Key Insights

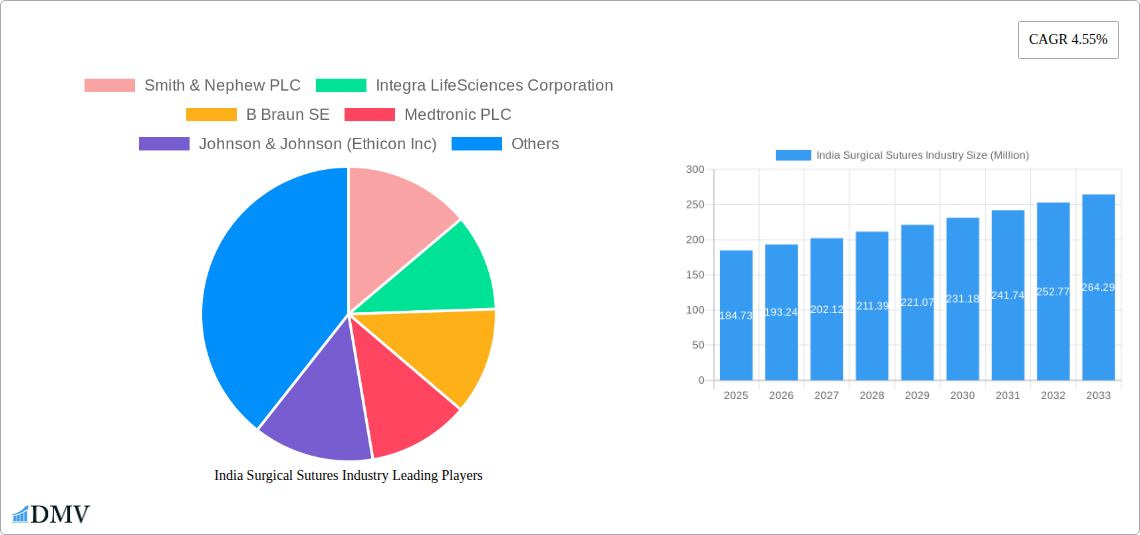

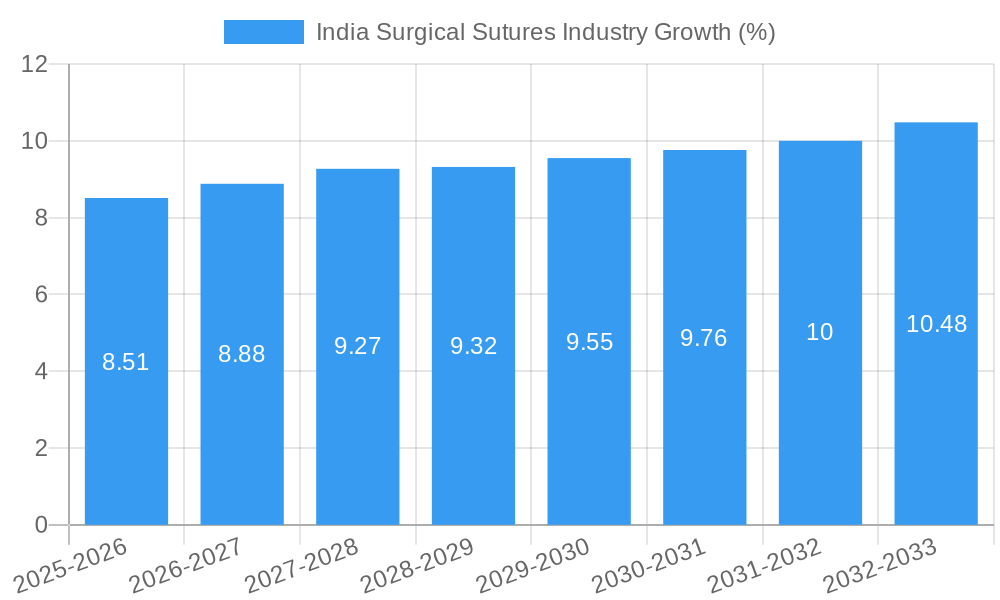

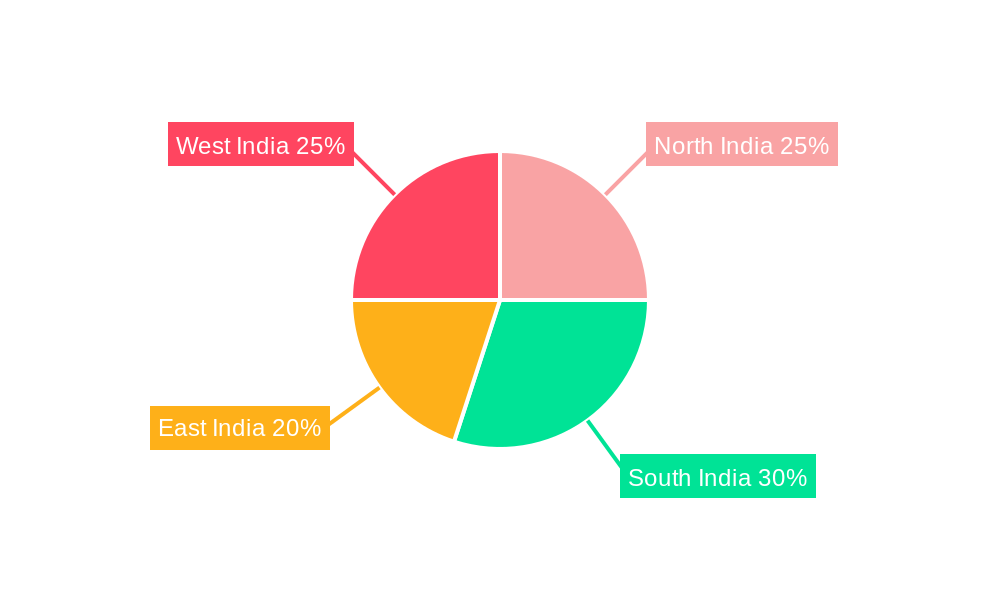

The Indian surgical sutures market, valued at $184.73 million in 2025, is projected to experience robust growth, driven by a rising prevalence of chronic diseases necessitating surgical interventions, increasing geriatric population requiring more surgeries, and expanding healthcare infrastructure. The market's Compound Annual Growth Rate (CAGR) of 4.55% from 2025 to 2033 indicates a steady expansion. Growth is further fueled by advancements in surgical techniques, a preference for minimally invasive procedures, and the rising adoption of advanced suture materials offering improved wound healing and reduced infection risk. The segment encompassing absorbable sutures is anticipated to dominate the market due to their convenience and reduced risk of complications. Hospitals and clinics constitute the largest end-user segment, driven by their higher surgical volumes compared to ambulatory surgical centers. Geographically, the market shows significant potential across all regions of India (North, South, East, and West), with the South and West regions potentially demonstrating faster growth due to higher concentration of advanced medical facilities and increasing healthcare awareness. Key players, including Smith & Nephew, Integra LifeSciences, B. Braun, Medtronic, Johnson & Johnson (Ethicon), Boston Scientific, Conmed, and others are actively shaping the market through product innovation and strategic partnerships. Competition is expected to intensify as new players enter the market, particularly in the production of cost-effective and high-quality synthetic sutures.

The increasing demand for specialized surgical sutures for ophthalmic, cardiovascular, and orthopedic surgeries presents significant opportunities for market expansion. However, challenges such as high costs associated with advanced suture materials, stringent regulatory approvals, and the availability of cheaper alternatives from local manufacturers could potentially restrain market growth. To maintain momentum, manufacturers are focusing on developing innovative products with improved biocompatibility, strength, and ease of use, catering to the diverse needs of surgeons across different specializations. Furthermore, strategic collaborations with hospitals and distribution networks will play a crucial role in penetrating the market effectively and capturing significant market share. The long-term outlook for the Indian surgical sutures market remains positive, with consistent growth expected throughout the forecast period.

India Surgical Sutures Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the India surgical sutures market, offering invaluable insights for stakeholders across the value chain. Covering the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033, this report unveils the market's dynamic landscape, highlighting growth drivers, challenges, and future opportunities. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033, exhibiting a CAGR of xx%.

India Surgical Sutures Industry Market Composition & Trends

The Indian surgical sutures market is characterized by a moderately consolidated structure, with both multinational corporations and domestic players vying for market share. Key players such as Smith & Nephew PLC, Integra LifeSciences Corporation, B Braun SE, Medtronic PLC, Johnson & Johnson (Ethicon Inc), Boston Scientific Corporation, Conmed Corporation, Unisur Lifecare Pvt Ltd, Teleflex Incorporated, and Lotus Surgicals compete fiercely, resulting in a dynamic competitive landscape. The market share distribution is currently estimated as follows: Smith & Nephew PLC (xx%), Johnson & Johnson (Ethicon Inc) (xx%), B. Braun SE (xx%), and others (xx%).

Innovation in suture materials and delivery systems, driven by the need for improved biocompatibility, strength, and ease of use, is a significant catalyst for growth. The regulatory landscape, governed by the Central Drugs Standard Control Organization (CDSCO), influences product approvals and market access. Substitute products, such as surgical adhesives and staples, pose a moderate competitive threat. The end-user profile includes hospitals/clinics, ambulatory surgical centers, and various surgical specialties. M&A activities have been relatively moderate in recent years, with notable transactions like the Healthium Medtech’s Clinisupplies divestment to KKR in December 2022, which was valued at xx Million. This deal highlighted strategic shifts towards strengthening and expanding product portfolios within the surgical sector.

India Surgical Sutures Industry Industry Evolution

The Indian surgical sutures market has witnessed robust growth over the past five years (2019-2024), driven by factors such as rising surgical procedures, increasing prevalence of chronic diseases, improving healthcare infrastructure, and a growing preference for minimally invasive surgeries. The market has experienced a CAGR of xx% during the historical period (2019-2024). Technological advancements, such as the introduction of advanced suture materials (e.g., barbed sutures) and minimally invasive surgical techniques, have further stimulated market expansion. Consumer demand is shifting towards absorbable sutures, owing to their reduced infection risk and faster healing times. The increasing adoption of advanced suture materials and minimally invasive surgical techniques is expected to drive significant growth over the forecast period (2025-2033). The market is expected to maintain a robust growth trajectory, fueled by continued investments in healthcare infrastructure, government initiatives promoting healthcare access, and a burgeoning medical tourism sector. The anticipated market size in 2033 is expected to be xx Million, indicating sustained growth momentum.

Leading Regions, Countries, or Segments in India Surgical Sutures Industry

- By End User: Hospitals/clinics constitute the largest segment, driven by high surgical volumes and advanced medical facilities. Ambulatory surgical centers are witnessing increasing adoption of surgical sutures due to their convenience and cost-effectiveness.

- By Product Type: Absorbable sutures dominate the market due to their superior biocompatibility and reduced risk of infection. Synthetic sutures (non-absorbable) also hold a substantial market share, catering to specific surgical applications requiring prolonged strength.

- By Application: Cardiovascular surgery and orthopedic surgery are significant application segments, accounting for a considerable share of the market due to the high demand for sutures in these procedures. Ophthalmic and neurology surgeries also contribute significantly, with growing demand for specialized suture materials.

Key Drivers:

- Significant investments in hospital infrastructure and modernization across major cities.

- Government initiatives to improve healthcare access and affordability.

- Rising prevalence of chronic diseases requiring surgical intervention.

The dominance of hospitals/clinics in the end-user segment is primarily due to their high surgical volumes and the availability of advanced surgical infrastructure. The substantial share of absorbable sutures in the product type segment stems from their clinical advantages, while cardiovascular and orthopedic surgeries lead in application segments due to higher surgical procedures requiring sutures.

India Surgical Sutures Industry Product Innovations

Recent innovations focus on enhancing suture performance and ease of use. Barbed sutures, for example, reduce the time required for suturing and enhance precision. New biocompatible materials are being developed to minimize tissue reactions and improve healing outcomes. The focus on developing sutures tailored for minimally invasive surgeries has led to the emergence of smaller-gauge and improved handling features. These innovations significantly improve surgical outcomes and patient recovery times.

Propelling Factors for India Surgical Sutures Industry Growth

Technological advancements in suture materials and delivery systems are driving market expansion. Rising disposable incomes and increasing healthcare expenditure are fueling demand for advanced surgical care. Government initiatives to improve healthcare infrastructure and access contribute to the market’s growth. The increasing prevalence of chronic diseases necessitates more surgical procedures, boosting suture demand.

Obstacles in the India Surgical Sutures Industry Market

Stringent regulatory requirements for medical devices can delay product launches and increase costs. Supply chain disruptions caused by geopolitical events or raw material shortages can impact production and availability. Intense competition among established players and new entrants can exert pressure on pricing and profitability.

Future Opportunities in India Surgical Sutures Industry

Untapped markets in rural areas offer significant potential for expansion. The development of biodegradable and smart sutures presents exciting opportunities. Growing demand for minimally invasive surgical procedures will further drive market growth.

Major Players in the India Surgical Sutures Industry Ecosystem

- Smith & Nephew PLC

- Integra LifeSciences Corporation

- B Braun SE

- Medtronic PLC

- Johnson & Johnson (Ethicon Inc)

- Boston Scientific Corporation

- Conmed Corporation

- Unisur Lifecare Pvt Ltd

- Teleflex Incorporated

- Lotus Surgicals

Key Developments in India Surgical Sutures Industry Industry

- August 2023: Healthium Medtech launched TRUMAS, a range of sutures designed to address challenges faced during suturing in minimal-access surgeries. This launch signifies an expansion into specialized suture technologies within the Indian market.

- December 2022: Healthium Medtech Ltd. (formerly Sutures India) sold a stake in its Clinisupplies to private equity firm KKR for xx Million. This divestment reflects a strategic shift towards focusing on core surgical and post-surgical product portfolios.

Strategic India Surgical Sutures Industry Market Forecast

The Indian surgical sutures market is poised for sustained growth driven by factors such as technological advancements, rising healthcare expenditure, and the increasing prevalence of chronic diseases. The market's expansion will be further fueled by the growing demand for minimally invasive procedures and increasing adoption of advanced suture materials. This presents significant opportunities for market participants to innovate and expand their product portfolios, catering to the evolving needs of the surgical sector.

India Surgical Sutures Industry Segmentation

-

1. Product Type

-

1.1. Absorbable Sutures

- 1.1.1. Natural Sutures

- 1.1.2. Synthetic Sutures

-

1.2. Non-absorbable Sutures

- 1.2.1. Nylon

- 1.2.2. Prolene

- 1.2.3. Other Non-absorbable Sutures

-

1.1. Absorbable Sutures

-

2. Application

- 2.1. Ophthalmic Surgery

- 2.2. Cardiovascular Surgery

- 2.3. Orthopedic Surgery

- 2.4. Neurology Surgery

- 2.5. Other Applications

-

3. End User

- 3.1. Hospitals/Clinics

- 3.2. Ambulatory Surgical Centers

India Surgical Sutures Industry Segmentation By Geography

- 1. India

India Surgical Sutures Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.55% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increased Surgeries Owing to Unhealthy Lifestyles and Chronic Diseases; Technological Advances in Suture Design and Applications; Favorable Government Regulations

- 3.3. Market Restrains

- 3.3.1. Needle-related Infections; Increasing Preference Toward Minimally Invasive Surgeries

- 3.4. Market Trends

- 3.4.1. Orthopedic Surgery Segment is Expected to Witness Growth Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Surgical Sutures Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Absorbable Sutures

- 5.1.1.1. Natural Sutures

- 5.1.1.2. Synthetic Sutures

- 5.1.2. Non-absorbable Sutures

- 5.1.2.1. Nylon

- 5.1.2.2. Prolene

- 5.1.2.3. Other Non-absorbable Sutures

- 5.1.1. Absorbable Sutures

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Ophthalmic Surgery

- 5.2.2. Cardiovascular Surgery

- 5.2.3. Orthopedic Surgery

- 5.2.4. Neurology Surgery

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospitals/Clinics

- 5.3.2. Ambulatory Surgical Centers

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. India

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. North India India Surgical Sutures Industry Analysis, Insights and Forecast, 2019-2031

- 7. South India India Surgical Sutures Industry Analysis, Insights and Forecast, 2019-2031

- 8. East India India Surgical Sutures Industry Analysis, Insights and Forecast, 2019-2031

- 9. West India India Surgical Sutures Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Smith & Nephew PLC

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Integra LifeSciences Corporation

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 B Braun SE

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Medtronic PLC

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Johnson & Johnson (Ethicon Inc)

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Boston Scientific Corporat

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Conmed Corporation

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Unisur Lifecare Pvt Ltd

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Teleflex Incorporated*List Not Exhaustive

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Lotus Surgicals

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Smith & Nephew PLC

List of Figures

- Figure 1: India Surgical Sutures Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India Surgical Sutures Industry Share (%) by Company 2024

List of Tables

- Table 1: India Surgical Sutures Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India Surgical Sutures Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 3: India Surgical Sutures Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: India Surgical Sutures Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 5: India Surgical Sutures Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: India Surgical Sutures Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: North India India Surgical Sutures Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: South India India Surgical Sutures Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: East India India Surgical Sutures Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: West India India Surgical Sutures Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: India Surgical Sutures Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 12: India Surgical Sutures Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 13: India Surgical Sutures Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 14: India Surgical Sutures Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Surgical Sutures Industry?

The projected CAGR is approximately 4.55%.

2. Which companies are prominent players in the India Surgical Sutures Industry?

Key companies in the market include Smith & Nephew PLC, Integra LifeSciences Corporation, B Braun SE, Medtronic PLC, Johnson & Johnson (Ethicon Inc), Boston Scientific Corporat, Conmed Corporation, Unisur Lifecare Pvt Ltd, Teleflex Incorporated*List Not Exhaustive, Lotus Surgicals.

3. What are the main segments of the India Surgical Sutures Industry?

The market segments include Product Type, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 184.73 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Surgeries Owing to Unhealthy Lifestyles and Chronic Diseases; Technological Advances in Suture Design and Applications; Favorable Government Regulations.

6. What are the notable trends driving market growth?

Orthopedic Surgery Segment is Expected to Witness Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Needle-related Infections; Increasing Preference Toward Minimally Invasive Surgeries.

8. Can you provide examples of recent developments in the market?

August 2023: Healthium Medtech launched TRUMAS, a range of sutures designed to address challenges faced during suturing in minimal-access surgeries.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Surgical Sutures Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Surgical Sutures Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Surgical Sutures Industry?

To stay informed about further developments, trends, and reports in the India Surgical Sutures Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence