Key Insights

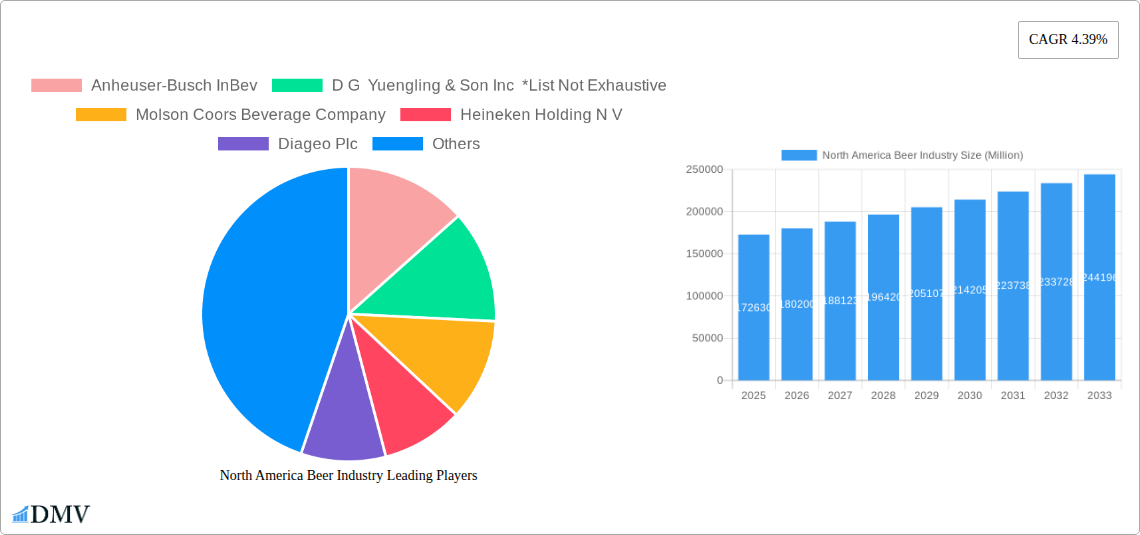

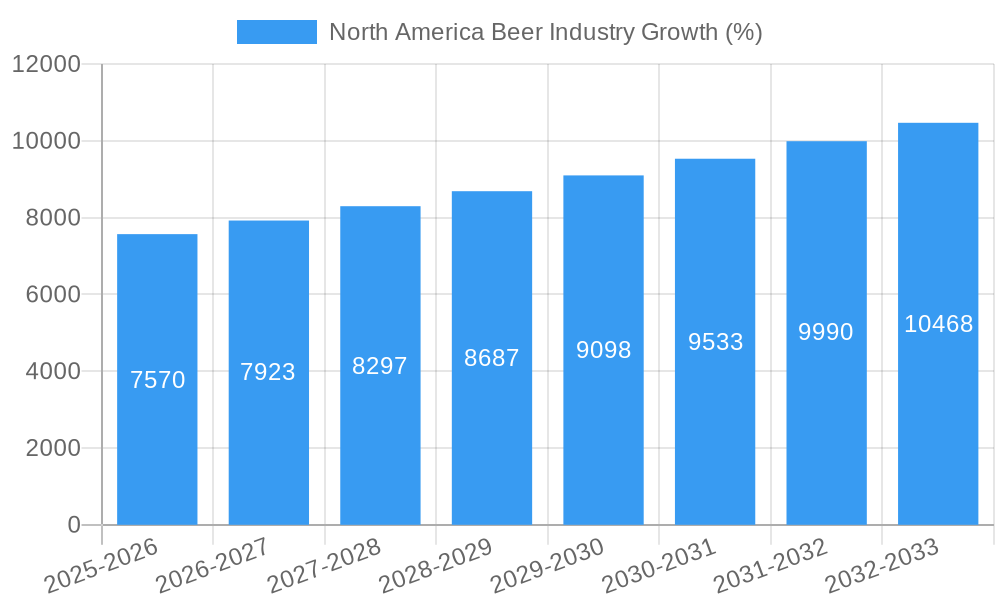

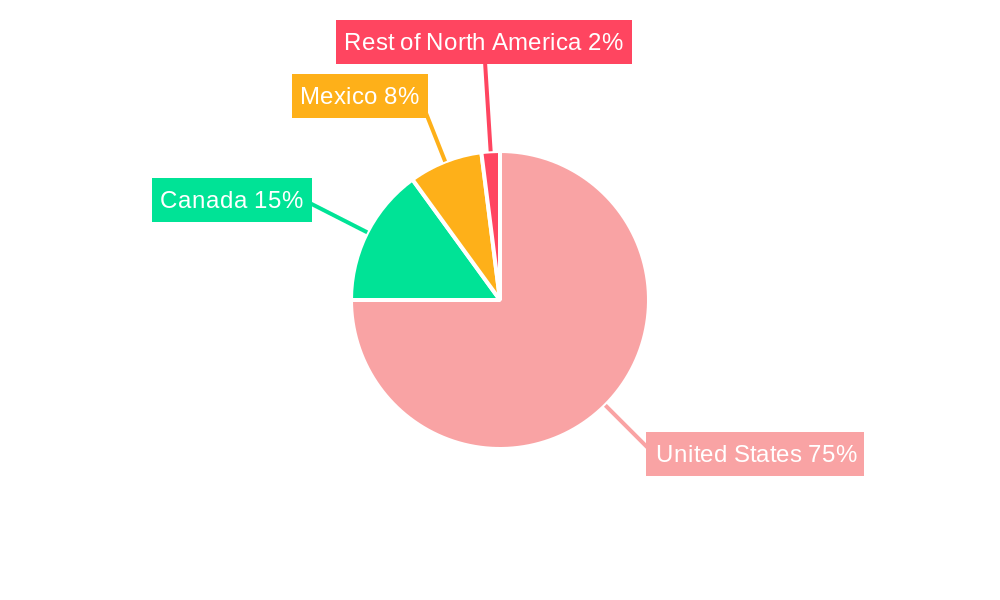

The North American beer market, valued at $172.63 billion in 2025, is projected to experience steady growth, driven by several key factors. The increasing popularity of craft beers and diverse flavor profiles is fueling market expansion, particularly within the Ale segment. Consumer preference for premium and imported beers also contributes to the overall market value. The on-trade channel (bars, restaurants) remains significant, but the off-trade channel (grocery stores, liquor stores) is showing robust growth, reflecting changing consumption habits and the rise of online alcohol delivery services. While the United States dominates the market, Canada and Mexico are also contributing to overall growth, with Mexico showing significant potential for expansion due to its burgeoning middle class and tourism sector. However, the market faces challenges including increasing excise duties and regulations, which could impact pricing and profitability for manufacturers. Furthermore, health concerns regarding alcohol consumption and the rise of non-alcoholic beverages represent potential restraints to market growth. Competition among major players like Anheuser-Busch InBev, Molson Coors, and Heineken, along with the continued rise of craft breweries, further shapes the market landscape. The projected CAGR of 4.39% indicates a consistent, albeit moderate, expansion trajectory over the forecast period (2025-2033).

The segmentation of the North American beer market reveals further insights. The Lager segment, while still dominant, is facing increasing competition from the rapidly expanding Ale segment, reflecting evolving consumer tastes. The "Others" category, encompassing specialty and imported beers, is also showing strong growth potential. Distribution channel analysis highlights the dynamic interplay between on-trade and off-trade segments, reflecting broader societal trends. Geographical analysis underscores the US market’s dominance, while Canada and Mexico present significant growth opportunities due to varied cultural preferences and economic conditions. Future growth is contingent on navigating evolving consumer preferences, managing regulatory hurdles, and adapting to competitive pressures from both established players and emerging craft breweries. A successful market strategy necessitates a keen understanding of these dynamics to capture market share and maximize profitability in this dynamic and competitive industry.

North America Beer Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the North America beer industry, encompassing market trends, competitive dynamics, and future growth prospects. Covering the period 2019-2033, with a base year of 2025, this report is an invaluable resource for stakeholders seeking to understand and navigate this dynamic market.

North America Beer Industry Market Composition & Trends

This section evaluates the North American beer market's composition and prevailing trends from 2019 to 2024. The market, valued at xx Million in 2024, is characterized by a moderate level of concentration, with key players like Anheuser-Busch InBev, Molson Coors Beverage Company, and Constellation Brands holding significant market share. However, craft breweries continue to emerge, challenging the dominance of established players. Innovation is driven by consumer demand for diverse flavors and styles, leading to a surge in craft beers and specialized offerings. The regulatory landscape, varying across countries (US, Canada, Mexico), impacts pricing, distribution, and marketing strategies. Substitute products, such as wine, spirits, and non-alcoholic beverages, compete for consumer spending. The end-user profile is diverse, ranging from young adults to older generations, with varying preferences and consumption habits. M&A activity has been significant, with deal values reaching xx Million annually in recent years, reflecting consolidation and expansion strategies.

- Market Share Distribution (2024): Anheuser-Busch InBev (xx%), Molson Coors (xx%), Constellation Brands (xx%), Others (xx%)

- Key M&A Activities (2019-2024): Royal Unibrew's acquisition of Amsterdam Brewery (July 2022), representing a significant move in the Canadian craft beer sector. Total M&A deal value: xx Million.

- Innovation Catalysts: Growing demand for craft beers, flavored beers, and low/no-alcohol options.

North America Beer Industry Industry Evolution

The North American beer industry has experienced significant evolution from 2019 to 2024. The market has shown a Compound Annual Growth Rate (CAGR) of xx% during the historical period (2019-2024). This growth has been fueled by several factors, including shifting consumer preferences toward premium and craft beers, increased disposable incomes, and targeted marketing campaigns. Technological advancements in brewing processes and distribution networks have enhanced efficiency and product quality. Furthermore, the rise of e-commerce and direct-to-consumer (DTC) channels has disrupted traditional distribution models. Consumer demand has shifted towards more diverse and specialized beer styles, including the growing popularity of IPAs, sours, and other craft beer varieties. Health-conscious consumers are also driving the demand for low-alcohol and non-alcoholic options. The industry continues to adapt to changing demographics and consumer preferences by embracing sustainable practices and responding to health and wellness trends. The projected CAGR for 2025-2033 is xx%, indicating continued market expansion.

Leading Regions, Countries, or Segments in North America Beer Industry

The United States remains the dominant market within North America, accounting for xx% of total beer volume sales in 2024. Mexico follows with xx%, showing robust growth in the premium beer segment. Canada holds xx% share.

- Dominant Segment (Type): Lager remains the largest segment, followed by Ale and "Others" (specialty beers, ciders).

- Dominant Segment (Distribution): Off-trade (retail stores, supermarkets) dominates, followed by on-trade (bars, restaurants).

- Key Drivers (United States): Strong consumer spending, diverse product offerings, established distribution infrastructure.

- Key Drivers (Mexico): Growing middle class, popularity of premium and flavored beers, increasing tourism.

- Key Drivers (Canada): Expanding craft beer sector, proximity to the US market, government regulations.

North America Beer Industry Product Innovations

Recent years have witnessed significant product innovations, with breweries introducing unique flavor profiles, utilizing new brewing techniques (e.g., barrel-aging), and focusing on sustainability. The introduction of hard seltzers and other low/no-alcohol options reflects a broader trend toward healthier alternatives. Goose Island's Bourbon County Stout and Modelo's Oro are prime examples of premium offerings leveraging existing brands. These innovations often incorporate unique selling propositions such as specific ingredient sourcing, unique brewing methods (e.g., souring), and high-quality packaging. Technological advancements in brewing and packaging are improving efficiency and product consistency.

Propelling Factors for North America Beer Industry Growth

Several factors propel the growth of the North American beer industry. Increasing disposable incomes, particularly among younger demographics, support higher beer consumption. Changing consumer preferences, favoring diverse and premium beer styles, fuel market expansion. Technological advancements in brewing and distribution enhance efficiency and product quality. The rise of craft breweries and their unique offerings contributes to market dynamism and consumer interest. Favorable regulatory environments in some regions also support market expansion.

Obstacles in the North America Beer Industry Market

The North American beer industry faces challenges such as intense competition, increasing raw material costs, and potential regulatory hurdles. Supply chain disruptions can impact production and distribution. Fluctuations in consumer spending and changing preferences pose risks. The increasing popularity of substitute beverages (wine, spirits, etc.) represents a significant competitive pressure. Stricter regulations on alcohol marketing and consumption in some areas also hinder growth. The impact of these factors can translate into reduced profitability and slowed growth. The estimated impact of these challenges on revenue is approximately xx Million annually.

Future Opportunities in North America Beer Industry

The future of the North American beer industry presents multiple opportunities. Expanding into new markets (e.g., specific demographics or regions) is a key growth strategy. Technological innovation, such as improved brewing techniques and sustainable packaging, offers competitive advantages. Capitalizing on trends like low/no-alcohol options and personalized offerings will attract health-conscious consumers. Expansion into international markets is also an avenue for growth.

Major Players in the North America Beer Industry Ecosystem

- Anheuser-Busch InBev

- D G Yuengling & Son Inc

- Molson Coors Beverage Company

- Heineken Holding N V

- Diageo Plc

- Constellation Brands Inc

- Suntory Beverage & Food Limited

- FIFCO USA

- Carlsberg Group

- Boston Beer Company

Key Developments in North America Beer Industry Industry

- November 2022: Goose Island Beer Company launches the 2022 edition of Bourbon County Stout in the US.

- July 2022: Royal Unibrew acquires Amsterdam Brewery Co. Ltd., expanding its Canadian presence and production capacity.

- March 2022: Modelo launches Modelo Oro premium light beer, expanding its product portfolio in Mexico.

Strategic North America Beer Industry Market Forecast

The North American beer market is projected to experience robust growth in the forecast period (2025-2033), driven by continued consumer demand, product innovation, and strategic investments by major players. Opportunities exist in premium segments, craft beer categories, and low/no-alcohol options. The market's dynamic nature, coupled with consumer preference shifts, presents exciting avenues for growth and significant market potential. The total market value is expected to reach xx Million by 2033.

North America Beer Industry Segmentation

-

1. Type

- 1.1. Lager

- 1.2. Ale

- 1.3. Others

-

2. Distribution Channel

- 2.1. On-Trade

- 2.2. Off-Trade

North America Beer Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Beer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.39% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Demand for Nutricosmetics Among Millennials; Growing Beauty and Wellness Trend

- 3.3. Market Restrains

- 3.3.1. Stringent Government Regulations and Product Guidelines

- 3.4. Market Trends

- 3.4.1. Growing Demand for Beer Across the United States

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Lager

- 5.1.2. Ale

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. On-Trade

- 5.2.2. Off-Trade

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United States North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Beer Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Anheuser-Busch InBev

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 D G Yuengling & Son Inc *List Not Exhaustive

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Molson Coors Beverage Company

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Heineken Holding N V

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Diageo Plc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Constellation Brands Inc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Suntory Beverage & Food Limited

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 FIFCO USA

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Carlsberg Group

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Boston Beer Company

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Anheuser-Busch InBev

List of Figures

- Figure 1: North America Beer Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Beer Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Beer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Beer Industry Volume liter Forecast, by Region 2019 & 2032

- Table 3: North America Beer Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: North America Beer Industry Volume liter Forecast, by Type 2019 & 2032

- Table 5: North America Beer Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 6: North America Beer Industry Volume liter Forecast, by Distribution Channel 2019 & 2032

- Table 7: North America Beer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: North America Beer Industry Volume liter Forecast, by Region 2019 & 2032

- Table 9: North America Beer Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: North America Beer Industry Volume liter Forecast, by Country 2019 & 2032

- Table 11: United States North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United States North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 13: Canada North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 15: Mexico North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Mexico North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 17: Rest of North America North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Rest of North America North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 19: North America Beer Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 20: North America Beer Industry Volume liter Forecast, by Type 2019 & 2032

- Table 21: North America Beer Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 22: North America Beer Industry Volume liter Forecast, by Distribution Channel 2019 & 2032

- Table 23: North America Beer Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: North America Beer Industry Volume liter Forecast, by Country 2019 & 2032

- Table 25: United States North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: United States North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 27: Canada North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Canada North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 29: Mexico North America Beer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Mexico North America Beer Industry Volume (liter ) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Beer Industry?

The projected CAGR is approximately 4.39%.

2. Which companies are prominent players in the North America Beer Industry?

Key companies in the market include Anheuser-Busch InBev, D G Yuengling & Son Inc *List Not Exhaustive, Molson Coors Beverage Company, Heineken Holding N V, Diageo Plc, Constellation Brands Inc, Suntory Beverage & Food Limited, FIFCO USA, Carlsberg Group, Boston Beer Company.

3. What are the main segments of the North America Beer Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 172.63 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Nutricosmetics Among Millennials; Growing Beauty and Wellness Trend.

6. What are the notable trends driving market growth?

Growing Demand for Beer Across the United States.

7. Are there any restraints impacting market growth?

Stringent Government Regulations and Product Guidelines.

8. Can you provide examples of recent developments in the market?

In November 2022, Goose Island Beer Company's Canada branch announced the launch of the 2022 edition of Bourbon County Stout. It was officially introduced in the United States on Black Friday. The 2022 Original Bourbon County Stout was aged in a mix of bourbon barrels from Buffalo Trace, Heaven Hill, and Wild Turkey distilleries.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in liter .

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Beer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Beer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Beer Industry?

To stay informed about further developments, trends, and reports in the North America Beer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence