Key Insights

The North American confectionery market, valued at approximately $XX million in 2025, is projected to experience robust growth, driven by several key factors. A rising disposable income, particularly amongst younger demographics known for their high confectionery consumption, fuels market expansion. The increasing popularity of premium and artisanal confectionery products, offering unique flavors and high-quality ingredients, contributes to higher average spending per consumer. Furthermore, strategic marketing initiatives by major players focusing on innovative product launches and appealing to specific consumer segments (e.g., health-conscious options, specialized dietary needs) are stimulating market growth. The convenience store and online retail channels are witnessing significant growth, reflecting changing consumer shopping habits and the increasing reach of e-commerce platforms. While potential economic downturns could act as a restraint, the inherent emotional connection consumers have with confectionery, coupled with its role in celebrations and everyday indulgences, ensures a relatively resilient market even during economic fluctuations. Competition among established players like Nestlé, Mars, and Hershey, coupled with the emergence of smaller, niche brands, fosters innovation and product diversification, further driving market expansion. The US holds the largest market share within North America, followed by Canada and Mexico, with the Rest of North America segment displaying steady but slower growth.

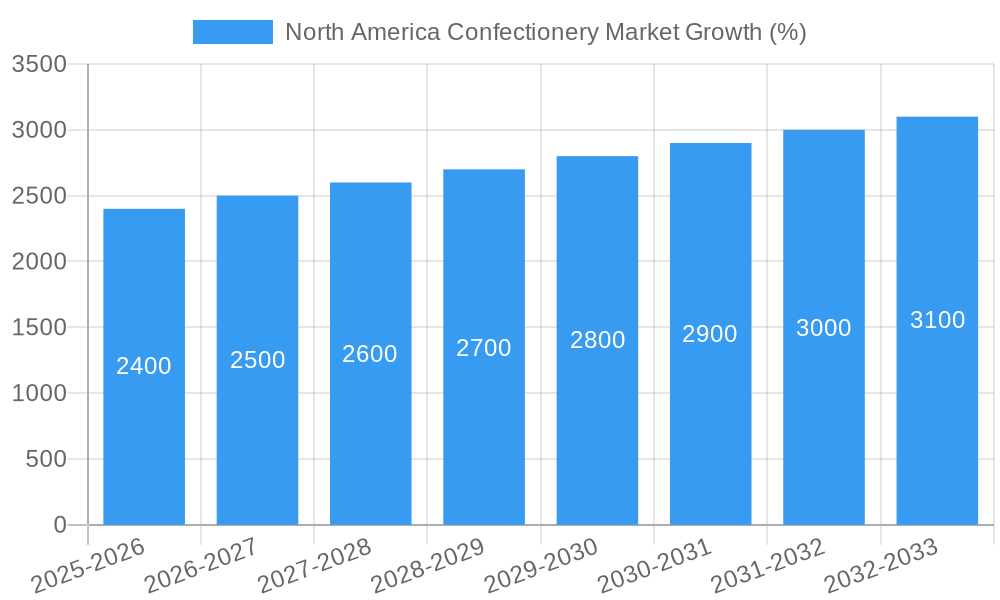

Looking ahead to 2033, the North American confectionery market is expected to continue its upward trajectory. The CAGR of 4.80% indicates consistent growth, although variations within specific segments are likely. Chocolate, a dominant segment, will maintain its market leadership due to its established consumer preference. However, growth in other confectionery categories, such as gummies and hard candies, is expected, particularly driven by trends towards healthier options and innovative product formats. The shift toward online retail will continue, posing both opportunities and challenges for established players. Companies need to adapt their strategies to navigate the changing landscape, investing in e-commerce platforms, optimizing online marketing, and ensuring seamless delivery experiences. Maintaining product quality, addressing health and wellness concerns, and effectively targeting key demographic segments remain critical for sustained success within this dynamic market.

North America Confectionery Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the North America confectionery market, encompassing the historical period (2019-2024), base year (2025), and forecast period (2025-2033). It offers a comprehensive overview of market trends, competitive landscape, and future growth prospects, empowering stakeholders to make informed strategic decisions. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period.

North America Confectionery Market Composition & Trends

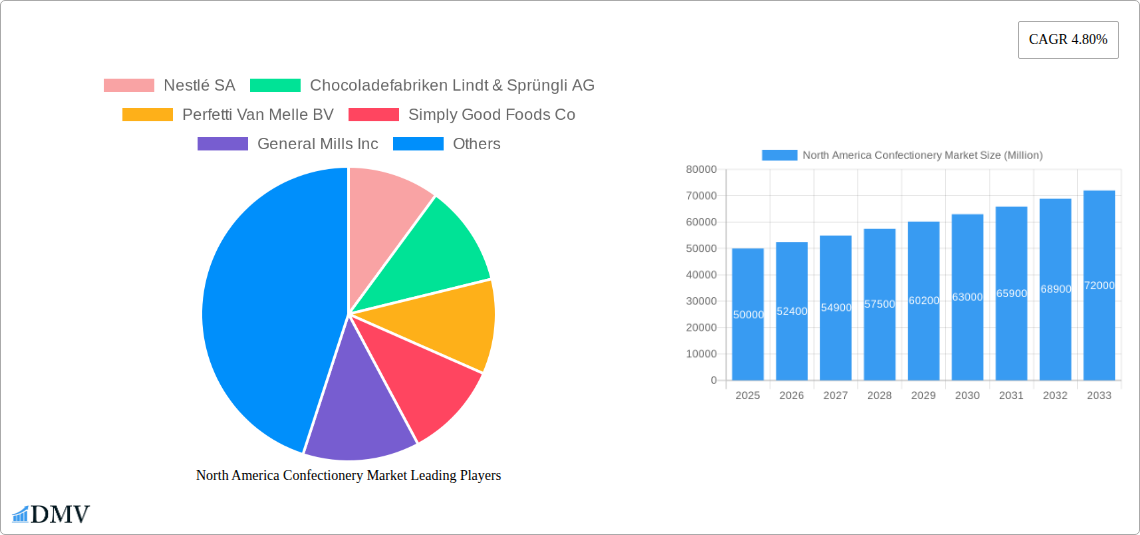

This section delves into the intricate dynamics of the North American confectionery market, examining market concentration, innovation drivers, regulatory frameworks, substitute products, consumer profiles, and merger & acquisition (M&A) activities. The market is highly concentrated, with key players like Nestlé SA, Chocoladefabriken Lindt & Sprüngli AG, and The Hershey Company commanding significant market share. However, smaller, specialized players continue to emerge, driven by consumer demand for unique and healthier options.

- Market Share Distribution: Nestlé SA holds an estimated xx% market share in 2025, followed by Mondelez International at xx%, and Hershey's at xx%. The remaining share is distributed among other key players listed above and smaller regional brands.

- Innovation Catalysts: Growing consumer preference for premium chocolate, organic ingredients, and functional confectionery is driving innovation.

- Regulatory Landscape: Regulations concerning sugar content, labeling, and ingredient sourcing are constantly evolving, influencing product development and marketing strategies.

- Substitute Products: The market faces competition from healthier snack alternatives, such as fruit snacks and granola bars.

- End-User Profiles: The market caters to diverse consumer segments, including children, adults, and health-conscious individuals, each with unique preferences.

- M&A Activities: The confectionery sector has witnessed significant M&A activity in recent years, with deal values totaling xx Million in 2024. These activities are primarily driven by the desire to expand product portfolios and geographic reach.

North America Confectionery Market Industry Evolution

The North American confectionery market has undergone a significant transformation over the past five years. Market growth has been fueled by factors such as increasing disposable incomes, changing consumer preferences towards premium and specialty confectionery, and the rise of e-commerce. Technological advancements in production and packaging have also played a crucial role in improving efficiency and product quality. Shifting consumer demands towards healthier options, including reduced sugar and organic products, have forced manufacturers to adapt their product offerings and marketing strategies. The market experienced a xx% growth rate from 2019 to 2024, primarily driven by the increasing popularity of chocolate confectionery and the growing demand for convenient snack options. The adoption rate of online retail channels has increased significantly, contributing to market expansion.

Leading Regions, Countries, or Segments in North America Confectionery Market

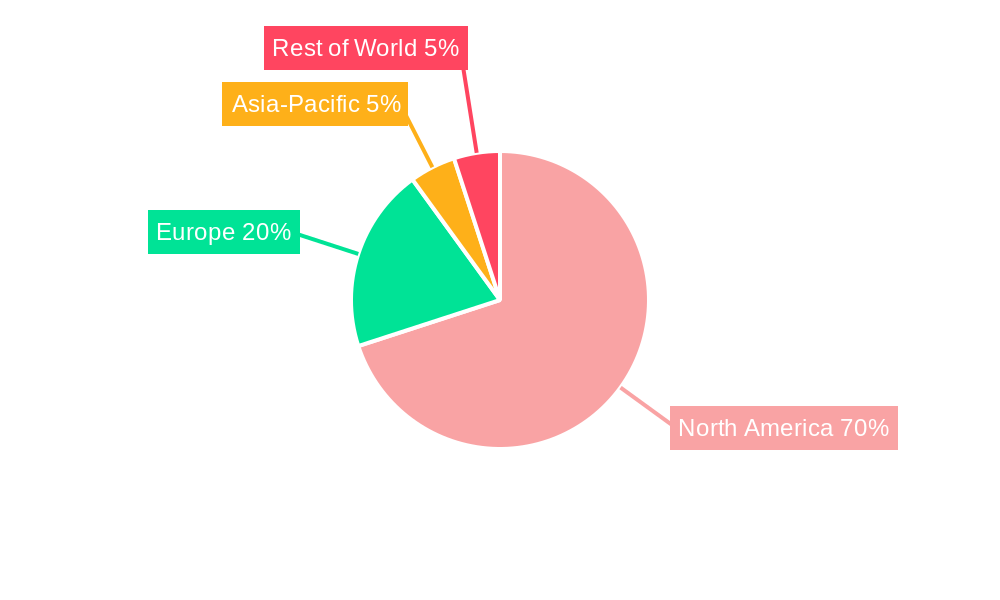

The United States remains the dominant market within North America, accounting for approximately xx% of the total market value in 2025. This dominance is attributed to several factors, including high per capita consumption, strong brand presence, and a robust retail infrastructure. Canada and Mexico exhibit significant growth potential, driven by expanding middle-class populations and rising disposable incomes.

- Key Drivers for US Dominance:

- High per capita consumption of confectionery products.

- Strong presence of major confectionery manufacturers.

- Extensive distribution network, including supermarkets, convenience stores, and online retailers.

- Robust marketing and advertising campaigns targeting various consumer segments.

- Chocolate Confectionery: This segment dominates the market, driven by the enduring popularity of chocolate across all demographics.

- Supermarket/Hypermarket: This distribution channel holds the largest market share due to its wide reach and extensive product availability.

North America Confectionery Market Product Innovations

Recent innovations focus on healthier options like reduced sugar content, organic ingredients, and functional confectionery incorporating protein or probiotics. Manufacturers are increasingly using sustainable packaging and incorporating unique flavors and textures to cater to evolving consumer preferences. The use of innovative technology such as 3D printing is also emerging, allowing for customized and personalized confectionery products. Unique selling propositions include high-quality ingredients, unique flavor combinations, and ethical sourcing practices.

Propelling Factors for North America Confectionery Market Growth

The North American confectionery market is projected to experience robust growth due to several key factors. The rising disposable incomes of consumers, particularly in emerging economies, significantly contribute to increased spending on discretionary items like confectionery. Furthermore, the continued rise of e-commerce provides new distribution channels, allowing for wider market penetration. Government regulations surrounding food safety and labeling also indirectly impact the growth, by stimulating innovation and enhancing consumer confidence.

Obstacles in the North America Confectionery Market

Several factors hinder the growth of the North American confectionery market. Fluctuating raw material prices, particularly cocoa and sugar, impact production costs and profitability. Moreover, increasing health concerns surrounding sugar consumption lead to reduced demand and the need for healthier product reformulations. Intense competition among established players and the entry of new players also pose a challenge. Supply chain disruptions, particularly those experienced in recent years, can significantly impact production and distribution.

Future Opportunities in North America Confectionery Market

The market offers significant opportunities for expansion. The growing demand for premium and artisanal confectionery products creates a niche for high-quality offerings. Moreover, tapping into the increasing popularity of vegan and plant-based confectionery presents a lucrative opportunity. Exploring emerging markets within North America, such as underserved regions and ethnic communities, will also contribute to market expansion.

Major Players in the North America Confectionery Market Ecosystem

- Nestlé SA

- Chocoladefabriken Lindt & Sprüngli AG

- Perfetti Van Melle BV

- Simply Good Foods Co

- General Mills Inc

- PepsiCo Inc

- Tootsie Roll Industries Inc

- Ferrero International SA

- The Bazooka Companies Inc

- Mars Incorporated

- HARIBO Holding GmbH & Co KG

- Ford Gum & Machine Company Inc

- Mondelēz International Inc

- The Hershey Company

- Kellogg Company

Key Developments in North America Confectionery Market Industry

- August 2023: Ferrero North America launched new Kinder Chocolate products and seasonal offerings at the Sweets & Snacks Expo in Chicago, signaling a focus on product innovation and expansion.

- July 2023: HARIBO opened its first North American manufacturing facility in Wisconsin, signifying increased investment and capacity to meet growing US consumer demand.

- May 2023: General Mills Inc. expanded its facilities in Geneva and Illinois, indicating confidence in future market growth and distribution capabilities.

Strategic North America Confectionery Market Forecast

The North American confectionery market is poised for continued growth, driven by several factors including increasing disposable incomes, evolving consumer preferences, and technological advancements. The focus on healthier options, along with the expansion into e-commerce, presents lucrative opportunities for manufacturers. The market's future hinges on adapting to evolving consumer demands, navigating regulatory changes, and effectively managing supply chain challenges. The forecast predicts significant growth in both volume and value over the next decade.

North America Confectionery Market Segmentation

-

1. Confections

-

1.1. Chocolate

-

1.1.1. By Confectionery Variant

- 1.1.1.1. Dark Chocolate

- 1.1.1.2. Milk and White Chocolate

-

1.1.1. By Confectionery Variant

-

1.2. Gums

- 1.2.1. Bubble Gum

-

1.2.2. Chewing Gum

-

1.2.2.1. By Sugar Content

- 1.2.2.1.1. Sugar Chewing Gum

- 1.2.2.1.2. Sugar-free Chewing Gum

-

1.2.2.1. By Sugar Content

-

1.3. Snack Bar

- 1.3.1. Cereal Bar

- 1.3.2. Fruit & Nut Bar

- 1.3.3. Protein Bar

-

1.4. Sugar Confectionery

- 1.4.1. Hard Candy

- 1.4.2. Lollipops

- 1.4.3. Mints

- 1.4.4. Pastilles, Gummies, and Jellies

- 1.4.5. Toffees and Nougats

- 1.4.6. Others

-

1.1. Chocolate

-

2. Distribution Channel

- 2.1. Convenience Store

- 2.2. Online Retail Store

- 2.3. Supermarket/Hypermarket

- 2.4. Others

North America Confectionery Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Confectionery Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.80% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Influence of Endorsements

- 3.2.2 Aggressive Marketing

- 3.2.3 and Strategic Investments; Demand for Sustainable Chocolates and Single Origin Certified Chocolates

- 3.3. Market Restrains

- 3.3.1. Availability of Counterfeit Products; Fluctuating Price of Raw Materials

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Confections

- 5.1.1. Chocolate

- 5.1.1.1. By Confectionery Variant

- 5.1.1.1.1. Dark Chocolate

- 5.1.1.1.2. Milk and White Chocolate

- 5.1.1.1. By Confectionery Variant

- 5.1.2. Gums

- 5.1.2.1. Bubble Gum

- 5.1.2.2. Chewing Gum

- 5.1.2.2.1. By Sugar Content

- 5.1.2.2.1.1. Sugar Chewing Gum

- 5.1.2.2.1.2. Sugar-free Chewing Gum

- 5.1.2.2.1. By Sugar Content

- 5.1.3. Snack Bar

- 5.1.3.1. Cereal Bar

- 5.1.3.2. Fruit & Nut Bar

- 5.1.3.3. Protein Bar

- 5.1.4. Sugar Confectionery

- 5.1.4.1. Hard Candy

- 5.1.4.2. Lollipops

- 5.1.4.3. Mints

- 5.1.4.4. Pastilles, Gummies, and Jellies

- 5.1.4.5. Toffees and Nougats

- 5.1.4.6. Others

- 5.1.1. Chocolate

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Convenience Store

- 5.2.2. Online Retail Store

- 5.2.3. Supermarket/Hypermarket

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Confections

- 6. United States North America Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Nestlé SA

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Chocoladefabriken Lindt & Sprüngli AG

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Perfetti Van Melle BV

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Simply Good Foods Co

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 General Mills Inc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 PepsiCo Inc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Tootsie Roll Industries Inc

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Ferrero International SA

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 The Bazooka Companies Inc

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Mars Incorporated

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 HARIBO Holding GmbH & Co KG

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 Ford Gum & Machine Company Inc

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 Mondelēz International Inc

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.14 The Hershey Company

- 10.2.14.1. Overview

- 10.2.14.2. Products

- 10.2.14.3. SWOT Analysis

- 10.2.14.4. Recent Developments

- 10.2.14.5. Financials (Based on Availability)

- 10.2.15 Kellogg Company

- 10.2.15.1. Overview

- 10.2.15.2. Products

- 10.2.15.3. SWOT Analysis

- 10.2.15.4. Recent Developments

- 10.2.15.5. Financials (Based on Availability)

- 10.2.1 Nestlé SA

List of Figures

- Figure 1: North America Confectionery Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Confectionery Market Share (%) by Company 2024

List of Tables

- Table 1: North America Confectionery Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Confectionery Market Revenue Million Forecast, by Confections 2019 & 2032

- Table 3: North America Confectionery Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 4: North America Confectionery Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: North America Confectionery Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States North America Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada North America Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico North America Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America North America Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: North America Confectionery Market Revenue Million Forecast, by Confections 2019 & 2032

- Table 11: North America Confectionery Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 12: North America Confectionery Market Revenue Million Forecast, by Country 2019 & 2032

- Table 13: United States North America Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada North America Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Mexico North America Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Confectionery Market?

The projected CAGR is approximately 4.80%.

2. Which companies are prominent players in the North America Confectionery Market?

Key companies in the market include Nestlé SA, Chocoladefabriken Lindt & Sprüngli AG, Perfetti Van Melle BV, Simply Good Foods Co, General Mills Inc, PepsiCo Inc, Tootsie Roll Industries Inc, Ferrero International SA, The Bazooka Companies Inc, Mars Incorporated, HARIBO Holding GmbH & Co KG, Ford Gum & Machine Company Inc, Mondelēz International Inc, The Hershey Company, Kellogg Company.

3. What are the main segments of the North America Confectionery Market?

The market segments include Confections, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Influence of Endorsements. Aggressive Marketing. and Strategic Investments; Demand for Sustainable Chocolates and Single Origin Certified Chocolates.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Availability of Counterfeit Products; Fluctuating Price of Raw Materials.

8. Can you provide examples of recent developments in the market?

August 2023: Ferrero North America, in the United States, revealed new products and seasonal offerings, including Kinder Chocolate, at the Annual Sweets & Snacks Expo in Chicago.July 2023: HARIBO® officially began gummi production at its first-ever North American manufacturing facility, located in Pleasant Prairie, Wis. The brand-new, state-of-the-art factory was created to meet the growing demand by US consumers of the beloved gummi brand, which produces over 25 varieties of gummi treats in the US and more than 1,200 types globally.May 2023: General Mills Inc. added two new buildings in Geneva and Illinois: a 65,600-square-foot asset located in Geneva and a 48,600-square-foot warehouse expansion in Illinois.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Confectionery Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Confectionery Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Confectionery Market?

To stay informed about further developments, trends, and reports in the North America Confectionery Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence