Key Insights

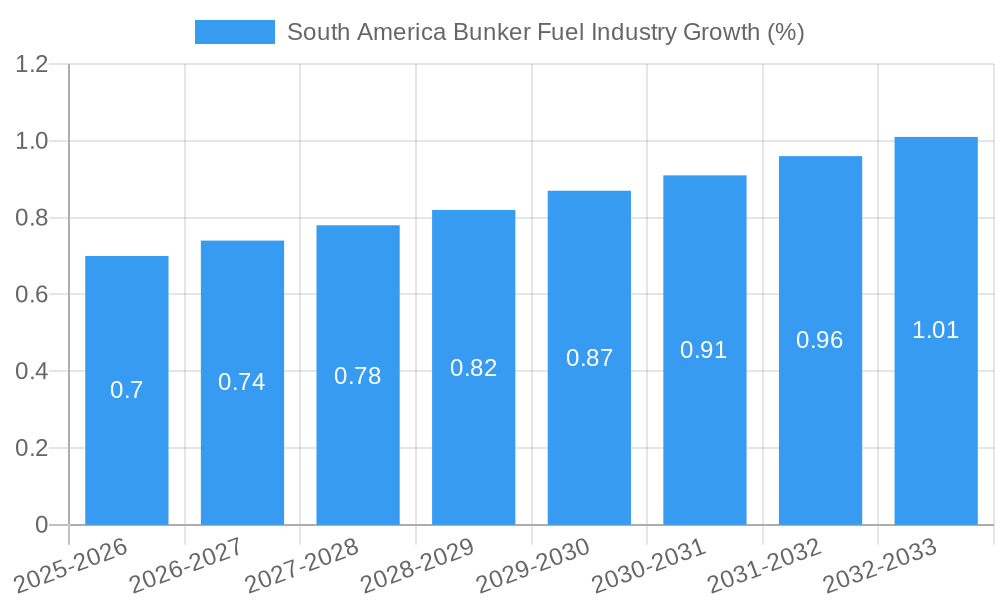

The South American bunker fuel market, valued at approximately $14.74 million in 2025, is projected to experience steady growth, driven by increasing maritime trade activity within the region and expanding economies such as Brazil and Argentina. The market's Compound Annual Growth Rate (CAGR) of 4.80% from 2025 to 2033 indicates a positive outlook, fueled by the growing demand for efficient and environmentally friendly fuel options. This growth is particularly pronounced in segments such as Very Low Sulfur Fuel Oil (VLSFO), driven by stringent environmental regulations aimed at reducing sulfur emissions. While the adoption of Liquefied Natural Gas (LNG) is still in its early stages in South America, its market share is anticipated to increase gradually as infrastructure develops and regulatory pressures intensify. The preference for VLSFO over High Sulfur Fuel Oil (HSFO) is expected to continue, although HSFO may remain relevant in specific niche applications. The container and tanker vessel segments dominate the market, reflecting the significant maritime freight transportation occurring within and through South America. Challenges include price volatility in global fuel markets and potential infrastructure limitations, particularly in the adoption of alternative fuels like LNG and biodiesel. Nevertheless, the South American bunker fuel market’s growth trajectory remains optimistic, driven by increasing cargo volumes and a supportive regulatory environment for cleaner fuel adoption.

The major players in the South American bunker fuel market include global giants like Vitol Holding BV, AP Moeller Maersk A/S, and Chevron Corporation, alongside regional suppliers. These companies strategically position themselves to capitalize on growth opportunities within the region. Competition is intense, driven by both price and service differentiation. The market's structure includes a mix of large international companies and smaller, regional suppliers, resulting in a dynamic and competitive landscape. Strategic partnerships and mergers and acquisitions can be expected as companies seek to expand their market share and optimize their supply chains. The increasing adoption of digital technologies in fuel procurement and logistics will contribute to further efficiencies and transparency within the market, benefitting both suppliers and vessel operators. This will likely lead to the rise of innovative solutions such as blockchain-based fuel traceability and automated bunker delivery systems.

South America Bunker Fuel Industry: A Comprehensive Market Report (2019-2033)

This insightful report provides a comprehensive analysis of the South America bunker fuel industry, offering crucial market intelligence for stakeholders, investors, and industry professionals. Covering the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033, this report dives deep into market dynamics, competitive landscapes, and future growth prospects. Expect detailed analysis of market size (in Millions), fuel types, vessel segments, and key players shaping this dynamic sector.

South America Bunker Fuel Industry Market Composition & Trends

This section evaluates the South American bunker fuel market's concentration, innovation drivers, regulatory environment, substitute fuels, end-user profiles, and mergers & acquisitions (M&A) activity. The market is characterized by a high level of concentration, with the top five players holding approximately xx% of the market share in 2024. This section delves into the distribution of this market share across key players and provides analysis of recent M&A deal values, totaling approximately xx Million in the last five years.

- Market Concentration: High, with top 5 players holding approximately xx% market share in 2024.

- Innovation Catalysts: Stringent environmental regulations driving demand for cleaner fuels like LNG and biofuels.

- Regulatory Landscape: Varied across South American countries, impacting fuel pricing and compliance.

- Substitute Products: LNG, methanol, LPG, and biodiesel are emerging as substitutes for traditional fuels.

- End-User Profiles: Primarily comprises container ships, tankers, bulk carriers, and general cargo vessels.

- M&A Activities: Significant consolidation expected, driven by the need for scale and access to diverse fuel sources. Recent M&A activity valued at approximately xx Million.

South America Bunker Fuel Industry Industry Evolution

This section analyzes the evolutionary trajectory of the South American bunker fuel market, highlighting growth trends, technological advancements, and evolving consumer preferences. From 2019 to 2024, the market experienced a Compound Annual Growth Rate (CAGR) of approximately xx%, driven by increasing maritime trade and stricter environmental regulations. The transition to low-sulfur fuels like VLSFO is accelerating, while the adoption of alternative fuels like LNG is steadily gaining momentum. Technological advancements in fuel efficiency and bunkering infrastructure are further shaping market dynamics. This section provides a detailed analysis of these trends, offering insights into the future growth trajectory of the sector.

Leading Regions, Countries, or Segments in South America Bunker Fuel Industry

This section identifies the dominant regions, countries, and segments within the South American bunker fuel market. Analysis considers key factors driving dominance in each segment, including investment trends and regulatory support.

Dominant Fuel Types:

- VLSFO: Growing rapidly due to stricter emission regulations. Key drivers include increasing demand from larger container vessels and regulatory pressure.

- MGO: Remains significant, especially in smaller vessels and coastal operations.

- LNG: Experiencing significant growth, fueled by environmental concerns and technological advancements in LNG bunkering infrastructure. Brazil and potentially other countries are showing promise due to new partnerships and initiatives.

- HSFO: Demand declining due to environmental regulations.

Dominant Vessel Types:

- Container Ships: Represent the largest segment due to the growth of global trade.

- Tankers: Significant segment, driven by the transportation of crude oil and refined petroleum products.

South America Bunker Fuel Industry Product Innovations

Significant innovations are shaping the South American bunker fuel market. The introduction of biofuels, the refinement of LNG bunkering technologies, and the development of more efficient fuel systems are key examples. These innovations deliver improved fuel efficiency, reduced emissions, and enhanced operational performance. The unique selling propositions of these new solutions center around environmental compliance and cost savings.

Propelling Factors for South America Bunker Fuel Industry Growth

The South American bunker fuel market’s growth is driven by several factors, including increased maritime trade, the implementation of stricter environmental regulations like IMO 2020, and investments in LNG bunkering infrastructure. Economic growth across South American nations also contributes to the market's expansion. The shift towards cleaner fuels is further accelerated by government incentives and carbon reduction targets.

Obstacles in the South America Bunker Fuel Industry Market

The South American bunker fuel market faces challenges, including inconsistent regulatory frameworks across different countries, potential supply chain disruptions, and intense competition from both established and emerging players. Volatility in fuel prices and the high upfront investment costs associated with adopting alternative fuels also pose significant barriers. These factors can cause price fluctuations and impact overall market stability.

Future Opportunities in South America Bunker Fuel Industry

Future opportunities include the expansion of LNG bunkering infrastructure, the growing adoption of alternative fuels like methanol and biofuels, and the development of innovative technologies to improve fuel efficiency and reduce emissions. The increasing focus on decarbonization presents significant opportunities for companies that can provide sustainable and environmentally friendly solutions.

Major Players in the South America Bunker Fuel Industry Ecosystem

- Vitol Holding BV

- AP Moeller Maersk A/S

- Chevron Corporation

- TotalEnergies SA

- World Fuel Services Corp

- CMA CGM Group

- Hapag-Lloyd AG

- Bunker Holding A/S

- Peninsula Petroleum Ltd

- China COSCO Holdings Company Limited

- Mediterranean Shipping Company SA

- Monjasa Holding A/S

- 6 Ocean Network Express

Key Developments in South America Bunker Fuel Industry Industry

- January 2023: Petrobras conducts Brazil's first bunker delivery with renewable content.

- November 2022: Nimofast Brasil SA partners with KanferShipping AS to provide LNG bunkering solutions in Brazil.

- October 2022: Trinidad and Tobago's NGC begins designing a small-scale LNG hub.

Strategic South America Bunker Fuel Industry Market Forecast

The South American bunker fuel market is poised for significant growth over the next decade, driven by increasing maritime activity, the adoption of cleaner fuels, and supportive government policies. The transition to low-carbon fuels will present substantial opportunities for innovative companies, while market consolidation among major players is expected to continue. The market is anticipated to reach approximately xx Million by 2033.

South America Bunker Fuel Industry Segmentation

-

1. Fuel Type

- 1.1. High Sulfur Fuel Oil (HSFO)

- 1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 1.3. Marine Gas Oil (MGO)

- 1.4. Liquefied Natural Gas (LNG)

- 1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

-

2. Vessel Type

- 2.1. Containers

- 2.2. Tankers

- 2.3. General Cargo

- 2.4. Bulk Container

- 2.5. Other Vessel Types

-

3. Geography

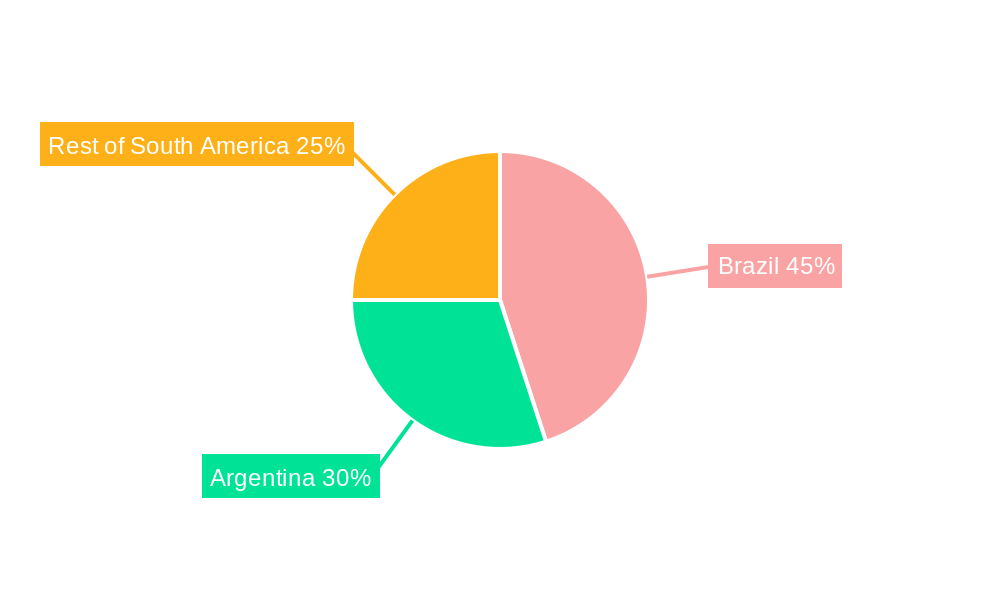

- 3.1. Brazil

- 3.2. Chile

- 3.3. Argentina

- 3.4. Rest of South America

South America Bunker Fuel Industry Segmentation By Geography

- 1. Brazil

- 2. Chile

- 3. Argentina

- 4. Rest of South America

South America Bunker Fuel Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.80% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Rising Marine Transportation of Essential Commodities in South America4.; Supportive Policies for Cleaner Bunker Fuel

- 3.3. Market Restrains

- 3.3.1. 4.; Volatile Nature of Oil Market

- 3.4. Market Trends

- 3.4.1. Very Low Sulfur Fuel Oil (VLSFO) to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. South America Bunker Fuel Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. High Sulfur Fuel Oil (HSFO)

- 5.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 5.1.3. Marine Gas Oil (MGO)

- 5.1.4. Liquefied Natural Gas (LNG)

- 5.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 5.2. Market Analysis, Insights and Forecast - by Vessel Type

- 5.2.1. Containers

- 5.2.2. Tankers

- 5.2.3. General Cargo

- 5.2.4. Bulk Container

- 5.2.5. Other Vessel Types

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Chile

- 5.3.3. Argentina

- 5.3.4. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Chile

- 5.4.3. Argentina

- 5.4.4. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. Brazil South America Bunker Fuel Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. High Sulfur Fuel Oil (HSFO)

- 6.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 6.1.3. Marine Gas Oil (MGO)

- 6.1.4. Liquefied Natural Gas (LNG)

- 6.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 6.2. Market Analysis, Insights and Forecast - by Vessel Type

- 6.2.1. Containers

- 6.2.2. Tankers

- 6.2.3. General Cargo

- 6.2.4. Bulk Container

- 6.2.5. Other Vessel Types

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Chile

- 6.3.3. Argentina

- 6.3.4. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. Chile South America Bunker Fuel Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7.1.1. High Sulfur Fuel Oil (HSFO)

- 7.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 7.1.3. Marine Gas Oil (MGO)

- 7.1.4. Liquefied Natural Gas (LNG)

- 7.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 7.2. Market Analysis, Insights and Forecast - by Vessel Type

- 7.2.1. Containers

- 7.2.2. Tankers

- 7.2.3. General Cargo

- 7.2.4. Bulk Container

- 7.2.5. Other Vessel Types

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Chile

- 7.3.3. Argentina

- 7.3.4. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8. Argentina South America Bunker Fuel Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8.1.1. High Sulfur Fuel Oil (HSFO)

- 8.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 8.1.3. Marine Gas Oil (MGO)

- 8.1.4. Liquefied Natural Gas (LNG)

- 8.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 8.2. Market Analysis, Insights and Forecast - by Vessel Type

- 8.2.1. Containers

- 8.2.2. Tankers

- 8.2.3. General Cargo

- 8.2.4. Bulk Container

- 8.2.5. Other Vessel Types

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Chile

- 8.3.3. Argentina

- 8.3.4. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9. Rest of South America South America Bunker Fuel Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9.1.1. High Sulfur Fuel Oil (HSFO)

- 9.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 9.1.3. Marine Gas Oil (MGO)

- 9.1.4. Liquefied Natural Gas (LNG)

- 9.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 9.2. Market Analysis, Insights and Forecast - by Vessel Type

- 9.2.1. Containers

- 9.2.2. Tankers

- 9.2.3. General Cargo

- 9.2.4. Bulk Container

- 9.2.5. Other Vessel Types

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Brazil

- 9.3.2. Chile

- 9.3.3. Argentina

- 9.3.4. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10. Brazil South America Bunker Fuel Industry Analysis, Insights and Forecast, 2019-2031

- 11. Argentina South America Bunker Fuel Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of South America South America Bunker Fuel Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 6 Ocean Network Express*List Not Exhaustive 6 4 Market Ranking/Share (%) Analysi

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 7 Chevron Corporation

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 2 Monjasa Holding A/S

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 1 Vitol Holding BV

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 1 AP Moeller Maersk A/S

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 3 China COSCO Holdings Company Limited

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 2 Mediterranean Shipping Company SA

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Ship Owners

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Fuel Suppliers

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 6 TotalEnergies SA

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 4 World Fuel Services Corp

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 4 CMA CGM Group

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 5 Peninsula Petroleum Ltd

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 3 Bunker Holding A/S

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.15 5 Hapag-Lloyd AG

- 13.2.15.1. Overview

- 13.2.15.2. Products

- 13.2.15.3. SWOT Analysis

- 13.2.15.4. Recent Developments

- 13.2.15.5. Financials (Based on Availability)

- 13.2.1 6 Ocean Network Express*List Not Exhaustive 6 4 Market Ranking/Share (%) Analysi

List of Figures

- Figure 1: South America Bunker Fuel Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: South America Bunker Fuel Industry Share (%) by Company 2024

List of Tables

- Table 1: South America Bunker Fuel Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Region 2019 & 2032

- Table 3: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 4: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2019 & 2032

- Table 5: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2019 & 2032

- Table 6: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2019 & 2032

- Table 7: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 8: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2019 & 2032

- Table 9: South America Bunker Fuel Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Region 2019 & 2032

- Table 11: South America Bunker Fuel Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2019 & 2032

- Table 13: Brazil South America Bunker Fuel Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Brazil South America Bunker Fuel Industry Volume (metric tonnes) Forecast, by Application 2019 & 2032

- Table 15: Argentina South America Bunker Fuel Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Argentina South America Bunker Fuel Industry Volume (metric tonnes) Forecast, by Application 2019 & 2032

- Table 17: Rest of South America South America Bunker Fuel Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Rest of South America South America Bunker Fuel Industry Volume (metric tonnes) Forecast, by Application 2019 & 2032

- Table 19: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 20: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2019 & 2032

- Table 21: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2019 & 2032

- Table 22: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2019 & 2032

- Table 23: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 24: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2019 & 2032

- Table 25: South America Bunker Fuel Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 26: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2019 & 2032

- Table 27: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 28: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2019 & 2032

- Table 29: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2019 & 2032

- Table 30: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2019 & 2032

- Table 31: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 32: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2019 & 2032

- Table 33: South America Bunker Fuel Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2019 & 2032

- Table 35: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 36: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2019 & 2032

- Table 37: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2019 & 2032

- Table 38: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2019 & 2032

- Table 39: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 40: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2019 & 2032

- Table 41: South America Bunker Fuel Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2019 & 2032

- Table 43: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 44: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2019 & 2032

- Table 45: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2019 & 2032

- Table 46: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2019 & 2032

- Table 47: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 48: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2019 & 2032

- Table 49: South America Bunker Fuel Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 50: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Bunker Fuel Industry?

The projected CAGR is approximately 4.80%.

2. Which companies are prominent players in the South America Bunker Fuel Industry?

Key companies in the market include 6 Ocean Network Express*List Not Exhaustive 6 4 Market Ranking/Share (%) Analysi, 7 Chevron Corporation, 2 Monjasa Holding A/S, 1 Vitol Holding BV, 1 AP Moeller Maersk A/S, 3 China COSCO Holdings Company Limited, 2 Mediterranean Shipping Company SA, Ship Owners, Fuel Suppliers, 6 TotalEnergies SA, 4 World Fuel Services Corp, 4 CMA CGM Group, 5 Peninsula Petroleum Ltd, 3 Bunker Holding A/S, 5 Hapag-Lloyd AG.

3. What are the main segments of the South America Bunker Fuel Industry?

The market segments include Fuel Type, Vessel Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.74 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Rising Marine Transportation of Essential Commodities in South America4.; Supportive Policies for Cleaner Bunker Fuel.

6. What are the notable trends driving market growth?

Very Low Sulfur Fuel Oil (VLSFO) to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Volatile Nature of Oil Market.

8. Can you provide examples of recent developments in the market?

In January 2023, Brazilian state-controlled oil and gas producer Petrobras carried out the country's first bunker delivery with renewable content at the Rio Grande Terminal (Terig) in Rio Grande do Sul.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in metric tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Bunker Fuel Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Bunker Fuel Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Bunker Fuel Industry?

To stay informed about further developments, trends, and reports in the South America Bunker Fuel Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence