Key Insights

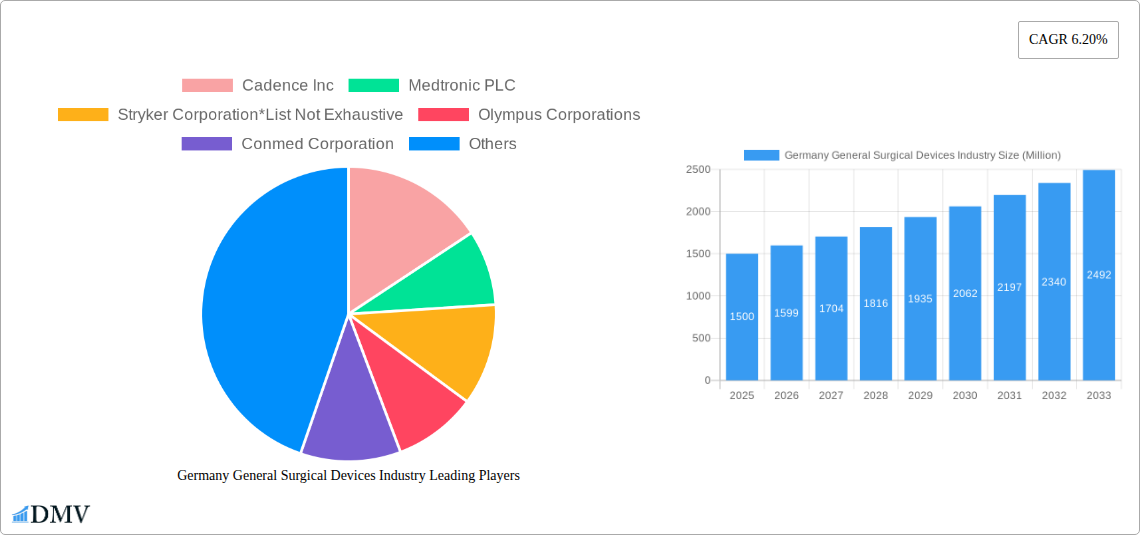

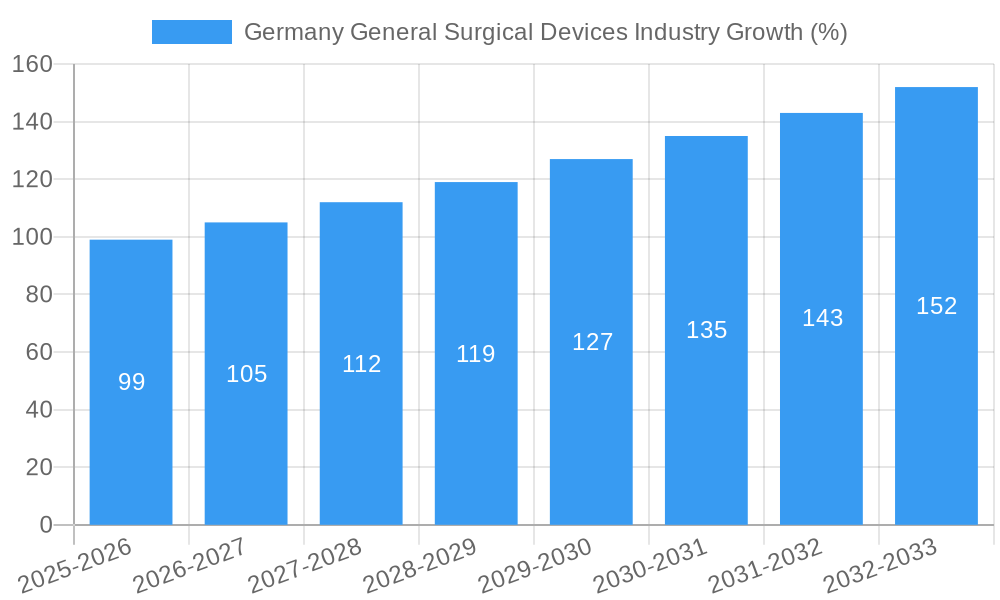

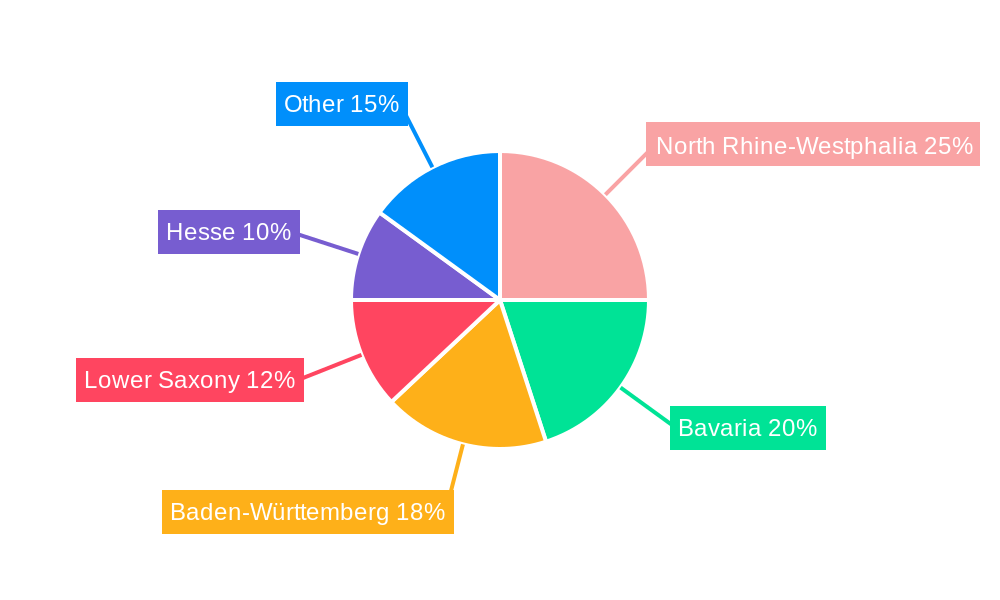

The German general surgical devices market, valued at approximately €1.5 billion in 2025, is projected to experience robust growth, driven by a rising elderly population, increasing prevalence of chronic diseases necessitating surgical interventions, and advancements in minimally invasive surgical techniques. The market's Compound Annual Growth Rate (CAGR) of 6.20% from 2025 to 2033 indicates a significant expansion, with projected values exceeding €2.5 billion by 2033. Key segments driving this growth include laparoscopic devices, fueled by their minimally invasive nature and shorter recovery times; and electro surgical devices, benefiting from technological advancements offering enhanced precision and efficiency. The strong presence of established medical device companies in Germany, coupled with substantial government investment in healthcare infrastructure, further contributes to the market's positive outlook. However, stringent regulatory approvals and rising healthcare costs pose potential challenges. Regional variations within Germany exist, with states like North Rhine-Westphalia, Bavaria, and Baden-Württemberg expected to contribute significantly due to their higher population density and well-established healthcare systems.

The market segmentation reveals a diverse landscape. Handheld devices maintain a significant share due to their versatility and affordability, while the demand for advanced technologies such as robotic surgery is gradually increasing. Application-wise, gynecology and urology, cardiology, and orthopedics constitute the largest segments, reflecting the high volume of surgical procedures performed in these areas. Competitive pressures among established players like Medtronic, Stryker, and Johnson & Johnson are intense, leading to continuous innovation and a focus on delivering superior products and services. The market's future trajectory hinges on technological advancements, regulatory landscape evolution, and the ongoing prioritization of healthcare expenditure in Germany. Focus areas for future growth include the integration of digital technologies into surgical devices and the development of personalized surgical solutions.

Germany General Surgical Devices Industry: Market Analysis & Forecast (2019-2033)

This comprehensive report provides an in-depth analysis of the Germany general surgical devices market, offering invaluable insights for stakeholders seeking to understand current market dynamics and future growth potential. The study period covers 2019-2033, with 2025 as the base and estimated year. The forecast period spans 2025-2033, and the historical period encompasses 2019-2024. The report leverages rigorous research methodologies to provide a precise and actionable overview of this dynamic sector.

Germany General Surgical Devices Industry Market Composition & Trends

The German general surgical devices market, valued at €XX Million in 2024, exhibits a moderately consolidated structure. Key players such as Medtronic PLC, Stryker Corporation, Johnson & Johnson, and B. Braun SE hold significant market share, collectively accounting for approximately XX% of the market in 2024. However, the presence of numerous smaller, specialized companies fosters competition and innovation.

Market growth is driven by several factors: an aging population requiring more surgical procedures, technological advancements leading to minimally invasive techniques, and increasing government investment in healthcare infrastructure. Regulatory changes, including the implementation of new medical device regulations, influence market dynamics. Substitute products, such as minimally invasive therapies, pose a competitive challenge. The market witnesses consistent mergers and acquisitions (M&A) activity, with deal values exceeding €XX Million annually in recent years. End-users primarily include hospitals, surgical centers, and clinics across Germany.

- Market Concentration: Moderately consolidated, with top players holding XX% market share in 2024.

- Innovation Catalysts: Technological advancements in minimally invasive surgery and digital health.

- Regulatory Landscape: Stringent regulations impacting product approval and market entry.

- Substitute Products: Minimally invasive therapies and alternative treatment methods.

- End-User Profile: Hospitals, surgical centers, and specialized clinics.

- M&A Activity: Significant M&A activity with annual deal values exceeding €XX Million.

Germany General Surgical Devices Industry Industry Evolution

The German general surgical devices market has witnessed robust growth over the historical period (2019-2024), with a CAGR of approximately XX%. This growth trajectory is expected to continue during the forecast period (2025-2033), albeit at a slightly moderated pace, reaching €XX Million by 2033, driven by technological advancements such as robotic surgery, improved imaging techniques, and the development of smart surgical devices. Consumer demand is shifting towards minimally invasive procedures, resulting in increased adoption of laparoscopic and handheld devices. The integration of digital technologies, including AI and machine learning, is transforming surgical practices, enhancing precision and efficiency, and streamlining workflows. This transition to advanced technologies is driving market growth, although the initial investment costs can pose a challenge for some healthcare providers.

Leading Regions, Countries, or Segments in Germany General Surgical Devices Industry

The German general surgical devices market shows strong performance across various segments and regions. While detailed regional breakdowns require further analysis, the following observations are notable:

- By Product: Laparoscopic devices and electro surgical devices dominate the market, driven by a rising preference for minimally invasive procedures and technological advancements. Handheld devices maintain a significant share due to their versatility and affordability.

- By Application: Gynecology and urology, along with orthopedic applications, represent the largest segments due to high procedure volumes. Cardiology and neurology segments are also experiencing significant growth, driven by rising incidences and advancements in surgical techniques.

Key Drivers (across all leading segments):

- High Investment in Healthcare Infrastructure: Significant public and private investment in modernizing hospitals and surgical centers.

- Government Support for Technological Advancements: Funding initiatives aimed at promoting innovation and adoption of advanced surgical technologies.

- Rising Prevalence of Chronic Diseases: Increased demand for surgical interventions to address prevalent health conditions.

The dominance of specific segments is primarily attributable to consistent technological advancements, increased demand for minimally invasive procedures, and robust government support for healthcare infrastructure.

Germany General Surgical Devices Industry Product Innovations

Recent years have witnessed significant innovation within the German general surgical devices market. Manufacturers are focusing on developing advanced minimally invasive devices, incorporating features such as enhanced imaging capabilities, improved precision, and enhanced ergonomics. The integration of digital technologies, particularly in robotic surgery systems and smart instruments, is a prominent trend. These innovations not only improve surgical outcomes but also increase efficiency and reduce the risk of complications. Unique selling propositions often include improved visualization, intuitive interfaces, and reduced trauma during procedures.

Propelling Factors for Germany General Surgical Devices Industry Growth

The German general surgical devices market growth is propelled by a combination of factors. Technological advancements, such as the development of robotic surgery systems and minimally invasive devices, are significantly impacting market growth. Economic factors, including government healthcare spending and increasing private health insurance coverage, are also crucial drivers. Favorable regulatory environments, promoting innovation and medical device approvals, further stimulate market growth.

Obstacles in the Germany General Surgical Devices Industry Market

Several challenges hinder the growth of the German general surgical devices market. Strict regulatory approvals and reimbursement policies can create delays in product launches and limit market access for new technologies. Supply chain disruptions, particularly evident in recent years due to global events, impact the availability of devices and increase manufacturing costs. Intense competition from both domestic and international players creates pressure on pricing and profitability. These factors create an environment that is both dynamic and challenging for market entrants.

Future Opportunities in Germany General Surgical Devices Industry

Future opportunities lie in the continued development and adoption of minimally invasive surgical techniques, personalized medicine approaches and integrating AI and machine learning into surgical procedures. Growth in areas such as robotic surgery, 3D-printed implants, and smart surgical tools present further avenues for market expansion. Expanding into new application areas and catering to the increasing demand for advanced surgical technologies presents significant opportunities for growth within the German market.

Major Players in the Germany General Surgical Devices Industry Ecosystem

- Cadence Inc

- Medtronic PLC

- Stryker Corporation

- Olympus Corporations

- Conmed Corporation

- Johnson & Johnson

- Boston Scientific Corporation

- B Braun SE

- Integer Holdings Corporation

- Getinge (Maquet Holding BV & Co KG)

Key Developments in Germany General Surgical Devices Industry Industry

- September 2022: Installation of the Senhance Surgical System by Asensus Surgical at Evangelical Hospital Goettingen-Weende, marking the introduction of a new digital laparoscopic platform.

- April 2022: Carl Zeiss Meditec's acquisition of Kogent Surgical, LLC and Katalyst Surgical, LLC, strengthens its position in the German surgical instruments market.

Strategic Germany General Surgical Devices Industry Market Forecast

The German general surgical devices market is poised for sustained growth, driven by technological innovations, favorable regulatory environments, and an increasing demand for advanced surgical solutions. The market's future potential is significant, with continued expansion expected across various segments. The adoption of minimally invasive procedures and integration of digital technologies will be key growth catalysts.

Germany General Surgical Devices Industry Segmentation

-

1. Product

- 1.1. Handheld Devices

- 1.2. Laproscopic Devices

- 1.3. Electro Surgical Devices

- 1.4. Wound Closure Devices

- 1.5. Trocars and Access Devices

- 1.6. Other Products

-

2. Application

- 2.1. Gynecology and Urology

- 2.2. Cardiology

- 2.3. Orthopedic

- 2.4. Neurology

- 2.5. Other Applications

Germany General Surgical Devices Industry Segmentation By Geography

- 1. Germany

Germany General Surgical Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.20% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Minimally Invasive Devices; Growing Cases of Injuries and Accidents; Increasing Healthcare Expenditure in Germany

- 3.3. Market Restrains

- 3.3.1. Stringent Government Regulations and Improper Reimbursement for Surgical Devices

- 3.4. Market Trends

- 3.4.1. Handheld Surgical Devices to Witness Steady Growth Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Germany General Surgical Devices Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Handheld Devices

- 5.1.2. Laproscopic Devices

- 5.1.3. Electro Surgical Devices

- 5.1.4. Wound Closure Devices

- 5.1.5. Trocars and Access Devices

- 5.1.6. Other Products

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Gynecology and Urology

- 5.2.2. Cardiology

- 5.2.3. Orthopedic

- 5.2.4. Neurology

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North Rhine-Westphalia Germany General Surgical Devices Industry Analysis, Insights and Forecast, 2019-2031

- 7. Bavaria Germany General Surgical Devices Industry Analysis, Insights and Forecast, 2019-2031

- 8. Baden-Württemberg Germany General Surgical Devices Industry Analysis, Insights and Forecast, 2019-2031

- 9. Lower Saxony Germany General Surgical Devices Industry Analysis, Insights and Forecast, 2019-2031

- 10. Hesse Germany General Surgical Devices Industry Analysis, Insights and Forecast, 2019-2031

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Cadence Inc

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Medtronic PLC

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Stryker Corporation*List Not Exhaustive

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Olympus Corporations

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Conmed Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Johnson & Johnson

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Boston Scientific Corporation

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 B Braun SE

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Integer Holdings Corporation

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Getinge (Maquet Holding BV & Co KG)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Cadence Inc

List of Figures

- Figure 1: Germany General Surgical Devices Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Germany General Surgical Devices Industry Share (%) by Company 2024

List of Tables

- Table 1: Germany General Surgical Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Germany General Surgical Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 3: Germany General Surgical Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Germany General Surgical Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Germany General Surgical Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: North Rhine-Westphalia Germany General Surgical Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Bavaria Germany General Surgical Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Baden-Württemberg Germany General Surgical Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Lower Saxony Germany General Surgical Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Hesse Germany General Surgical Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Germany General Surgical Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 12: Germany General Surgical Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 13: Germany General Surgical Devices Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany General Surgical Devices Industry?

The projected CAGR is approximately 6.20%.

2. Which companies are prominent players in the Germany General Surgical Devices Industry?

Key companies in the market include Cadence Inc, Medtronic PLC, Stryker Corporation*List Not Exhaustive, Olympus Corporations, Conmed Corporation, Johnson & Johnson, Boston Scientific Corporation, B Braun SE, Integer Holdings Corporation, Getinge (Maquet Holding BV & Co KG).

3. What are the main segments of the Germany General Surgical Devices Industry?

The market segments include Product, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Minimally Invasive Devices; Growing Cases of Injuries and Accidents; Increasing Healthcare Expenditure in Germany.

6. What are the notable trends driving market growth?

Handheld Surgical Devices to Witness Steady Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Stringent Government Regulations and Improper Reimbursement for Surgical Devices.

8. Can you provide examples of recent developments in the market?

September 2022: Senhance Surgical System, manufactured by Asensus Surgical, was installed at Evangelical Hospital Goettingen-Weende of Göttingen, Germany. Senhance Surgical System is a first-of-its-kind digital laparoscopic platform that is powered by the company's Intelligent Surgical Unit (ISU).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany General Surgical Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany General Surgical Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany General Surgical Devices Industry?

To stay informed about further developments, trends, and reports in the Germany General Surgical Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence