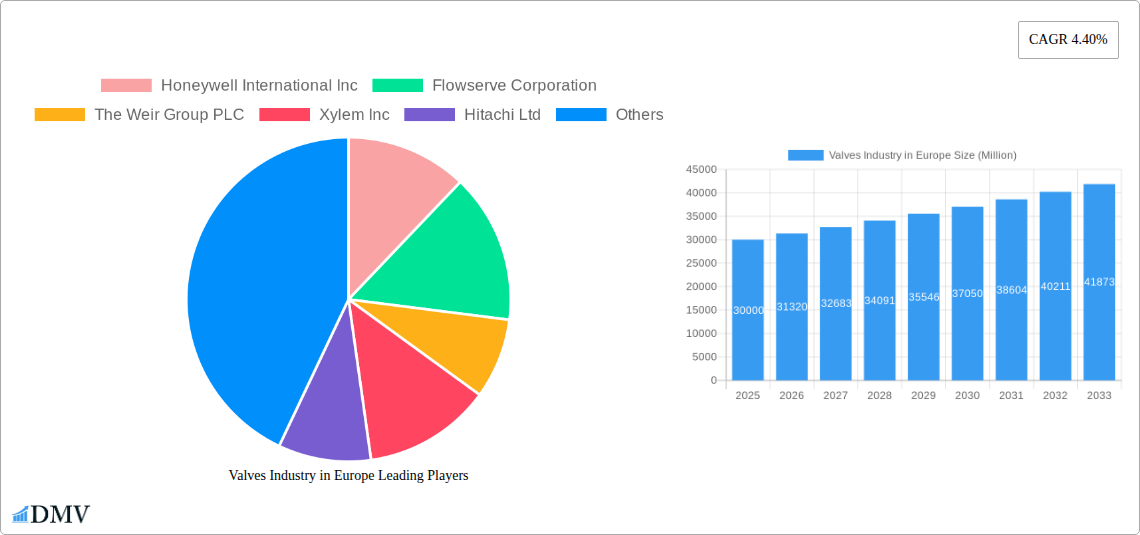

Key Insights

The European valves market, valued at approximately €[Estimate based on market size XX and regional breakdown. For example, if XX is $100 million and Europe constitutes 30% of the global market, the European market size would be approximately €30 million in the base year. Adjust this based on your actual 'XX' value and reasonable regional distribution], is projected to experience robust growth, driven by a Compound Annual Growth Rate (CAGR) of 4.40% from 2025 to 2033. This expansion is fueled by several key factors. Firstly, increasing investments in infrastructure projects across Europe, particularly in energy and water management, are boosting demand for various valve types, including ball, butterfly, and gate valves. Secondly, the growing emphasis on automation and smart technologies within industrial processes is driving the adoption of advanced control valves and related systems. The oil and gas sector, along with the chemical and water & wastewater treatment industries, remain significant end-users, consistently requiring valve replacements and upgrades to maintain operational efficiency and safety. Furthermore, stringent environmental regulations are promoting the utilization of valves designed for energy efficiency and reduced emissions.

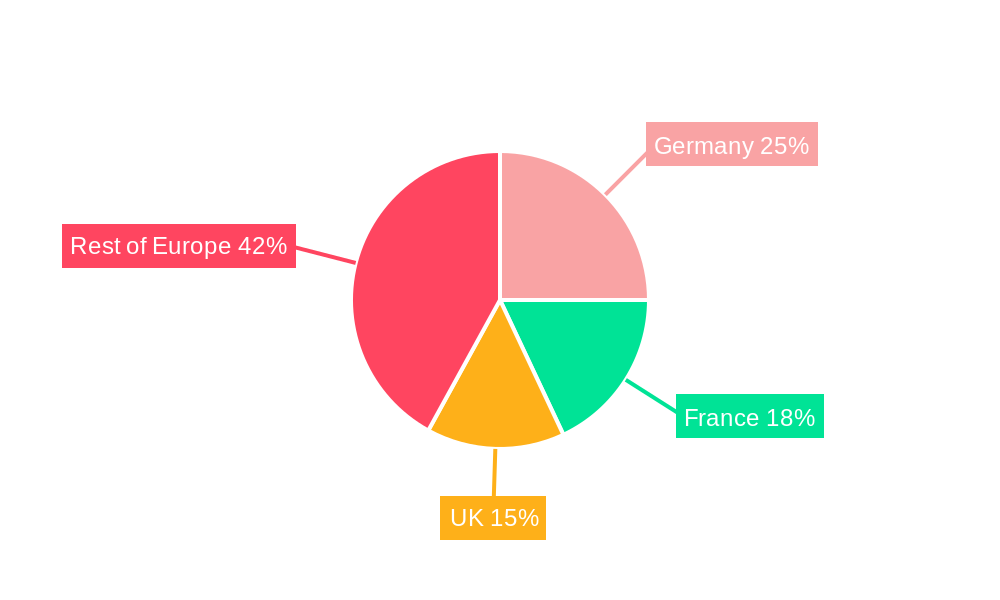

However, the market growth is not without challenges. Economic fluctuations and potential supply chain disruptions remain potential restraints. Competition among established players like Honeywell, Flowserve, Weir Group, and Xylem, alongside regional players, is also intense. The market segmentation shows a strong reliance on established valve types like ball and butterfly valves, while the “other types” segment showcases opportunities for innovation and niche product development. Within the regional breakdown, Germany, France, and the United Kingdom are expected to maintain their dominant positions, driven by their robust industrial base and infrastructure investment programs. The “Rest of Europe” segment presents a significant growth potential, driven by developing economies and increasing industrialization in these regions.

Valves Industry in Europe: A Comprehensive Market Report (2019-2033)

This insightful report provides a detailed analysis of the European valves industry, encompassing market size, trends, leading players, and future growth prospects. With a comprehensive study period spanning 2019-2033 (base year 2025, forecast period 2025-2033), this report is an indispensable resource for stakeholders seeking to navigate this dynamic sector. The report delves deep into various segments, including by type (ball, butterfly, gate/globe/check, plug, control, other), end-user industry (oil & gas, chemicals, water & wastewater, power generation, mining, others), and key European countries (United Kingdom, Germany, France, and Rest of Europe). The total market size in 2025 is estimated at €XX Million.

Valves Industry in Europe Market Composition & Trends

The European valves market exhibits a moderately concentrated landscape, with several multinational players holding significant market share. Honeywell International Inc, Flowserve Corporation, and The Weir Group PLC are among the leading players, each commanding a substantial portion of the market (exact figures are detailed within the report). Market share distribution is influenced by factors such as technological innovation, brand reputation, and strategic partnerships. The regulatory landscape, particularly concerning environmental compliance and safety standards, plays a crucial role in shaping industry practices. Substitute products, such as alternative flow control technologies, present ongoing competitive pressure. The report analyzes end-user industry profiles, revealing the dominance of the oil & gas, chemicals, and water & wastewater sectors. Furthermore, M&A activities, such as the April 2022 acquisition of Habonim by ITT Inc for USD 140 Million, significantly impact market dynamics, altering competitive landscapes and driving innovation.

- Market Concentration: Moderately concentrated, with top 5 players controlling approximately XX% of the market.

- M&A Deal Value (2019-2024): €XX Million

- Innovation Catalysts: Stringent environmental regulations, demand for improved energy efficiency, and advancements in smart valve technologies.

- Regulatory Landscape: Compliance with EU directives on industrial safety and environmental protection.

- Substitute Products: Emerging technologies in flow control, such as smart actuators and digital twin technologies.

Valves Industry in Europe Industry Evolution

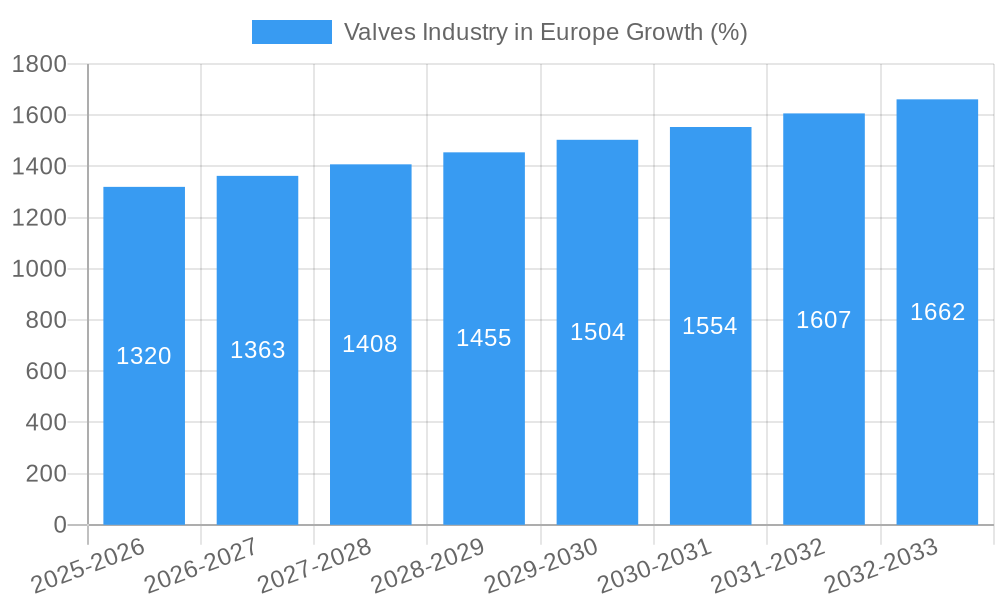

The European valves industry has experienced steady growth over the historical period (2019-2024), driven by robust demand from key end-user sectors like oil & gas and water & wastewater. The market's growth trajectory is expected to continue, albeit at a moderated pace, during the forecast period (2025-2033). Technological advancements, such as the integration of smart sensors and digital control systems, are transforming the industry. This is leading to the adoption of advanced automation and remote monitoring capabilities, which are improving operational efficiency and reducing maintenance costs. Shifting consumer demands toward energy efficiency, sustainability, and process optimization are also influencing the evolution of the market. These trends are leading to increased adoption of smart and high-performance valves across various applications. Expected CAGR from 2025 to 2033: XX%.

Leading Regions, Countries, or Segments in Valves Industry in Europe

The United Kingdom and Germany lead the European valves market, accounting for a significant share of the overall revenue. These countries benefit from established industrial bases, strong technological capabilities, and significant investments in infrastructure projects, particularly in the energy and water sectors. France follows as the third largest market. The ball, butterfly, and gate/globe/check valve segments dominate the market in terms of volume and revenue.

- Key Drivers in the UK: Strong oil & gas sector, robust infrastructure investments, and a skilled workforce.

- Key Drivers in Germany: Large industrial base, focus on automation and efficiency improvements, robust manufacturing sector.

- Key Drivers in France: Significant investments in water infrastructure, expanding chemical sector, commitment to environmental sustainability.

- Dominant Segments: Ball, Butterfly, and Gate/Globe/Check valves due to their widespread applicability across various end-user industries.

Valves Industry in Europe Product Innovations

Recent innovations focus on enhancing valve performance, reliability, and ease of maintenance. Smart valves with embedded sensors and data analytics capabilities are gaining traction, providing real-time monitoring and predictive maintenance capabilities. Advances in materials science are leading to the development of valves that can withstand harsher operating conditions and last longer. These innovations contribute to improved operational efficiency and reduced downtime in various industrial processes, driving adoption rates across different sectors.

Propelling Factors for Valves Industry in Europe Growth

Growth in the European valves industry is propelled by several factors. Firstly, increasing investments in infrastructure projects, particularly in energy and water, drive demand for advanced flow control solutions. Secondly, the growing focus on industrial automation and digitalization fuels adoption of smart valves with enhanced monitoring and control capabilities. Finally, stringent environmental regulations incentivize the use of energy-efficient valves, further bolstering market growth.

Obstacles in the Valves Industry in Europe Market

The European valves industry faces challenges such as supply chain disruptions, which can lead to increased costs and delays in project timelines. Fluctuations in raw material prices also impact production costs and profitability. Intense competition among existing players also restricts margin growth. Furthermore, compliance with evolving environmental regulations and safety standards adds to the operational costs of businesses.

Future Opportunities in Valves Industry in Europe

The valves industry in Europe presents opportunities in the adoption of smart valves and digitalization across diverse sectors. The expansion of renewable energy infrastructure opens up new growth avenues. Increased focus on sustainable manufacturing and circular economy practices also presents prospects for valves made from recycled or sustainable materials. Emerging technologies, such as 3D printing for customized valves, could offer considerable opportunities.

Major Players in the Valves Industry in Europe Ecosystem

- Honeywell International Inc

- Flowserve Corporation

- The Weir Group PLC

- Xylem Inc

- Hitachi Ltd

- Emerson Electric Co

- ITT INC

- AVK Holding A/S

- Danfoss A/S

- Schlumberger Limited

- Pentair PLC

- KITZ Corporation

Key Developments in Valves Industry in Europe Industry

- April 2022: ITT Inc acquires Habonim for USD 140 Million, expanding its ball valve offerings and strengthening its position in harsh-application markets.

Strategic Valves Industry in Europe Market Forecast

The European valves market is poised for continued growth, driven by the long-term trends of infrastructure development, industrial automation, and environmental sustainability. The adoption of smart and sustainable valve technologies will play a key role in shaping the future of the market. Significant opportunities exist for companies that can innovate, adapt to evolving regulations, and meet the increasing demand for high-performance, energy-efficient flow control solutions. The market is expected to reach €XX Million by 2033.

Valves Industry in Europe Segmentation

-

1. Type

- 1.1. Ball

- 1.2. Butterfly

- 1.3. Gate/Globe/Check

- 1.4. Plug

- 1.5. Control

- 1.6. Other Types

-

2. End-user Industry

- 2.1. Oil & Gas

- 2.2. Chemicals

- 2.3. Water & Wastewater

- 2.4. Power Generation

- 2.5. Mining

- 2.6. Other End-user Industries

Valves Industry in Europe Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Russia

- 1.7. Benelux

- 1.8. Nordics

- 1.9. Rest of Europe

Valves Industry in Europe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.40% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing emphasis on Power and Water & Wastewater in Emerging Markets; Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive

- 3.3. Market Restrains

- 3.3.1. High Cost of Microplate Systems

- 3.4. Market Trends

- 3.4.1. Control Valves to Hold a Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Ball

- 5.1.2. Butterfly

- 5.1.3. Gate/Globe/Check

- 5.1.4. Plug

- 5.1.5. Control

- 5.1.6. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Oil & Gas

- 5.2.2. Chemicals

- 5.2.3. Water & Wastewater

- 5.2.4. Power Generation

- 5.2.5. Mining

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 7. France Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 8. Italy Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Honeywell International Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Flowserve Corporation

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 The Weir Group PLC

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Xylem Inc

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Hitachi Ltd

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Emerson Electric Co

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 ITT INC

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 AVK Holding A/S

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Danfoss A/S

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Schlumberger Limited

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Pentair PLC

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 KITZ Corporation

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.1 Honeywell International Inc

List of Figures

- Figure 1: Valves Industry in Europe Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Valves Industry in Europe Share (%) by Company 2024

List of Tables

- Table 1: Valves Industry in Europe Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Valves Industry in Europe Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Valves Industry in Europe Revenue Million Forecast, by Type 2019 & 2032

- Table 4: Valves Industry in Europe Volume K Unit Forecast, by Type 2019 & 2032

- Table 5: Valves Industry in Europe Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 6: Valves Industry in Europe Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 7: Valves Industry in Europe Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Valves Industry in Europe Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: Valves Industry in Europe Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Valves Industry in Europe Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: Germany Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Germany Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 13: France Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: France Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 15: Italy Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Italy Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 17: United Kingdom Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: United Kingdom Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 19: Netherlands Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Netherlands Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: Sweden Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Sweden Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: Rest of Europe Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Rest of Europe Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 25: Valves Industry in Europe Revenue Million Forecast, by Type 2019 & 2032

- Table 26: Valves Industry in Europe Volume K Unit Forecast, by Type 2019 & 2032

- Table 27: Valves Industry in Europe Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 28: Valves Industry in Europe Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 29: Valves Industry in Europe Revenue Million Forecast, by Country 2019 & 2032

- Table 30: Valves Industry in Europe Volume K Unit Forecast, by Country 2019 & 2032

- Table 31: United Kingdom Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: United Kingdom Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 33: Germany Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Germany Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 35: France Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: France Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 37: Italy Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Italy Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 39: Spain Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Spain Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 41: Russia Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Russia Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 43: Benelux Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Benelux Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 45: Nordics Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Nordics Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 47: Rest of Europe Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Rest of Europe Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Valves Industry in Europe?

The projected CAGR is approximately 4.40%.

2. Which companies are prominent players in the Valves Industry in Europe?

Key companies in the market include Honeywell International Inc, Flowserve Corporation, The Weir Group PLC, Xylem Inc, Hitachi Ltd, Emerson Electric Co, ITT INC, AVK Holding A/S, Danfoss A/S, Schlumberger Limited, Pentair PLC, KITZ Corporation.

3. What are the main segments of the Valves Industry in Europe?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing emphasis on Power and Water & Wastewater in Emerging Markets; Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive.

6. What are the notable trends driving market growth?

Control Valves to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

High Cost of Microplate Systems.

8. Can you provide examples of recent developments in the market?

April 2022 - ITT Inc announced that the company had acquired Habonim, a provider of industrial valves and actuators, for USD 140 million. Habonim will become part of ITT's Industrial Process (IP) segment. The company's complementary ball valve offering and focus on harsh applications in attractive end-user markets will drive stronger sales growth for Industrial Process and ITT over the long term.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Valves Industry in Europe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Valves Industry in Europe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Valves Industry in Europe?

To stay informed about further developments, trends, and reports in the Valves Industry in Europe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence