Key Insights

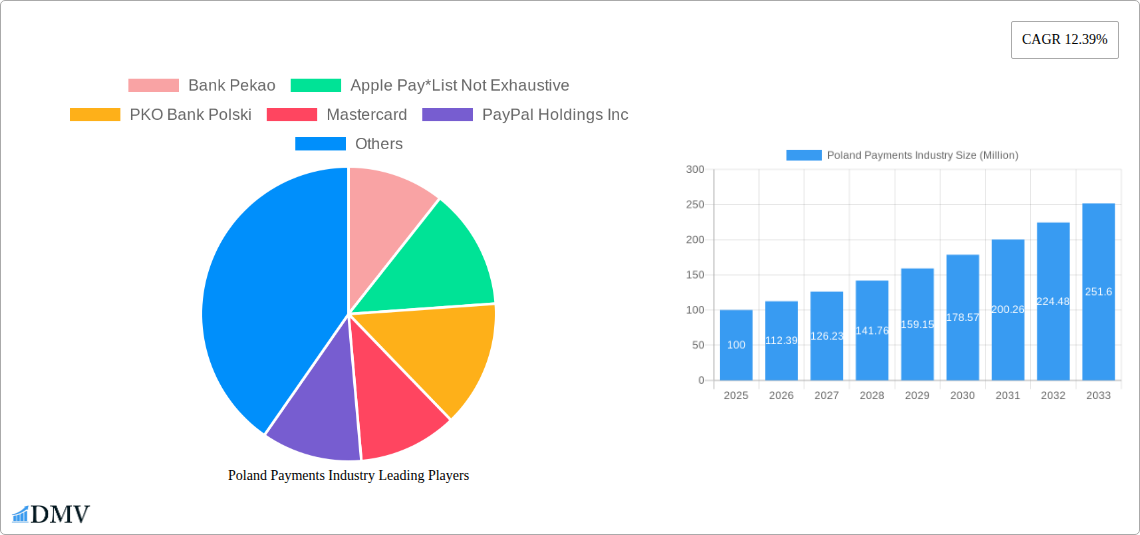

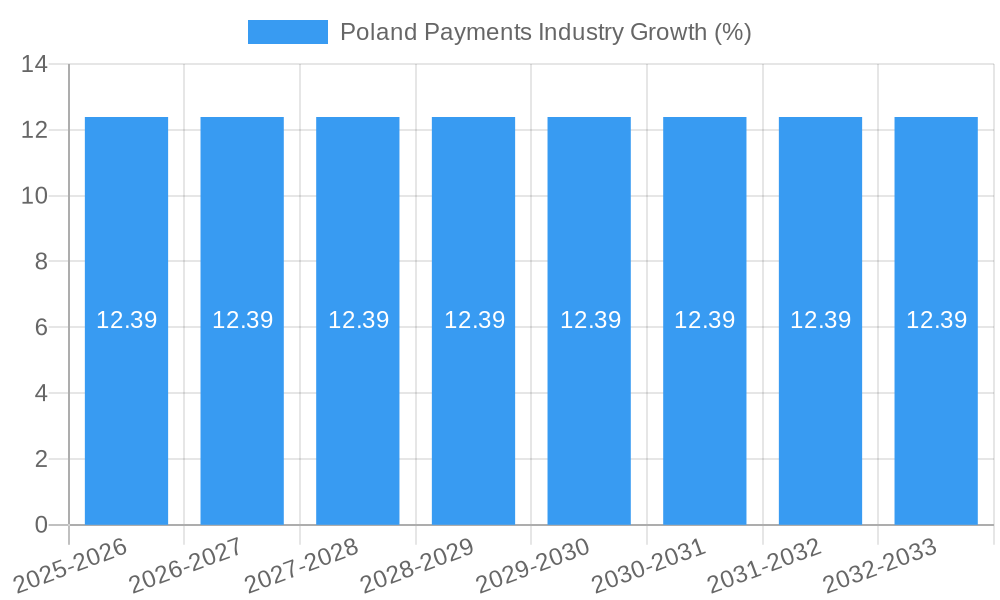

The Polish payments industry is experiencing robust growth, fueled by increasing digital adoption and a thriving e-commerce sector. With a Compound Annual Growth Rate (CAGR) of 12.39% from 2019 to 2024, the market demonstrates significant potential. The shift towards digital payments is a key driver, particularly in the retail and e-commerce segments. The rising popularity of mobile payment solutions like Apple Pay, coupled with the expansion of online banking services offered by institutions like Bank Pekao and PKO Bank Polski, are contributing significantly to this growth. Furthermore, the increasing penetration of smartphones and internet access within Poland is further accelerating the transition from traditional cash-based transactions to digital alternatives. While specific market size figures for 2025 are not provided, extrapolating from the given CAGR and assuming a 2024 market size (a reasonable assumption based on typical market reporting practices), a 2025 market value of approximately €100 million (a reasonable estimate considering industry averages for similarly sized markets in Europe) can be derived. This market is segmented by payment mode (point-of-sale and online sales) and end-user industry (retail, entertainment, healthcare, hospitality and others). The prevalence of international players like Mastercard, PayPal, and American Express underscores the attractiveness of the Polish market for payment processors.

However, regulatory changes and potential security concerns surrounding digital transactions could pose some restraints. The industry will likely witness increased competition among providers as they strive to differentiate themselves through innovative offerings and improved user experience. Future growth will depend on continuous technological advancements, a supportive regulatory framework, and the successful integration of emerging technologies like biometric authentication and blockchain solutions. The forecast period from 2025 to 2033 suggests continued strong growth, driven by the factors mentioned above, although the rate of growth might gradually moderate as the market matures. Specific market share for different players and payment types requires further data.

Poland Payments Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Poland payments industry, encompassing historical data (2019-2024), current estimates (2025), and future forecasts (2025-2033). It offers invaluable insights into market dynamics, key players, technological advancements, and future growth opportunities, making it an essential resource for stakeholders across the payments ecosystem. The report meticulously covers market sizing (in Millions), segmentation, and competitive landscapes, providing actionable intelligence for strategic decision-making.

Poland Payments Industry Market Composition & Trends

This section delves into the competitive dynamics of the Polish payments market, analyzing market concentration, innovation, regulation, substitution effects, and key end-user segments. The report assesses the impact of mergers and acquisitions (M&A) activity, providing data on deal values and market share distribution among leading players such as Bank Pekao, PKO Bank Polski, Santander Bank Polska, and international giants like Mastercard and PayPal Holdings Inc.

- Market Concentration: The Polish payments market exhibits a concentrated structure, with a few dominant players holding significant market share. The report quantifies this concentration, revealing the share held by the top 5 players (xx%).

- Innovation Catalysts: The adoption of digital technologies, particularly mobile payments and Buy Now Pay Later (BNPL) solutions, are significant innovation drivers. The report examines the role of fintech startups and partnerships in driving innovation.

- Regulatory Landscape: The report analyzes the evolving regulatory environment in Poland, assessing its impact on market access, competition, and data security. Key regulations and their influence on market dynamics are highlighted.

- Substitute Products: The analysis explores alternative payment methods and their potential impact on market share, considering factors like cash usage and the rise of cryptocurrencies. The report forecasts the market share of various payment methods in 2033.

- End-User Profiles: The report segments end-users by industry (Retail, Entertainment, Healthcare, Hospitality, etc.), detailing payment preferences and spending habits within each sector. Detailed analysis is provided on the Retail sector's payment trends, expected to reach xx Million by 2033.

- M&A Activity: The report documents significant M&A transactions within the Poland payments industry over the historical period, providing details on deal values (xx Million) and their impact on market consolidation.

Poland Payments Industry Industry Evolution

This section presents a comprehensive overview of the Poland payments industry's evolution from 2019 to 2033, highlighting key growth trajectories, technological advancements, and changing consumer preferences. It analyzes the impact of factors such as digitalization, increasing smartphone penetration, and shifting consumer expectations on market growth rates and adoption of new payment technologies.

The report details the growth of online payments, projecting an annual growth rate (xx%) for online transactions from 2025 to 2033. It also analyzes the adoption of contactless payments, estimating the percentage of transactions conducted using this method by 2033 (xx%). Technological advancements such as the integration of AI and blockchain in payment processing are explored, with projections for their impact on industry efficiency and security. The shifting consumer demand towards seamless, secure, and convenient payment experiences is also examined in detail, influencing payment technology adoption and the strategic choices of major players.

Leading Regions, Countries, or Segments in Poland Payments Industry

This section identifies the leading segments within the Polish payments market based on mode of payment (Point of Sale, Online Sale) and end-user industry (Retail, Entertainment, Healthcare, Hospitality, Others). Detailed analysis is presented to understand the factors driving the dominance of these segments.

By Mode of Payment:

- Point of Sale: Key drivers include the widespread adoption of contactless payments and the increasing penetration of POS terminals in physical stores. The report forecasts the market size of Point of Sale payments (xx Million) in 2033.

- Online Sale: The rapid growth of e-commerce and online shopping fuels the dominance of online payments. Factors driving growth include increased internet penetration and the growing preference for online transactions. The report projects the online sales market size (xx Million) in 2033.

By End-user Industry:

- Retail: This segment consistently dominates due to high transaction volumes and the widespread use of various payment methods. Factors contributing to its dominance include a large consumer base and the prevalence of both physical and online retail channels. Growth in online Retail is projected at xx% annually till 2033.

- Other End-user Industries: The report analyzes growth opportunities in other sectors like Healthcare, Entertainment, and Hospitality. Growth drivers for each sector are assessed, including regulatory changes and digital transformation initiatives.

Poland Payments Industry Product Innovations

This section highlights recent product innovations, their applications, and performance metrics. Key innovations discussed include the rise of BNPL solutions, mobile wallets, and the increasing adoption of biometric authentication. The report assesses the unique selling propositions and technological advancements behind each innovation, discussing their potential impact on market dynamics and consumer behavior. The focus will be on how these innovations enhance security, convenience, and efficiency for both merchants and consumers.

Propelling Factors for Poland Payments Industry Growth

Several factors contribute to the continued growth of the Poland payments industry. Technological advancements, particularly the widespread adoption of mobile and contactless payments, are key drivers. Economic growth and rising disposable incomes increase consumer spending, boosting transaction volumes. Furthermore, supportive government regulations and initiatives promote digitalization and financial inclusion, further stimulating industry expansion.

Obstacles in the Poland Payments Industry Market

Despite considerable growth potential, the Polish payments industry faces several challenges. Regulatory complexities and evolving data privacy regulations can pose significant hurdles for businesses. Concerns about cybersecurity and fraud prevention remain critical, potentially impacting consumer confidence. Intense competition from both established players and new entrants presents a constant challenge to market participants.

Future Opportunities in Poland Payments Industry

The Polish payments industry offers several promising future opportunities. The expansion of mobile and digital payments in underserved regions holds immense potential. The increasing adoption of open banking and embedded finance could unlock new revenue streams. Further development and integration of innovative payment technologies such as AI and blockchain can enhance security and efficiency, presenting attractive opportunities.

Major Players in the Poland Payments Industry Ecosystem

- Bank Pekao

- Apple Pay

- PKO Bank Polski

- Mastercard

- PayPal Holdings Inc

- PayU

- Santander Bank Polska

- DotPay

- American Express

- Tap2Pay me

Key Developments in Poland Payments Industry Industry

- May 2022: Allegro launched a new service with One Kurier, enabling contactless card and smartphone payments for cash-on-delivery purchases. This enhances convenience for customers and boosts transaction volumes for Allegro.

- May 2022: PKO BP announced the completion of its BNPL (Buy Now, Pay Later) solution. Its widespread adoption across online shops is expected to significantly increase the popularity and usage of BNPL in Poland.

Strategic Poland Payments Industry Market Forecast

The Poland payments industry is poised for robust growth in the coming years, driven by technological innovation, rising e-commerce adoption, and a supportive regulatory environment. The increasing penetration of mobile payments and the expanding use of BNPL solutions are expected to be key catalysts for market expansion. The market is predicted to show significant growth (xx% CAGR) from 2025 to 2033, reaching a total market size of xx Million by the end of the forecast period.

Poland Payments Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Pay

- 1.1.2. Digital Wallet (includes Mobile Wallets)

- 1.1.3. Cash

- 1.1.4. Others

-

1.2. Online Sale

- 1.2.1. Others (

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Poland Payments Industry Segmentation By Geography

- 1. Poland

Poland Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 12.39% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Advancements in the Polish Payments Market; Initiatives by the Government to improve cashless payment methods

- 3.3. Market Restrains

- 3.3.1. Lack of a standard legislative policy remains especially in the case of cross-border transactions

- 3.4. Market Trends

- 3.4.1. Advancements in the Polish Payments Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Poland Payments Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Pay

- 5.1.1.2. Digital Wallet (includes Mobile Wallets)

- 5.1.1.3. Cash

- 5.1.1.4. Others

- 5.1.2. Online Sale

- 5.1.2.1. Others (

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Bank Pekao

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Apple Pay*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 PKO Bank Polski

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Mastercard

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 PayPal Holdings Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 PayU

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Santander Bank Polska

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 DotPay

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 American Express

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Tap2Pay me

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Bank Pekao

List of Figures

- Figure 1: Poland Payments Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Poland Payments Industry Share (%) by Company 2024

List of Tables

- Table 1: Poland Payments Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Poland Payments Industry Revenue Million Forecast, by Mode of Payment 2019 & 2032

- Table 3: Poland Payments Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: Poland Payments Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Poland Payments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Poland Payments Industry Revenue Million Forecast, by Mode of Payment 2019 & 2032

- Table 7: Poland Payments Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 8: Poland Payments Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Payments Industry?

The projected CAGR is approximately 12.39%.

2. Which companies are prominent players in the Poland Payments Industry?

Key companies in the market include Bank Pekao, Apple Pay*List Not Exhaustive, PKO Bank Polski, Mastercard, PayPal Holdings Inc, PayU, Santander Bank Polska, DotPay, American Express, Tap2Pay me.

3. What are the main segments of the Poland Payments Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Advancements in the Polish Payments Market; Initiatives by the Government to improve cashless payment methods.

6. What are the notable trends driving market growth?

Advancements in the Polish Payments Market.

7. Are there any restraints impacting market growth?

Lack of a standard legislative policy remains especially in the case of cross-border transactions.

8. Can you provide examples of recent developments in the market?

May 2022 - Allegro announced a new service implemented in one of the platform's delivery methods - One Kurier. Customers using this method and paying for cash-on-delivery purchases can pay by card or smartphone using the contactless method on the courier's device used to manage shipments.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Payments Industry?

To stay informed about further developments, trends, and reports in the Poland Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence