: Analysis of investment flows into specific regions and segments.

- Regulatory Support: Examination of government policies and regulations that favor certain regions or segments.

- Consumer Preferences: Analysis of regional variations in consumer preferences that drive segment dominance.

- Infrastructure: Evaluation of the impact of logistical and transportation infrastructure on market access and distribution.

The detailed analysis will examine the factors contributing to the dominance of the identified segment, providing insights into market opportunities and potential future trends. The report will highlight the differences in growth rates between various segments, providing a comparative analysis of their performance and future potential.

MEA Wine Industry Product Innovations

This section highlights recent product innovations, their applications, and performance metrics in the MEA wine market. The report discusses unique selling propositions (USPs) and technological advancements driving product development. The rise of innovative packaging, such as eco-friendly alternatives, and the introduction of new wine blends and varietals targeting specific consumer segments will be explored.

Propelling Factors for MEA Wine Industry Growth

This section identifies key growth drivers for the MEA wine industry, including technological, economic, and regulatory influences. Specific examples will be used to illustrate these factors. Growth is being propelled by factors such as increasing disposable incomes in key markets, tourism, and the growing popularity of wine-related events and festivals. The development of efficient distribution networks and the rise of e-commerce platforms are also key drivers.

Obstacles in the MEA Wine Industry Market

This section discusses barriers and restraints impacting the MEA wine market. These include regulatory challenges, supply chain disruptions, and competitive pressures. Quantifiable impacts of these challenges on market growth will be assessed. High import tariffs and excise duties in some countries restrict market access and increase prices. The impact of climatic conditions on grape production is another significant concern. Increased competition from other alcoholic beverages and non-alcoholic alternatives also poses a challenge.

Future Opportunities in MEA Wine Industry

This section highlights emerging opportunities within the MEA wine market, including new markets, technologies, and consumer trends. The report suggests avenues for future growth, such as expanding into untapped markets, developing innovative products catering to specific consumer segments, and investing in sustainable and eco-friendly wine production methods. Focus will be on the potential for growth in specific regions, leveraging e-commerce, and catering to the rising demand for premium and organic wines.

Major Players in the MEA Wine Industry Ecosystem

- E & J Gallo Winery

- Birthmark of Africa Wines

- Compagnia del Vino

- Suntory Holdings Limited

- Constellation Brands Inc

- Treasury Wine Estates

- Accolade Wines

- The Wine Group

- Davide Campari-Milano N V

- Pernod Ricard

Key Developments in MEA Wine Industry Industry

- December 2021: Launch of new Princi wine brands (Pinal, Merlot, Cabernet Sauvignon) in Nigeria by a partnership between Nigerian pharmacists and French winemakers.

- April 2021: Birthmark of Africa Wines launches a new collection including Brut Chardonnay MCC, various red and white blends, and Premium varietals.

- April 2020: Spinneys Liquor launches a home delivery service for wine, beer, and spirits in Abu Dhabi.

Strategic MEA Wine Industry Market Forecast

The MEA wine market is poised for significant growth, driven by a confluence of factors including rising disposable incomes, expanding tourism, and a burgeoning middle class with evolving tastes. The increasing popularity of premium wines and the growing adoption of online sales channels will further fuel market expansion. Strategic investments in sustainable wine production and targeted marketing campaigns will be crucial for achieving long-term success within this dynamic market. The forecast suggests a promising future for players who adapt to changing consumer preferences and embrace innovation in product development and distribution strategies.

MEA Wine Industry Segmentation

-

1. Type

- 1.1. Still Wine

- 1.2. Sparkling Wine

- 1.3. Dessert Wine

- 1.4. Fortified Wine

-

2. Distribution Channel

- 2.1. On-Trade

-

2.2. Off-Trade

- 2.2.1. Supermarkets/Hypermarkets

- 2.2.2. Specialty Stores

- 2.2.3. Other Distribution Channels

MEA Wine Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

MEA Wine Industry Regional Market Share

Geographic Coverage of MEA Wine Industry

MEA Wine Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Still Wine

- 5.1.2. Sparkling Wine

- 5.1.3. Dessert Wine

- 5.1.4. Fortified Wine

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. On-Trade

- 5.2.2. Off-Trade

- 5.2.2.1. Supermarkets/Hypermarkets

- 5.2.2.2. Specialty Stores

- 5.2.2.3. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global MEA Wine Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Still Wine

- 6.1.2. Sparkling Wine

- 6.1.3. Dessert Wine

- 6.1.4. Fortified Wine

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. On-Trade

- 6.2.2. Off-Trade

- 6.2.2.1. Supermarkets/Hypermarkets

- 6.2.2.2. Specialty Stores

- 6.2.2.3. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Still Wine

- 7.1.2. Sparkling Wine

- 7.1.3. Dessert Wine

- 7.1.4. Fortified Wine

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. On-Trade

- 7.2.2. Off-Trade

- 7.2.2.1. Supermarkets/Hypermarkets

- 7.2.2.2. Specialty Stores

- 7.2.2.3. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Still Wine

- 8.1.2. Sparkling Wine

- 8.1.3. Dessert Wine

- 8.1.4. Fortified Wine

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. On-Trade

- 8.2.2. Off-Trade

- 8.2.2.1. Supermarkets/Hypermarkets

- 8.2.2.2. Specialty Stores

- 8.2.2.3. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Still Wine

- 9.1.2. Sparkling Wine

- 9.1.3. Dessert Wine

- 9.1.4. Fortified Wine

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. On-Trade

- 9.2.2. Off-Trade

- 9.2.2.1. Supermarkets/Hypermarkets

- 9.2.2.2. Specialty Stores

- 9.2.2.3. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Still Wine

- 10.1.2. Sparkling Wine

- 10.1.3. Dessert Wine

- 10.1.4. Fortified Wine

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. On-Trade

- 10.2.2. Off-Trade

- 10.2.2.1. Supermarkets/Hypermarkets

- 10.2.2.2. Specialty Stores

- 10.2.2.3. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Still Wine

- 11.1.2. Sparkling Wine

- 11.1.3. Dessert Wine

- 11.1.4. Fortified Wine

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. On-Trade

- 11.2.2. Off-Trade

- 11.2.2.1. Supermarkets/Hypermarkets

- 11.2.2.2. Specialty Stores

- 11.2.2.3. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 E & J Gallo Winery

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Birthmark of Africa Wines

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Compagnia del Vino*List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Suntory Holdings Limited

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Constellation Brands Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Treasury Wine Estates

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Accolade Wines

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 The Wine Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Davide Campari-Milano N V

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Pernod Ricard

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 E & J Gallo Winery

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global MEA Wine Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 5: North America MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 6: North America MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: South America MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: South America MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 11: South America MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: South America MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 17: Europe MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Europe MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East & Africa MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East & Africa MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 23: Middle East & Africa MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: Middle East & Africa MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Asia Pacific MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 29: Asia Pacific MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Asia Pacific MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Global MEA Wine Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 30: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 38: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 39: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the MEA Wine Industry?

The projected CAGR is approximately 9.1%.

2. Which companies are prominent players in the MEA Wine Industry?

Key companies in the market include E & J Gallo Winery, Birthmark of Africa Wines, Compagnia del Vino*List Not Exhaustive, Suntory Holdings Limited, Constellation Brands Inc, Treasury Wine Estates, Accolade Wines, The Wine Group, Davide Campari-Milano N V, Pernod Ricard.

3. What are the main segments of the MEA Wine Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 549.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Focus on Maintaining Health and Well-Being; Launching Supplements For Specific Purposes and Targeted Population.

6. What are the notable trends driving market growth?

Changing Lifestyle and Consumption Habits of Wine.

7. Are there any restraints impacting market growth?

Supplement Consumption and Their Side-effects; Inclination Towards Substitute Products.

8. Can you provide examples of recent developments in the market?

In December 2021, Nigerian pharmacists launched new wine brands in Nigeria. He partnered with leading wine makers in France to produce Princi wines like Princi Pinal, Princi Merlot, and Princi Cabernet Sauvignon for the Nigerian market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "MEA Wine Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the MEA Wine Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the MEA Wine Industry?

To stay informed about further developments, trends, and reports in the MEA Wine Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence