Key Insights

The Indian smart grid market is experiencing robust growth, driven by increasing electricity demand, the need for improved grid reliability, and the government's push for renewable energy integration. A CAGR exceeding 3% signifies a consistently expanding market, projected to reach significant value within the forecast period (2025-2033). Key segments driving this growth include smart metering (AMI, smart meters, data concentrators), which enhances energy efficiency and consumer engagement; smart transmission and distribution (smart transformers, switches, sensors) improving grid stability and reducing transmission losses; and smart substations (digital substations, SCADA systems) enabling advanced grid management and control. The burgeoning adoption of smart grid software and analytics (SCADA, DMS, EMS, AMI software) further strengthens the market, offering advanced data analysis and predictive capabilities for improved grid operation. Leading players like Honeywell, ABB, Accenture, and Siemens are actively participating in this growth, contributing to the development and deployment of smart grid technologies across India. While challenges such as high initial investment costs and the need for robust cybersecurity measures exist, the long-term benefits of improved energy efficiency, reliability, and integration of renewable sources outweigh these constraints, making the Indian smart grid market an attractive investment opportunity. The Asia-Pacific region, particularly India, with its large population and expanding energy needs, presents a substantial growth potential within the global smart grid landscape. This market's expansion is expected to be fuelled by continued government initiatives focusing on infrastructure modernization and energy security.

The Indian government's initiatives focusing on infrastructure development and renewable energy integration are key catalysts for this growth. The substantial investment in upgrading the existing power infrastructure and expanding the reach of electricity to rural areas presents a significant opportunity for smart grid technology adoption. The integration of renewable energy sources like solar and wind power requires sophisticated grid management capabilities, which are readily addressed by smart grid solutions. Moreover, the increasing awareness among consumers regarding energy efficiency and the rising demand for reliable and uninterrupted power supply are further propelling the market forward. Despite the challenges, the Indian smart grid market is poised for strong growth in the coming years, driven by a combination of government support, technological advancements, and increasing consumer demand for a more reliable and efficient power grid. The focus on digitalization and data analytics within the energy sector is further accelerating the adoption of smart grid technologies across various segments.

Indian Smart Grid Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Indian smart grid industry, offering invaluable insights for stakeholders across the value chain. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report presents a robust understanding of the market's historical performance, current state, and future trajectory. The report leverages extensive data analysis to reveal key trends, challenges, and opportunities shaping this dynamic sector, providing a crucial roadmap for informed decision-making. The Indian smart grid market, valued at xx Million in 2025, is poised for significant expansion, driven by government initiatives and increasing energy demands.

Indian Smart Grid Industry Market Composition & Trends

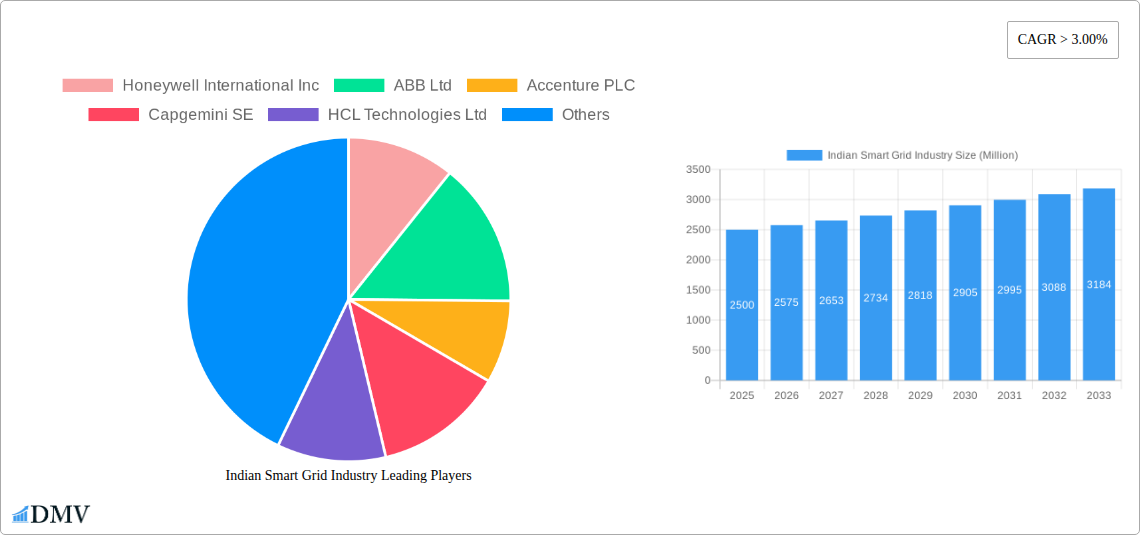

The Indian smart grid market is characterized by a moderately concentrated landscape, with both established global players and domestic companies competing fiercely. Major players include Honeywell International Inc, ABB Ltd, Accenture PLC, Capgemini SE, HCL Technologies Ltd, Siemens AG, Cisco Systems Inc, Schneider Electric SE, General Electric Company, and Power Grid Corporation of India Limited. Market share distribution varies across segments, with smart metering currently holding a significant portion. Innovation is spurred by government policies promoting renewable energy integration and improved grid efficiency. The regulatory landscape, while evolving, presents both opportunities and challenges. Substitute products remain limited, with smart grid technologies offering superior performance and efficiency. End-user profiles encompass discoms, utilities, and industrial consumers. M&A activity has been moderate, with deal values totaling xx Million in the last five years.

- Market Concentration: Moderately concentrated, with a mix of global and domestic players.

- Innovation Catalysts: Government policies favoring renewable energy integration and grid modernization.

- Regulatory Landscape: Evolving, with both supportive and challenging aspects.

- Substitute Products: Limited viable substitutes.

- End-User Profiles: Discoms, utilities, and industrial consumers.

- M&A Activity: Moderate, with xx Million in deal values (2019-2024).

Indian Smart Grid Industry Industry Evolution

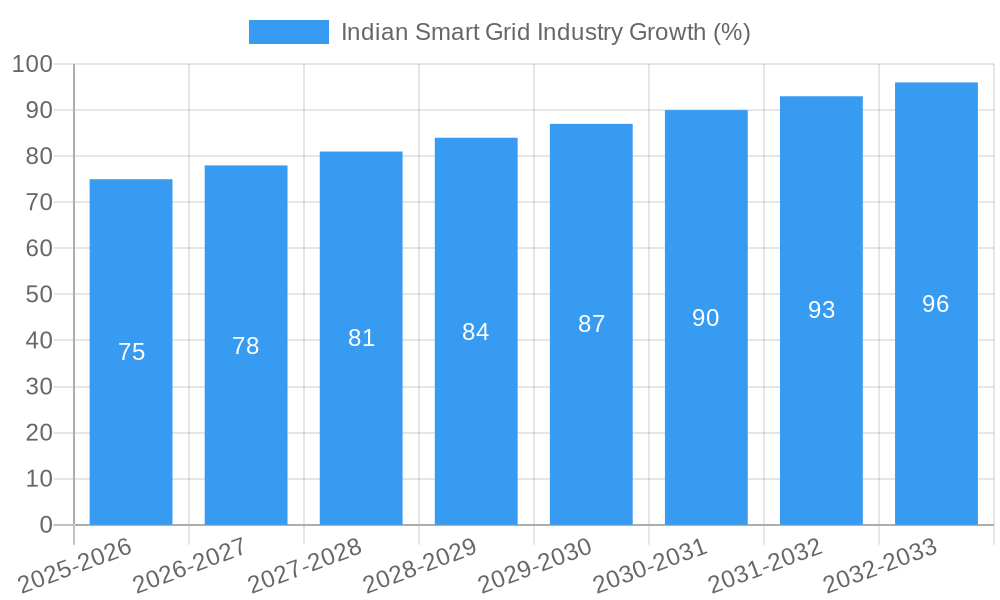

The Indian smart grid industry has witnessed significant growth over the past five years, driven by increasing electricity demand, the need for enhanced grid reliability, and government initiatives promoting smart city projects and renewable energy integration. The market experienced a Compound Annual Growth Rate (CAGR) of xx% during the historical period (2019-2024), and this growth is projected to accelerate in the forecast period (2025-2033), reaching a CAGR of xx%. Technological advancements, such as the adoption of advanced metering infrastructure (AMI) and the integration of artificial intelligence (AI) and machine learning (ML) for improved grid management, are key growth drivers. Consumer demand for reliable and affordable electricity is also fueling market expansion. The adoption rate of smart meters is steadily increasing, with significant projects underway across various states. Smart grid software and analytics are gaining traction as utilities seek to optimize grid operations and improve energy efficiency. The integration of renewable energy sources is also driving the need for advanced grid management systems capable of handling intermittent power supply.

Leading Regions, Countries, or Segments in Indian Smart Grid Industry

The smart metering segment, encompassing AMI, smart meters, and data concentrators, currently dominates the Indian smart grid market. This is fueled by government mandates for smart meter deployment and the potential for significant efficiency gains. However, other segments, particularly smart transmission and distribution, are experiencing rapid growth.

Key Drivers for Smart Metering Dominance:

- Massive government investment in smart meter rollouts across multiple states.

- Strong regulatory support for AMI implementation.

- Significant cost savings and efficiency improvements through reduced energy losses and improved billing accuracy.

Growth in Smart Transmission & Distribution: Investment in upgrading aging infrastructure, increasing focus on grid modernization, and growing adoption of smart sensors and switches are key drivers.

Smart Substations: While comparatively smaller, this segment is crucial for grid modernization, reliability, and efficiency.

Smart Grid Software & Analytics: The adoption of advanced software solutions like SCADA, DMS, and EMS is growing rapidly.

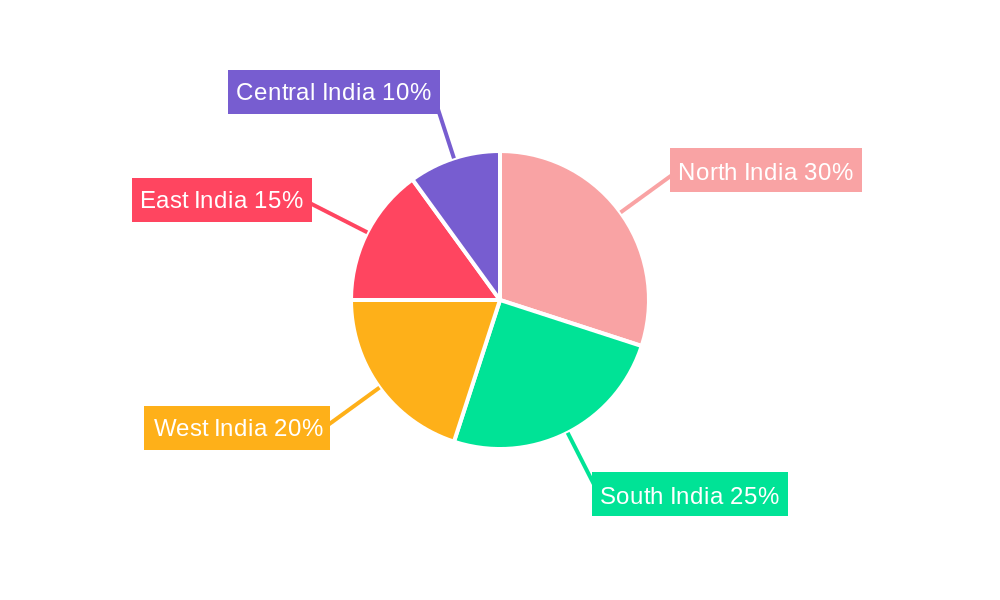

The states of Uttar Pradesh, Maharashtra, and Gujarat are currently leading in smart grid deployments due to large-scale projects and favorable government policies.

Indian Smart Grid Industry Product Innovations

Recent innovations in smart grid technologies focus on enhancing efficiency, reliability, and security. This includes the development of advanced sensors with improved accuracy and longevity, AI-powered predictive maintenance solutions for grid assets, and cybersecurity enhancements to protect against cyber threats. The emergence of 5G-enabled smart meters offers improved communication capabilities and data transmission speeds. The unique selling proposition of many new products centers around improved data analytics, enabling more precise grid management and predictive maintenance.

Propelling Factors for Indian Smart Grid Industry Growth

Several factors are driving the growth of the Indian smart grid industry. Government initiatives like the Smart Cities Mission and the National Electricity Plan are providing significant impetus. The increasing adoption of renewable energy sources, along with the need to manage intermittency and enhance grid reliability, is pushing the demand for sophisticated grid management systems. Furthermore, economic incentives for energy efficiency and reduced transmission & distribution losses are encouraging utilities to invest in smart grid technologies.

Obstacles in the Indian Smart Grid Industry Market

The Indian smart grid market faces several obstacles. Regulatory complexities and bureaucratic hurdles can delay project implementation. Supply chain disruptions and the availability of skilled labor can also present challenges. Finally, the high initial investment costs associated with smart grid deployment can be a barrier for some utilities, particularly smaller discoms.

Future Opportunities in Indian Smart Grid Industry

Future opportunities lie in expanding smart grid deployments to rural areas, enhancing cybersecurity measures, and integrating advanced analytics for improved grid management and demand-side response. The increasing adoption of electric vehicles and the growth of distributed energy resources will also create new opportunities for smart grid technologies. The development of new business models and financing mechanisms to support smart grid investments will also be crucial.

Major Players in the Indian Smart Grid Industry Ecosystem

- Honeywell International Inc

- ABB Ltd

- Accenture PLC

- Capgemini SE

- HCL Technologies Ltd

- Siemens AG

- Cisco Systems Inc

- Schneider Electric SE

- General Electric Company

- Power Grid Corporation of India Limited

Key Developments in Indian Smart Grid Industry Industry

- October 2022: Several corporate giants bid for the installation of approximately 28.5 Million prepaid smart meters in Uttar Pradesh. This signifies substantial market expansion in a key state.

- February 2023: BEST announced plans to install smart meters for 1.05 Million consumers, showcasing growing adoption in major urban areas.

Strategic Indian Smart Grid Industry Market Forecast

The Indian smart grid market is poised for robust growth, driven by government support, increasing energy demand, and the need for grid modernization. The focus on renewable energy integration, smart city initiatives, and the rising adoption of advanced metering infrastructure will continue to fuel market expansion. Significant investments are expected in smart grid technologies, creating substantial opportunities for both domestic and international players.

Indian Smart Grid Industry Segmentation

- 1. Transmission

- 2. Advanced Metering Infrastructure (AMI)

- 3. Communication Technology

- 4. Other Technology Application Areas

Indian Smart Grid Industry Segmentation By Geography

- 1. India

Indian Smart Grid Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 3.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Growing Power Demand from the Commercial and Industrial Sectors

- 3.3. Market Restrains

- 3.3.1. 4.; Stringent Environmental and Safety Regulations

- 3.4. Market Trends

- 3.4.1. Advanced Metering Infrastructure (AMI) is Expected to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Transmission

- 5.2. Market Analysis, Insights and Forecast - by Advanced Metering Infrastructure (AMI)

- 5.3. Market Analysis, Insights and Forecast - by Communication Technology

- 5.4. Market Analysis, Insights and Forecast - by Other Technology Application Areas

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. India

- 5.1. Market Analysis, Insights and Forecast - by Transmission

- 6. China Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 7. Japan Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 8. India Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 9. South Korea Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 10. Taiwan Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 11. Australia Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Asia-Pacific Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Honeywell International Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 ABB Ltd

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Accenture PLC

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Capgemini SE

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 HCL Technologies Ltd

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Siemens AG*List Not Exhaustive

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Cisco Systems Inc

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Schneider Electric SE

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 General Electric Company

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Power Grid Corporation of India Limited

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Honeywell International Inc

List of Figures

- Figure 1: Indian Smart Grid Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Indian Smart Grid Industry Share (%) by Company 2024

List of Tables

- Table 1: Indian Smart Grid Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Indian Smart Grid Industry Revenue Million Forecast, by Transmission 2019 & 2032

- Table 3: Indian Smart Grid Industry Revenue Million Forecast, by Advanced Metering Infrastructure (AMI) 2019 & 2032

- Table 4: Indian Smart Grid Industry Revenue Million Forecast, by Communication Technology 2019 & 2032

- Table 5: Indian Smart Grid Industry Revenue Million Forecast, by Other Technology Application Areas 2019 & 2032

- Table 6: Indian Smart Grid Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: Indian Smart Grid Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: China Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Japan Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: India Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: South Korea Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Taiwan Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Australia Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of Asia-Pacific Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Indian Smart Grid Industry Revenue Million Forecast, by Transmission 2019 & 2032

- Table 16: Indian Smart Grid Industry Revenue Million Forecast, by Advanced Metering Infrastructure (AMI) 2019 & 2032

- Table 17: Indian Smart Grid Industry Revenue Million Forecast, by Communication Technology 2019 & 2032

- Table 18: Indian Smart Grid Industry Revenue Million Forecast, by Other Technology Application Areas 2019 & 2032

- Table 19: Indian Smart Grid Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian Smart Grid Industry?

The projected CAGR is approximately > 3.00%.

2. Which companies are prominent players in the Indian Smart Grid Industry?

Key companies in the market include Honeywell International Inc, ABB Ltd, Accenture PLC, Capgemini SE, HCL Technologies Ltd, Siemens AG*List Not Exhaustive, Cisco Systems Inc, Schneider Electric SE, General Electric Company, Power Grid Corporation of India Limited.

3. What are the main segments of the Indian Smart Grid Industry?

The market segments include Transmission, Advanced Metering Infrastructure (AMI), Communication Technology, Other Technology Application Areas.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Power Demand from the Commercial and Industrial Sectors.

6. What are the notable trends driving market growth?

Advanced Metering Infrastructure (AMI) is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Stringent Environmental and Safety Regulations.

8. Can you provide examples of recent developments in the market?

February 2023: The Brihanmumbai Electric Supply and Transport (BEST) announced that the company is likely to start installing smart meters for its 10.5 lakh power consumers from March 2023 onward. These devices will be enabled with 4G and 5G SIM cards and will offer pre-paid payment options for consumers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian Smart Grid Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian Smart Grid Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian Smart Grid Industry?

To stay informed about further developments, trends, and reports in the Indian Smart Grid Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence