Key Insights

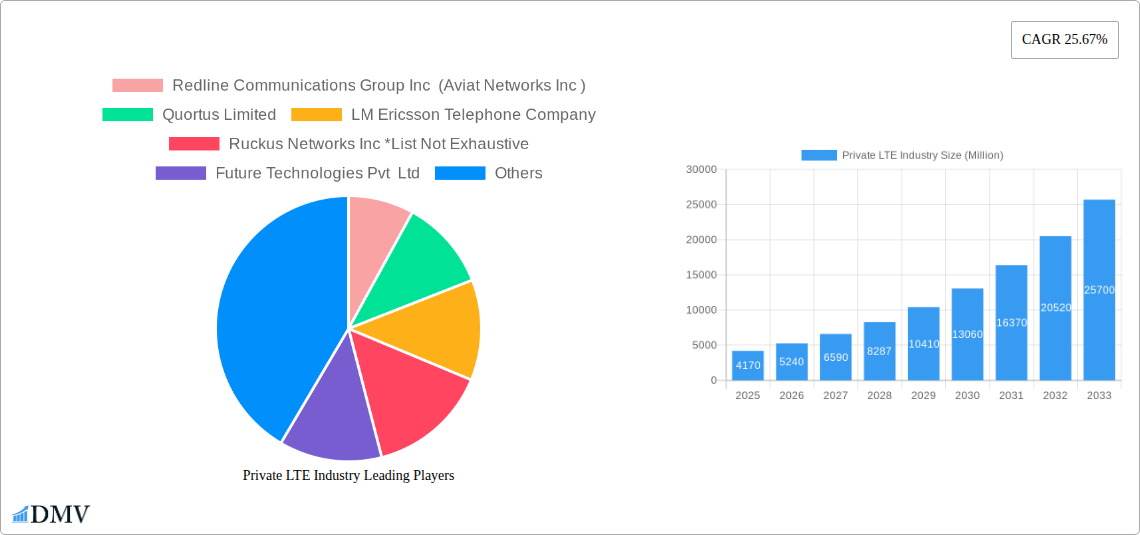

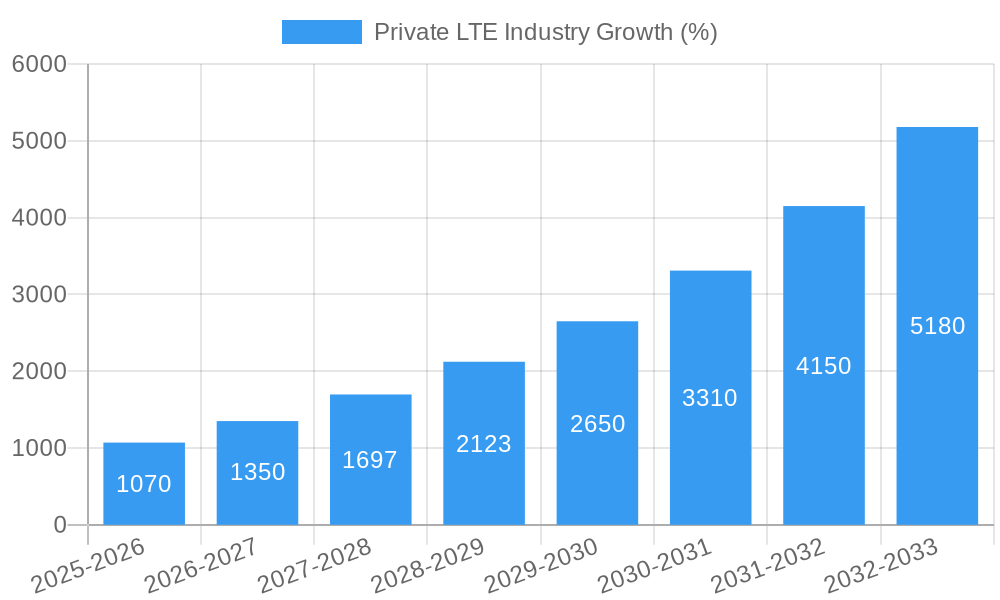

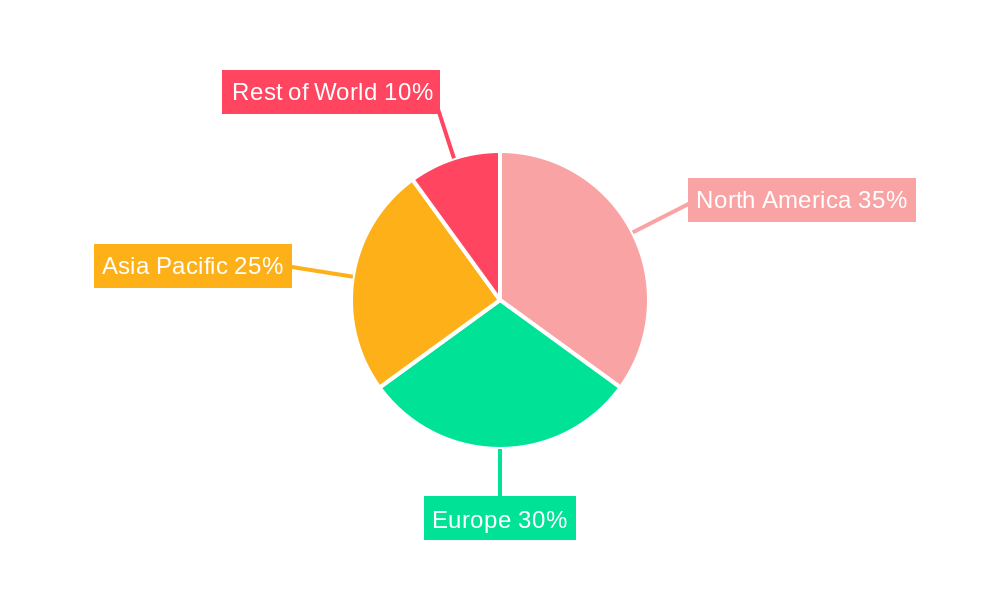

The Private LTE market is experiencing robust growth, projected to reach \$4.17 billion in 2025 and exhibiting a Compound Annual Growth Rate (CAGR) of 25.67% from 2025 to 2033. This expansion is fueled by several key drivers. The increasing demand for secure, reliable, and high-bandwidth communication in various sectors, such as industrial automation (particularly in manufacturing, public safety, and utilities), healthcare (remote patient monitoring, telehealth), and enterprise applications (improved internal communications and IoT deployments), is a major catalyst. Furthermore, the maturation of 5G technology and its integration with Private LTE networks offer enhanced capabilities and scalability, driving adoption. The transition towards Industry 4.0 and the burgeoning Internet of Things (IoT) are also significantly contributing factors, as Private LTE networks provide the necessary infrastructure for seamless connectivity and data management in these evolving environments. While regulatory hurdles and the initial investment costs associated with deploying Private LTE infrastructure might pose some challenges, the long-term benefits in terms of efficiency, security, and operational control outweigh these concerns for many organizations. The market is segmented by end-user industry, component (infrastructure and services), technology (FDD and TDD), deployment (centralized and distributed), and frequency band (licensed, unlicensed, and shared spectrum). Competition is intense, with established players like Ericsson, Nokia, and Huawei alongside emerging innovative companies vying for market share. The geographic distribution shows a strong presence across North America, Europe, and Asia Pacific, with China, the US, and several European countries leading the adoption.

The forecast period (2025-2033) anticipates sustained high growth, primarily driven by ongoing digital transformation initiatives across industries and increasing adoption of IoT devices requiring reliable and secure connectivity. The market's evolution will be shaped by continuous technological advancements, such as the integration of edge computing and AI capabilities within Private LTE networks, leading to improved performance and more sophisticated applications. Furthermore, the development of more cost-effective solutions and streamlined deployment processes will likely accelerate adoption among smaller businesses and organizations. The emergence of new frequency bands and spectrum sharing initiatives could also significantly influence market dynamics, enhancing network capacity and enabling broader deployment across diverse locations. Strategic partnerships and mergers and acquisitions are expected to play a significant role in shaping the competitive landscape in the years to come.

Private LTE Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Private LTE industry, projecting a market valuation exceeding $XX Million by 2033. It offers crucial insights for stakeholders, investors, and industry professionals seeking to navigate this rapidly evolving landscape. The report covers market composition, technological advancements, leading players, and future opportunities, employing rigorous data analysis based on the historical period (2019-2024), base year (2025), and forecast period (2025-2033).

Private LTE Industry Market Composition & Trends

This section evaluates the competitive landscape, highlighting market concentration, innovation drivers, regulatory frameworks, and the impact of mergers and acquisitions (M&A) on the Private LTE market. We analyze market share distribution among key players, including Redline Communications Group Inc (Aviat Networks Inc), Quortus Limited, LM Ericsson Telephone Company, Ruckus Networks Inc, Future Technologies Pvt Ltd, Qualcomm Technologies Inc, NEC Corporation, Huawei Technologies Co Ltd, Nokia Corporation, Sierra Wireless Inc, and Luminate Wireless Inc. (List not exhaustive). The report also examines the influence of substitute technologies and evolving end-user profiles across diverse sectors.

- Market Concentration: The Private LTE market exhibits a [Describe level of concentration: e.g., moderately concentrated] structure with the top 5 players holding an estimated [XX]% market share in 2025.

- Innovation Catalysts: Advancements in 5G technology, IoT integration, and edge computing are driving significant innovation.

- Regulatory Landscape: Varying regulatory environments across different regions impact deployment strategies and market growth.

- M&A Activity: Significant M&A activity, exemplified by Vocus’s USD 1 Billion acquisition of Challenge Networks (Feb 2023), reshapes the competitive landscape and expands service offerings. The total value of M&A deals in the period 2019-2024 is estimated at $XX Million.

- End-User Profiles: The report details end-user trends across Industrial (Public Safety, Supply Chain Management, Utilities, Manufacturing), Healthcare, Enterprise, and Other End-user Industries, providing granular insights into sector-specific demands.

Private LTE Industry Industry Evolution

This section analyzes the growth trajectory of the Private LTE industry, examining technological advancements and evolving consumer demands from 2019 to 2033. We explore the impact of technological innovations like FDD and TDD, centralized and distributed deployments, and the utilization of licensed, unlicensed, and shared spectrum frequencies. The market is projected to grow at a CAGR of [XX]% during the forecast period (2025-2033), driven by increased adoption across various sectors. Specific data points on growth rates and adoption metrics are provided for each segment. The partnership between NTT Ltd. and Albemarle Corporation (May 2022) exemplifies the growing adoption of private LTE/5G networks in demanding industrial settings. This showcases a rising trend of leveraging private networks for enhanced operational efficiency, security, and data control. Further, the report delves into the shift towards [mention specific shift in consumer demand, e.g., cloud-based solutions, enhanced security features].

Leading Regions, Countries, or Segments in Private LTE Industry

This section identifies the leading regions, countries, and segments within the Private LTE market, providing a detailed analysis of their dominance factors.

- By End-user Industry: The Industrial sector, particularly within Public Safety and Manufacturing, is projected to be the leading segment due to [explain reasons, e.g., high demand for reliable, secure communication].

- By Component: The Infrastructure segment dominates due to [explain reasons, e.g., significant upfront investments in network deployment].

- By Technology: [Identify leading technology: e.g., TDD] is experiencing faster growth due to [explain reasons, e.g., superior performance in specific applications].

- By Deployment: [Identify leading deployment type: e.g., Distributed] deployments are preferred due to [explain reasons, e.g., greater flexibility and scalability].

- By Frequency Band: Licensed spectrum remains the dominant frequency band due to [explain reasons, e.g., guaranteed bandwidth and reliability], although the use of shared spectrum is increasing.

Key Drivers: High investments in digital infrastructure, supportive government regulations, and the growing demand for secure and reliable communication networks fuel the growth of the dominant segments.

Private LTE Industry Product Innovations

Recent product innovations focus on enhancing network performance, security, and integration with other technologies. Key advancements include improved spectrum efficiency, the introduction of software-defined networking (SDN) capabilities for greater flexibility and manageability, and seamless integration with IoT devices and cloud platforms. These innovations offer unique selling propositions such as improved reliability, reduced latency, and increased security, catering to the specific needs of various vertical markets.

Propelling Factors for Private LTE Industry Growth

Technological advancements (e.g., 5G and edge computing), increasing demand for secure and reliable communication in critical infrastructure (e.g., smart cities, industrial automation), and favorable government regulations promoting private network deployments are key growth drivers. The expanding adoption of IoT devices across various sectors further fuels market expansion.

Obstacles in the Private LTE Industry Market

High initial investment costs, the complexity of network deployment and management, and potential regulatory hurdles in certain regions pose significant challenges to market growth. Supply chain disruptions and intense competition among major vendors also impact market dynamics. These factors can lead to project delays and increased costs.

Future Opportunities in Private LTE Industry

The integration of private LTE with other technologies like 5G and IoT presents significant future opportunities. The expansion into new markets, particularly in developing economies with rapidly growing infrastructure needs, offers substantial potential. Moreover, the development of innovative applications in sectors such as healthcare, transportation, and energy promises further market expansion.

Major Players in the Private LTE Industry Ecosystem

- Redline Communications Group Inc (Aviat Networks Inc)

- Quortus Limited

- LM Ericsson Telephone Company

- Ruckus Networks Inc

- Future Technologies Pvt Ltd

- Qualcomm Technologies Inc

- NEC Corporation

- Huawei Technologies Co Ltd

- Nokia Corporation

- Sierra Wireless Inc

- Luminate Wireless Inc

Key Developments in Private LTE Industry Industry

- February 2023: Vocus acquires Challenge Networks, expanding its service portfolio and completing a USD 1 Billion investment strategy focused on fiber and wireless infrastructure. This signifies a significant move towards integrated network solutions.

- May 2022: NTT Ltd. partners with Albemarle Corporation to deploy a private LTE/5G and Wi-Fi network at a lithium mine, showcasing the growing adoption of private networks in resource-intensive industries for remote operations and improved efficiency.

Strategic Private LTE Industry Market Forecast

The Private LTE market is poised for significant growth, driven by technological advancements, increasing demand across various sectors, and favorable regulatory policies. Continued innovation, particularly in areas such as 5G integration and improved security features, will fuel market expansion. The substantial investment in digital infrastructure globally further strengthens the long-term growth outlook for the Private LTE industry. The market is projected to reach $XX Million by 2033, presenting substantial opportunities for key players and new entrants.

Private LTE Industry Segmentation

-

1. Component

- 1.1. Infrastructure

- 1.2. Services

-

2. Technology

- 2.1. Frequency-Division Duplexing (FDD)

- 2.2. Time Division Duplex (TDD)

-

3. Deployment

- 3.1. Centralized

- 3.2. Distributed

-

4. Frequency Band

- 4.1. Licensed

- 4.2. Unlicensed

- 4.3. Shared Spectrum

-

5. End-user Industry

- 5.1. Industri

- 5.2. Healthcare

- 5.3. Enterprise

- 5.4. Other End-user Industries

Private LTE Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

- 4. Rest of the world

Private LTE Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 25.67% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Adoption of Isolated Systems; Growing Adoption of Smartphones

- 3.3. Market Restrains

- 3.3.1. Dearth of Skillful Workforce to Add New Solutions in Existing Network

- 3.4. Market Trends

- 3.4.1. Growing Adoption of Smartphones may Drive the Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Private LTE Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Infrastructure

- 5.1.2. Services

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Frequency-Division Duplexing (FDD)

- 5.2.2. Time Division Duplex (TDD)

- 5.3. Market Analysis, Insights and Forecast - by Deployment

- 5.3.1. Centralized

- 5.3.2. Distributed

- 5.4. Market Analysis, Insights and Forecast - by Frequency Band

- 5.4.1. Licensed

- 5.4.2. Unlicensed

- 5.4.3. Shared Spectrum

- 5.5. Market Analysis, Insights and Forecast - by End-user Industry

- 5.5.1. Industri

- 5.5.2. Healthcare

- 5.5.3. Enterprise

- 5.5.4. Other End-user Industries

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. Europe

- 5.6.3. Asia Pacific

- 5.6.4. Rest of the world

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. North America Private LTE Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Infrastructure

- 6.1.2. Services

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Frequency-Division Duplexing (FDD)

- 6.2.2. Time Division Duplex (TDD)

- 6.3. Market Analysis, Insights and Forecast - by Deployment

- 6.3.1. Centralized

- 6.3.2. Distributed

- 6.4. Market Analysis, Insights and Forecast - by Frequency Band

- 6.4.1. Licensed

- 6.4.2. Unlicensed

- 6.4.3. Shared Spectrum

- 6.5. Market Analysis, Insights and Forecast - by End-user Industry

- 6.5.1. Industri

- 6.5.2. Healthcare

- 6.5.3. Enterprise

- 6.5.4. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Europe Private LTE Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Infrastructure

- 7.1.2. Services

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Frequency-Division Duplexing (FDD)

- 7.2.2. Time Division Duplex (TDD)

- 7.3. Market Analysis, Insights and Forecast - by Deployment

- 7.3.1. Centralized

- 7.3.2. Distributed

- 7.4. Market Analysis, Insights and Forecast - by Frequency Band

- 7.4.1. Licensed

- 7.4.2. Unlicensed

- 7.4.3. Shared Spectrum

- 7.5. Market Analysis, Insights and Forecast - by End-user Industry

- 7.5.1. Industri

- 7.5.2. Healthcare

- 7.5.3. Enterprise

- 7.5.4. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Asia Pacific Private LTE Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Infrastructure

- 8.1.2. Services

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Frequency-Division Duplexing (FDD)

- 8.2.2. Time Division Duplex (TDD)

- 8.3. Market Analysis, Insights and Forecast - by Deployment

- 8.3.1. Centralized

- 8.3.2. Distributed

- 8.4. Market Analysis, Insights and Forecast - by Frequency Band

- 8.4.1. Licensed

- 8.4.2. Unlicensed

- 8.4.3. Shared Spectrum

- 8.5. Market Analysis, Insights and Forecast - by End-user Industry

- 8.5.1. Industri

- 8.5.2. Healthcare

- 8.5.3. Enterprise

- 8.5.4. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Rest of the world Private LTE Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Infrastructure

- 9.1.2. Services

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Frequency-Division Duplexing (FDD)

- 9.2.2. Time Division Duplex (TDD)

- 9.3. Market Analysis, Insights and Forecast - by Deployment

- 9.3.1. Centralized

- 9.3.2. Distributed

- 9.4. Market Analysis, Insights and Forecast - by Frequency Band

- 9.4.1. Licensed

- 9.4.2. Unlicensed

- 9.4.3. Shared Spectrum

- 9.5. Market Analysis, Insights and Forecast - by End-user Industry

- 9.5.1. Industri

- 9.5.2. Healthcare

- 9.5.3. Enterprise

- 9.5.4. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. North America Private LTE Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1 United States

- 10.1.2 Canada

- 11. Europe Private LTE Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 Germany

- 11.1.2 United Kingdom

- 11.1.3 France

- 11.1.4 Rest of Europe

- 12. Asia Pacific Private LTE Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 China

- 12.1.2 Japan

- 12.1.3 India

- 12.1.4 Rest of Asia Pacific

- 13. Rest of the world Private LTE Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Competitive Analysis

- 14.1. Global Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 Redline Communications Group Inc (Aviat Networks Inc )

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Quortus Limited

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 LM Ericsson Telephone Company

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 Ruckus Networks Inc *List Not Exhaustive

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Future Technologies Pvt Ltd

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Qualcomm Technologies Inc

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 NEC Corporation

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 Huawei Technologies Co Ltd

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Nokia Corporation

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 Sierra Wireless Inc

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.11 Luminate Wireless Inc

- 14.2.11.1. Overview

- 14.2.11.2. Products

- 14.2.11.3. SWOT Analysis

- 14.2.11.4. Recent Developments

- 14.2.11.5. Financials (Based on Availability)

- 14.2.1 Redline Communications Group Inc (Aviat Networks Inc )

List of Figures

- Figure 1: Global Private LTE Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Private LTE Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Private LTE Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Private LTE Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Private LTE Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Private LTE Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Private LTE Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Rest of the world Private LTE Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Rest of the world Private LTE Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: North America Private LTE Industry Revenue (Million), by Component 2024 & 2032

- Figure 11: North America Private LTE Industry Revenue Share (%), by Component 2024 & 2032

- Figure 12: North America Private LTE Industry Revenue (Million), by Technology 2024 & 2032

- Figure 13: North America Private LTE Industry Revenue Share (%), by Technology 2024 & 2032

- Figure 14: North America Private LTE Industry Revenue (Million), by Deployment 2024 & 2032

- Figure 15: North America Private LTE Industry Revenue Share (%), by Deployment 2024 & 2032

- Figure 16: North America Private LTE Industry Revenue (Million), by Frequency Band 2024 & 2032

- Figure 17: North America Private LTE Industry Revenue Share (%), by Frequency Band 2024 & 2032

- Figure 18: North America Private LTE Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 19: North America Private LTE Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 20: North America Private LTE Industry Revenue (Million), by Country 2024 & 2032

- Figure 21: North America Private LTE Industry Revenue Share (%), by Country 2024 & 2032

- Figure 22: Europe Private LTE Industry Revenue (Million), by Component 2024 & 2032

- Figure 23: Europe Private LTE Industry Revenue Share (%), by Component 2024 & 2032

- Figure 24: Europe Private LTE Industry Revenue (Million), by Technology 2024 & 2032

- Figure 25: Europe Private LTE Industry Revenue Share (%), by Technology 2024 & 2032

- Figure 26: Europe Private LTE Industry Revenue (Million), by Deployment 2024 & 2032

- Figure 27: Europe Private LTE Industry Revenue Share (%), by Deployment 2024 & 2032

- Figure 28: Europe Private LTE Industry Revenue (Million), by Frequency Band 2024 & 2032

- Figure 29: Europe Private LTE Industry Revenue Share (%), by Frequency Band 2024 & 2032

- Figure 30: Europe Private LTE Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 31: Europe Private LTE Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 32: Europe Private LTE Industry Revenue (Million), by Country 2024 & 2032

- Figure 33: Europe Private LTE Industry Revenue Share (%), by Country 2024 & 2032

- Figure 34: Asia Pacific Private LTE Industry Revenue (Million), by Component 2024 & 2032

- Figure 35: Asia Pacific Private LTE Industry Revenue Share (%), by Component 2024 & 2032

- Figure 36: Asia Pacific Private LTE Industry Revenue (Million), by Technology 2024 & 2032

- Figure 37: Asia Pacific Private LTE Industry Revenue Share (%), by Technology 2024 & 2032

- Figure 38: Asia Pacific Private LTE Industry Revenue (Million), by Deployment 2024 & 2032

- Figure 39: Asia Pacific Private LTE Industry Revenue Share (%), by Deployment 2024 & 2032

- Figure 40: Asia Pacific Private LTE Industry Revenue (Million), by Frequency Band 2024 & 2032

- Figure 41: Asia Pacific Private LTE Industry Revenue Share (%), by Frequency Band 2024 & 2032

- Figure 42: Asia Pacific Private LTE Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 43: Asia Pacific Private LTE Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 44: Asia Pacific Private LTE Industry Revenue (Million), by Country 2024 & 2032

- Figure 45: Asia Pacific Private LTE Industry Revenue Share (%), by Country 2024 & 2032

- Figure 46: Rest of the world Private LTE Industry Revenue (Million), by Component 2024 & 2032

- Figure 47: Rest of the world Private LTE Industry Revenue Share (%), by Component 2024 & 2032

- Figure 48: Rest of the world Private LTE Industry Revenue (Million), by Technology 2024 & 2032

- Figure 49: Rest of the world Private LTE Industry Revenue Share (%), by Technology 2024 & 2032

- Figure 50: Rest of the world Private LTE Industry Revenue (Million), by Deployment 2024 & 2032

- Figure 51: Rest of the world Private LTE Industry Revenue Share (%), by Deployment 2024 & 2032

- Figure 52: Rest of the world Private LTE Industry Revenue (Million), by Frequency Band 2024 & 2032

- Figure 53: Rest of the world Private LTE Industry Revenue Share (%), by Frequency Band 2024 & 2032

- Figure 54: Rest of the world Private LTE Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 55: Rest of the world Private LTE Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 56: Rest of the world Private LTE Industry Revenue (Million), by Country 2024 & 2032

- Figure 57: Rest of the world Private LTE Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Private LTE Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Private LTE Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 3: Global Private LTE Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 4: Global Private LTE Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 5: Global Private LTE Industry Revenue Million Forecast, by Frequency Band 2019 & 2032

- Table 6: Global Private LTE Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 7: Global Private LTE Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Global Private LTE Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: United States Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Canada Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Private LTE Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Germany Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: United Kingdom Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: France Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Europe Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Private LTE Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: China Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Japan Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: India Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of Asia Pacific Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Global Private LTE Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global Private LTE Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 24: Global Private LTE Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 25: Global Private LTE Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 26: Global Private LTE Industry Revenue Million Forecast, by Frequency Band 2019 & 2032

- Table 27: Global Private LTE Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 28: Global Private LTE Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 29: United States Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Canada Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global Private LTE Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 32: Global Private LTE Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 33: Global Private LTE Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 34: Global Private LTE Industry Revenue Million Forecast, by Frequency Band 2019 & 2032

- Table 35: Global Private LTE Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 36: Global Private LTE Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 37: Germany Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: United Kingdom Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: France Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Rest of Europe Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Global Private LTE Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 42: Global Private LTE Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 43: Global Private LTE Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 44: Global Private LTE Industry Revenue Million Forecast, by Frequency Band 2019 & 2032

- Table 45: Global Private LTE Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 46: Global Private LTE Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 47: China Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Japan Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: India Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Rest of Asia Pacific Private LTE Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: Global Private LTE Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 52: Global Private LTE Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 53: Global Private LTE Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 54: Global Private LTE Industry Revenue Million Forecast, by Frequency Band 2019 & 2032

- Table 55: Global Private LTE Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 56: Global Private LTE Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Private LTE Industry?

The projected CAGR is approximately 25.67%.

2. Which companies are prominent players in the Private LTE Industry?

Key companies in the market include Redline Communications Group Inc (Aviat Networks Inc ), Quortus Limited, LM Ericsson Telephone Company, Ruckus Networks Inc *List Not Exhaustive, Future Technologies Pvt Ltd, Qualcomm Technologies Inc, NEC Corporation, Huawei Technologies Co Ltd, Nokia Corporation, Sierra Wireless Inc, Luminate Wireless Inc.

3. What are the main segments of the Private LTE Industry?

The market segments include Component, Technology, Deployment, Frequency Band, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.17 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Isolated Systems; Growing Adoption of Smartphones.

6. What are the notable trends driving market growth?

Growing Adoption of Smartphones may Drive the Market Growth.

7. Are there any restraints impacting market growth?

Dearth of Skillful Workforce to Add New Solutions in Existing Network.

8. Can you provide examples of recent developments in the market?

February 2023: Vocus, a fiber and network solutions provider, signed to acquire Challenge Networks, an Australian provider of telecommunications services. The addition of wireless network capability completes Vocus' USD 1 billion investment strategy, which also includes the deployment of significant new fiber infrastructure, including the Horizon and Highclere projects in the northwest of Australia, as well as capacity upgrades to the company's current network.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Private LTE Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Private LTE Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Private LTE Industry?

To stay informed about further developments, trends, and reports in the Private LTE Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence