Key Insights

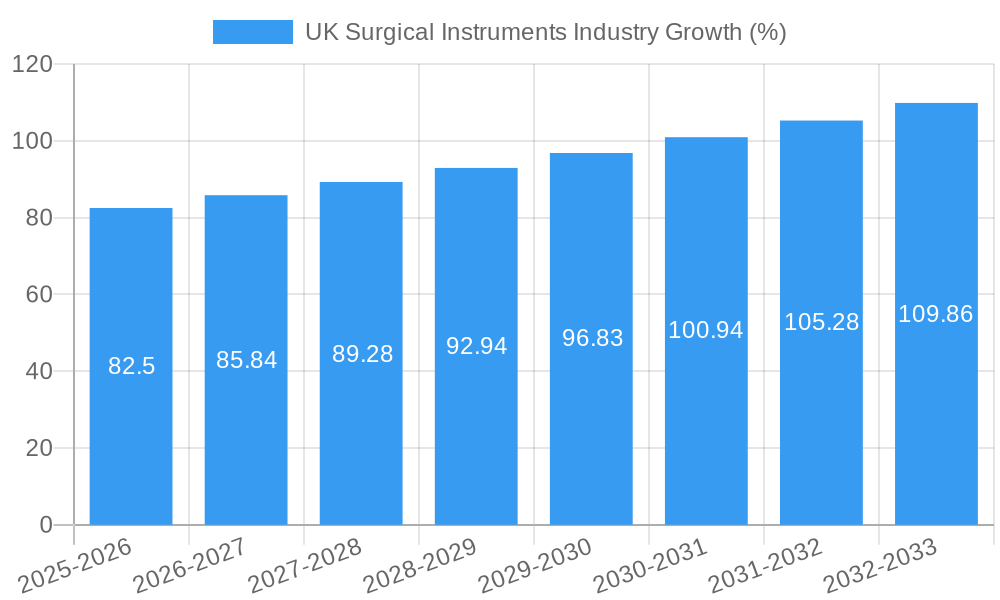

The UK surgical instruments market, valued at approximately £X million in 2025 (assuming a market size similar to other developed nations, given the missing data), is projected to experience robust growth, driven by a 5.5% CAGR through 2033. This expansion is fueled by several key factors. The aging population in the UK necessitates increased surgical procedures, particularly in cardiology, orthopedics, and neurology, thereby boosting demand for a wide array of surgical instruments. Furthermore, advancements in minimally invasive surgical techniques, such as laparoscopy, are driving adoption of sophisticated instruments like laparoscopic devices and trocars, contributing to market expansion. Technological innovations, including the development of more precise and ergonomic handheld devices and improved electro-surgical instruments, are also playing a crucial role in this market growth. The increasing prevalence of chronic diseases further adds to the demand for surgical interventions, solidifying the market's growth trajectory.

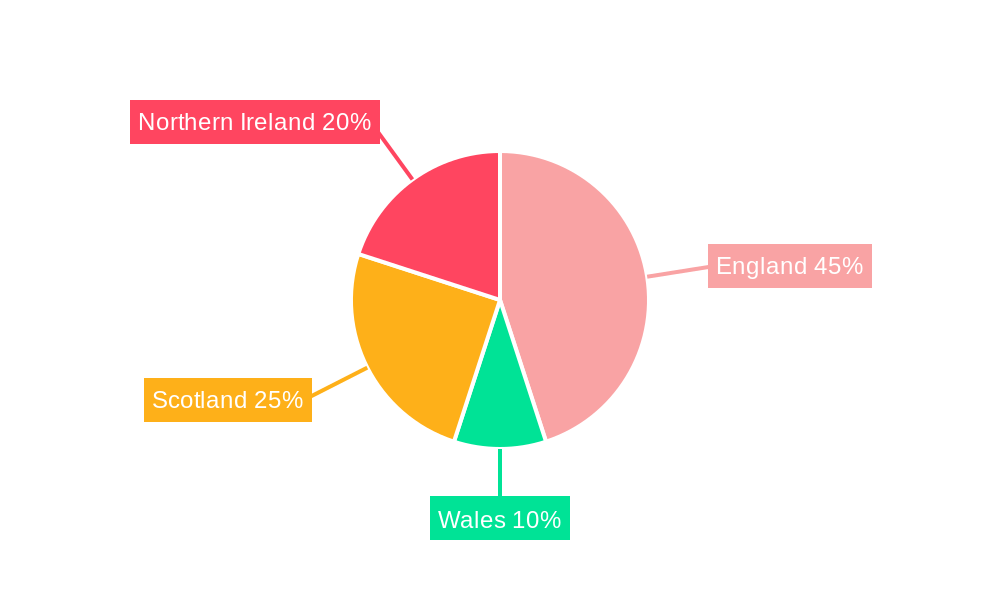

However, certain market restraints exist. Stringent regulatory approvals for new medical devices can cause delays in market entry and limit the availability of cutting-edge technology. Furthermore, pricing pressures from healthcare providers and the rising cost of advanced surgical instruments can potentially affect market growth. The competitive landscape, dominated by major players like Smith & Nephew, Stryker, and Johnson & Johnson, necessitates continuous innovation and strategic partnerships to maintain a strong market position. Despite these challenges, the substantial demand fueled by an aging population and technological advancements ensures a positive outlook for the UK surgical instruments market throughout the forecast period. Segmentation by application (Gynecology and Urology, Cardiology, Orthopaedic, Neurology, Other Applications) and end-user (Hospitals, Ambulatory Surgical Centers, Other End-Users) offers further insight into the dynamic market structure and specific growth opportunities within each niche. The market's regional division (England, Wales, Scotland, Northern Ireland) also reflects variations in demand across regions.

UK Surgical Instruments Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the UK surgical instruments market, offering invaluable insights for stakeholders across the industry value chain. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report delivers a clear picture of past performance, current market dynamics, and future growth potential. The market is valued at £XX Million in 2025 and is projected to reach £XX Million by 2033, exhibiting a robust CAGR. This report covers key segments including By Application (Gynecology and Urology, Cardiology, Orthopaedic, Neurology, Other Applications), By End-User (Hospitals, Ambulatory Surgical Centers, Other End-Users), and By Product (Handheld Devices, Laproscopic Devices, Electro Surgical Devices, Wound Closure Devices, Trocars and Access Devices, Other Products).

UK Surgical Instruments Industry Market Composition & Trends

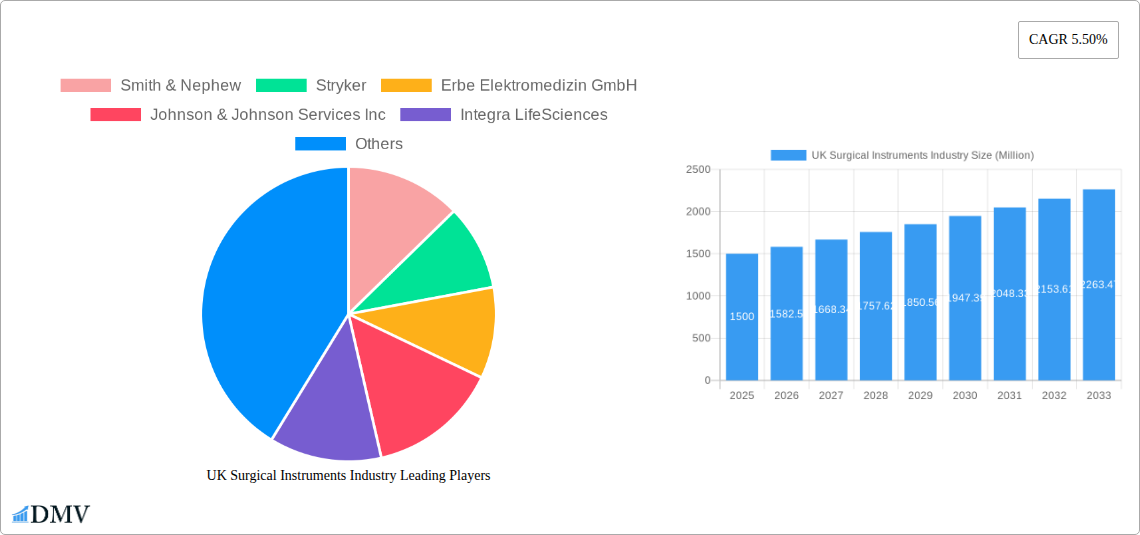

The UK surgical instruments market is characterized by a moderately concentrated landscape, with key players like Smith & Nephew, Stryker, Erbe Elektromedizin GmbH, Johnson & Johnson Services Inc, Integra LifeSciences, Getinge AB, Boston Scientific Corporation, B Braun SE, Olympus Corporation, and Medtronic plc holding significant market share. Market share distribution varies across segments, with orthopaedic and laparoscopic devices currently dominating. Innovation is driven by advancements in minimally invasive surgery (MIS), robotic surgery, and advanced materials. Stringent regulatory frameworks, including those set by the MHRA (Medicines and Healthcare products Regulatory Agency), significantly influence market operations. Substitute products, such as less invasive procedures, exert some competitive pressure. The market has witnessed several M&A activities in recent years, with deal values ranging from £XX Million to £XX Million, reflecting consolidation trends within the sector.

- Market Concentration: Moderately concentrated, with top 10 players accounting for approximately XX% of market share.

- Innovation Catalysts: Advancements in MIS, robotic surgery, and materials science.

- Regulatory Landscape: Stringent MHRA regulations shaping market access and product development.

- Substitute Products: Competition from less invasive procedures.

- M&A Activity: Consolidation through mergers and acquisitions, with deals valued at £XX Million - £XX Million in recent years.

- End-User Profile: Dominated by hospitals, followed by ambulatory surgical centers.

UK Surgical Instruments Industry Industry Evolution

The UK surgical instruments market has experienced steady growth over the historical period (2019-2024), driven by factors such as the increasing prevalence of chronic diseases, an aging population, technological advancements leading to improved surgical outcomes, and rising healthcare expenditure. The market has witnessed a shift towards minimally invasive surgical procedures, fueled by the adoption of advanced technologies like laparoscopic and robotic surgery. This trend has positively impacted the demand for specialized surgical instruments designed for MIS. The market has also seen an increased focus on patient safety and improved surgical outcomes, which has led to the development of innovative surgical instruments with enhanced features. Technological advancements have been a key driver, with the development of advanced materials, improved ergonomics, and integrated technologies increasing instrument efficacy and longevity. Shifting consumer demands towards minimally invasive procedures, quicker recovery times and less pain has propelled growth. The market is expected to continue this growth trajectory into the forecast period (2025-2033), with an estimated annual growth rate of XX%.

Leading Regions, Countries, or Segments in UK Surgical Instruments Industry

Within the UK surgical instruments market, the orthopaedic segment currently holds the largest market share, driven by the increasing prevalence of osteoarthritis and other musculoskeletal disorders. The hospital end-user segment also dominates due to the concentration of surgical procedures within these facilities. London and other major urban centers are key regional markets due to higher concentrations of hospitals and surgical centers.

Key Drivers for Orthopaedic Segment Dominance:

- High incidence of osteoarthritis and other musculoskeletal conditions.

- Significant investments in orthopedic surgery facilities.

- Technological advancements in orthopedic implants and instruments.

Key Drivers for Hospital Segment Dominance:

- Concentration of surgical procedures within hospitals.

- Extensive surgical infrastructure and expertise.

- Increased funding for hospital infrastructure and equipment upgrades.

Other significant segments: The laparoscopic devices segment is also exhibiting high growth due to its advantages in minimally invasive surgery.

UK Surgical Instruments Industry Product Innovations

Recent innovations in surgical instruments include the development of smart instruments with integrated sensors for real-time data collection, improved ergonomics for enhanced surgeon comfort and precision, and the use of biocompatible materials for reduced inflammation and faster healing. These advancements are improving the efficiency and effectiveness of surgical procedures and reducing patient recovery time. The integration of robotics and AI into surgical instruments offers further potential for improved precision, less invasiveness, and enhanced surgical outcomes.

Propelling Factors for UK Surgical Instruments Industry Growth

Several factors contribute to the growth of the UK surgical instruments market. Technological advancements in minimally invasive surgery (MIS) techniques and robotic-assisted surgery have increased demand for specialized instruments. The rising prevalence of chronic diseases necessitating surgical intervention fuels market growth. Government initiatives supporting healthcare infrastructure development and technological upgrades contribute to market expansion. Increased investment in research and development across the medical device industry is also a key factor.

Obstacles in the UK Surgical Instruments Industry Market

Challenges include stringent regulatory hurdles for new product approvals, potential supply chain disruptions impacting raw material availability and manufacturing timelines, and significant competitive pressures from both domestic and international players. The price sensitivity of healthcare providers can also restrict market expansion. These factors can have quantifiable impacts on market growth, potentially delaying new product launches or increasing costs.

Future Opportunities in UK Surgical Instruments Industry

Emerging opportunities lie in the increasing adoption of robotic surgery, personalized medicine, and 3D-printed surgical instruments. The growth of ambulatory surgical centers presents an expanding market segment. Focus on the development of single-use instruments and reusable, sustainable products in response to environmental concerns represents a growing market segment.

Major Players in the UK Surgical Instruments Industry Ecosystem

- Smith & Nephew

- Stryker

- Erbe Elektromedizin GmbH

- Johnson & Johnson Services Inc

- Integra LifeSciences

- Getinge AB

- Boston Scientific Corporation

- B Braun SE

- Olympus Corporation

- Medtronic plc

Key Developments in UK Surgical Instruments Industry Industry

- June 2022: Advanced Medical Solutions received FDA 510(k) approval for LiquiBand XL, expanding its wound closure device portfolio and potentially boosting market share in orthopedic procedures.

- March 2022: Surgical Innovations Group plc launched the YelloPort Elite 5mm surgical Port Access System, collaborating with CMR Surgical to leverage advancements in minimally invasive robotic surgery and enhancing their product offerings in this growing segment.

Strategic UK Surgical Instruments Industry Market Forecast

The UK surgical instruments market is poised for continued growth driven by technological advancements, increasing prevalence of chronic diseases, and rising healthcare spending. The market will see further innovation in minimally invasive procedures, smart instruments, and robotic surgery. The focus on improved patient outcomes, cost-effectiveness and sustainability will shape future growth. The market presents lucrative opportunities for both established players and emerging companies, promising a robust and dynamic industry landscape.

UK Surgical Instruments Industry Segmentation

-

1. Product

- 1.1. Handheld Devices

- 1.2. Laproscopic Devices

- 1.3. Electro-surgical Devices

- 1.4. Wound Closure Devices

- 1.5. Trocars and Access Devices

- 1.6. Other Products

-

2. Application

- 2.1. Gynecology and Urology

- 2.2. Cardiology

- 2.3. Orthopaedic

- 2.4. Neurology

- 2.5. Other Applications

-

3. End User

- 3.1. Hospitals

- 3.2. Ambulatory Surgical Centers

- 3.3. Other End Users

UK Surgical Instruments Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

UK Surgical Instruments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Minimally Invasive Devices; Increasing Prevalence of Chronic Diseases and Accidents

- 3.3. Market Restrains

- 3.3.1. Stringent Government Regulations

- 3.4. Market Trends

- 3.4.1. Handheld Devices are Expected to Witness a Growth in the the General Surgical Devices Market During the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Handheld Devices

- 5.1.2. Laproscopic Devices

- 5.1.3. Electro-surgical Devices

- 5.1.4. Wound Closure Devices

- 5.1.5. Trocars and Access Devices

- 5.1.6. Other Products

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Gynecology and Urology

- 5.2.2. Cardiology

- 5.2.3. Orthopaedic

- 5.2.4. Neurology

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospitals

- 5.3.2. Ambulatory Surgical Centers

- 5.3.3. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North America UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Handheld Devices

- 6.1.2. Laproscopic Devices

- 6.1.3. Electro-surgical Devices

- 6.1.4. Wound Closure Devices

- 6.1.5. Trocars and Access Devices

- 6.1.6. Other Products

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Gynecology and Urology

- 6.2.2. Cardiology

- 6.2.3. Orthopaedic

- 6.2.4. Neurology

- 6.2.5. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Hospitals

- 6.3.2. Ambulatory Surgical Centers

- 6.3.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. South America UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Handheld Devices

- 7.1.2. Laproscopic Devices

- 7.1.3. Electro-surgical Devices

- 7.1.4. Wound Closure Devices

- 7.1.5. Trocars and Access Devices

- 7.1.6. Other Products

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Gynecology and Urology

- 7.2.2. Cardiology

- 7.2.3. Orthopaedic

- 7.2.4. Neurology

- 7.2.5. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Hospitals

- 7.3.2. Ambulatory Surgical Centers

- 7.3.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Europe UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Handheld Devices

- 8.1.2. Laproscopic Devices

- 8.1.3. Electro-surgical Devices

- 8.1.4. Wound Closure Devices

- 8.1.5. Trocars and Access Devices

- 8.1.6. Other Products

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Gynecology and Urology

- 8.2.2. Cardiology

- 8.2.3. Orthopaedic

- 8.2.4. Neurology

- 8.2.5. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Hospitals

- 8.3.2. Ambulatory Surgical Centers

- 8.3.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Middle East & Africa UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Handheld Devices

- 9.1.2. Laproscopic Devices

- 9.1.3. Electro-surgical Devices

- 9.1.4. Wound Closure Devices

- 9.1.5. Trocars and Access Devices

- 9.1.6. Other Products

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Gynecology and Urology

- 9.2.2. Cardiology

- 9.2.3. Orthopaedic

- 9.2.4. Neurology

- 9.2.5. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Hospitals

- 9.3.2. Ambulatory Surgical Centers

- 9.3.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Asia Pacific UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Handheld Devices

- 10.1.2. Laproscopic Devices

- 10.1.3. Electro-surgical Devices

- 10.1.4. Wound Closure Devices

- 10.1.5. Trocars and Access Devices

- 10.1.6. Other Products

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Gynecology and Urology

- 10.2.2. Cardiology

- 10.2.3. Orthopaedic

- 10.2.4. Neurology

- 10.2.5. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Hospitals

- 10.3.2. Ambulatory Surgical Centers

- 10.3.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. England UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 12. Wales UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 13. Scotland UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 14. Northern UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 15. Ireland UK Surgical Instruments Industry Analysis, Insights and Forecast, 2019-2031

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Smith & Nephew

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Stryker

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Erbe Elektromedizin GmbH

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Johnson & Johnson Services Inc

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Integra LifeSciences

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Getinge AB*List Not Exhaustive

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Boston Scientific Corporation

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 B Braun SE

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Olympus Corporation

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Medtronic plc

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Smith & Nephew

List of Figures

- Figure 1: Global UK Surgical Instruments Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: United kingdom Region UK Surgical Instruments Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: United kingdom Region UK Surgical Instruments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: North America UK Surgical Instruments Industry Revenue (Million), by Product 2024 & 2032

- Figure 5: North America UK Surgical Instruments Industry Revenue Share (%), by Product 2024 & 2032

- Figure 6: North America UK Surgical Instruments Industry Revenue (Million), by Application 2024 & 2032

- Figure 7: North America UK Surgical Instruments Industry Revenue Share (%), by Application 2024 & 2032

- Figure 8: North America UK Surgical Instruments Industry Revenue (Million), by End User 2024 & 2032

- Figure 9: North America UK Surgical Instruments Industry Revenue Share (%), by End User 2024 & 2032

- Figure 10: North America UK Surgical Instruments Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: North America UK Surgical Instruments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: South America UK Surgical Instruments Industry Revenue (Million), by Product 2024 & 2032

- Figure 13: South America UK Surgical Instruments Industry Revenue Share (%), by Product 2024 & 2032

- Figure 14: South America UK Surgical Instruments Industry Revenue (Million), by Application 2024 & 2032

- Figure 15: South America UK Surgical Instruments Industry Revenue Share (%), by Application 2024 & 2032

- Figure 16: South America UK Surgical Instruments Industry Revenue (Million), by End User 2024 & 2032

- Figure 17: South America UK Surgical Instruments Industry Revenue Share (%), by End User 2024 & 2032

- Figure 18: South America UK Surgical Instruments Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: South America UK Surgical Instruments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Europe UK Surgical Instruments Industry Revenue (Million), by Product 2024 & 2032

- Figure 21: Europe UK Surgical Instruments Industry Revenue Share (%), by Product 2024 & 2032

- Figure 22: Europe UK Surgical Instruments Industry Revenue (Million), by Application 2024 & 2032

- Figure 23: Europe UK Surgical Instruments Industry Revenue Share (%), by Application 2024 & 2032

- Figure 24: Europe UK Surgical Instruments Industry Revenue (Million), by End User 2024 & 2032

- Figure 25: Europe UK Surgical Instruments Industry Revenue Share (%), by End User 2024 & 2032

- Figure 26: Europe UK Surgical Instruments Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Europe UK Surgical Instruments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: Middle East & Africa UK Surgical Instruments Industry Revenue (Million), by Product 2024 & 2032

- Figure 29: Middle East & Africa UK Surgical Instruments Industry Revenue Share (%), by Product 2024 & 2032

- Figure 30: Middle East & Africa UK Surgical Instruments Industry Revenue (Million), by Application 2024 & 2032

- Figure 31: Middle East & Africa UK Surgical Instruments Industry Revenue Share (%), by Application 2024 & 2032

- Figure 32: Middle East & Africa UK Surgical Instruments Industry Revenue (Million), by End User 2024 & 2032

- Figure 33: Middle East & Africa UK Surgical Instruments Industry Revenue Share (%), by End User 2024 & 2032

- Figure 34: Middle East & Africa UK Surgical Instruments Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Middle East & Africa UK Surgical Instruments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Asia Pacific UK Surgical Instruments Industry Revenue (Million), by Product 2024 & 2032

- Figure 37: Asia Pacific UK Surgical Instruments Industry Revenue Share (%), by Product 2024 & 2032

- Figure 38: Asia Pacific UK Surgical Instruments Industry Revenue (Million), by Application 2024 & 2032

- Figure 39: Asia Pacific UK Surgical Instruments Industry Revenue Share (%), by Application 2024 & 2032

- Figure 40: Asia Pacific UK Surgical Instruments Industry Revenue (Million), by End User 2024 & 2032

- Figure 41: Asia Pacific UK Surgical Instruments Industry Revenue Share (%), by End User 2024 & 2032

- Figure 42: Asia Pacific UK Surgical Instruments Industry Revenue (Million), by Country 2024 & 2032

- Figure 43: Asia Pacific UK Surgical Instruments Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global UK Surgical Instruments Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global UK Surgical Instruments Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 3: Global UK Surgical Instruments Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Global UK Surgical Instruments Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 5: Global UK Surgical Instruments Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global UK Surgical Instruments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: England UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Wales UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Scotland UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Northern UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Ireland UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global UK Surgical Instruments Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 13: Global UK Surgical Instruments Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 14: Global UK Surgical Instruments Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 15: Global UK Surgical Instruments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United States UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Canada UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Mexico UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Global UK Surgical Instruments Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 20: Global UK Surgical Instruments Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 21: Global UK Surgical Instruments Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 22: Global UK Surgical Instruments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 23: Brazil UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Argentina UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Rest of South America UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Global UK Surgical Instruments Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 27: Global UK Surgical Instruments Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 28: Global UK Surgical Instruments Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 29: Global UK Surgical Instruments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: United Kingdom UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Germany UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: France UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Italy UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Spain UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Russia UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Benelux UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Nordics UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Rest of Europe UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Global UK Surgical Instruments Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 40: Global UK Surgical Instruments Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 41: Global UK Surgical Instruments Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 42: Global UK Surgical Instruments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 43: Turkey UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Israel UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: GCC UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: North Africa UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: South Africa UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Rest of Middle East & Africa UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: Global UK Surgical Instruments Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 50: Global UK Surgical Instruments Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 51: Global UK Surgical Instruments Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 52: Global UK Surgical Instruments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 53: China UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: India UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Japan UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: South Korea UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 57: ASEAN UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 58: Oceania UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: Rest of Asia Pacific UK Surgical Instruments Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Surgical Instruments Industry?

The projected CAGR is approximately 5.50%.

2. Which companies are prominent players in the UK Surgical Instruments Industry?

Key companies in the market include Smith & Nephew, Stryker, Erbe Elektromedizin GmbH, Johnson & Johnson Services Inc, Integra LifeSciences, Getinge AB*List Not Exhaustive, Boston Scientific Corporation, B Braun SE, Olympus Corporation, Medtronic plc.

3. What are the main segments of the UK Surgical Instruments Industry?

The market segments include Product, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Minimally Invasive Devices; Increasing Prevalence of Chronic Diseases and Accidents.

6. What are the notable trends driving market growth?

Handheld Devices are Expected to Witness a Growth in the the General Surgical Devices Market During the Forecast Period.

7. Are there any restraints impacting market growth?

Stringent Government Regulations.

8. Can you provide examples of recent developments in the market?

June 2022: Advanced Medical Solutions, a specialist in tissue-healing technologies, received FDA 510(k) approval for LiquiBand XL, a new device that can close longer wounds than existing LiquiBand products. Since its European approval in 2021, the device has been used in a variety of orthopedic procedures in many different countries. It has also received very positive feedback regarding ease of use, effectiveness, and reduced pain and scarring when compared to other closure methods like stapling.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Surgical Instruments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Surgical Instruments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Surgical Instruments Industry?

To stay informed about further developments, trends, and reports in the UK Surgical Instruments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence