Key Insights

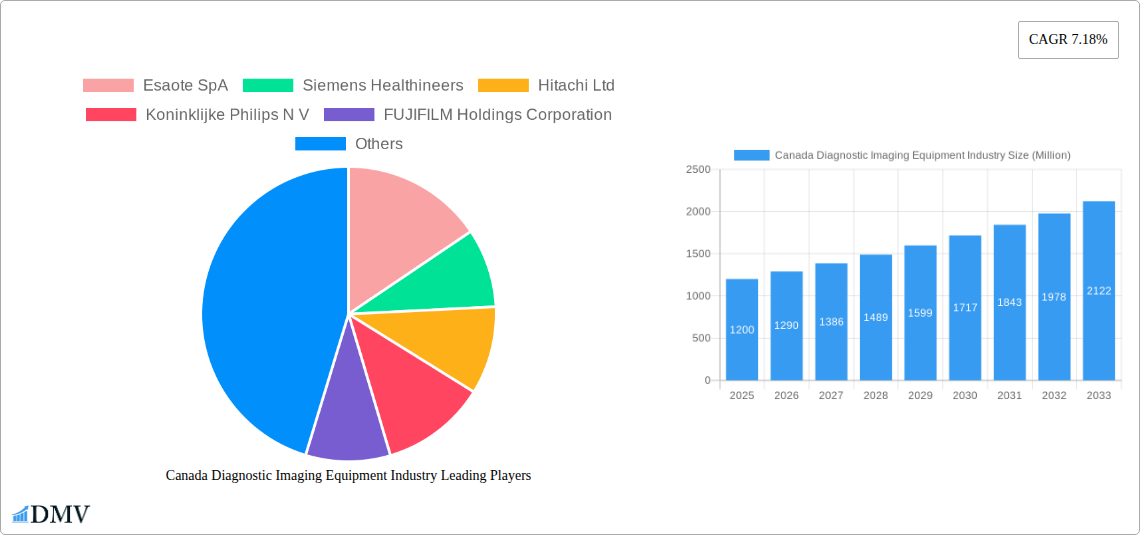

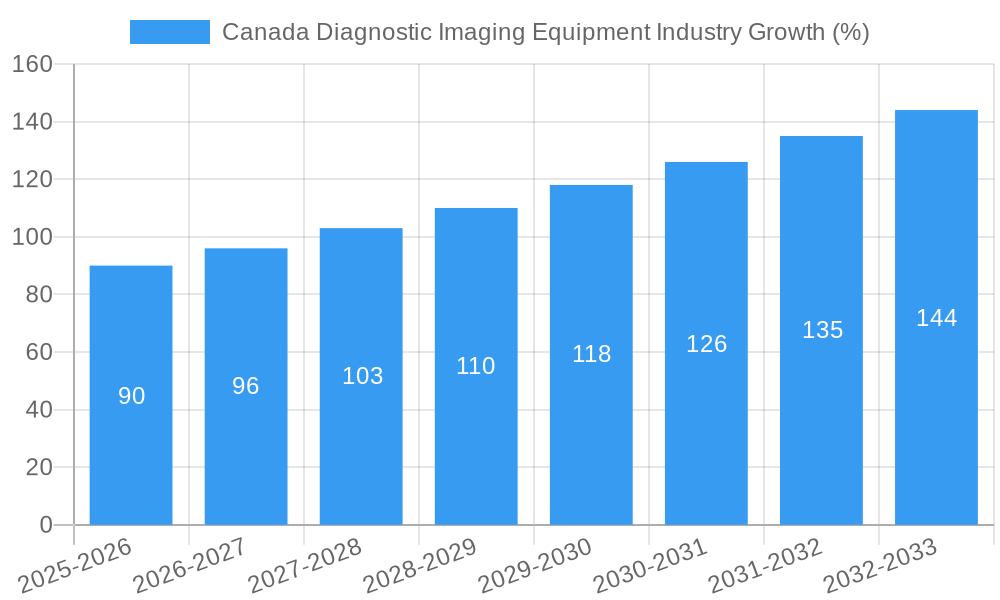

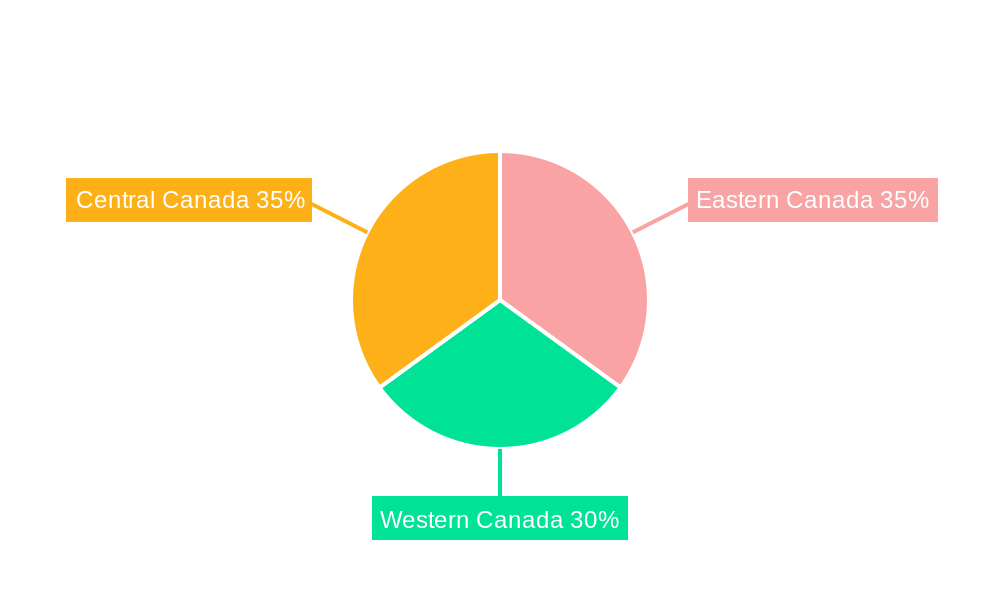

The Canadian diagnostic imaging equipment market, valued at approximately $1.2 billion CAD in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 7.18% from 2025 to 2033. This expansion is fueled by several key factors. An aging population necessitates increased diagnostic testing, driving demand for advanced imaging technologies like MRI and CT. Furthermore, rising prevalence of chronic diseases such as cardiovascular conditions and cancer necessitates more frequent and sophisticated diagnostic procedures. Technological advancements, including the development of AI-powered image analysis and minimally invasive techniques, are further enhancing the market's potential. Increased government funding for healthcare infrastructure improvements and initiatives promoting early disease detection also contribute positively. The market is segmented across various modalities (MRI, CT, Ultrasound, X-Ray, Nuclear Imaging, Fluoroscopy, Mammography), applications (Cardiology, Oncology, Neurology, Orthopedics), and end-users (Hospitals, Diagnostic Centers). While the market faces challenges such as high equipment costs and regulatory hurdles, the overall growth trajectory remains positive due to the aforementioned drivers. Competitive landscape analysis indicates a mix of established global players (Siemens Healthineers, Philips, GE Healthcare) and emerging players, fostering innovation and market penetration. Regional variations within Canada (Eastern, Western, Central) likely reflect differences in healthcare infrastructure and population density, with potentially higher growth in more populous regions.

The forecast period (2025-2033) promises substantial opportunities for market participants. Continued investment in research and development will likely lead to more sophisticated and efficient diagnostic imaging technologies. The increasing adoption of telehealth and remote diagnostics may also contribute to market growth by expanding access to imaging services in underserved areas. However, players need to address potential challenges, including managing escalating costs associated with advanced equipment and maintaining a skilled workforce capable of operating and interpreting the complex data generated by these systems. Strategic partnerships and collaborations among healthcare providers, technology developers, and regulatory bodies will be crucial for navigating these challenges and maximizing the market's growth potential.

Canada Diagnostic Imaging Equipment Industry: A Comprehensive Market Report (2019-2033)

This insightful report provides a comprehensive analysis of the Canada diagnostic imaging equipment market, offering valuable insights for stakeholders across the industry. Covering the period from 2019 to 2033, with a base year of 2025, this report meticulously examines market size, growth drivers, challenges, and future opportunities. It features detailed segmentation by modality (MRI, CT, Ultrasound, X-Ray, Nuclear Imaging, Fluoroscopy, Mammography), application (Cardiology, Oncology, Neurology, Orthopedics, Other Applications), and end-user (Hospitals, Diagnostic Centers, Others). The market is projected to reach xx Million by 2033.

Canada Diagnostic Imaging Equipment Industry Market Composition & Trends

The Canadian diagnostic imaging equipment market is characterized by a moderately concentrated landscape, with key players holding significant market share. The market share distribution is currently estimated as follows: Siemens Healthineers (xx%), GE Healthcare (xx%), Philips (xx%), and other players (xx%). Innovation is driven by advancements in AI, improved image quality, and the development of minimally invasive procedures. The regulatory landscape, primarily governed by Health Canada, plays a vital role in ensuring safety and efficacy. Substitute products are limited, with some overlap between modalities. The industry witnesses frequent mergers and acquisitions (M&A) activities, with deal values ranging from xx Million to xx Million in recent years. End-users, primarily hospitals and diagnostic centers, are increasingly focusing on cost-effectiveness, advanced technology, and streamlined workflows.

- Market Concentration: Moderately concentrated, with key players holding significant shares.

- Innovation Catalysts: AI integration, improved image quality, minimally invasive procedures.

- Regulatory Landscape: Primarily governed by Health Canada's stringent regulations.

- Substitute Products: Limited substitutes, with some overlap between modalities.

- M&A Activity: Frequent M&A activity with deal values ranging from xx Million to xx Million.

- End-User Profiles: Hospitals and diagnostic centers drive demand, prioritizing cost-effectiveness and advanced technology.

Canada Diagnostic Imaging Equipment Industry Industry Evolution

The Canadian diagnostic imaging equipment market has exhibited consistent growth over the historical period (2019-2024), driven by factors such as an aging population, rising prevalence of chronic diseases, and increasing government investments in healthcare infrastructure. The market experienced a Compound Annual Growth Rate (CAGR) of xx% during 2019-2024 and is projected to grow at a CAGR of xx% during the forecast period (2025-2033). This growth is further fueled by technological advancements, particularly in AI-powered image analysis, improved image resolution, and the introduction of portable and mobile diagnostic systems. Consumer demand is shifting towards more advanced, efficient, and user-friendly equipment. The adoption rate of advanced imaging technologies, such as MRI and CT, is steadily increasing, while the demand for traditional X-ray systems remains stable.

Leading Regions, Countries, or Segments in Canada Diagnostic Imaging Equipment Industry

The Canadian diagnostic imaging equipment market shows strong regional variations. Ontario and Quebec, being the most populous provinces, are leading consumers of advanced imaging equipment. Within modalities, MRI and CT scanners are the dominant segments, driven by their superior diagnostic capabilities. In terms of applications, Cardiology and Oncology contribute significantly to the market's growth due to the growing prevalence of cardiovascular diseases and cancer. Hospitals remain the largest end-users, followed by diagnostic centers.

- Key Drivers (Ontario & Quebec): High population density, significant healthcare investment, advanced medical infrastructure.

- Dominant Modalities: MRI and CT due to advanced diagnostic capabilities.

- Leading Applications: Cardiology and Oncology due to high prevalence of related diseases.

- Largest End-Users: Hospitals, followed by Diagnostic Centers.

Canada Diagnostic Imaging Equipment Industry Product Innovations

Recent product innovations focus on enhancing image quality, reducing radiation exposure, and improving workflow efficiency. AI-powered image analysis tools are becoming increasingly integrated into diagnostic equipment, enabling faster and more accurate diagnoses. The development of portable and mobile systems has expanded access to advanced imaging technologies in remote areas. These innovations translate into faster diagnosis, enhanced accuracy, and improved patient outcomes.

Propelling Factors for Canada Diagnostic Imaging Equipment Industry Growth

Technological advancements such as AI-powered diagnostics, improved image resolution, and portable systems are major drivers. Government funding and healthcare infrastructure development also contribute substantially. Rising prevalence of chronic diseases and an aging population create increased demand. Regulatory support for innovative technologies further accelerates growth.

Obstacles in the Canada Diagnostic Imaging Equipment Industry Market

High costs associated with purchasing and maintaining advanced equipment represent a significant barrier. Supply chain disruptions can cause delays and impact equipment availability. Intense competition among established and emerging players creates pricing pressure. Stringent regulatory requirements add to the complexity of market entry.

Future Opportunities in Canada Diagnostic Imaging Equipment Industry

Expansion into rural and remote areas through mobile imaging systems creates significant growth potential. The increasing integration of AI and machine learning presents new opportunities for improved diagnostic capabilities. Focus on personalized medicine and preventive care will drive demand for advanced imaging solutions.

Major Players in the Canada Diagnostic Imaging Equipment Industry Ecosystem

- Esaote SpA

- Siemens Healthineers

- Hitachi Ltd

- Koninklijke Philips N V

- FUJIFILM Holdings Corporation

- Mindray Medical International Limited

- Carestream Health

- General Electric Company (GE Healthcare)

- Canon Medical Systems Corporation

- Hologic Corporation

Key Developments in Canada Diagnostic Imaging Equipment Industry Industry

- April 2022: KA Imaging invested USD 1.5 Million to develop a dual-energy mobile X-ray system.

- March 2022: NovaSignal Corp.'s NovaGuide Intelligent Ultrasound received a Medical Device Licence from Health Canada.

Strategic Canada Diagnostic Imaging Equipment Industry Market Forecast

The Canadian diagnostic imaging equipment market is poised for sustained growth, driven by technological advancements, increasing healthcare spending, and the rising prevalence of chronic diseases. The market's potential is significant, with opportunities in new technologies like AI-powered diagnostics and expanding access to advanced imaging in underserved areas. The forecast period will witness continued adoption of advanced imaging modalities and a focus on improved efficiency and cost-effectiveness.

Canada Diagnostic Imaging Equipment Industry Segmentation

-

1. Modality

- 1.1. MRI

- 1.2. Computed Tomography

- 1.3. Ultrasound

- 1.4. X-Ray

- 1.5. Nuclear Imaging

- 1.6. Fluoroscopy

- 1.7. Mamography

-

2. Application

- 2.1. Cardiology

- 2.2. Oncology

- 2.3. Neurology

- 2.4. Orthopedics

- 2.5. Other Applications

-

3. End-user

- 3.1. Hospital

- 3.2. Diagnostic Centers

- 3.3. Others

Canada Diagnostic Imaging Equipment Industry Segmentation By Geography

- 1. Canada

Canada Diagnostic Imaging Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.18% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rise in the Prevalence of Chronic Diseases; Increasing Geriatric population; Increased Adoption of Advanced Technologies in Medical Imaging

- 3.3. Market Restrains

- 3.3.1. Expensive Procedures and Equipment

- 3.4. Market Trends

- 3.4.1. MRI is Expected to be Largest Growing Segment in the Canada Diagnostic Imaging Equipment Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Diagnostic Imaging Equipment Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Modality

- 5.1.1. MRI

- 5.1.2. Computed Tomography

- 5.1.3. Ultrasound

- 5.1.4. X-Ray

- 5.1.5. Nuclear Imaging

- 5.1.6. Fluoroscopy

- 5.1.7. Mamography

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Cardiology

- 5.2.2. Oncology

- 5.2.3. Neurology

- 5.2.4. Orthopedics

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End-user

- 5.3.1. Hospital

- 5.3.2. Diagnostic Centers

- 5.3.3. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Modality

- 6. Eastern Canada Canada Diagnostic Imaging Equipment Industry Analysis, Insights and Forecast, 2019-2031

- 7. Western Canada Canada Diagnostic Imaging Equipment Industry Analysis, Insights and Forecast, 2019-2031

- 8. Central Canada Canada Diagnostic Imaging Equipment Industry Analysis, Insights and Forecast, 2019-2031

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 Esaote SpA

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 Siemens Healthineers

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 Hitachi Ltd

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 Koninklijke Philips N V

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 FUJIFILM Holdings Corporation

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 Mindray Medical International Limited*List Not Exhaustive

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 Carestream Health

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 General Electric Company (GE Healthcare)

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 Canon Medical Systems Corporation

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.10 Hologic Corporation

- 9.2.10.1. Overview

- 9.2.10.2. Products

- 9.2.10.3. SWOT Analysis

- 9.2.10.4. Recent Developments

- 9.2.10.5. Financials (Based on Availability)

- 9.2.1 Esaote SpA

List of Figures

- Figure 1: Canada Diagnostic Imaging Equipment Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Canada Diagnostic Imaging Equipment Industry Share (%) by Company 2024

List of Tables

- Table 1: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Modality 2019 & 2032

- Table 3: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by End-user 2019 & 2032

- Table 5: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Eastern Canada Canada Diagnostic Imaging Equipment Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Western Canada Canada Diagnostic Imaging Equipment Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Central Canada Canada Diagnostic Imaging Equipment Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Modality 2019 & 2032

- Table 11: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 12: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by End-user 2019 & 2032

- Table 13: Canada Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Diagnostic Imaging Equipment Industry?

The projected CAGR is approximately 7.18%.

2. Which companies are prominent players in the Canada Diagnostic Imaging Equipment Industry?

Key companies in the market include Esaote SpA, Siemens Healthineers, Hitachi Ltd, Koninklijke Philips N V, FUJIFILM Holdings Corporation, Mindray Medical International Limited*List Not Exhaustive, Carestream Health, General Electric Company (GE Healthcare), Canon Medical Systems Corporation, Hologic Corporation.

3. What are the main segments of the Canada Diagnostic Imaging Equipment Industry?

The market segments include Modality, Application, End-user.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in the Prevalence of Chronic Diseases; Increasing Geriatric population; Increased Adoption of Advanced Technologies in Medical Imaging.

6. What are the notable trends driving market growth?

MRI is Expected to be Largest Growing Segment in the Canada Diagnostic Imaging Equipment Market.

7. Are there any restraints impacting market growth?

Expensive Procedures and Equipment.

8. Can you provide examples of recent developments in the market?

In April 2022, KA Imaging in Canada invested USD 1.5 million to develop a dual-energy mobile X-ray system.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Diagnostic Imaging Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Diagnostic Imaging Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Diagnostic Imaging Equipment Industry?

To stay informed about further developments, trends, and reports in the Canada Diagnostic Imaging Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence