Key Insights

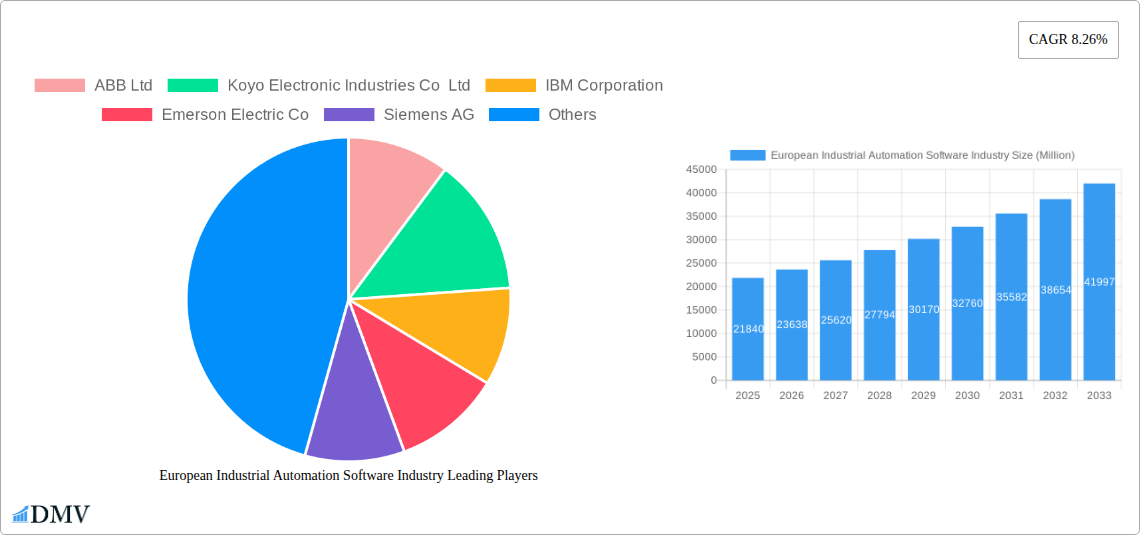

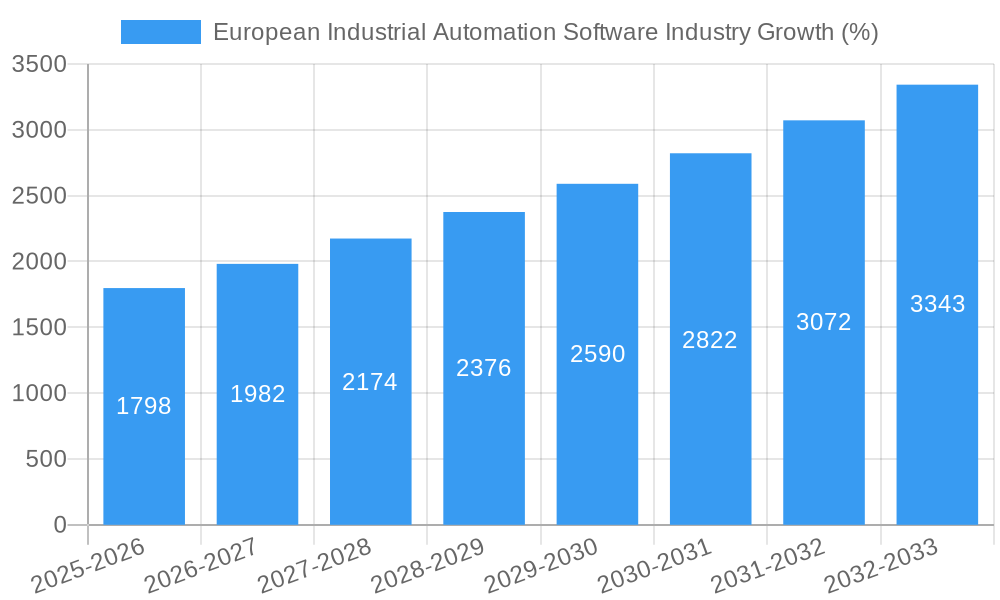

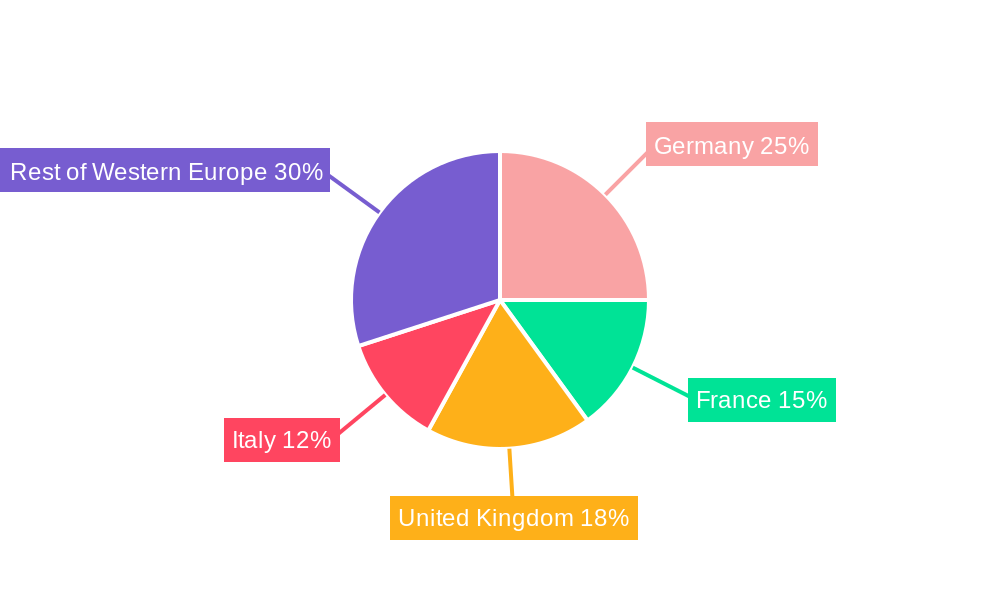

The European industrial automation software market, valued at €21.84 billion in 2025, is projected to experience robust growth, exhibiting a compound annual growth rate (CAGR) of 8.26% from 2025 to 2033. This expansion is fueled by several key drivers. The increasing adoption of Industry 4.0 principles across diverse sectors, including oil and gas, chemicals, power generation, and automotive manufacturing, necessitates advanced software solutions for optimizing processes, enhancing efficiency, and improving overall productivity. Furthermore, stringent government regulations aimed at improving safety and environmental sustainability are pushing industrial facilities to implement sophisticated automation software for compliance and improved operational control. The rising demand for predictive maintenance, enabled by Asset Performance Management (APM) and Manufacturing Execution Systems (MES) software, contributes significantly to market growth. This allows companies to reduce downtime, optimize maintenance schedules, and minimize operational disruptions. Competition is intense, with established players like ABB, Siemens, and Rockwell Automation vying for market share alongside innovative technology providers. The market is segmented by software type (MES, APM, APC, PLM, OTS, ICS) and end-user industry, with Germany, France, the UK, and Italy representing the largest national markets within Europe. The continued digital transformation within European industries ensures sustained demand for advanced industrial automation software solutions.

The market's growth trajectory is influenced by several trends. The increasing integration of Artificial Intelligence (AI) and Machine Learning (ML) into industrial automation software is enhancing capabilities in predictive analytics, anomaly detection, and autonomous decision-making. The growing emphasis on cybersecurity within industrial control systems (ICS) is driving the adoption of specialized software designed to protect critical infrastructure from cyber threats. The expansion of cloud-based industrial automation solutions is offering increased scalability, flexibility, and cost-effectiveness to businesses of all sizes. However, challenges remain, including the high initial investment costs associated with implementing advanced software solutions and the need for skilled personnel to manage and maintain these complex systems. Despite these restraints, the long-term outlook for the European industrial automation software market remains exceptionally positive, driven by ongoing technological advancements and the relentless pursuit of operational excellence across diverse industrial sectors.

European Industrial Automation Software Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the European industrial automation software market, covering the period from 2019 to 2033. It delves into market size, segmentation, key players, growth drivers, challenges, and future opportunities, offering valuable insights for stakeholders across the industry. The report utilizes data from the historical period (2019-2024), the base year (2025), and projects the market's future trajectory (2025-2033). The market is expected to reach xx Million by 2033.

European Industrial Automation Software Industry Market Composition & Trends

This section analyzes the competitive landscape, innovation drivers, regulatory environment, substitute products, end-user profiles, and merger and acquisition (M&A) activities within the European industrial automation software market. The market is characterized by a moderately concentrated landscape, with key players like ABB Ltd, Siemens AG, and Rockwell Automation Inc holding significant market share. However, numerous smaller, specialized firms also contribute significantly. The total market value in 2025 is estimated at xx Million.

Market Share Distribution (2025): ABB Ltd (xx%), Siemens AG (xx%), Rockwell Automation Inc (xx%), Others (xx%). These figures reflect an ongoing consolidation trend driven by M&A activity.

Innovation Catalysts: The demand for increased efficiency, improved safety, and data-driven decision-making are fueling innovations in areas such as AI-powered predictive maintenance, cloud-based solutions, and cybersecurity enhancements.

Regulatory Landscape: Compliance with stringent data privacy regulations (GDPR) and industrial safety standards significantly impacts the market.

Substitute Products: While specific software solutions are tailored for particular industrial needs, the availability of general-purpose software and open-source alternatives creates some competitive pressure.

End-User Profiles: The key end-user industries include Oil and Gas, Chemical and Petrochemical, Automotive and Transportation, and Power, each with unique software needs and adoption rates.

M&A Activities: Recent acquisitions, like the July 2022 acquisition of Hochrainer GmbH by Wipro PARI, illustrate the ongoing consolidation and expansion efforts within the market. The total value of M&A deals in the sector during 2019-2024 was estimated at xx Million.

European Industrial Automation Software Industry Industry Evolution

This section examines the market's growth trajectory, technological advancements, and evolving consumer demands from 2019 to 2033. The European industrial automation software market has experienced steady growth, driven by increasing digitalization across various industries. This trend is expected to continue, with a Compound Annual Growth Rate (CAGR) of xx% projected from 2025 to 2033. The adoption of cloud-based solutions, AI, and IoT technologies is accelerating, enhancing operational efficiency and enabling predictive maintenance. The rising demand for improved cybersecurity in industrial control systems is another key driver, prompting investments in advanced security solutions. Furthermore, changing consumer preferences toward more sustainable and environmentally friendly manufacturing processes are creating opportunities for automation software that enhances energy efficiency and reduces waste. The increasing complexity of industrial processes also fuels the need for sophisticated software solutions to optimize operations and improve productivity. Specific segments, like MES and APM, show particularly high growth rates due to their significant contribution to optimizing manufacturing processes and asset utilization respectively. Adoption rates for advanced technologies like AI and machine learning in industrial automation are growing rapidly, though varying across different sectors based on factors like the level of existing digital infrastructure and willingness to adopt new technologies.

Leading Regions, Countries, or Segments in European Industrial Automation Software Industry

This section identifies the dominant regions, countries, and segments within the European industrial automation software market.

Leading Regions: Germany, the United Kingdom, and France consistently lead the market due to their strong industrial base, advanced technological infrastructure, and high adoption of automation technologies. Eastern Europe, while showing slower growth than Western Europe, holds significant potential for future expansion.

Leading Countries:

- Germany: Strong automotive and manufacturing sectors drive high demand for automation software.

- United Kingdom: A robust industrial base and investments in digital transformation fuel market growth.

- France: A focus on innovation and digitalization strategies contributes to market expansion.

Leading Segments:

- Manufacturing Execution Systems (MES): High demand for improved production efficiency and traceability boosts MES adoption.

- Asset Performance Management (APM): Growing emphasis on optimizing asset utilization and reducing downtime fuels the growth of APM software.

- Industrial Control Systems Software: This sector shows robust growth driven by the need for enhanced operational reliability and improved cybersecurity.

Key Drivers:

- High levels of industrial automation investment: Significant investments by major industrial players are a key factor in the market's success.

- Government support for digital transformation: Initiatives and funding programs aimed at promoting the adoption of industrial automation technologies are accelerating market growth.

- Strong focus on enhancing operational efficiency: The constant pressure to reduce costs and improve productivity drives the adoption of automation software.

European Industrial Automation Software Industry Product Innovations

Recent product innovations focus on enhancing efficiency, security, and scalability. Advancements include AI-powered predictive maintenance algorithms that anticipate equipment failures, cloud-based platforms that enable remote monitoring and control, and integrated cybersecurity solutions that protect critical industrial infrastructure. Unique selling propositions often emphasize user-friendliness, integration capabilities, and specific industry-tailored functionality.

Propelling Factors for European Industrial Automation Software Industry Growth

Several factors contribute to the growth of the European industrial automation software market. Technological advancements, such as AI and IoT integration, are enhancing operational efficiency and enabling predictive maintenance. Government initiatives supporting digitalization and Industry 4.0 across various sectors are stimulating market growth. The increasing demand for optimized production processes and enhanced productivity among end-users fuels the adoption of advanced automation software. Furthermore, economic factors like rising labor costs and the need to improve competitiveness in the global market are pushing businesses to embrace automation solutions.

Obstacles in the European Industrial Automation Software Industry Market

The market faces challenges including the high cost of implementation for advanced solutions, integration complexities with legacy systems, cybersecurity threats, and the need for skilled personnel to operate and maintain these systems. Supply chain disruptions experienced in recent years have also posed challenges impacting the delivery of certain hardware and software components. The fragmentation of the market, with a mix of large global players and smaller niche companies, can also create challenges for standardization and integration.

Future Opportunities in European Industrial Automation Software Industry

Future opportunities lie in the expansion of AI and machine learning applications in industrial automation, the growth of cloud-based solutions, and the development of tailored solutions for emerging industries. The increasing demand for sustainable and environmentally friendly manufacturing processes creates opportunities for automation software to optimize energy efficiency and reduce waste. Furthermore, there is growing potential in expanding into less developed parts of the European market, like parts of Eastern Europe, and developing solutions for small and medium-sized enterprises (SMEs).

Major Players in the European Industrial Automation Software Industry Ecosystem

- ABB Ltd

- Koyo Electronic Industries Co Ltd

- IBM Corporation

- Emerson Electric Co

- Siemens AG

- OMRON Corporation

- Daifuku Co Ltd

- Rockwell Automation Inc

- Yokogawa Electric Corporation

- Honeywell International Inc

- List Not Exhaustive

Key Developments in European Industrial Automation Software Industry Industry

- July 2022: Wipro PARI acquired Hochrainer GmbH, expanding its European presence.

- February 2021: Liebherr Mining expanded its use of Operator Training Simulators through a partnership with ThoroughTec Simulation.

Strategic European Industrial Automation Software Industry Market Forecast

The European industrial automation software market is poised for continued growth, driven by technological innovation, increasing digitalization across various sectors, and government initiatives supporting Industry 4.0. The market's future potential is significant, with opportunities for growth across various segments, fueled by expanding adoption of advanced technologies and a growing need for efficient and sustainable manufacturing processes across diverse end-user industries. The market is expected to experience a CAGR of xx% during the forecast period (2025-2033), reaching a projected value of xx Million by 2033.

European Industrial Automation Software Industry Segmentation

-

1. Type of Software

- 1.1. Manufacturing Execution Systems (MES)

- 1.2. Asset Performance Management (APM)

- 1.3. Advanced Process Control (APC)

- 1.4. Product Lifecycle Management (PLM)

- 1.5. Operator Training Simulator (OTS)

- 1.6. Industri

-

2. End-user Industry

- 2.1. Oil and Gas

- 2.2. Chemical and Petrochemical

- 2.3. Power

- 2.4. Water and Wastewater

- 2.5. Food and Beverage

- 2.6. Automotive and Transportation

- 2.7. Other End-user Industries

European Industrial Automation Software Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

European Industrial Automation Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.26% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Launch of Stringent Energy Conservation Standards and Drive for Local Processing Across Various Geographies; Growing Need for Mass Production with Reduced Operating Costs; Adoption of Emerging Technologies such as IoT and AI in Industrial Environments

- 3.3. Market Restrains

- 3.3.1. High Maintenance and Operation Cost

- 3.4. Market Trends

- 3.4.1. Launch of Stringent Energy Conservation Standards and the Drive for Local Processing is Driving the Market in Europe

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. European Industrial Automation Software Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type of Software

- 5.1.1. Manufacturing Execution Systems (MES)

- 5.1.2. Asset Performance Management (APM)

- 5.1.3. Advanced Process Control (APC)

- 5.1.4. Product Lifecycle Management (PLM)

- 5.1.5. Operator Training Simulator (OTS)

- 5.1.6. Industri

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Oil and Gas

- 5.2.2. Chemical and Petrochemical

- 5.2.3. Power

- 5.2.4. Water and Wastewater

- 5.2.5. Food and Beverage

- 5.2.6. Automotive and Transportation

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type of Software

- 6. Germany European Industrial Automation Software Industry Analysis, Insights and Forecast, 2019-2031

- 7. France European Industrial Automation Software Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy European Industrial Automation Software Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom European Industrial Automation Software Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands European Industrial Automation Software Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden European Industrial Automation Software Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe European Industrial Automation Software Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 ABB Ltd

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Koyo Electronic Industries Co Ltd

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 IBM Corporation

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Emerson Electric Co

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Siemens AG

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 OMRON Corporation

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Daifuku Co Ltd

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Rockwell Automation Inc

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Yokogawa Electric Corporation

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Honeywell International Inc *List Not Exhaustive

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 ABB Ltd

List of Figures

- Figure 1: European Industrial Automation Software Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: European Industrial Automation Software Industry Share (%) by Company 2024

List of Tables

- Table 1: European Industrial Automation Software Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: European Industrial Automation Software Industry Revenue Million Forecast, by Type of Software 2019 & 2032

- Table 3: European Industrial Automation Software Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: European Industrial Automation Software Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: European Industrial Automation Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: European Industrial Automation Software Industry Revenue Million Forecast, by Type of Software 2019 & 2032

- Table 14: European Industrial Automation Software Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 15: European Industrial Automation Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United Kingdom European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Germany European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Spain European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Netherlands European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Belgium European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Sweden European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Norway European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Poland European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Denmark European Industrial Automation Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Industrial Automation Software Industry?

The projected CAGR is approximately 8.26%.

2. Which companies are prominent players in the European Industrial Automation Software Industry?

Key companies in the market include ABB Ltd, Koyo Electronic Industries Co Ltd, IBM Corporation, Emerson Electric Co, Siemens AG, OMRON Corporation, Daifuku Co Ltd, Rockwell Automation Inc, Yokogawa Electric Corporation, Honeywell International Inc *List Not Exhaustive.

3. What are the main segments of the European Industrial Automation Software Industry?

The market segments include Type of Software, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 21.84 Million as of 2022.

5. What are some drivers contributing to market growth?

Launch of Stringent Energy Conservation Standards and Drive for Local Processing Across Various Geographies; Growing Need for Mass Production with Reduced Operating Costs; Adoption of Emerging Technologies such as IoT and AI in Industrial Environments.

6. What are the notable trends driving market growth?

Launch of Stringent Energy Conservation Standards and the Drive for Local Processing is Driving the Market in Europe.

7. Are there any restraints impacting market growth?

High Maintenance and Operation Cost.

8. Can you provide examples of recent developments in the market?

July 2022: Wipro PARI, an industrial automation company, announced the acquisition of Freilassing-based automation technology and assembly systems supplier Hochrainer GmbH. This acquisition is expected to further help the company in expanding its presence in Europe and consolidate its global position.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Industrial Automation Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Industrial Automation Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Industrial Automation Software Industry?

To stay informed about further developments, trends, and reports in the European Industrial Automation Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence