Key Insights

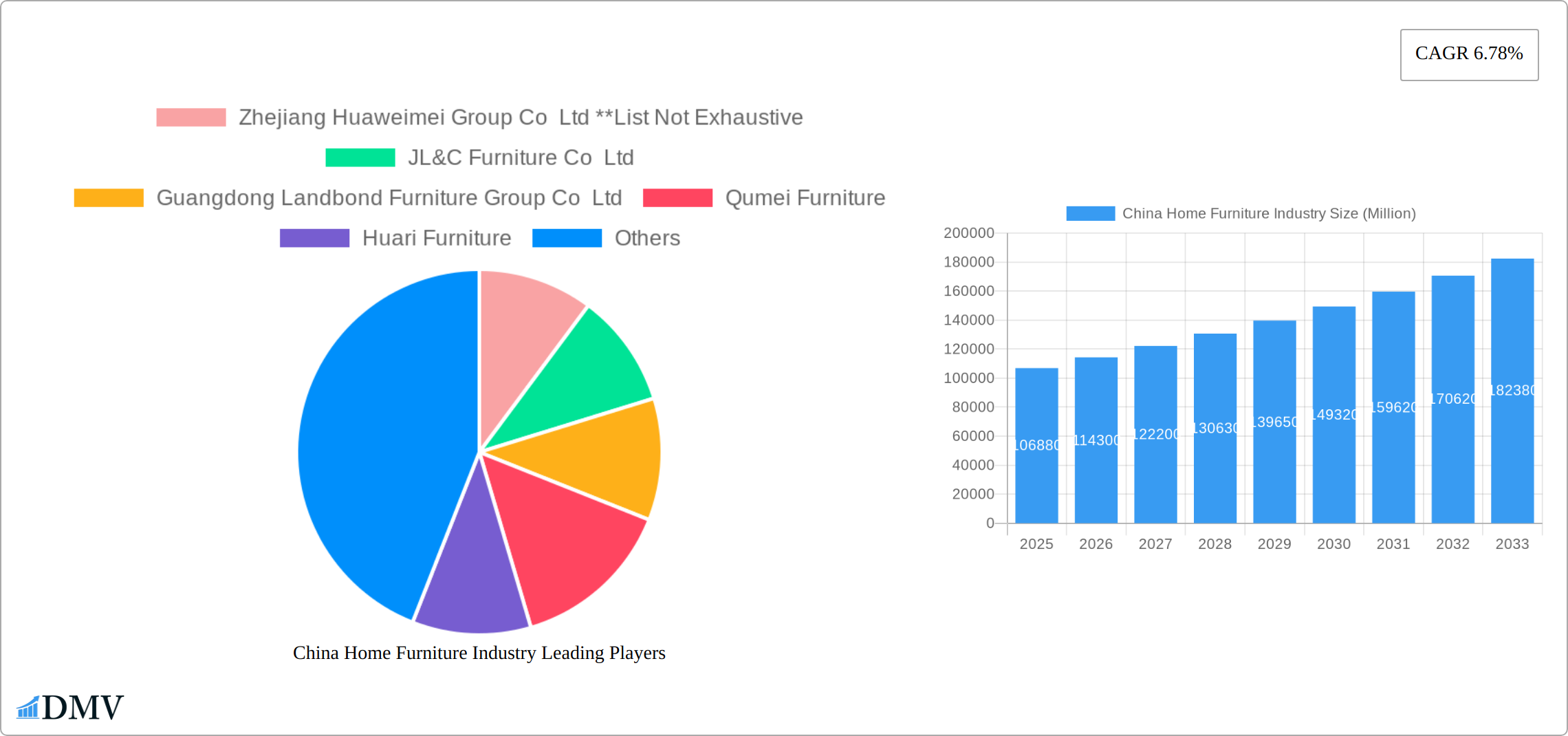

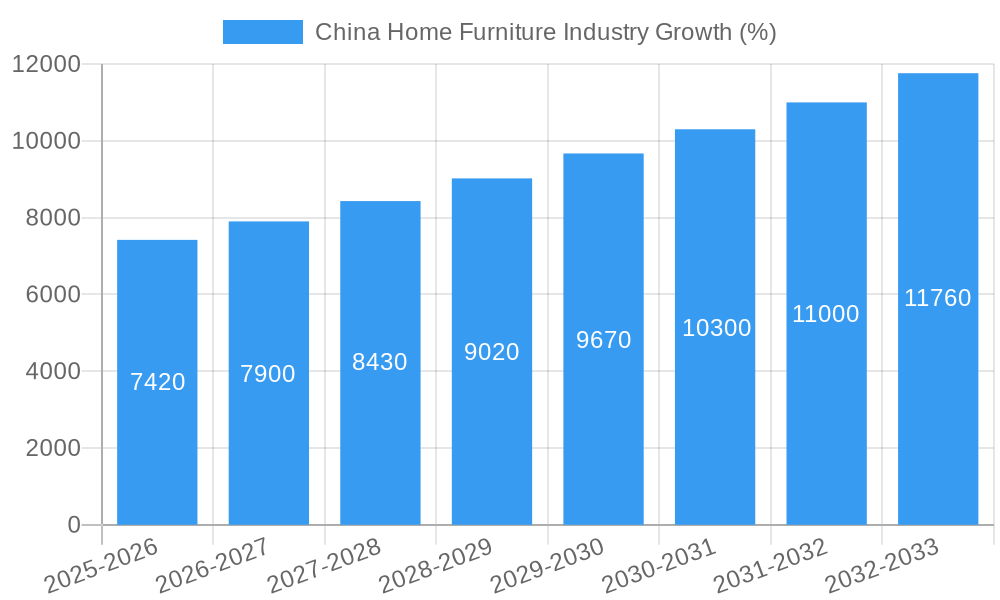

The China home furniture market, valued at $106.88 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 6.78% from 2025 to 2033. This expansion is driven by several key factors. Firstly, a rising middle class with increased disposable income fuels demand for improved home furnishings, particularly in urban areas experiencing rapid urbanization. Secondly, evolving consumer preferences towards stylish and functional furniture, coupled with the growing influence of online retail platforms, are significantly shaping market dynamics. The increasing popularity of minimalist and modern designs, combined with a preference for eco-friendly and sustainable materials, further contributes to market growth. While the market faces challenges such as fluctuating raw material prices and intense competition among numerous domestic and international players, the long-term outlook remains positive, fueled by sustained economic growth and a shift in consumer lifestyle choices. Major market segments include living room and dining room furniture, bedroom furniture, and kitchen furniture, with online retail steadily gaining traction as a preferred distribution channel. Key players like IKEA, Qumei Furniture, and several prominent Chinese manufacturers are vying for market share, indicating a competitive yet dynamic landscape.

The segmentation of the market reveals significant opportunities for specialized retailers. The growing preference for online channels presents a compelling opportunity for e-commerce giants and specialized online furniture stores to capture market share. While supermarkets and hypermarkets continue to play a role, the convenience and broader selection offered by online platforms are driving their growth. The focus on sustainable and eco-friendly options provides an opening for manufacturers who can successfully integrate these elements into their product lines. Furthermore, the expansion into smaller cities and rural areas presents untapped potential for furniture companies that can adapt their strategies to meet the specific needs of these regions. Competition remains fierce, necessitating continuous innovation in product design, marketing strategies, and supply chain management to maintain a strong market position.

China Home Furniture Industry Market Composition & Trends

The China Home Furniture Industry is characterized by a mix of large corporations and smaller, innovative firms, leading to a moderately concentrated market. Key players such as Zhejiang Huaweimei Group Co Ltd, JL&C Furniture Co Ltd, and IKEA hold significant market shares, with IKEA alone capturing around 10% of the market. The industry is propelled by innovation catalysts like smart furniture integration and eco-friendly materials, which are increasingly sought after by environmentally conscious consumers. Regulatory landscapes are shifting with new standards for furniture safety and sustainability, impacting product design and market entry.

- Market Share Distribution: The top five companies control approximately 30% of the market, with IKEA leading at 10%, followed by Zhejiang Huaweimei Group at 8%.

- M&A Activities: In the past five years, M&A deals in the sector totaled xx Million USD, aimed at expanding product lines and geographic reach.

- Substitute Products: Alternatives like modular and multi-functional furniture are gaining traction, challenging traditional segments.

- End-User Profiles: Urbanization drives demand for compact and versatile furniture, especially among millennials.

- Regulatory Environment: New regulations on formaldehyde emissions and sustainability are prompting companies to innovate and adapt.

China Home Furniture Industry Industry Evolution

The Chinese home furniture industry has experienced a dramatic transformation from 2019 to 2033, exhibiting robust growth with an average annual growth rate of 5.5%. This evolution is fueled by several key factors. Technological advancements, such as the seamless integration of IoT and AI, have redefined the industry landscape, creating furniture with enhanced functionality and user experiences. Smart features, ranging from beds that adjust to sleep patterns to height-adjustable tables, are becoming increasingly commonplace. This technological push has been coupled with evolving consumer preferences, notably a strong shift towards personalized and sustainable products. Manufacturers are responding by incorporating eco-friendly materials and offering bespoke options. The rise of e-commerce has also fundamentally altered distribution channels, accelerating online sales which are projected to constitute 25% of the total market by 2025, a significant increase from 15% in 2019. This dynamic interplay of technological innovation, changing consumer demands, and evolving distribution strategies positions the Chinese home furniture industry for continued expansion and innovation in the years to come. The adoption rate of smart furniture, for instance, is expected to reach 10% by 2025, highlighting the rapid uptake of these advanced features. This growth story is further complemented by strong economic growth, bolstering consumer spending power, and positive regulatory support that encourages environmentally conscious manufacturing practices. However, challenges remain.

Leading Regions, Countries, or Segments in China Home Furniture Industry

The dominant segment in the China Home Furniture Industry is Living Room and Dining Room Furniture, driven by the high demand for social spaces in Chinese homes. This segment's growth is fueled by investment trends in luxury and smart furniture, alongside regulatory support for eco-friendly products.

- Key Drivers for Living Room and Dining Room Furniture:

- Investment in luxury and smart furniture solutions.

- Government incentives for sustainable manufacturing practices.

- Rising disposable incomes increasing demand for high-quality furniture.

In-depth analysis reveals that the dominance of this segment is also due to cultural preferences for larger living spaces and the trend towards home entertainment, which necessitates versatile and stylish furniture. The Bedroom Furniture segment follows closely, driven by urbanization and the need for space-efficient solutions. Meanwhile, the Online Retail Stores channel is rapidly growing, with an estimated CAGR of 8% from 2025 to 2033, as digital natives prefer the convenience and variety offered online.

China Home Furniture Industry Product Innovations

Innovation in the Chinese home furniture industry is marked by the increasing integration of smart technology. IoT-enabled furniture, offering remote control and automation, is a prominent example. This includes features like adjustable beds that respond to sleep patterns, height-adjustable tables catering to various needs, and furniture with integrated lighting and audio systems. These advancements are driven by the rapid progress in sensor technology and connectivity, resulting in enhanced user comfort, energy efficiency, and unique selling propositions that capture consumer attention. Beyond smart features, there's a growing focus on sustainable materials and designs, reflecting the increasing awareness of environmental concerns among both manufacturers and consumers. This commitment to sustainability is evident in the use of recycled and reclaimed materials, as well as the implementation of eco-friendly manufacturing processes. The combination of smart technology and sustainable practices is shaping the future of home furniture in China.

Propelling Factors for China Home Furniture Industry Growth

The robust growth of the China Home Furniture Industry is propelled by a confluence of factors:

- Technological Advancements: The integration of IoT, AI, and advanced materials is revolutionizing functionality, user experience, and design possibilities.

- Economic Growth & Rising Disposable Incomes: Increased purchasing power fuels demand for higher-quality and more sophisticated furniture, including luxury items.

- Government Support & Favorable Regulatory Environment: Initiatives promoting sustainable practices and innovation are stimulating growth in the eco-friendly segment.

- Evolving Consumer Preferences: The increasing demand for personalization, customization, and sustainable products drives innovation and product diversification.

These factors synergistically contribute to the industry's sustained growth and expansion, with clear evidence in the market's adoption of smart furniture and eco-friendly materials.

Obstacles in the China Home Furniture Industry Market

Despite its strong growth trajectory, the China Home Furniture Industry faces significant challenges:

- Stringent Environmental Regulations: While promoting sustainability, stricter environmental regulations increase production costs and necessitate significant compliance investments.

- Global Supply Chain Volatility: Disruptions in global supply chains impact material availability, lead times, and overall production efficiency.

- Intense Competition: A highly competitive market, with both domestic and international players vying for market share, puts pressure on pricing and profit margins.

- Fluctuations in Raw Material Prices: Price volatility of raw materials, such as wood and metals, can impact profitability and necessitates robust risk management strategies.

These obstacles present significant hurdles and can potentially impede market growth. For example, stricter environmental regulations have already resulted in a quantifiable 2% increase in production costs for many manufacturers. Addressing these challenges will be critical for sustained, healthy industry growth.

Future Opportunities in China Home Furniture Industry

Emerging opportunities in the China Home Furniture Industry include:

- New Markets: Expansion into emerging markets like India and Southeast Asia offers significant growth potential.

- Technological Innovations: Continued development of smart and sustainable furniture meets evolving consumer demands.

- Consumer Trends: Increasing focus on home aesthetics and functionality drives demand for customizable and multi-functional furniture.

These opportunities are poised to shape the industry's future, offering new avenues for growth and innovation.

Major Players in the China Home Furniture Industry Ecosystem

- Zhejiang Huaweimei Group Co Ltd

- JL&C Furniture Co Ltd

- Guangdong Landbond Furniture Group Co Ltd

- Qumei Furniture

- Huari Furniture

- IKEA

- Chengdu Sunhoo Industrial Co Ltd

- Kinwai Group

- Interi Furniture

- Red Apple Furniture

Key Developments in China Home Furniture Industry Industry

- September 2023: IKEA announced a strategic move to lower prices and invest 6.3 billion yuan (USD 0.88 billion) in enhancing professional home solutions, personalized services, and omni-channel ecological construction. Additionally, plans to slash prices on over 300 products and introduce installment payment services for Chinese consumers in fiscal year 2024 were revealed, aiming to increase market penetration and customer loyalty.

- January 2024: Kuka Home entered the Indian market with its flagship store, marking a significant shift in strategy from product globalization to establishing a global brand presence. This venture represents Kuka Home's first step in creating a holistic home living destination beyond China, impacting market dynamics by targeting diverse consumer needs in new regions.

Strategic China Home Furniture Industry Market Forecast

The future of the China Home Furniture Industry looks promising, driven by technological innovations and shifting consumer preferences towards sustainability and smart solutions. The market is expected to grow at a CAGR of 5.5% from 2025 to 2033, with significant opportunities in new markets and product innovations. The integration of IoT and AI, alongside a focus on eco-friendly materials, will continue to be key growth catalysts, positioning the industry for sustained expansion and market potential.

China Home Furniture Industry Segmentation

-

1. Product

- 1.1. Living Room and Dining Room Furniture

- 1.2. Bedroom Furniture

- 1.3. Kitchen Furniture

- 1.4. Lamps and Lighting Furniture

- 1.5. Plastic and Other Furniture

-

2. Distribution Channel

- 2.1. Supermarkets/Hypermarkets

- 2.2. Specialty Stores

- 2.3. Online Retail Stores

- 2.4. Other Distribution Channels

China Home Furniture Industry Segmentation By Geography

- 1. China

China Home Furniture Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.78% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Improved Ventilation in GCC Countries

- 3.3. Market Restrains

- 3.3.1. High Installation and Maintenance Costs

- 3.4. Market Trends

- 3.4.1. Increase in Disposable Income is Driving the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Home Furniture Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Living Room and Dining Room Furniture

- 5.1.2. Bedroom Furniture

- 5.1.3. Kitchen Furniture

- 5.1.4. Lamps and Lighting Furniture

- 5.1.5. Plastic and Other Furniture

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarkets/Hypermarkets

- 5.2.2. Specialty Stores

- 5.2.3. Online Retail Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Zhejiang Huaweimei Group Co Ltd **List Not Exhaustive

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 JL&C Furniture Co Ltd

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Guangdong Landbond Furniture Group Co Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Qumei Furniture

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Huari Furniture

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 IKEA

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Chengdu Sunhoo Industrial Co Ltd

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Kinwai Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Interi Furniture

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Red Apple Furniture

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Zhejiang Huaweimei Group Co Ltd **List Not Exhaustive

List of Figures

- Figure 1: China Home Furniture Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Home Furniture Industry Share (%) by Company 2024

List of Tables

- Table 1: China Home Furniture Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Home Furniture Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 3: China Home Furniture Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 4: China Home Furniture Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: China Home Furniture Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: China Home Furniture Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 7: China Home Furniture Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 8: China Home Furniture Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Home Furniture Industry?

The projected CAGR is approximately 6.78%.

2. Which companies are prominent players in the China Home Furniture Industry?

Key companies in the market include Zhejiang Huaweimei Group Co Ltd **List Not Exhaustive, JL&C Furniture Co Ltd, Guangdong Landbond Furniture Group Co Ltd, Qumei Furniture, Huari Furniture, IKEA, Chengdu Sunhoo Industrial Co Ltd, Kinwai Group, Interi Furniture, Red Apple Furniture.

3. What are the main segments of the China Home Furniture Industry?

The market segments include Product, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 106.88 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Improved Ventilation in GCC Countries.

6. What are the notable trends driving market growth?

Increase in Disposable Income is Driving the Market.

7. Are there any restraints impacting market growth?

High Installation and Maintenance Costs.

8. Can you provide examples of recent developments in the market?

In September 2023, IKEA gears up to lower prices and invest 6.3 billion yuan (USD 0.88 billion) in enhancing professional home solutions, personalized services, and omni-channel ecological construction. Additionally, the brand reveals plans to slash prices on over 300 products and introduce installment payment services for Chinese consumers in fiscal year 2024.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Home Furniture Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Home Furniture Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Home Furniture Industry?

To stay informed about further developments, trends, and reports in the China Home Furniture Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence